Weighing the Week Ahead: Is it Time to Worry About a Trade War?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is light. Most of the “financial” news flow relates to non-core stories. Of the various geo-political themes, there is one that is most significant for investors. Expect pundits to be asking:

Is it time for investors to worry about a trade war?

Last Week Recap

In my last edition of WTWA I suggested that investors were too focused on the shifting geopolitical winds. For most, it was better to ignore them. The chart of the week’s events illustrates the value of that advice. Stories about Italy, North Korea, and China had twists and turns leaving the market unchanged. If you tried to trade them, you probably lost money. Wade Slome calls it S.T.I.N.K. and invokes the wisdom of Yogi Berra. Some will wonder whether this week’s theme contradicts last week’s. No. While trade talk progress ebbs and flows, the overall issue merits consideration. I go into more detail in today’s Final Thought.

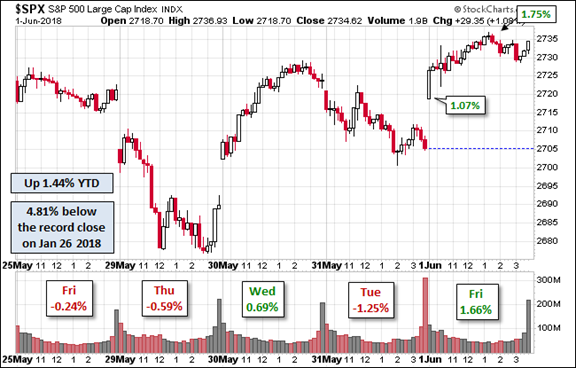

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market rose 0.5% with a trading range of about 2.5%. The pattern is quite interesting, including several gaps from “fresh” geopolitical news. As we can see, these big stories made little difference by week’s end. I summarize actual and implied volatility each week in our Indicator Snapshot section below. Volatility is back into the long-term range.

Noteworthy – Debt and Auto Sales

A few years ago, a conversation with a top salesperson at a large auto dealer provided some great information. Nearly all their buyers of new pickup trucks were under water on their current vehicle. The dealership was trying to convince them to adopt a 3-year (or at worst, 4-year) buying cycle and the loans were five and six-year loans. The popular rebate structure allows the rebate to be treated as a down payment and makes the whole deal work. Cars are sold according to payments, so stretching time out is helpful for sales. With continuing high auto sales, investors should take a deeper look. CNBC’s Phil LeBeau does his typical nice job with this story. Here are three key elements:

- The new standard monthly payment is now $523, up $15 from last year.

- The average loan is a record high of $31,453.

- The average loan length is now five years and nine months.

On the positive side:

- Fewer delinquencies, 1.86% for thirty days.

- Fewer subprime loans – down 8.4% for subprime and 14.1% for deep subprime.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The Good

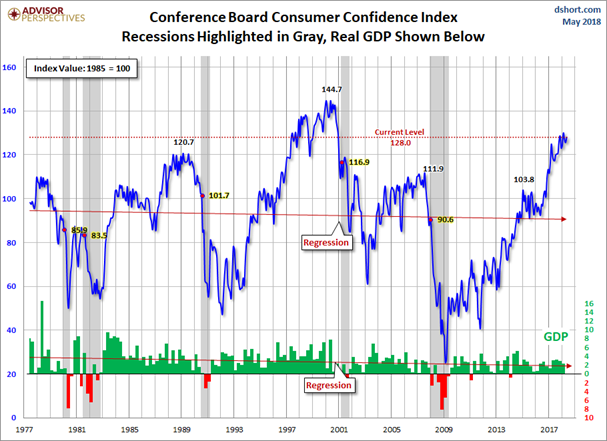

- Consumer confidence hit 128 on the Conference Board measure. While this was slightly below the expectation of 128.2, it is difficult to be negative about this level. We can see this from the Jill Mislinski update.

- US – North Korean summit. On again. Here is some objective background for those watching closely.

- The beige book, intended to provide some anecdotal color for the Fed’s decision, was upbeat about current economic conditions.

- PCE prices, the Fed’s favorite measure of inflation, remained at the expected 0.2% level.

- Rail traffic remains strong. Steven Hansen’s focus on the most important cargoes enhances this indicator.

- Personal income (up 0.3% as expected) and spending (up 0.6% vs 0.3% expected) signal continuing consumer-driven economic strength.

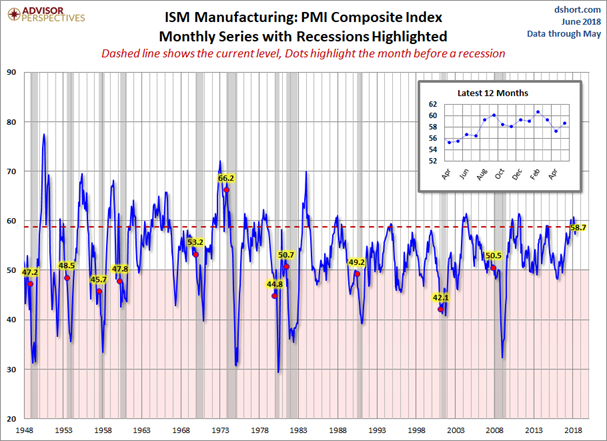

- ISM manufacturing was hit 58.7, up 1.4 points from April. Brian Wesbury cites the consensus beat, and notes that this is the best year since 2004. Jill Mislinski’s chart nicely illustrates recent results as well as the long-term perspective.

-

Employment

- Initial jobless claims were 221K, below expectations of 227K and the prior week’s 234K.

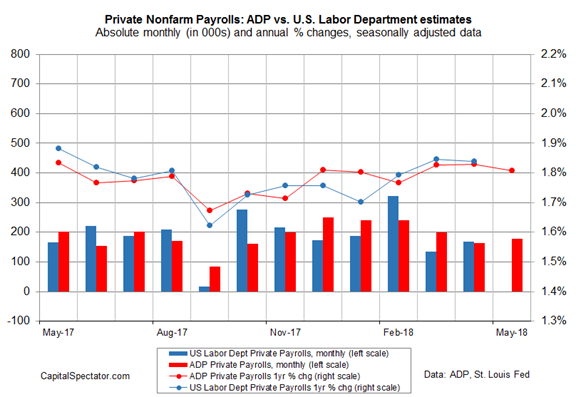

- ADP private employment — a slight miss but supportive a the continuing moderate trend (Capital Spectator).

The Bad

- Pending home sales declined 1.3% versus and expected increase of 1.0% and a March gain of 0.6%. Calculated Riskhas the details.

- Slow U.S. Wage Growth despite the apparent tightening in the labor market. Nick Bunker (Equitable Growth) discusses the viewpoints.

-

Trade talks

- China. News breaking this weekend as talks continue.

- Europe. Voice of America.

- North America (Canada Tariffs)

The Ugly

Cell phone spying near the White House. I remain concerned over hacking and security issues. During a time when government spending has been under pressure, this is the kind of line item that is easy to postpone.

