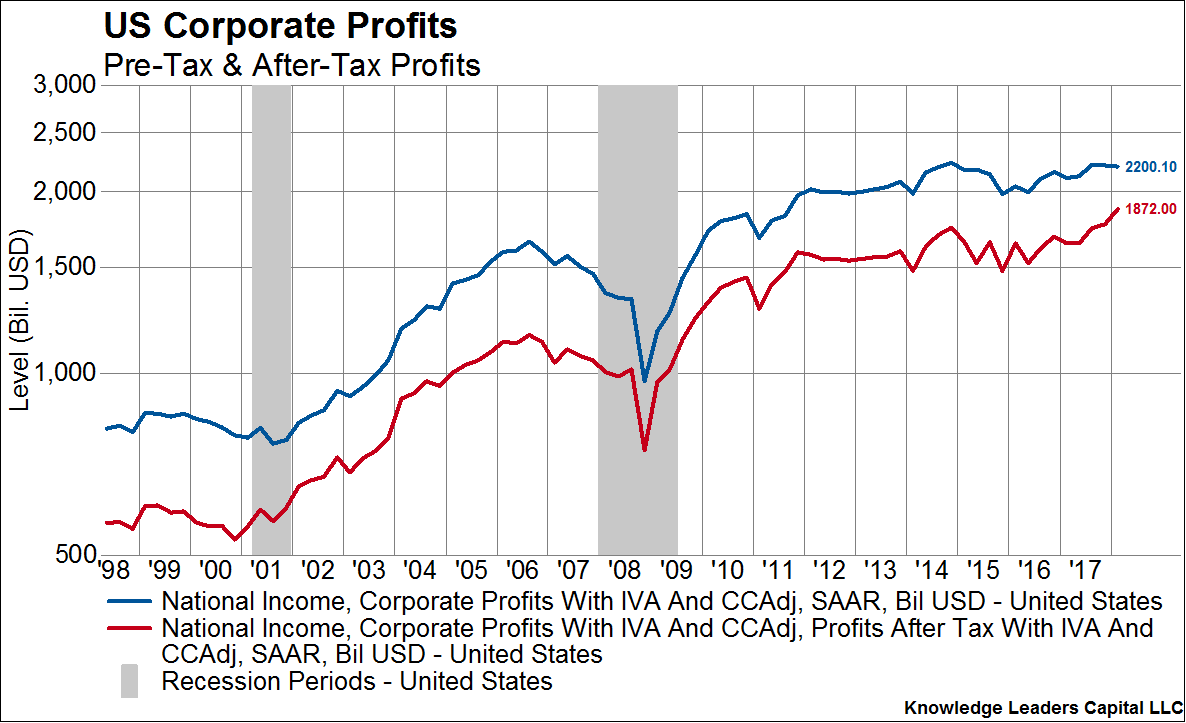

Yesterday we got the latest glimpse into US corporate profitability. Depending on the series observed, corporate profits are either flat-lining or rising. Before-tax corporate profits, the blue series in the chart below, are actually net down by $32 billion from the peak in 2014. Yet, after-tax profits are up about $130 billion from that same year. Of course, the recently enacted tax cuts explain the divergence here.

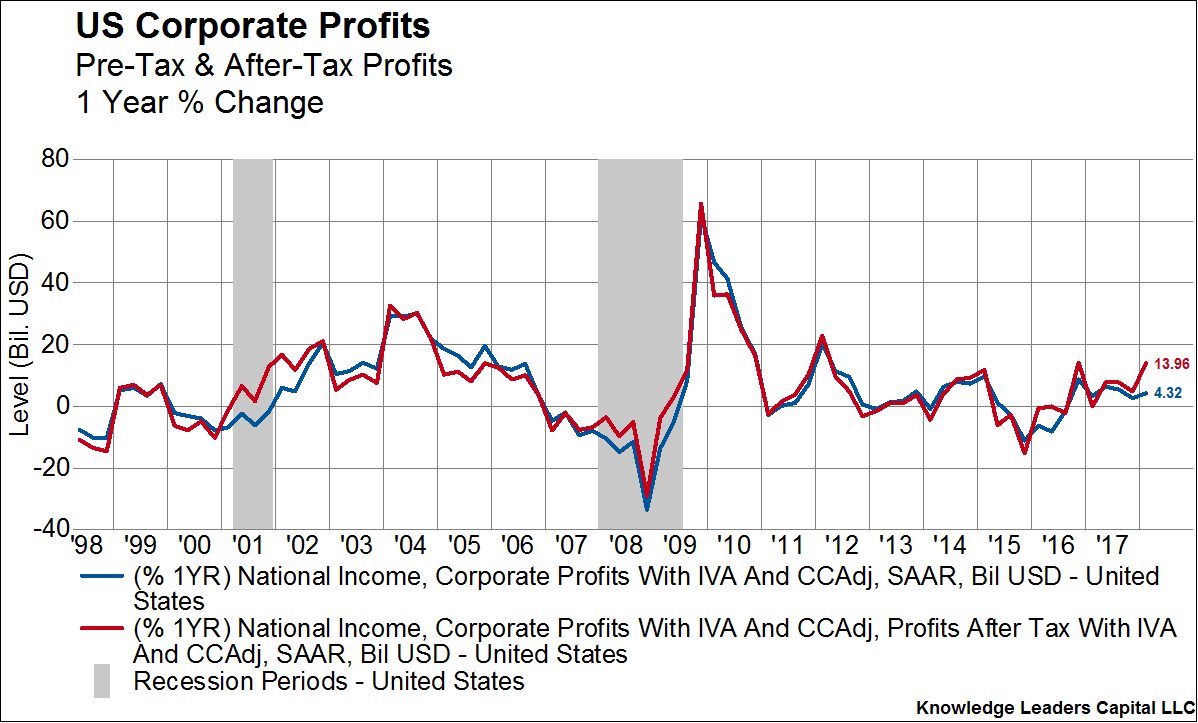

When looking at year-over-year growth rates, the divergence is more easily observed. Pre-tax profits are up about 4.3% from a year ago while after-tax profits are up almost 14% from a year ago.

Both series seem to confirm that peak profit margins for this cycle have come and gone. Pre-tax profit margins peaked in 2014 at just under 13% and now hover slightly over 11%.

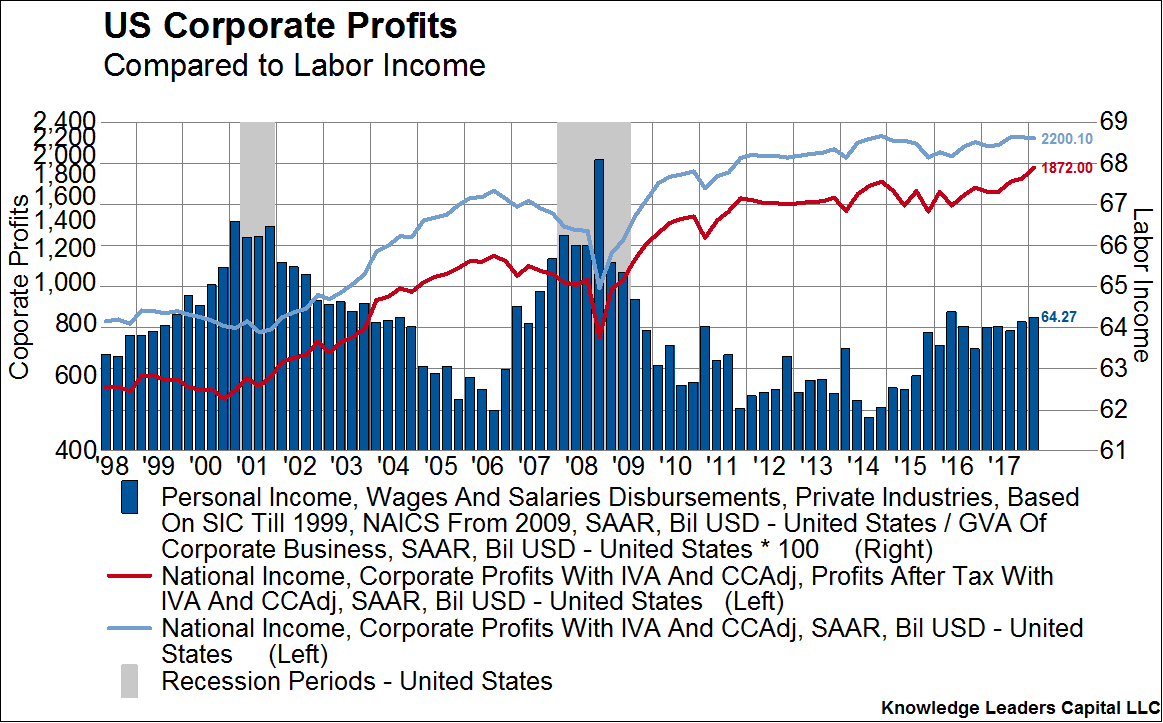

With labor income as a share of gross value-added rising (blue bars below), it is likely the signal from pre-tax profits is the correct one. Labor’s share of income has ticked up from about 62% of gross value-added to a bit over 64% since 2014, helping explain the contraction in pre-tax profit margins.

The Trump tax cuts have certainly provided a one-time boost to the level of corporate profits which will linger in the data for another three quarters. But, by the first quarter of 2019 the effect will be gone and after-tax profit growth will converge on pre-tax profit growth. If the tight labor markets continue to pressure the share of national income going to workers, it is likely profit margins continue to contract in a typical late cycle fashion. Beware of the apparent divergence in corporate profits. It won’t last long.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital