In observing the equity markets over the last several weeks, we cannot help but be reminded of the Jimmy Cliff song, “Sitting Here in Limbo”, which was famously covered by Jerry Garcia. The first two lines go like this:

“Sitting here in limbo, like a bird without a song

Sitting here in limbo, but I know it won’t be long”

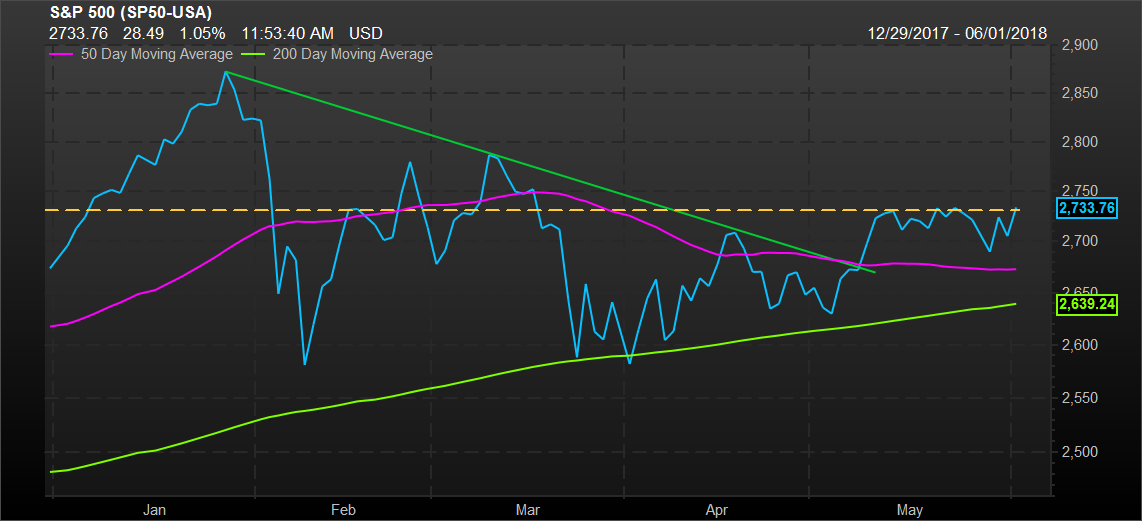

As investors, it does feel like we are in limbo, stuck between the push of higher growth and employment and the pull of higher inflation, higher rates, and policy risk. And and the end of the day, despite quite a lot of directional volatility so far this year, the S&P 500 trades at the same level as it did back on January 4th. But, it’s not just the level of stock prices that seem to be stuck in limbo, internal measures of stock market breadth are also stuck in this sort of no-man’s land.

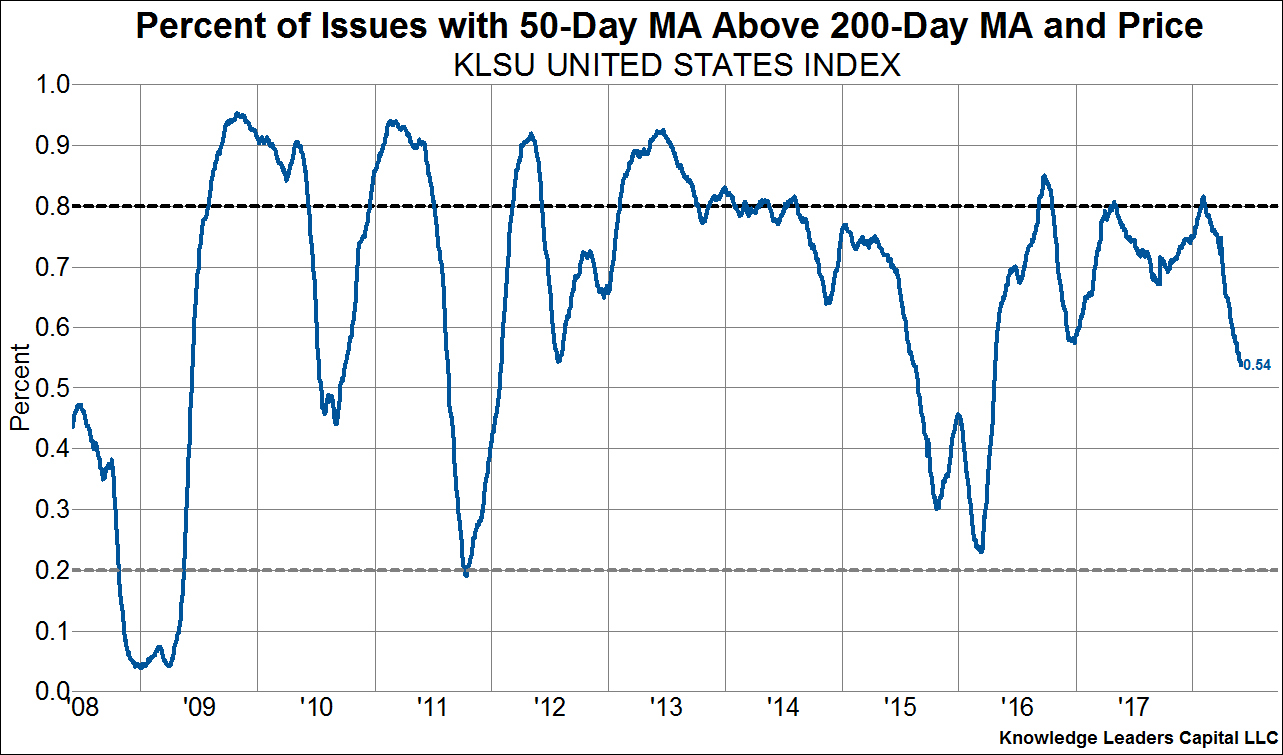

For example, when we look at a simple indicator of the percentage of stocks in uptrends – those with their 50-day moving average price that is higher than their 200-day moving average price – we observe a reading of 54% that looks to be falling quickly towards 50%. In other words, when we peak under the surface, only about half of US stocks are in uptrends. But is it even important? It turns out, yes.

The next table below shows the conditional forward returns and hit rate of positive returns when the market is in a state of agreement (most all stocks are in either uptrends or downtrends) compared to when the market is in a state of limbo (when the percentage of stocks in uptrends resides between 20%-80%). Across all time horizons, forward returns and the hit rate of positive returns is the strongest when investors are in agreement about the ugliness of stocks – when the percent of stocks in uptrends drops below 20%. When investors are in agreement about the attractiveness of stocks – when the percent of stocks in uptrends is greater than 80% – forward returns and the hit rate of positive returns ranks second across almost all time horizons. When investors are in a state of indifference – as they are now – forward returns and the hit rate of positive returns are the weakest.

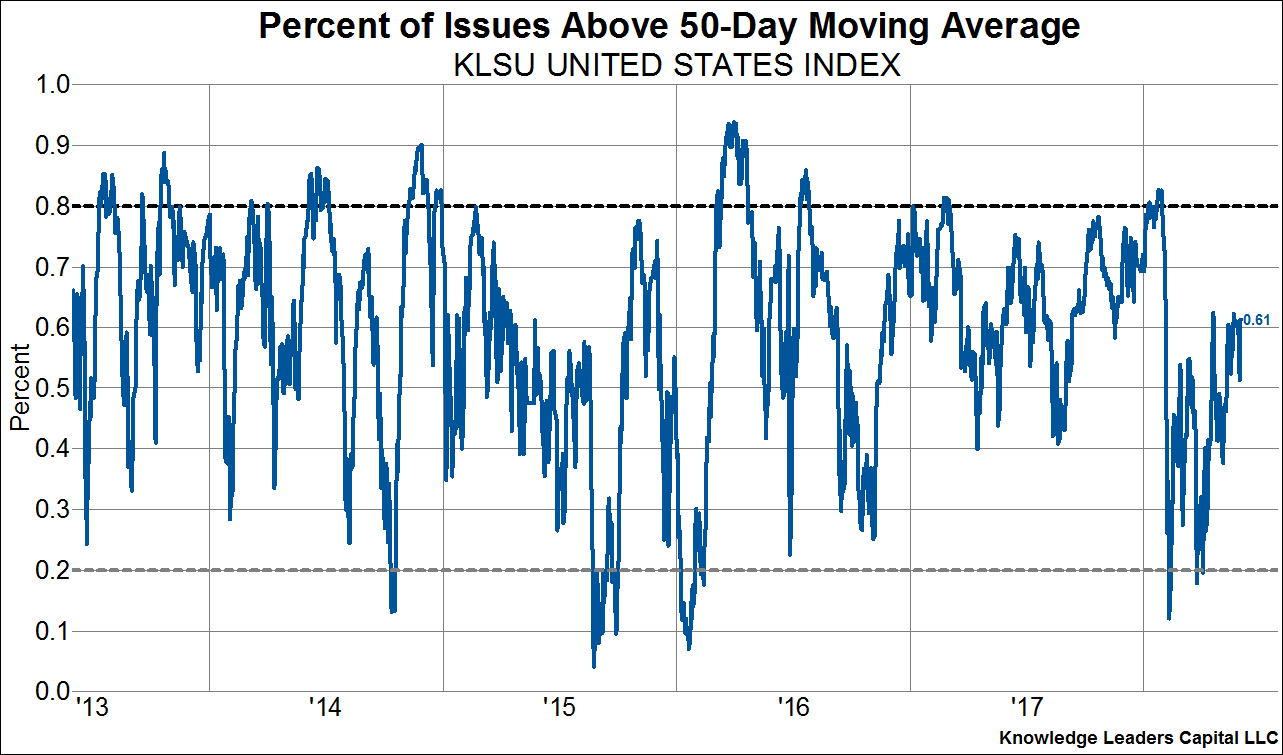

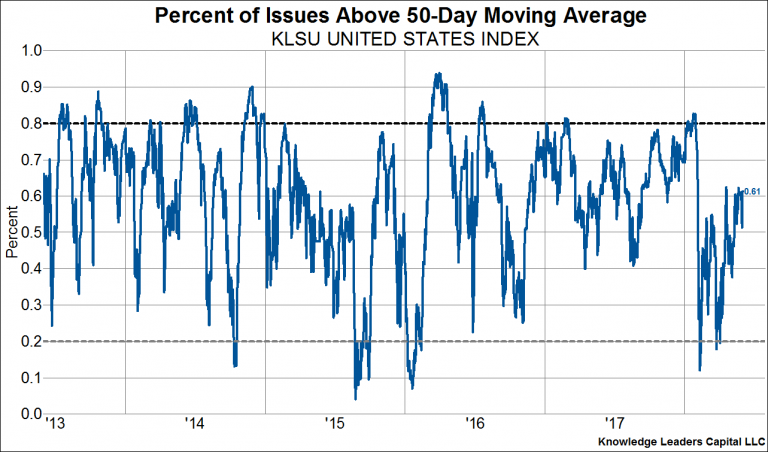

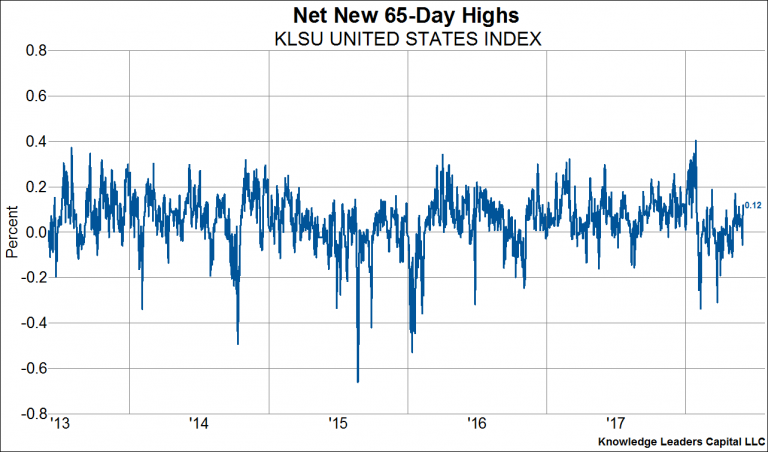

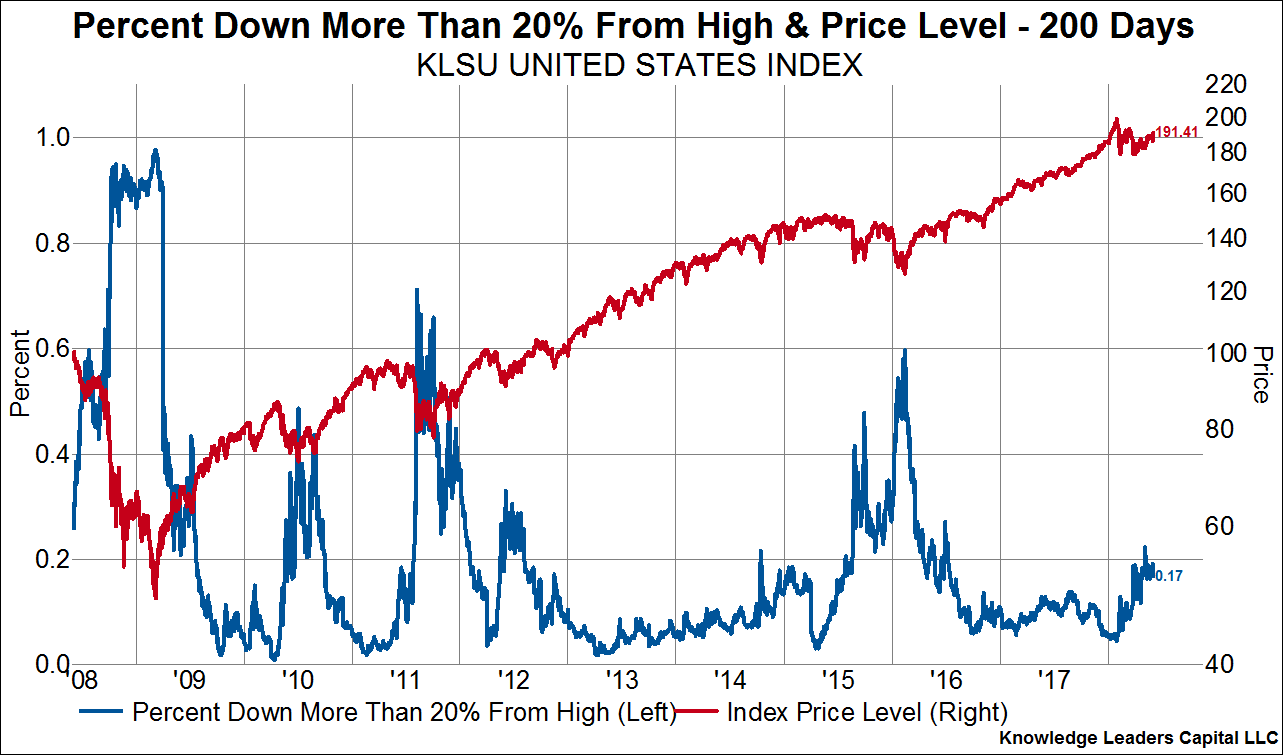

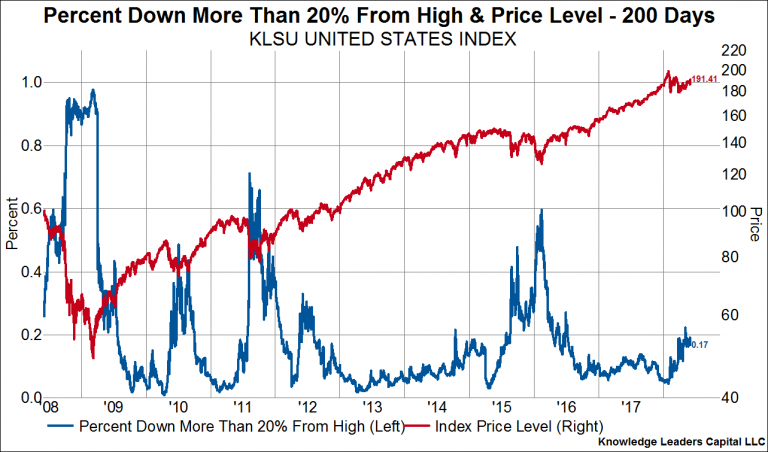

We also see indications of investor indifference in other measures, as the next three charts show. For example, despite the rally off of the lows earlier in the year, only about 60% of stocks are trading above their own 50 day moving average (chart 1). Furthermore, only a net 12% of stocks are making new 65 day highs, a rather mediocre reading that isn’t indicative of either an oversold condition or a breadth thrust, both of which lead to strong forward returns (chart 2). Finally, about 17% of stocks are in an outright bear market (down more than 20% from a recent high), which happens to be a level associated with indecision rather than a strongly trending market, one way or the other (chart 3).

As the data shows, sitting here in limbo implies rather average returns with also the largest distribution of outcomes. It may be prudent for the time being, therefore, for investors to maintain disciplined risk management while also focusing on investment factors that tend to outperform in the late stages of an economic advance like commodity sensitivity, quality and innovation.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital