The April inflation reports were a bit on the soft side of expectations, reducing somewhat the fears that we’re on the verge of an upside breakout in inflation. There’s no sign that a strong economy is putting much upward pressure on consumer prices. However, the evidence suggests that the tight job market is getting even tighter. Importantly, higher oil prices are seen less as a catalyst for higher inflation and more as a restraint on consumer spending growth. This is all consistent with gradually tighter monetary policy in the months ahead.

Weekly claims for unemployment benefits are often noisy, which is why economists recommend following the four-week average. That average has dipped further, now at the lowest level since December 1969 (when the labor force was about half of its current size). There is always some friction in the job market, partly reflecting the seasonal nature of a lot of industries. However, in a very tight job market, someone laid off is more likely to find a new job right away – and therefore is less likely to file a claim for unemployment benefits.

Click here to enlarge

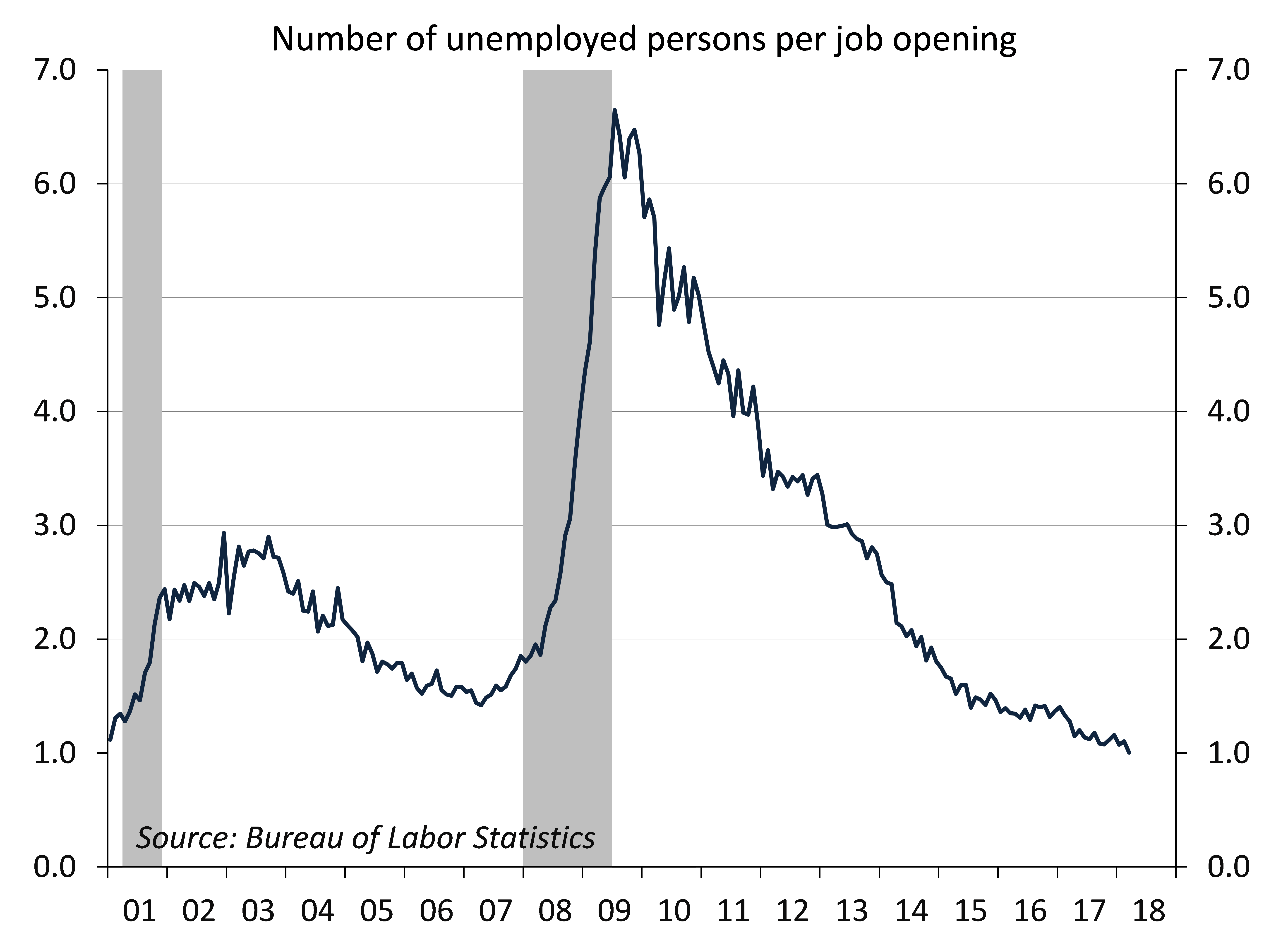

The March Job Opening and Labor Turnover Survey (JOLTS) survey results showed job openings exceeding the number of unemployed persons for the first time (the survey originated in late 2000). In a tight job market, workers are more likely to quit to pursue other employment. However, quit rates have remained little changed, at a moderate level, over the last year. That likely reflects an aging population (older workers are less able to pull up stakes and job hop). Presumably, younger workers should be moving up more readily than in recent years. The National Federation of Independent Business’ April Small Business Optimism survey showed that labor quality remained the #1 concern for the fourth consecutive month. Firms are responding to the tight job market by raising wages somewhat, but also by boosting job training, overtime, and automation.

Click here to enlarge

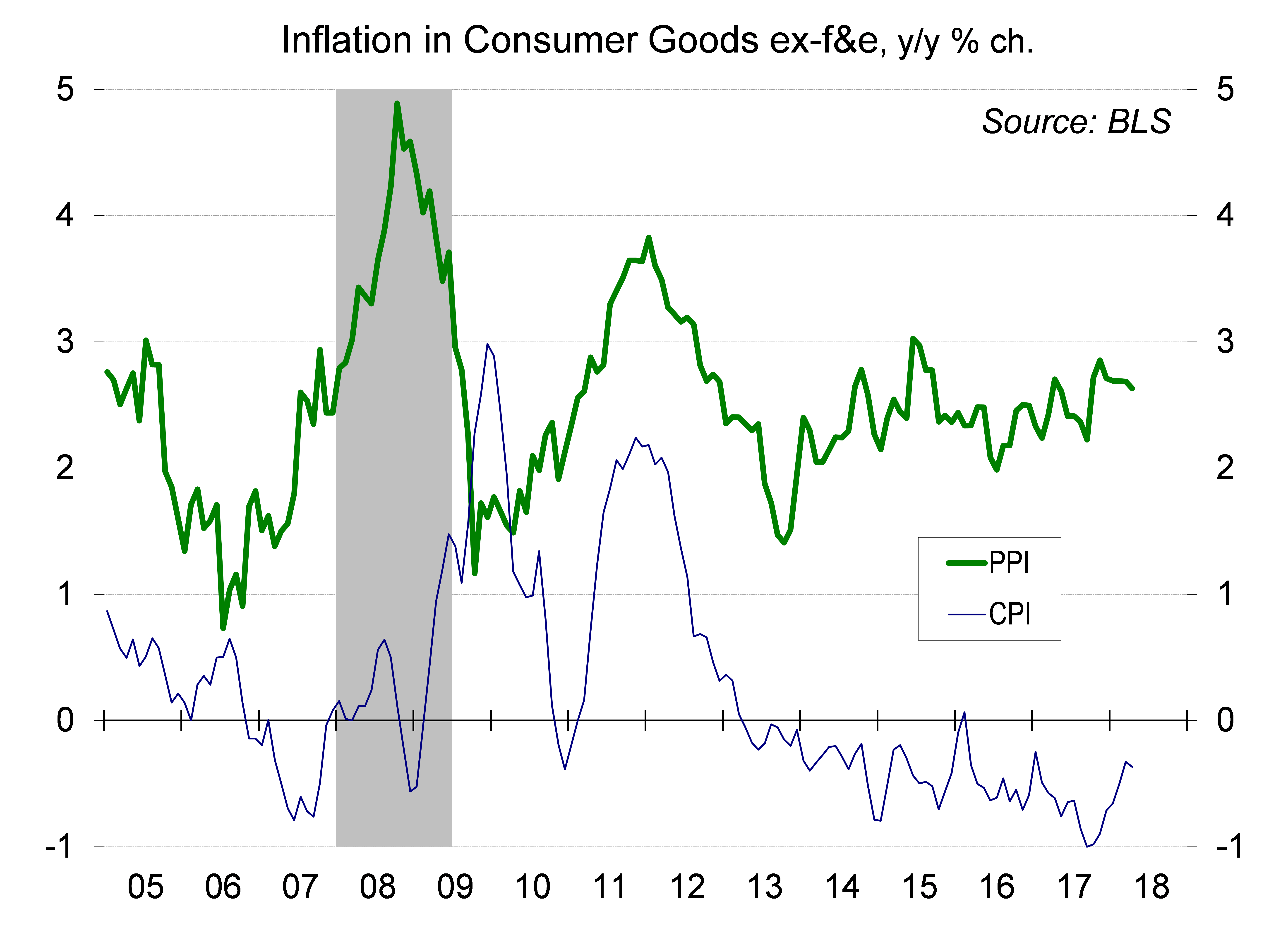

Labor cost pressures have remained moderate overall, but they are creeping higher. Commodity price pressures have been more evident, but in general it takes a gigantic increase in the prices of raw materials to have much of an impact on prices at the consumer level. The PPI and CPI data have continued to reflect a wide gap between wholesale and retail price inflation in consumer goods. Retail prices reflect more than the basic cost of goods (labor, advertising, etc.)

Click here to enlarge

Commodity price pressures generally have a hard time making it through to the consumer level, but oil prices are the exception. Higher gasoline prices will add to the impact of current constraints in transportation (a shortage of trucks and truckers) and dampen consumer spending growth (the idea is that if people are spending more money to fill their tanks, they will have less money to spend on other things).

Weighing the impact of higher gasoline prices on inflation and growth will add to the Fed’s challenge in the coming months – and the risks of a monetary policy error continue to rise.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© 2018 Raymond James Financial, Inc. All rights reserved.

© Raymond James

Read more commentaries by Raymond James