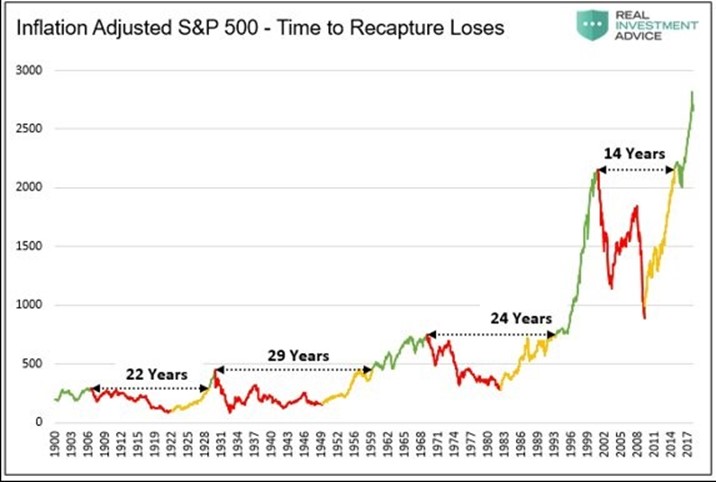

The Silver Target

About a year ago I asked for reader suggestions about improving WTWA. The comments were very helpful, and I have implemented many of them. I had hoped to do the Silver Bullet feature as a standalone piece, but that has not worked well. More on that later.

Meanwhile, I am testing a new idea. I am going to post a chart that I do not like, a possible target for one trying to earn a Silver Bullet award. Readers may test their own skill and share ideas in the comments. I will follow up with my own take in the next post. I am also considering a podcast on charting, since it is so difficult to do in written form. I will focus on prominent sources, and I invite responses.

The thesis of this chart, drawing upon several of those of the bearish persuasion, is that it is important to pick the right time to invest. Go to the original source for more background, and share with all of us what you think about the chart.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

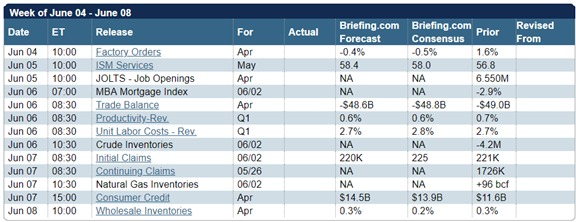

The Calendar

The economic calendar is modest. The ISM services index is the biggest indicator with a leading quality. The JOLTS report is important to the Fed’s assessment of labor market tightness and under-appreciated by markets. There is more interest in trade data, but the reports do not provide much useful current information.

The Fed is in a quiet period before the next meeting, but don’t worry. There is no shortage of other Washingtonians ready to fill the gap.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

There is little economic news leaving the door wide open for pundits. In the absence of any sports or social fluff stories, I expect many to be asking:

Is it time to worry about a trade war?

While this story has been in the headlines for months, there has been a change in the intensity of interest. Until now, various meetings were scheduled, negotiations were underway, progress was noted, and the worst might be avoided.

We have now moved to a stage where actual policy implementation is taking place. What does it mean for investors?

Here are a few ideas. There is some truth in each, making this an exceptionally challenging policy question.

- It is past time to deal with currency manipulation, dumping, and theft of intellectual property.

- U.S. companies deserve fair competition with the rest of the world.

- U.S. consumers benefit from low prices, even if they are artificially low because of foreign subsidies.

- The U.S. can compete with high-tech products and services, ceding low-cost manufacturing to others.

- Most products involve a complex mix of services from several countries. Parsing the differences is challenging and not meaningful.

- U.S. exporters benefit from free trade and would suffer from retaliatory tariff increases.

- All countries benefit from free trade (in general). Rules are needed.

As usual, I’ll save my overall personal conclusions for today’s Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

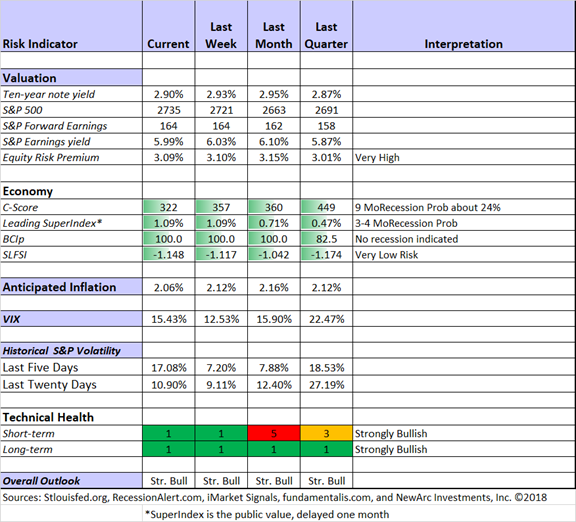

The Indicator Snapshot

Short-term trading conditions continue at favorable levels, much improved from the month-ago data.

A notable feature of the chart is that we recently increased the nine-month recession odds to a chance of 25%. While this is significantly higher than it has been during the long stock rally, it does not yet represent a real threat. Instead of thinking of the odds as higher than before, we must keep in mind the continuing evidence that a near-term recession is unlikely. The odds are only slightly higher than the long term average.

That said, we watch this quite closely and plan to reduce position sizes if the risk grows much larger.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian provides his conclusions about danger levels in earnings yield, considering when asset allocations might need a review.

Guest Sources

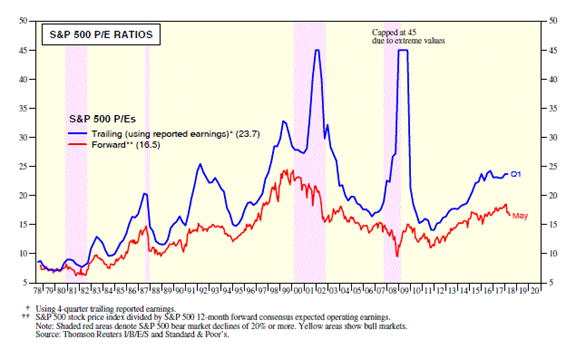

Ed Yardeni generally agrees with Brian. He prefers forward earnings to trailing versions when no recession is on the horizon. He notes that in the post-1990 period of low inflation, the average forward earnings multiple was 25.5. Right now it is 16.5.

The forward P/E based on estimated earnings has been lower than the multiple based on four-quarter-trailing earnings because analysts are looking forward, not backward. There’s one major flaw with the forward valuation approach: Analysts’ earnings estimates tend to be unrealistically inflated in advance of recessions because analysts collectively never see recessions coming until it is too late. Once they do, they slash their earnings estimates at the same time as reported earnings take a dive, and share prices take an unanticipated hit. Conversely, the flaw with P/Es based on trailing earnings, which produce the higher multiples of the two approaches, is that they tend to turn bearish much too early in a bull market. The higher the multiple, the more likely it is to be deemed unduly heady as a bull market continues.

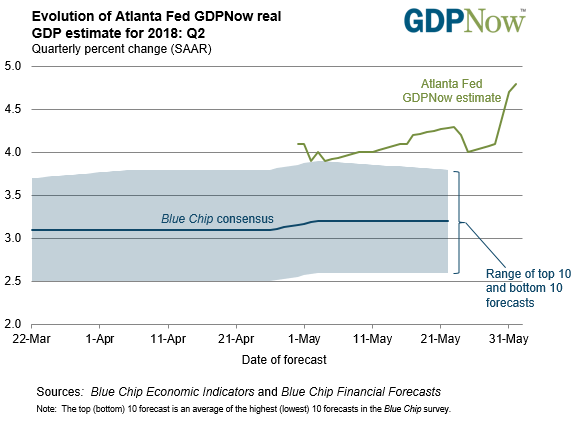

The Atlanta Fed GDPNow (via the Daily Shot from the WSJ) reflects the strength of current economic data.

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we asked readers about their odds of trading success, reviewing results and comments from several leading experts. We also discussed some stock ideas and updated the ratings lists for Felix and Oscar, this week featuring the Russell 1000. Blue Harbinger is back on the job as editor of this information and ringleader for the group.

There is often some insight for non-traders as well. If you have not visited the series recently, you might wish to take a look.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Dr. Brett Steenbarger’s Forbes article, The Growing Crisis in Modern Finance. Drawing upon interviews with top mathematicians working in financial markets, he explains the significance in his customary clear language. The topic is technical, but you will never see a better explanation. He also quotes his interview subjects.

Bailey: Yes, it is very distressing that after all of the research published by ourselves and many others, numerous unproven and technically dubious techniques (“head and shoulder patterns”, “b-waves”, “technical indicators”, “support levels”, etc.) are still widely featured in the financial press, and thus presumed by millions of consumers and professionals alike to be the “scientific” way of handling one’s investments. Our own research has amply confirmed that these methods do not work. For example, in our recent study of market forecasters, we found that those forecasters who rely on charting, technical analysis and/or wave analysis averaged only 44% correct predictions, which is even less than the disappointing score (49%) achieved by the full collection in our study. It may well be that the vast majority of persons featuring and promoting these techniques do not realize that they are scientifically ill-founded, but that does not excuse those who do.

And

Lopez de Prado: Statistical tests assume a certain false discovery probability. In the context of investing, that’s the probability of saying a false strategy will make money. That probability is generally accurate if the test is dispensed only once. However, if a researcher dispenses 20 times a test with let’s say a 5% false positive probability, it is all but guaranteed that one false strategy will be produced. In modern finance, researchers conduct millions of tests. The implication is that most discoveries in finance are likely false, and that most investors are putting their money on losing strategies. This methodological error is called selection bias under multiple testing. One reason financial researchers get away with this scientific fraud is because we don’t have laboratories where discoveries can be challenged based on new evidence. It will take decades to collect the new evidence needed to debunk each of these claims, and by then new false claims will be marketed to investors.

Stock Ideas

Individual investors seeking high-quality research on their stock holdings and ideas already use the many resources at Seeking Alpha. Just in case you are not following the Today’s Editors’ Picks series, take a look. You will definitely find ideas that you would otherwise have missed.

Chuck Carnevale continues his analysis of valuation in many of the leading dividend stocks. This week he takes up Kimberly-Clark (KMB) and 3M (MMM). For the full benefit, be sure to watch his explanatory videos.

Annuity sales companies? Barron’s sees Lincoln National as a bargain, with sales on the rebound.

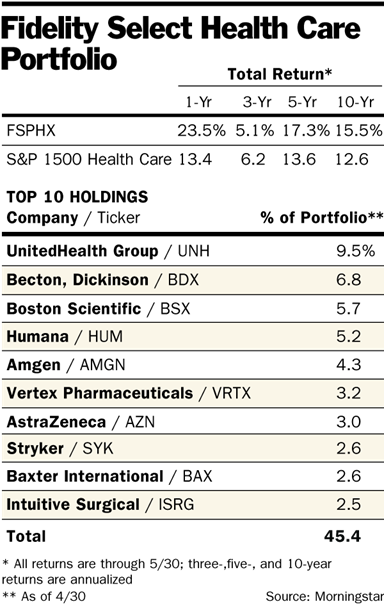

Health care stocks? A look inside Fidelity’s portfolio (Barron’s).

Energy stocks? Morningstar examines valuations in the wake of energy price declines.

Internet-related stocks? Half of the world will be on the internet this year. Mary Meeker’s annual report provides ideas about what it all means. There are nearly 300 slides, so settle back with some morning coffee.

Outlook

David Templeton (HORAN Capital Advisors) sees potential in the second half of 2018. He notes that until the yield curve inverts, a flattening process is “sweet spot” for stocks. Check out his charts and analysis. His explanation of why inflation will push long rates higher, matching the Fed moves on the short end, is excellent.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich has expanded his excellent series for financial advisors (and serious individual investors) to include some podcasts. This week I especially enjoyed his post on financial literacy and risk. Adult Americans got only half of the questions right. Read the entire post for a clear discussion of the implications.

Abnormal Returns is always worth reading, with many links on an array of interesting topics. Wednesday the focus is onpersonal finance. Among many good choices, I especially appreciated Jonathan Clements’ discussion of annuities. He describes four types that can make sense for investors. This is great reading for those shopping in this market.

Morningstar has 7 Ways to Improve Your Credit Score. Some are very easy and can save you money on future loans.

Watch out for…

Within two years, the reward for mining new Bitcoin will be cut by half. This will be the third halvening. What will this mean for the price?

Changes in MLP policies. Simon Lack takes up the latest changes in FERC rules and what they can mean for you.

Final Thoughts

Is it time to worry about a trade war? For investors, not yet. For citizens, yes.

Free trade is an issue that differs dramatically in two ways:

- First-order impacts are very clear and immediate. The impact is on cohesive industry and worker groups. Nations emphasize their role as exporters.

- Other impacts are delayed, nuanced, and difficult to measure. Retaliatory tariffs have gradual impacts – inflation, producers (think soybean farmers) leaving the business, Fed rate increases in response to price pressures, and eventually a recession.

Investors cannot profitably plan now for these effects, since they will take many months or even years to show up. Bryan Caplan’s excellent The Myth of the Rational Voter describes this issue as one with the biggest opinion gap between economists and the population as a whole. (Wiki summary here). For many years it was as popular theme for many Democrats, since it played well to their base. The Trump Administration policy aims at the same base and had engendered significant opposition from mainstream Republicans.

As a citizen, feel free to agree with the logic behind an American First approach, but be prepared to accept the resulting costs.

Immediate Impacts

In past posts I cited sources suggesting that the proposed US/China tariffs implied a 0.5% hit on US GDP and a 1.0% cost for China. These are major losses, but do not include the impacts of similar tariffs and retaliation from US friends in North America and Europe. This puts it on the watch list of serious worries, where I continuously monitor effects.

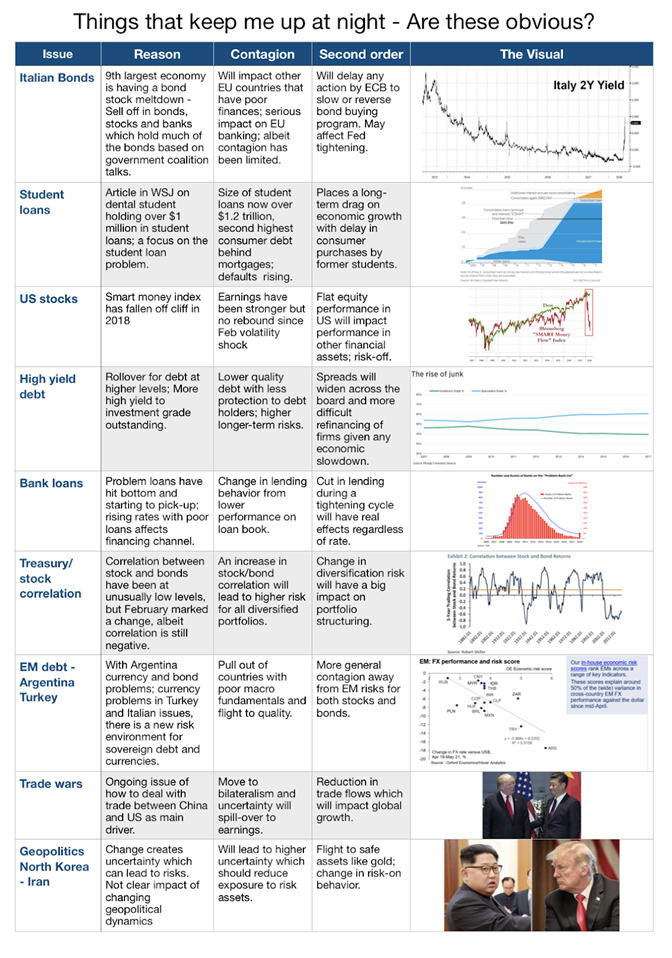

We might compare this with other worries. Mark Rzepczynski has compiled these into an excellent visual, summarizing the key points for each.

I am truly sorry that Mark is losing so much sleep! I do not see important, near-term consequences from any of these items. Trade wars is the closest to a current issue. I am resisting the temptation to analyze all of them here. In general, we should be wary of speculation about relationships and the idea that good times must become bad (right away).

Please contrast this with the colorful, witty, and sage observations from Alan Steel. How he gets from the need to reboot your router to his final market analysis is well worth reading. I am trying to find the smallest taste I can to convey, but not spoil, the story.

Once again, that’s 9.6%, folks, over the last 90 years.

And that wonderful level of investment return has happened during rampant global geopolitical unrest, the Great Depression, the economic recessions of 1956, 1961, the early 1970s, 80s, 90s and 2000s, (not to mention the subprime mortgage crisis of 2008), inflation/deflation/stagflation, the Cuban missile crisis, some big and several small wars, and Queen Elizabeth owning 30 corgis.

Despite all that drama and the worries that went with it, alongside the ridiculously inaccurate predictions of celebrity bear market commentators from Joe Granville to the Roubinis, Dents and Edwards of late, and the continual weakness of Sterling over the 90 years since 1928, the return from US equities for UK based investors would be much higher than the 9.6% per annum quoted by Carlson.

And So, We Have a Choice…

We can believe our routers to have Orwellian wiring, cringe at tomorrow’s hemlock-laced headlines, and succumb to our insidious biaseseses – just like when you notice a sudden preponderance of the type of car you want to buy, if you’re looking for signs of trouble you’re going to start seeing them everywhere.

We see what we want to see. There is an important lesson for the individual investor.

Do not attempt to see too far into the future!

You cannot do it, and neither can anyone else.

No one should base today’s investment decisions on something they expect to happen within the next ten years. Will there be a recession? Sure. Does that mean you should sell stocks now? No. It means that you should monitor the economy and your asset allocations, thinking about the attractiveness of various sectors. You can do it yourself by reading WTWA.

A Small Rant

Please forgive a little rant. Each week I see scores of articles that are selected for publication based upon attractiveness and written by someone with an axe to grind. The articles bearish on stocks are most frequently from those selling bonds, gold, or annuities. Here is an example from this week (properly identified as an opinion piece):

Opinion: The next U.S. recession likely will be wok-shaped: shallower and longer

This is an amazing prediction, meeting the key elements of poor forecasting: non-specific as to timing and size and very difficult to grade in the aftermath.

Or how about this quote:

To be fair, a poll we conducted among sell-side economists and strategists suggests that a U.S. recession over the next three to five years has now become consensus — even though markets do not seem to be pricing in this risk, judging by risk spreads and volatility.

How can one disagree? Sheesh! (TM OldProf exclamation). When we cannot even predict recessions more than a year in advance, the market is supposed to be pricing in risks seen by these bond salesmen?

This could be a crucial moment for investors who still need some portfolio growth. Things are great right now but could change quickly. You want to enjoy the remaining part of the bull market, but you must have the right risk controls in place. The popular media will not help you. My free paper on the Top Investor Pitfalls lets you make a self-assessment about flying solo. Just send a note to main at newarc dot com. We will happily send some free resources and provide a (no-pressure) consultation if you wish.

I’m more worried about:

- Trade policy. The chances for friendly solutions seem to be getting worse. I am hoping for improvement.

- Over-reaction to volatility. People see it as scary. It is not. Volatility is a coincident or trailing indicator and current levels are at historical norms.

I’m less worried about:

- North Korea. Skepticism about the upcoming talks remains. I am aware that my concern on this topic has shifted often – just like the news. Let’s see how it plays out.

- Technical market concerns. Those watching charts got further relief last week. I am told that there was a bear trap and a reversal at an important level. The idea of dip-buying has been reinforced. My main interest in this is that individual investors are not led astray by temporary market reactions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits