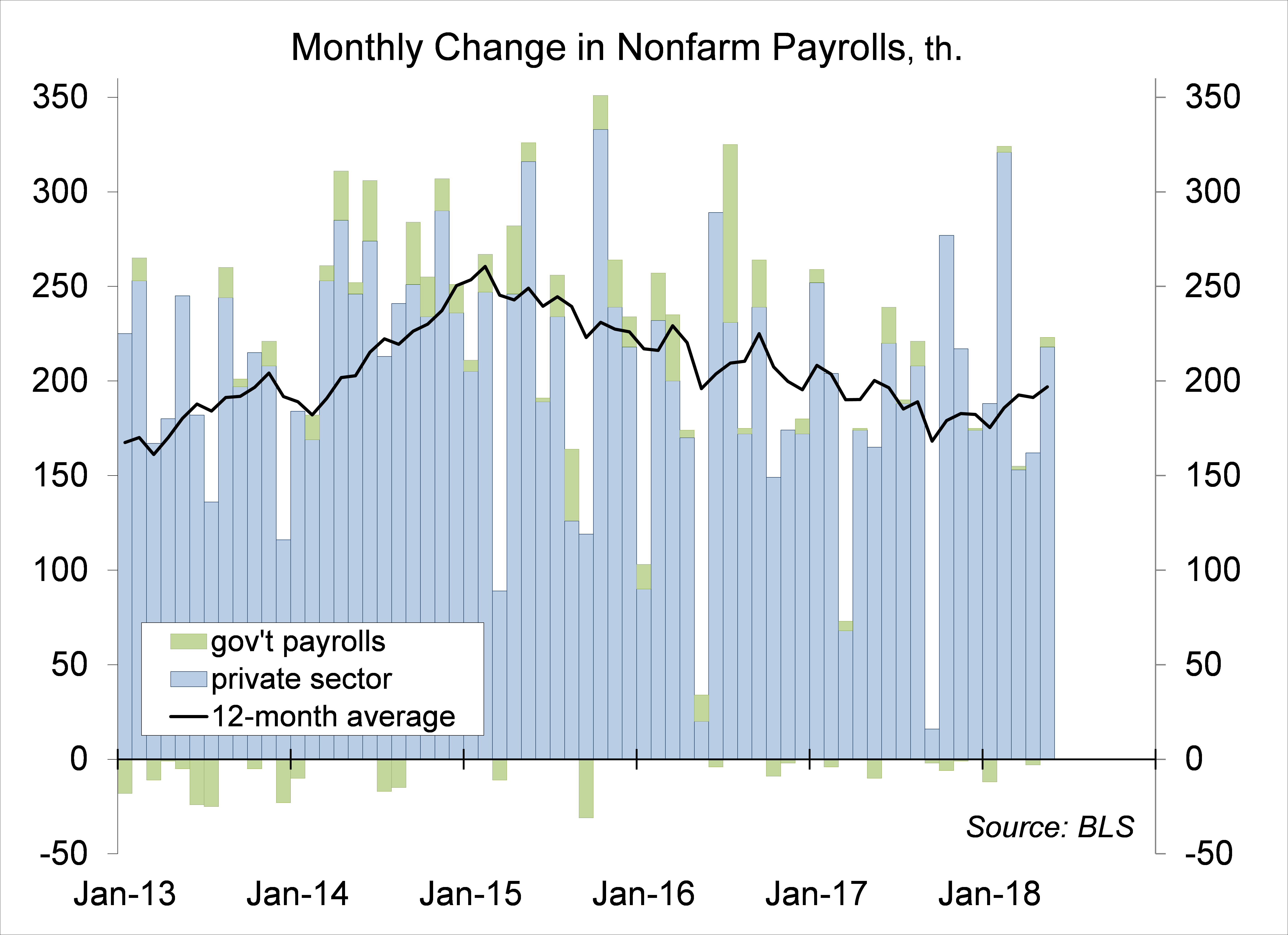

Nonfarm payrolls rose by 223,000 in the initial estimate for May, stronger than expected, but not statistically outside of the moderately strong trend of the last year. We need a little less than 100,000 jobs per month to absorb new entrants into the workforce. Hence, it’s no surprise that the broad range of data has indicated a further tightening in labor market conditions. The unemployment rate, 3.8% in May, is trending lower. Measures of underemployment are falling. Obviously, that can’t go on forever. Wage pressures still appear to be moderate overall, although salary increases are more apparent for skilled labor positions, and we can probably expect faster wage growth in the months ahead. This creates a dilemma for the Fed.

There’s always a fair amount of noise in the monthly payroll estimate (as reflected in the chart below). Seasonal adjustment can be tricky, but the underlying trend has remained relatively strong this year. We know that demographic changes (the aging of the population) imply significantly slower growth in the labor force than in past decades (when the baby-boomers were entering, female labor force participation was rising, and immigration was higher). Job growth has to slow as the U.S. runs out of people to hire. That hasn’t happened yet, as there appears to have been greater slack than previously thought. Fed officials fear that the unemployment rate has fallen below a level consistent with normal underlying frictions in the labor market. Initial claims for unemployment benefits, for example, have been trending at multi-decade lows (impressive, in that the labor force is twice the size that it was in the late 1960s).

Click here to enlarge

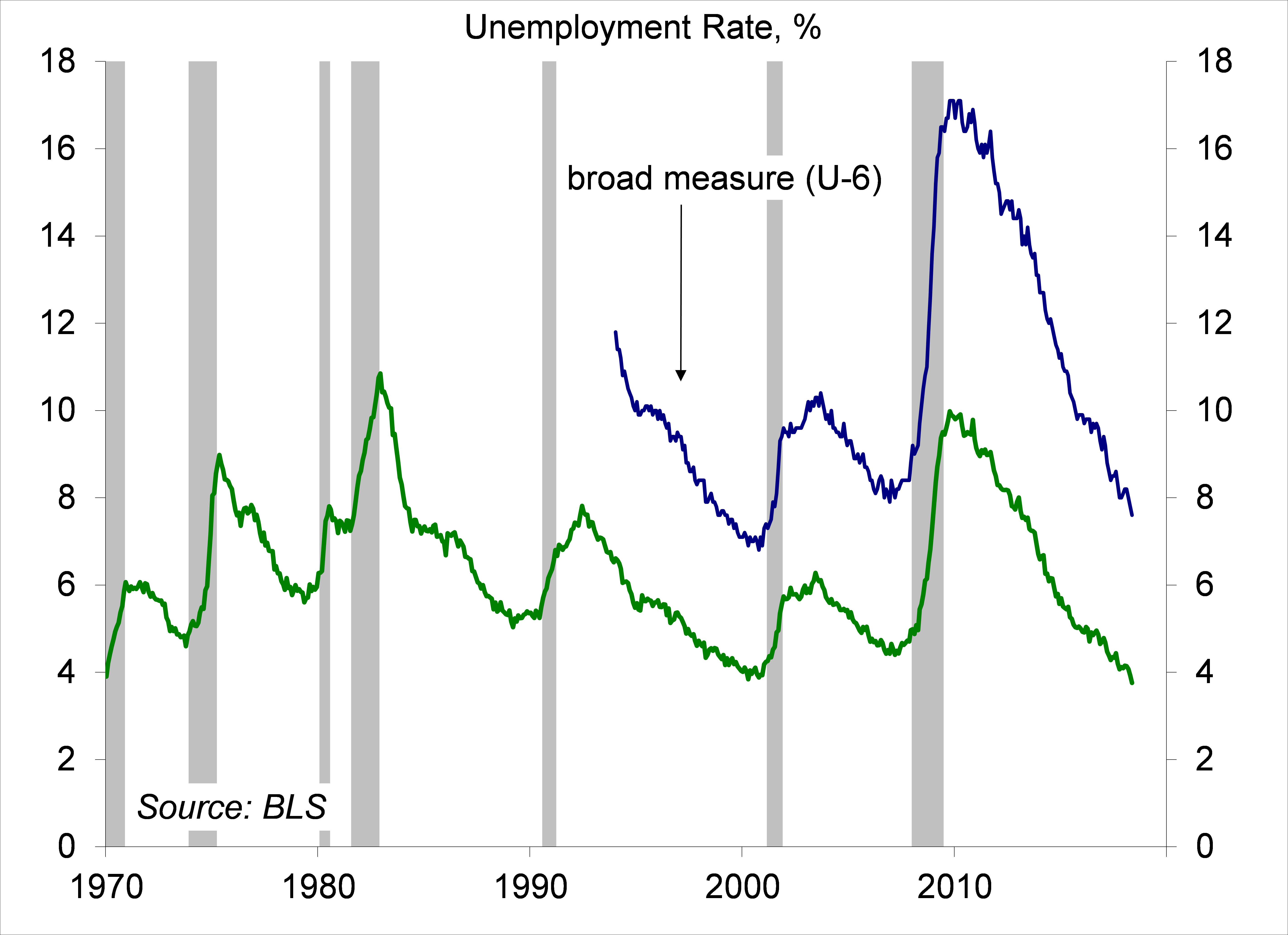

Nobody knows what the natural rate of unemployment is. In the past, unemployment rates of around 4% have been associated with pending recession. That’s because the Fed’s attempts at slowing the economy typically result in a harder landing than expected. Alternatively, the central bank may have waited too long to tighten and was forced to move more aggressively later on (this is the main argument behind the Fed’s current path of gradual rate hikes).

Click here to enlarge

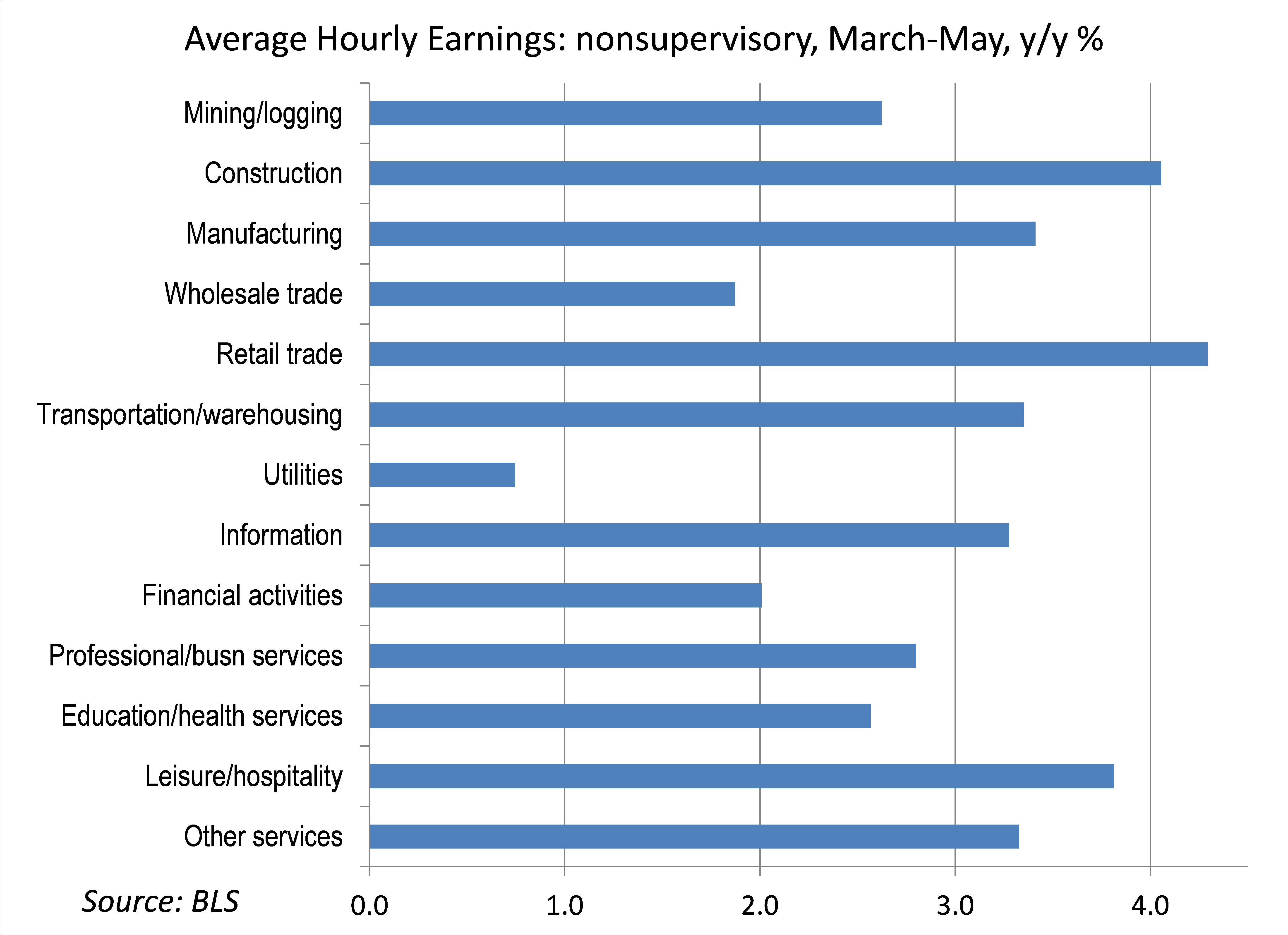

Average hourly earnings are not the best measure of labor costs pressures. However, the trend for production workers is higher in a number of industries that are currently showing strength. The Fed’s most recent Beige Book noted that “shortages of qualified workers were reported in various specialized trades and occupations, including truck drivers, sales personnel, carpenters, electricians, painters, and information technology professionals.” Firms are responding by raising compensation packages (some increase in salaries, but also hiring bonuses, more time off, and other perks).

Click here to enlarge

There is an argument for letting the labor market run. Faster wage growth would facilitate a reallocation of labor, further reduce underemployment, increase productivity growth, and create incentives for in-house worker training, fundamentally transforming the economy (as we saw in the late 1990s). For the Fed the key questions are whether firms will be able to pass higher costs along and what the risks are of not acting sooner.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James