As we write, comments by officials in Saudi Arabia about possible OPEC production increases later this year have sent WTI crude oil futures down below $68.00/barrel (-4%), down from nearly $73/barrel just three days ago. Meanwhile, global energy stocks are lower by about -2% for the day and -5.5% for the week. We therefore thought it a prudent idea to post a quick review of energy fundamentals that, despite (or indeed because of) the selloff, point to this pullback as an interesting time to add exposure to the energy space.

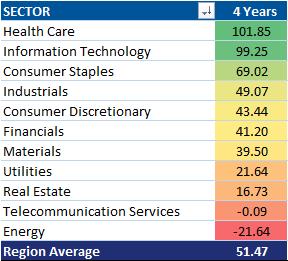

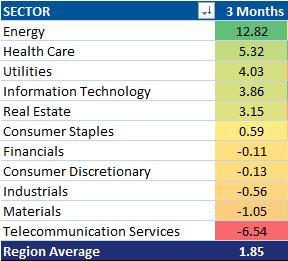

First off, it’s useful to review were we’ve come from in the energy complex. Not that long ago, energy commodities and energy stocks were absolutely hated. Indeed, the energy sector is the worst performing developed market equity sector over the last four years, down 22%. The energy sector finished 2017 with its lowest weighting in the S&P 500 ever. But, over the last three months, energy is the best performing global sector, even after taking into account this week’s selloff. Momentum is turning for energy.

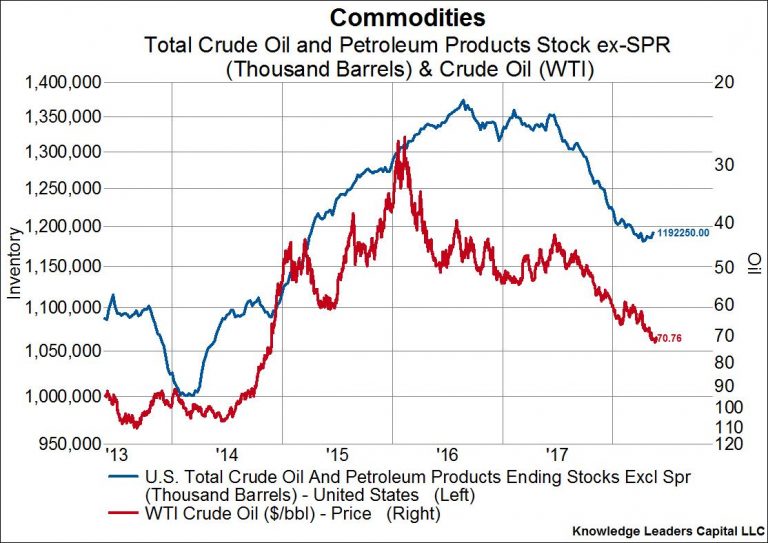

Next to inventories. US inventories this week registered a build of 5.8m barrels when the market was expecting a draw of 1.6m barrels. This helped push oil prices down this week, but the trend in inventories is clearly down. As the next chart below shows, inventories have been falling since the second half of 2016, and oil prices follow the trend in inventories closely.

But, the more interesting fact is that the futures curve remains in a state of steep backwardation (near prices higher than out year prices). This is incentive for holders of inventory to bring those inventories to market. As long as the futures curve is backwardated, there will be pressure on inventories, which should support the underlying price.

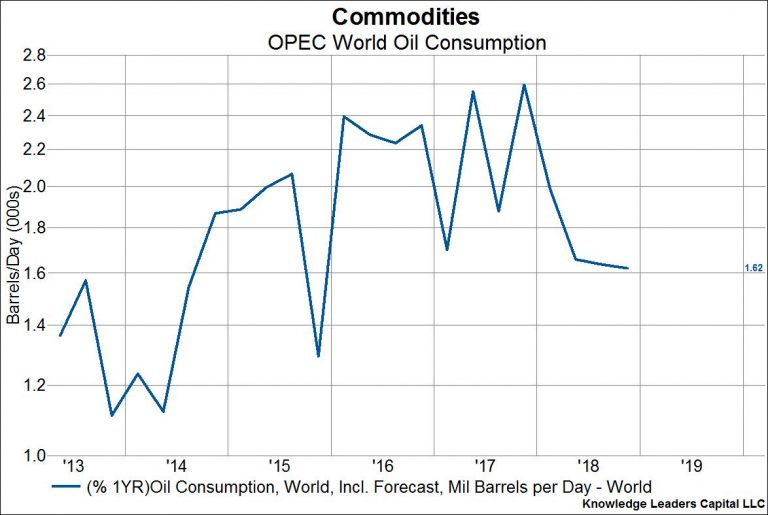

Consumption is also still growing. OPEC expects world oil consumption to rise by 1.6% in 2018.

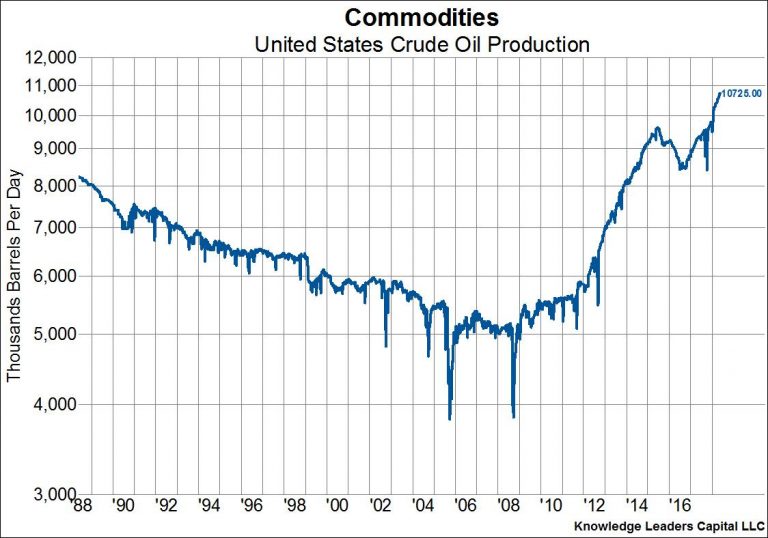

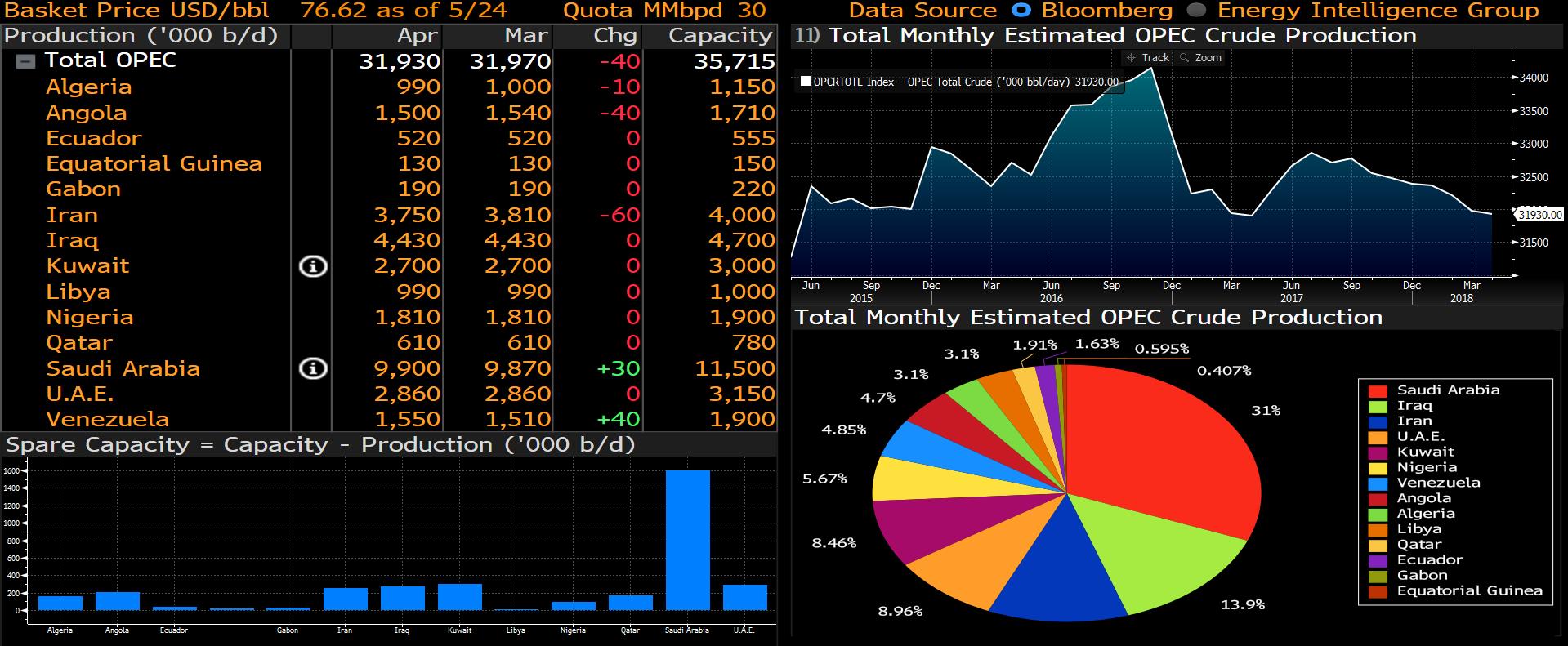

Next onto production. US crude oil production is growing at a breakneck speed, with some estimates putting total US production at 12m barrels/day by 2020. But, OPEC production (displayed in the Bloomberg screenshot below) is falling and despite the remarks today, the risk is to the downside. Venezuelan and Iranian production in particular is at risk of a major drop on political disarray and sanctions. And, just last month Saudi Arabia was on record saying it wanted $80 oil to support the Aramco IPO.

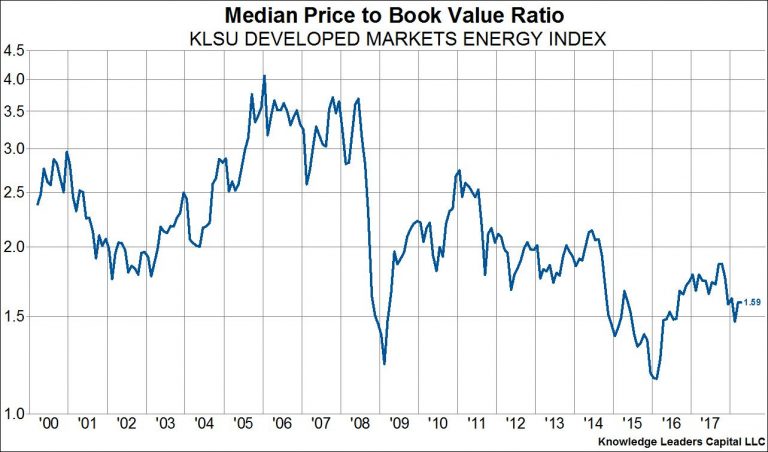

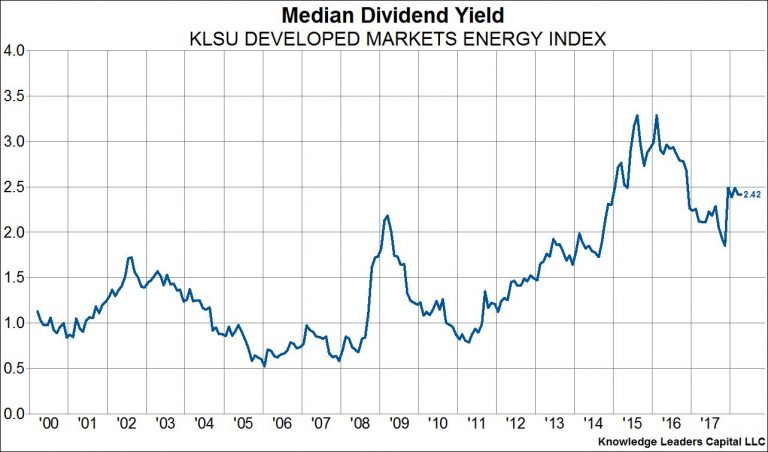

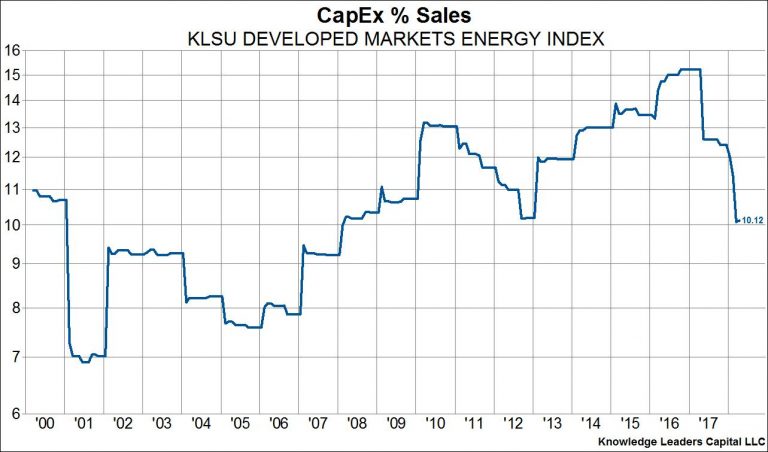

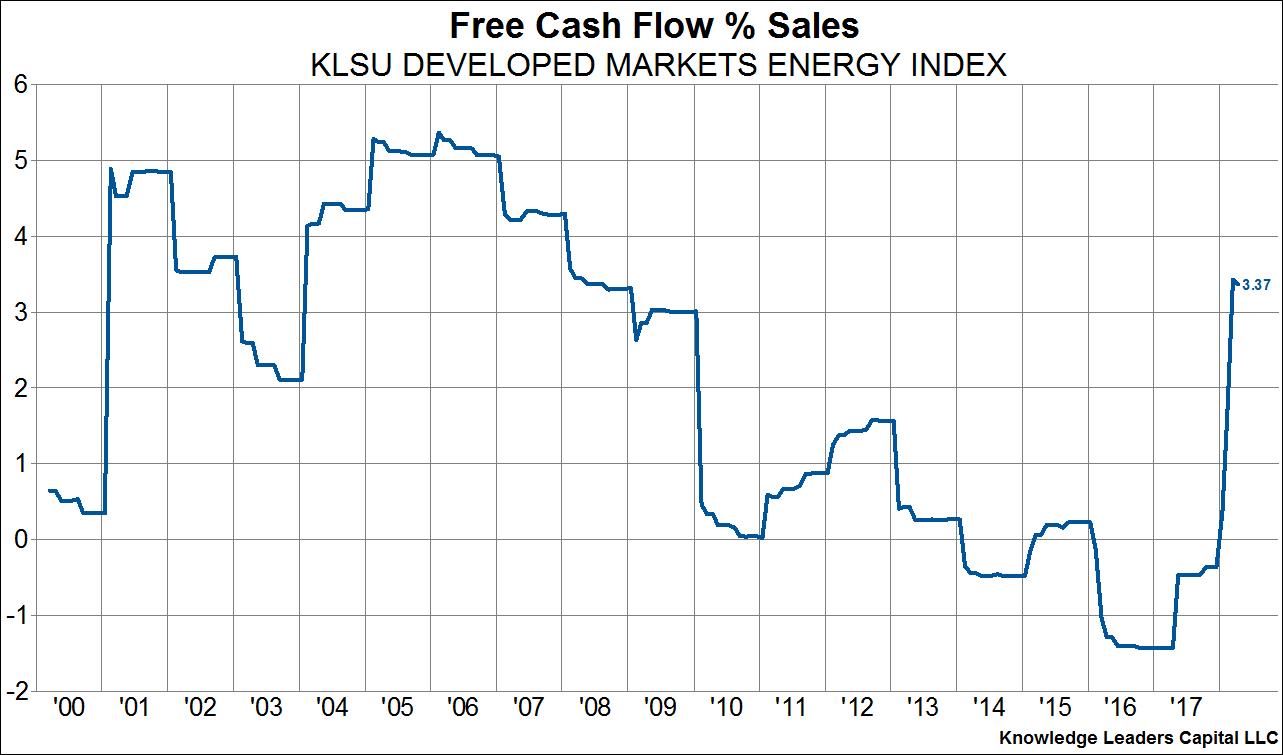

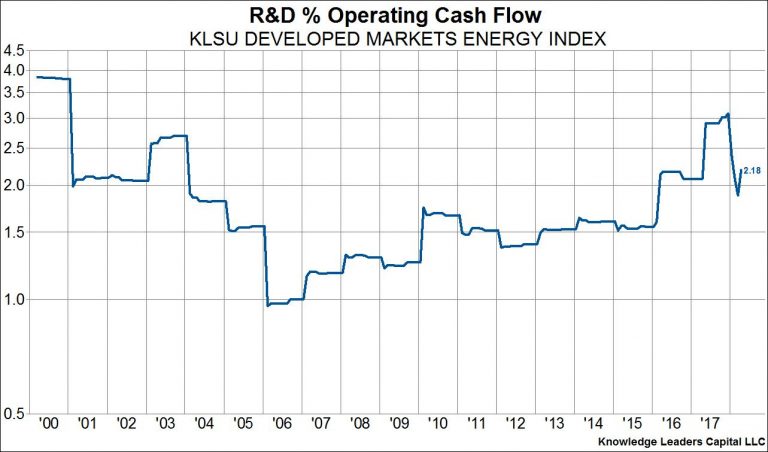

Energy stock fundamentals remain appealing. Global developed market energy stocks are still trading at recessionary valuation levels with the median dividend yield of 2.5% being near the highest recorded over the last two decades. CapEx as a percent of sales has fallen from 15% to 10% (which will act as a limiter to supply over the coming years), which has pushed up free cash flow to the highest level since 2007. Meanwhile, R&D investment – which we view as a higher return investing endeavor – continues to march higher.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital