The rise in oil prices is expected to have mixed effects on the U.S. economy. Higher gasoline prices will restrain consumer spending growth to some extent. However, increased energy exploration implies more capital spending, adding to GDP growth. For Federal Reserve policymakers, the key question is whether higher costs of transporting goods may be passed along to consumer prices. This adds to the Fed’s difficulties in achieving a soft landing for the economy in the months ahead.

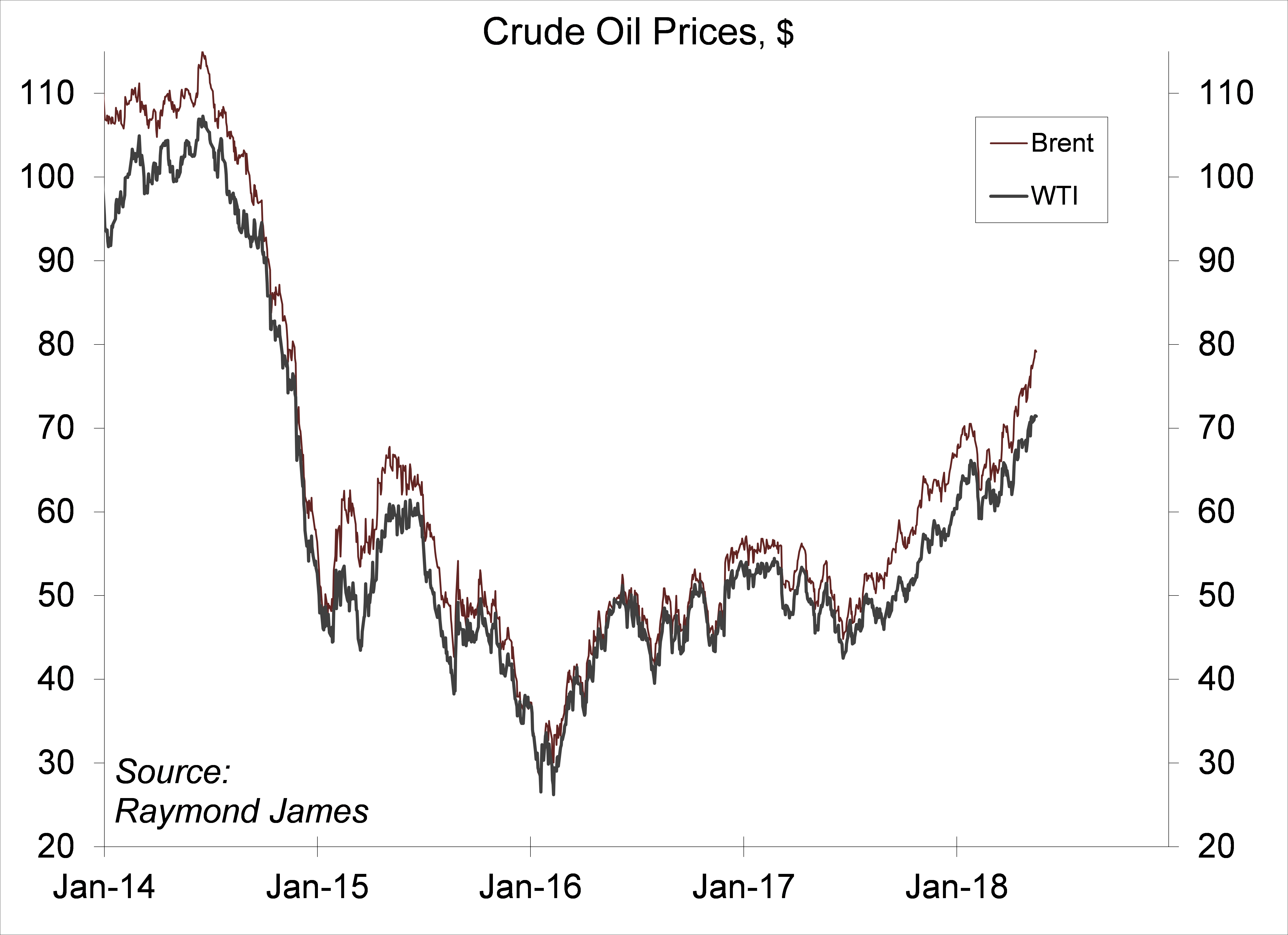

The increase in U.S. energy production has reduced our reliance on foreign oil in recent years. However, oil is still a global commodity. High prices overseas mean high prices here. Political tensions in the Middle East and problems in Venezuela should leave oil prices higher for the foreseeable future.

Click here to enlarge

The increase in gasoline prices has already had a noticeable impact on the consumer. Average hourly earnings, adjusted for inflation, are roughly flat on a year-over-year basis. The typical worker may be seen as running in place. You can still get gains in aggregate consumer spending, due to job growth, but the overall pace of spending growth is likely to be somewhat limited. That’s important, since consumer spending accounts for about 69% of Gross Domestic Product.

In the Great Inflation of the 1970s and early 1980s, higher oil prices boosted the Consumer Price Index. Many union wage contracts had inflation clauses in them, and non-union wages typically followed what was happening to union wages. The increase in the CPI fueled wage inflation, which in turn, added to consumer price inflation – a vicious cycle, which required a major recession in the 1980s to begin wringing inflation expectations lower. That lesson isn’t lost on the Fed.

In recent decades, the impact of oil prices on the economy has changed. Rising oil prices are seen less as a catalyst for higher inflation and more as a restraint on economic growth.

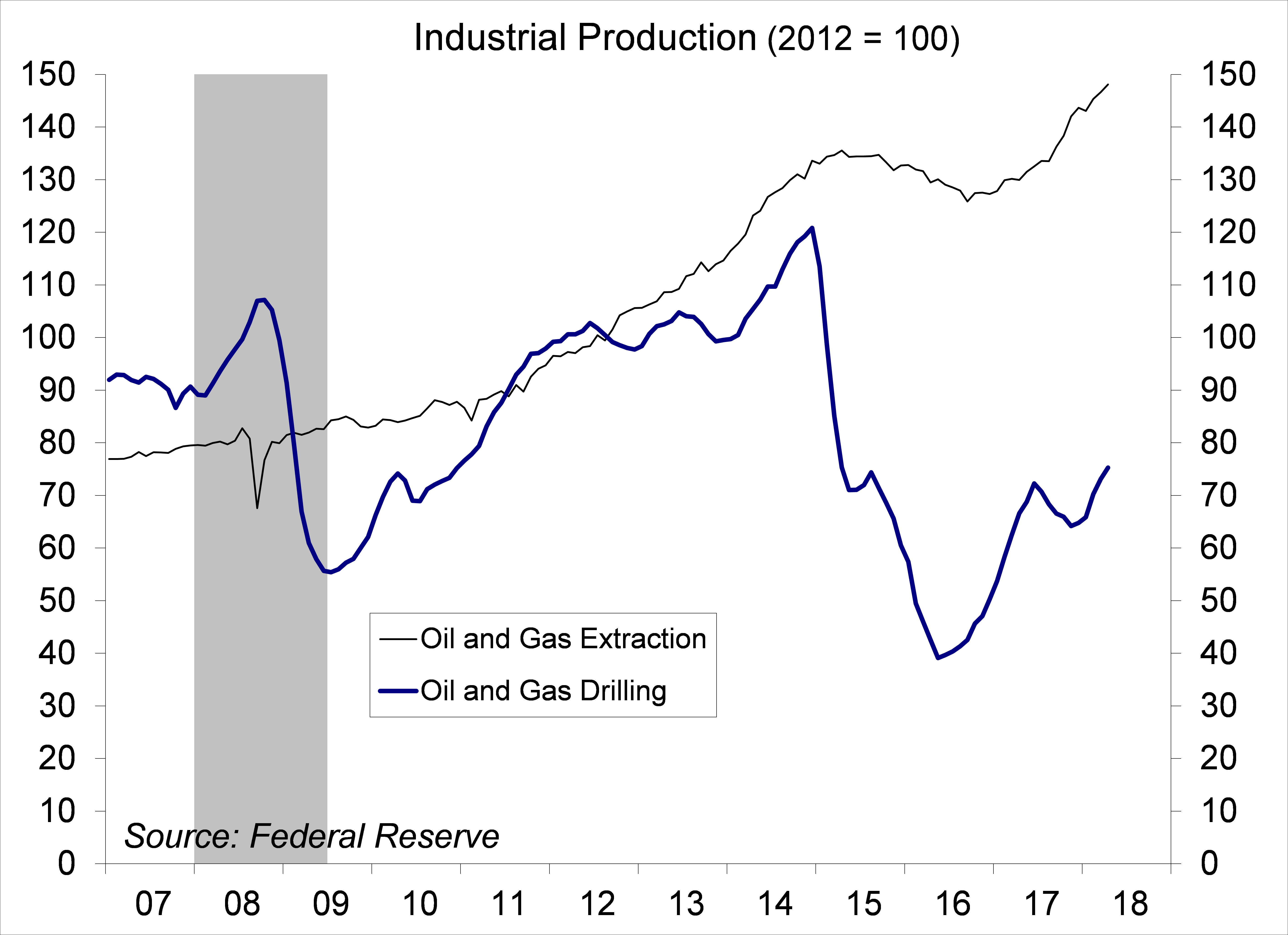

When oil prices fell in late 2014, the expectation was that we would see a significant boost to consumer spending growth. That pop failed to materialize, as consumers were faced with other constraints, such as rising rents and higher healthcare costs. Moreover, the contraction in (capital-intensive) oil and gas well drilling hit business fixed investment and overall GDP growth. The current rise in oil prices will restrain consumer spending growth, but also add further to business fixed investment.

Click here to enlarge

Finally, we listened so you don’t have to:

Richard Clarida – Time No Changes

In addition to being a well-respected economist, Fed Vice Chair-nominee Richard Clarida is also musician of sorts. He reportedly busked Beatles tunes at Harvard Square, and it shows in his first album, recorded over several years (two songs at the Abbey Roads Studios) and released in 2016. Beatlesque indeed, Clarida is pleasantly on pitch and has a good sense of harmony (more McCartney than Lennon). Some tracks include French horn and cello. Unfortunately, we get a sense about how Clarida feels about automation. Drums are handled by machine, leaving this reviewer unsatisfied. Ringo Starr was important, dammit! Drumming isn’t about keeping time – it’s about adding necessary color and complexity to the performance. That aside, Clarida proves himself to be a competent pop composer. The tunes are catchy. The lyrics, on the other hand, are often cringe-worthy. Lots of mushy “love” stuff (and nothing about monetary policy). Will Clarida’s approach to monetary policy be similarly “stuck in the 60s”? Hard to say (on a side note, this album could be played to disperse crowds of loitering teenagers). A second album is reported to be in the works. No word yet on whether it will include Chair Powell, who plays electric guitar.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James