“At a time when the unemployment rate is well below full employment and inflation is accelerating, the Federal Reserve (Fed)

is already on a course to tighten policy in order to cool the economy. Fiscal stimulus has only served

to elevate concerns about economic overheating, meaning that the Fed will likely lean harder against much

of the boost from tax cuts and government spending in the form of higher interest rates.”

– Scott Minerd, Brian Smedley, Matt Bush of Guggenheim, “Forecasting the Next Recession”

Let me begin by saying our equity market trend model signals remain moderately bullish and our bond market trend model signals remain bearish. With that caveat, I do see us speeding down the road with limited visibility to the problem that exists just around the next turn. The mother of all bubbles exists and it is in the debt markets. It is global in scale and there is no easy way around the problem. Like bubbles past, this too will pop. The trigger? Rising interest rates.

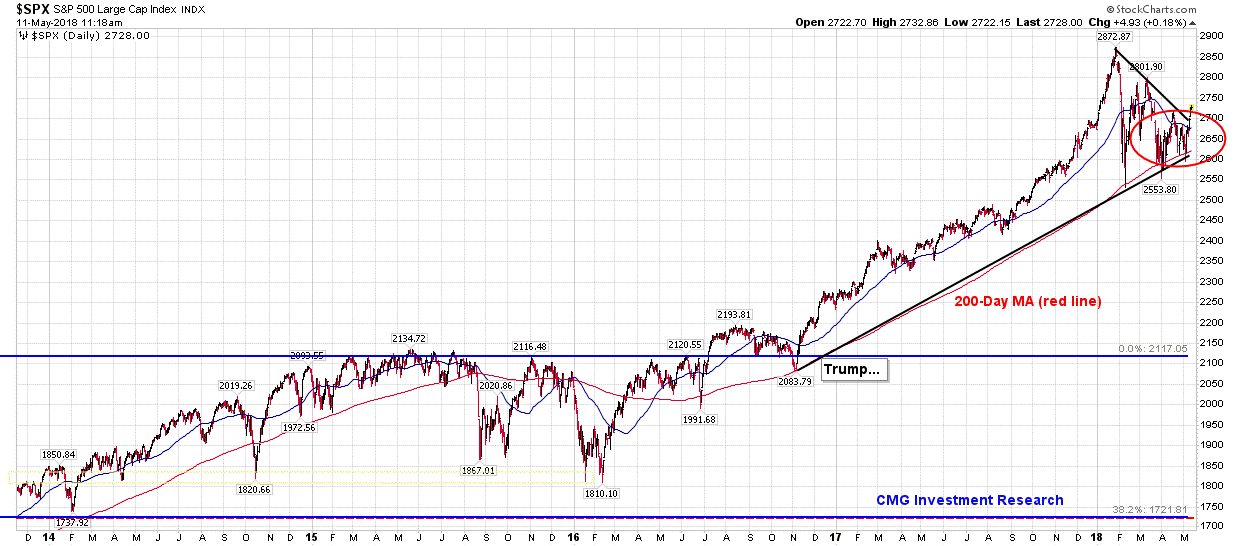

First, a quick look at the market. Tech is doing well this week and the S&P 500 has successfully held the 200-day moving average line and has made a positive break out to the upside as circled in the next chart.

Here’s how to read the chart:

- The thin red line is the 200-day moving average line (i.e., the average price of the S&P 500 Index for the prior 200 days).

- The red circle shows the test and hold of that trend line.

- The two black lines show a triangle pattern.

- Bottom line: The break out to the upside is bullish from a technical perspective.

While good news for the short-term trend, the larger macroeconomic picture has its challenges. We face a number of headwinds, the biggest issue is DEBT.

The debt situation in the U.S. is bad. As of December 31, 2017, it stands at 329% debt-to-GDP. It’s worse in the Eurozone at 446% debt-to-GDP. For perspective, credible studies show countries get into trouble when debt-to-GDP exceeds 90%. But what does this really mean for the economy and for you?

Think of debt-to-GDP as how much debt you have versus how much income you make. If you owe $300,000 on your mortgage, $20,000 on your car loan and $9,000 on your credit cards and you earn $100,000 per year in income, your total debt-to-GDP is 329% ($329,000 in debt and $100,000 in income). For your personal and family economy, at what point do your mandatory monthly interest and principal payments become a drag on your personal situation? With less to spend, it impacts the overall economy.

Now that’s not a big deal if it is your brother who is the only person who’s borrowed too much. Picture what happens to him when interest rates rise. Even more of his $100,000 income has to be used to cover the debt. His problem!

It is a really big problem for our collective economy if many people/corporations/governments are deeply in debt all at the same time. As you’ll see in the chart to follow shortly, we don’t experience very good growth when debt is high. We get great growth when debt is low.

If we don’t get good economic growth, we don’t get good business growth. Period. So earnings struggle and if stock prices are high relative to earnings, then something has to give. Earnings must rise to justify current prices or prices must fall to get back to fair value. And based on the high level of debt and the evidence you’ll see in the chart below, outside of a short-term shot to the arm in the form of tax cuts and shareholder buybacks, I don’t think we will get greater earnings. So equity prices will likely mean revert back to fair value. Fair value on the S&P 500 based on 52 years of price-to-earnings ratios is about 1,821.96, as of the end of April 2018. That’s a decline of 35% from the current level 2,790 of the S&P 500.

Just how bad is the global debt problem? Following is the most recent debt-to-GDP data from Ned David Research (NDR):

Japan 590%

France 480%

Germany 279%

Greece 360%

S. Korea 357%

Netherlands 725%

Denmark 585%

Canada 332%

Italy 360%

Portugal 488%

Ireland 828%

Spain 397%

Sweden 467%

Switzerland 382%

UK 476%

China? This from Bloomberg, “In 2008, China’s total debt was about 141 percent of its gross domestic product. By mid-2017 that number had risen to 256%. Countries that take on such a large amount of debt in such a short period typically face a hard landing. That’s why everyone—academics, private banks, the International Monetary Fund, the Organization of Economic Cooperation and Development, the Bank for International Settlements, and People’s Bank of China Governor Zhou Xiaochuan—is sounding the alarm.”

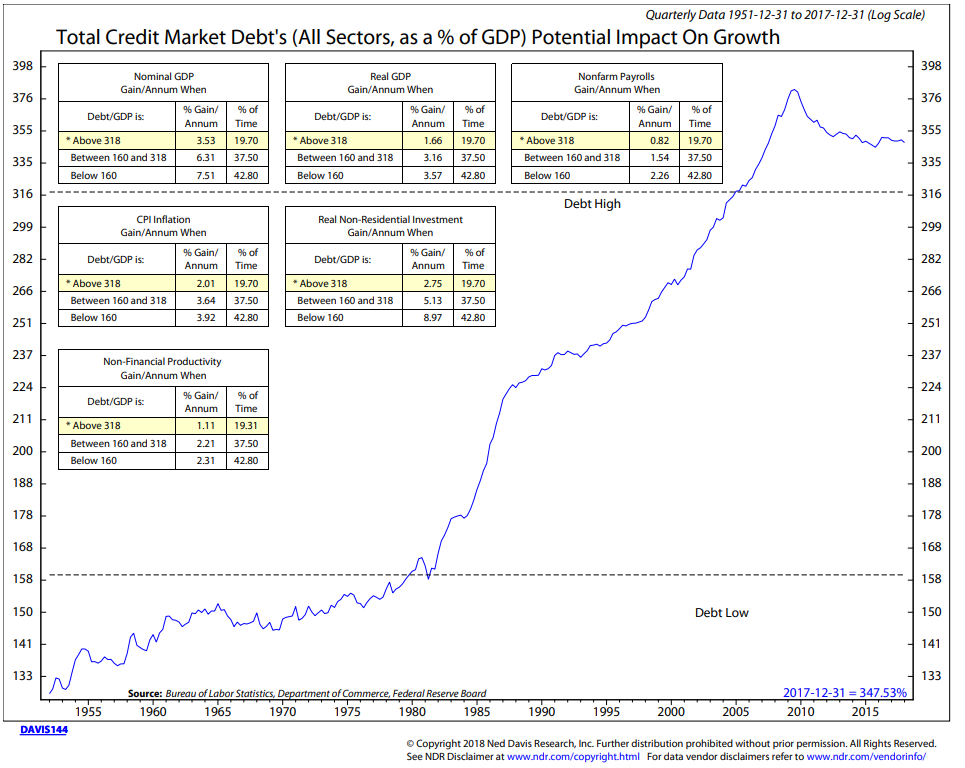

The next chart is one shared with you many times in prior letters. NDR looked at the history of total U.S. credit market debt and compared it to U.S. GDP. You can see clearly that when debt was low, growth was high. When debt was high, growth was low.

Here is how you read the chart:

- The blue line tracks the level of total credit market debt’s potential impact on growth of all sectors in the U.S. relative to the U.S.’s GDP. Think of that like the example of your total debt compared to your income or your personal GDP – what you produce.

- The boxes show various economic data points. Think of them like an economic dashboard: Nominal GDP is growth before inflation, Real GDP is growth after inflation, Payrolls (the annual gain in wages relative to debt levels, inflation, investment and productivity.

- NDR looks at the stats back to 1951.

- The yellow highlights the current zone.

- Bottom line: Periods of low debt levels are good for growth, periods of high debt are a drag on growth. The economy cycles. The world turns.

I really like how NDR plotted the impact on the U.S. economy in the above chart. Think of it as a high probablity way of measuring and assessing future outcomes. And if you look at the very poor growth since 2000, it’s hard to refute the facts. Debt’s a drag on growth after it reaches a certain threshold.

Since the 2008 crisis, we have slowly begun a process of deleveraging (blue line declining). But not by very much. The bubble remains. We are currently late in a long-term debt cycle not too dissimilar to where the world was in the mid-1930s. And frankly, we are seeing many of the same protectionist uprisings we saw then. It’s the economy. People are not happy. How and when we find resolve and solution to restructure the debt will determine the outcome for the markets and the economy. We just don’t know what that looks like yet.

Ray Dalio founded the world’s largest hedge fund, Bridgewater Associates. His investment process is based on his understanding of “How the Economic Machine Works.” To which, he and his team wrote a long paper (required reading for our incoming summer interns… and my kids) and created a short video that explains just how the system works. This simple but not simplistic video shows the basic driving forces behind the economy and explains why economic cycles occur by breaking down concepts such as credit, interest rates, leveraging and deleveraging.

The Interest Rate Trigger

We have all likely taken advantage of refinancing our mortgages when rates dropped. Many of us did it a number of times. One of my sisters kept playing the 0% credit card interest game until she couldn’t anymore. Then wham! Rates down = good for borrowers and bad for savers. Rates up = bad for borrowers and good for savers.

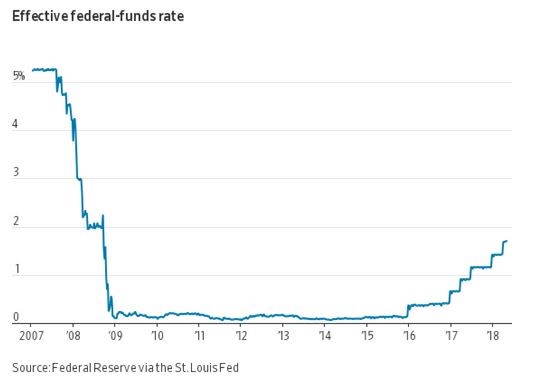

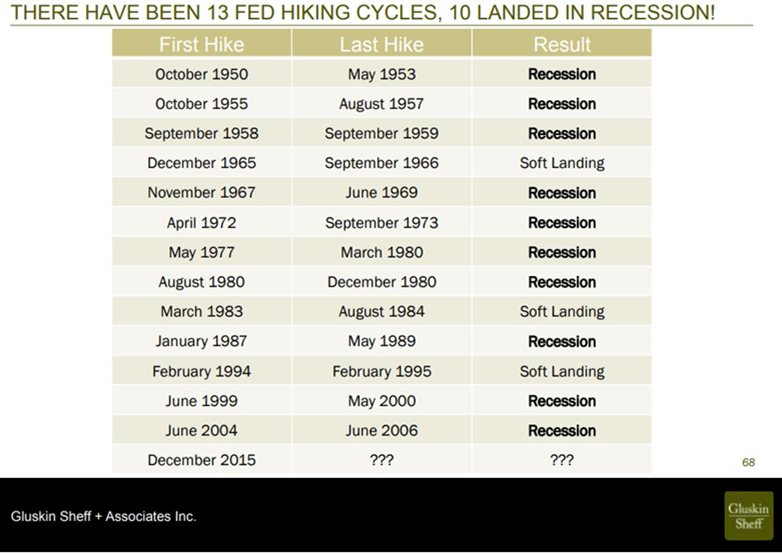

When debt is excessive and rates rise, the squeeze is on. And that is what’s happening now. We are early in the rising interest rate move but it is real and the stakes are high. Interest rates are the trigger.

And interest rates are heading higher. At least over the short-to-intermediate term. This from Scott Minerd and team as introduced above, “At a time when the unemployment rate is well below full employment and inflation is accelerating, the Federal Reserve (Fed) is already on a course to tighten policy in order to cool the economy… The Fed will likely lean harder against much of the boost from tax cuts and government spending in the form of higher interest rates.” Yup… agreed.

We have a new Fed lead by Jerome Powell. It is a hawkish Fed. They are determined to get rates higher. We may see another 1½% on top of what you see in the chart that follows next. That is going to be tricky with so much debt.

What will transpire? As rates rise, interest payments will become a bigger burden on corporate, individual and government budgets. This is serious. Many governments will raise taxes to try to keep the game going but that will cause even more deflation. States will try to do the same. Ultimately, this will cause even more deflation. Like rate cycles past, the Fed’s higher interest rate game plan will drive us right into the recession. You’ll find a great illustrative chart in the debt section. On my radar is a #2019-2021DebtCrisis, #Recession and what John Mauldin calls “The Great Reset.” Debt’s the problem and rising interest rates are the trigger. We’ll keep a close eye on the recession watch indicators. Right now? All good…

Can we smooth our way through this? Maybe. Likely? Doubtful. The resolve requires politicians and central bankers to come together and sing “Kumbaya.” Republicans and Democrats, the President, the Fed, the ECB, the European Union, Germany, Italy, Spain, the U.K., the Bank of Japan, China… and the beat goes on. The great Billy Joel whispers in my mind:

We didn’t start the fire

It was always burning

Since the world’s been turning

We didn’t start the fire

No we didn’t light it

But we tried to fight it

Can our global leaders all hold hands agreeing to strict currency bands (control the currency shocks) as we all burn the debt in a coordinated effort? The Great American Debt Restitution Act or something that sounds pleasing to us but in reality is really risky. Bottom line: The Fed and the Treasury with newly enacted laws by Congress do a swap. Print, buy and evaporate to get debt-to-GDP to a more manageable number. Say 50% of GDP.

Until then, the dominant long-term trend remains “deflation.” After the reset, we run inflation risks.

Do you remember when Boston College’s quarterback, Doug Flutie, threw a last-second Hail Mary pass to wide receiver, Gerard Phelan, to give Boston College a come from behind victory? If you missed it, you can find it here. Look, it can be done.

Here’s the play: The global central bankers and politicians are on offense. Trump calls the play, hands the ball to Jerome Powell who tosses it backwards to Mario Draghi. Draghi leans back, Flutie-like, and launches a long pass to wide receiver, Angela Merkel. She catches it at the 50-yard line, runs forward then laterals the ball to Theresa May. May dodges a pesky ultra-conservative far right defender and yells to Shinzō Abe and Xi Jinping to block the remaining five defenders as she races towards the brightly glowing Brexit sign she spots in the back of the end zone. Odds of that play working?

But boy, do we need a Hail Mary. Just not sure we can get our offense in sync.

If equity market valuations were not so obscenely high, I would not be as concerned. If interest rates were not just off 5,000-year lows (not a typo), I would not be as concerned about loss on bonds. Our initial starting conditions are simply not so good. I think it will take a crisis to get the players on the same page.

Game plan: seek growth and have a trader’s mentality to minimize downside loss. More defense than offense is prescribed. We sit in a similar place as we did in 1999 (the great tech bubble) and 2007 (the housing bubble). But today it is the great debt bubble. It is the mother of all bubbles. You can shape your risk and return outcome based on the mix of strategies, but have a stop-loss process on everything you own.

I know this sounds all depressing, but please don’t ingest it that way. I just don’t see it that way. Instead, see the opportunity in this message. Recall the return opportunities that presented in 2002 and 2009. The next dislocation will be specular if you sit in the privileged position to act. Let’s get to it in good shape.

Grab that coffee and find your favorite chair. I have a few more debt charts and another fun cartoon from Ray Dalio where he provides a “crib notes”-like version of his new book, Principles. I’m adding to the summer intern’s to-do list and sharing it with my kids. Finally, you’ll find the link to the most recent Trade Signals report. Thanks for reading. I hope you find the letter helpful for you and your work with your clients. Have a wonderful weekend!

Included in this week’s On My Radar:

- A Few More Debt Charts

- Ray Dalio’s Principles of Success

- Trade Signals — Bearish Bond Signals, Moderately Bullish Equity Signals, 200-Day MA Holding

A Few More Debt Charts

JPMorgan’s Jamie Dimon said on Tuesday, “Prepare for 4% yields and volatility to rise as QE exit precedes.”

“With the Fed paring back its balance sheet and the federal government increasing its borrowing, the U.S. will have to finance by the end of the year “$400 billion a quarter — that’s a lot, that’s a huge shift from the past,” Dimon also said. “Along with cutbacks in bond purchases by other central banks, it “may cause more volatility, higher rates in a way we don’t fully understand” given the exit from quantitative easing is unprecedented,” he said. (Source: Bloomberg.)

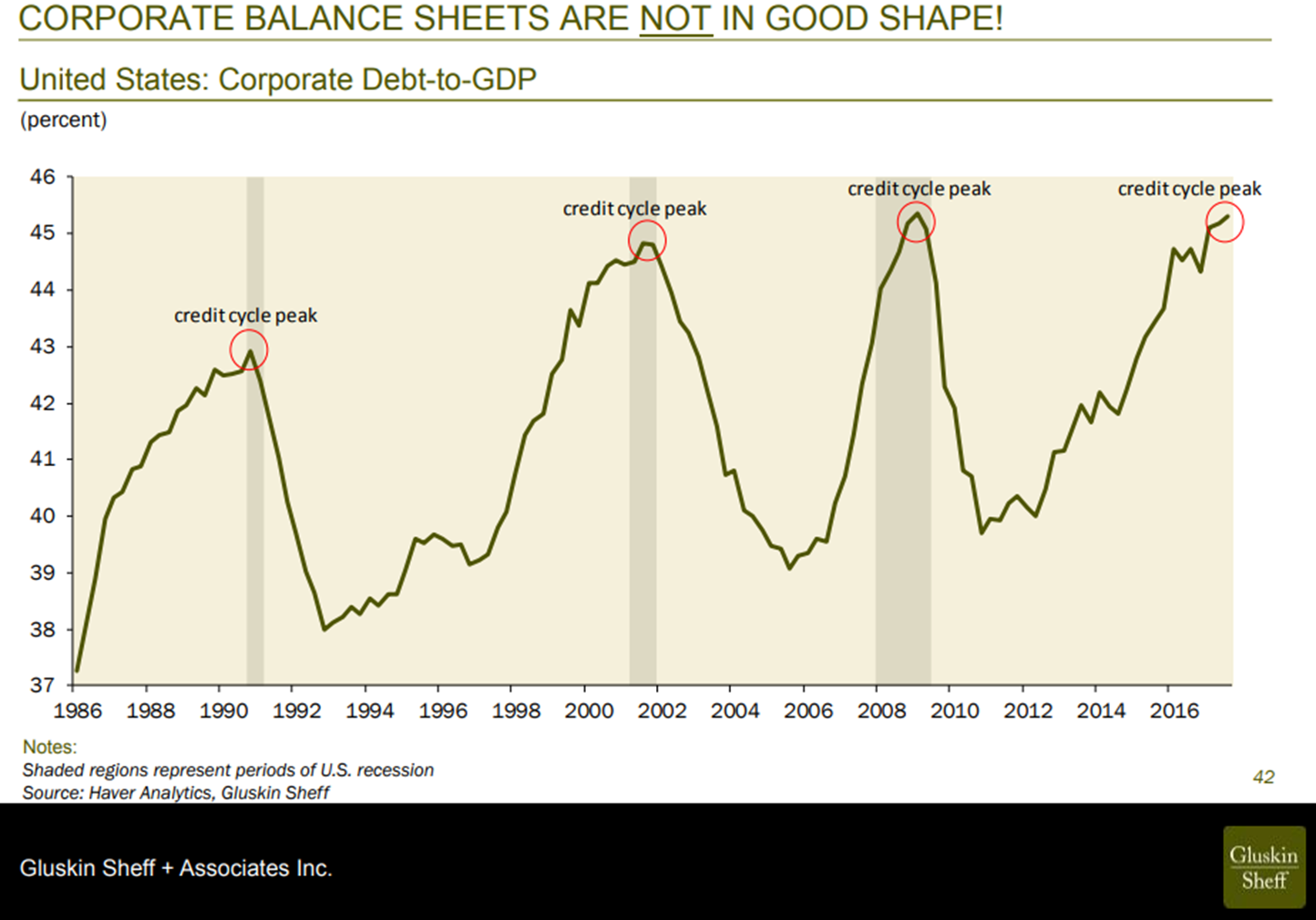

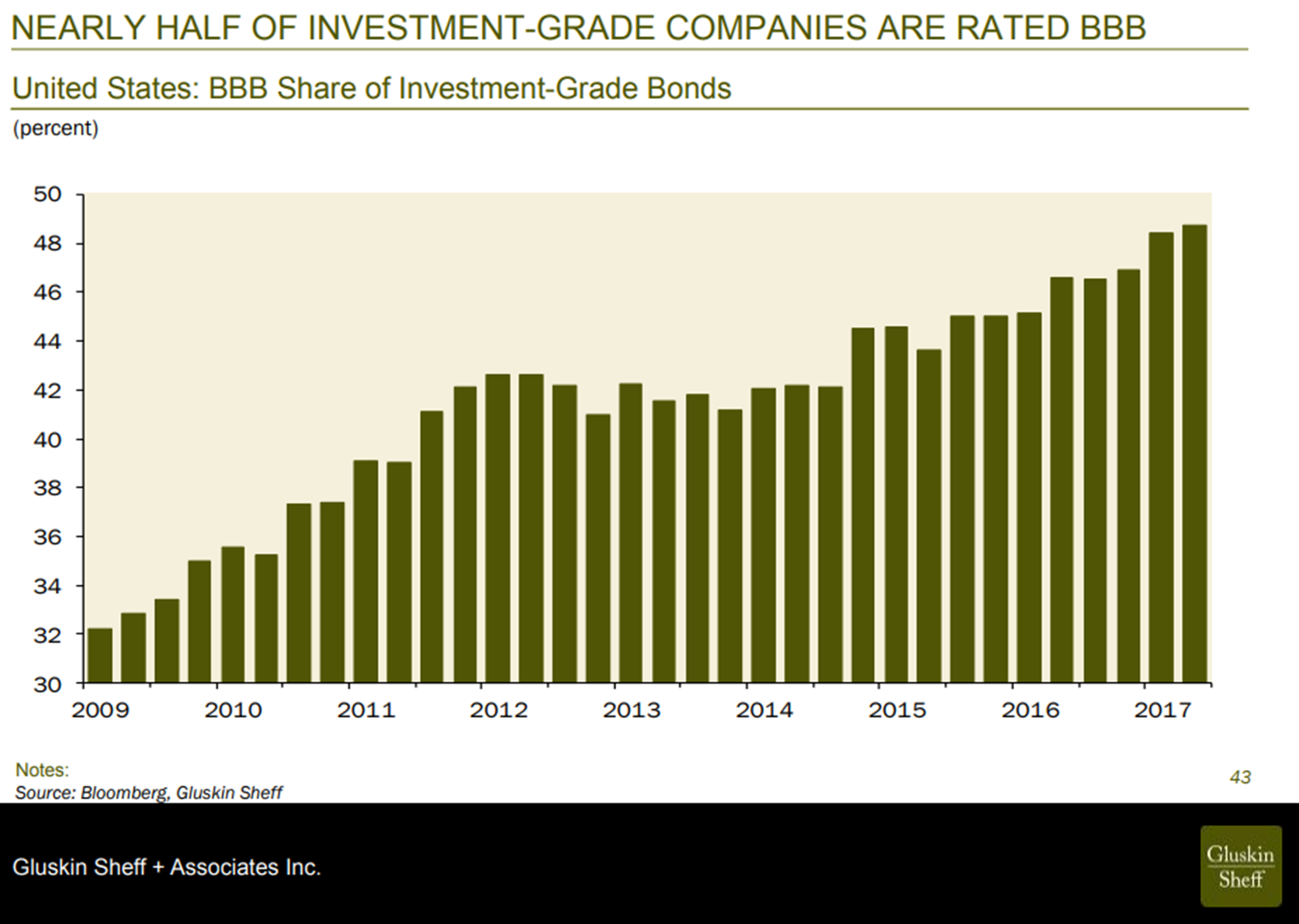

I’ll be sharing more about debt over the weeks to come. Following are a few more charts for your review. I conclude with my thoughts.

Money chasing into riskier assets has enabled companies to finance at terms least favorable to the investor. Nearly half of investment grade debt is BBB rated. Compare that to 2009… Yikes.

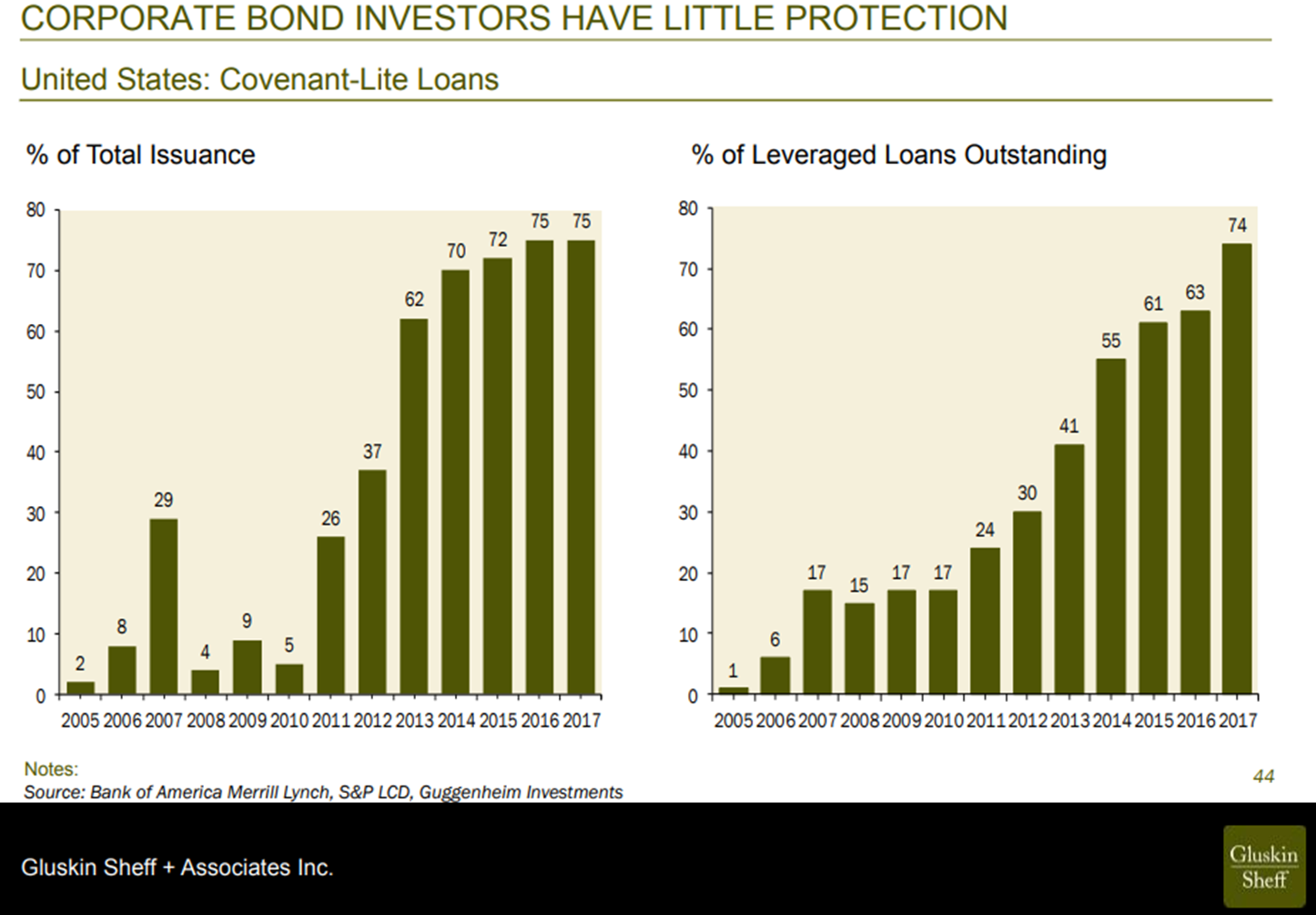

And bond holders are getting little protection (come on… this is crazy):

The current business cycle is aged. Expect recession soon. In recession defaults rise and with little protection in the bonds and an abundance of poor quality. Expect record defaults.

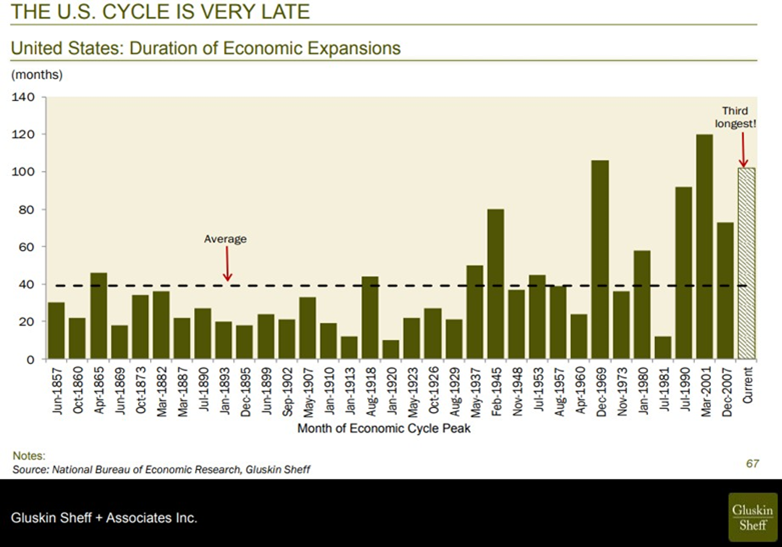

Recessions happen especially when the Fed raises rates:

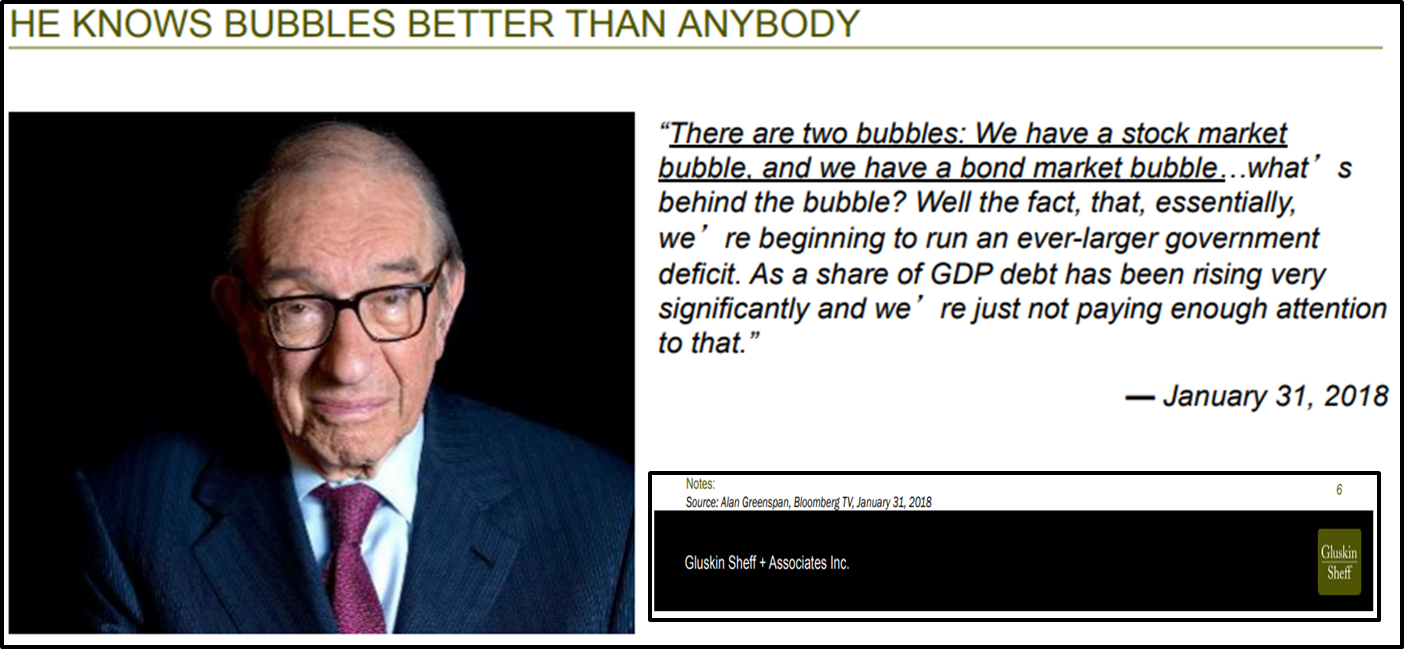

Now he sees bubbles?

My two cents:

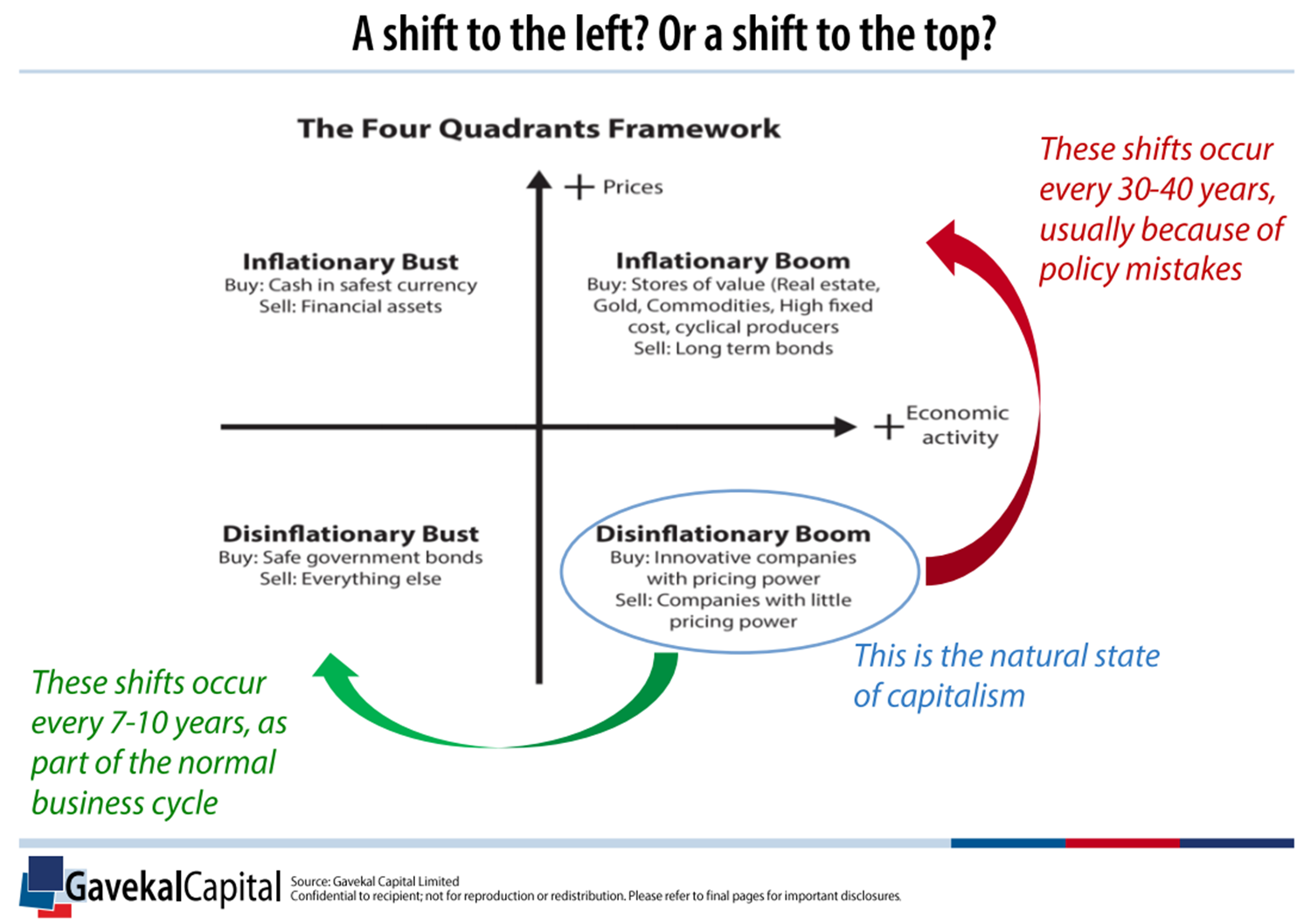

I believe this next charts sums up where we sit today:

Here’s how to read the chart:

- Current state today is a “Disinflationary Boom.”

- The shifts from disinflationary boom to inflationary boom occurs every 30 to 40 years. The last inflationary boom ended in the early 1980s.

- It is possible we move to a disinflationary bust, then “reset” the debt, then move to an inflationary boom period.

- Note the assets that perform best in each quadrant.

As I’ve stated, I believe probabilities point to a coming debt crisis and recession. That will take us along the green arrow above to a “disinflationary bust.” During which time, my hope is the debt crisis will enable global political resolve to such a degree that will enable a restructuring of the debt. Print, buy and make much of it disappear. Burn the tally sticks, as they did in time past. That will then drive us to the upper right quadrant creating an “inflationary boom.”

Neither left nor right are good choices for buy-and-hold investors. We are entering a period of time that will again favor active management. My hope, of course, but it is what I feel is most probable.

Ray Dalio’s Principles for Success

I enjoyed Ray Dalio’s short video summarizing his recent book Principles. In the early 1980s, he believed that a collapse was coming in the financial system and positioned aggressively for that outcome. He lost, had to lay off his entire staff and borrow $4,000 from his parents to survive. Since then he has thrived and found that his greatest point of distress became his greatest teacher. Today, he runs the largest hedge fund in the world.

Two quotes I really liked:

- “Having big dreams, plus a sense of reality plus determination is the key to a rewarding and successful life.”

- “View problems like puzzles. Treat pain as a clue that a great learning opportunity is at hand.”

Trade Signals — Bearish Bond Signals, Moderately Bullish Equity Signals, 200-Day MA Holding

S&P 500 Index — 2,694 (05-09-2018)

Notable this week:

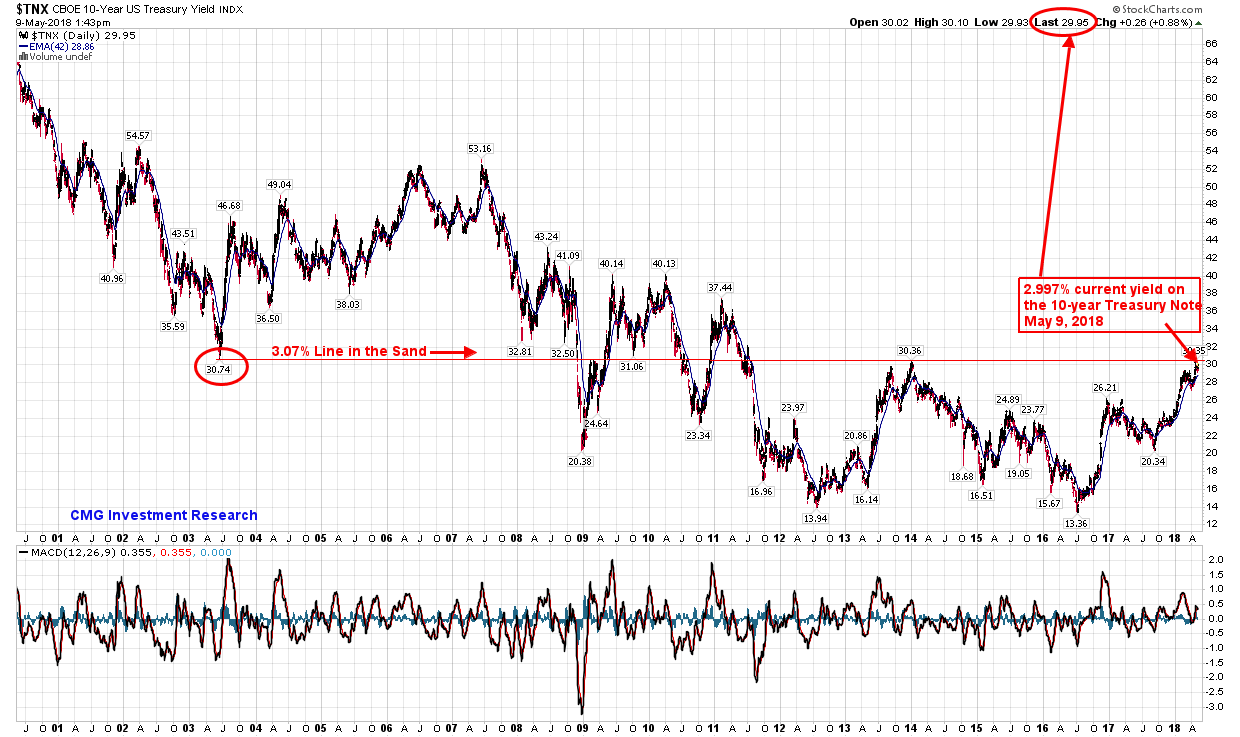

The Ned Davis Research CMG U.S. Large Cap Long/Flat Index remains at a moderately bullish 80% large cap exposure buy signal (down from 100%). The 13-week trend line vs. the 34-week trend line remains on a “buy” signal; however, the short-term 13-week moving average is rolling down. Volume demand continues to be greater than volume supply, which also supports a bullish posture. The CMG Managed High Yield Bond Program is in a “sell” signal. Gold remains in a long-term cyclical bull market trend. The Zweig Bond Model remains on a sell and the 10-year Treasury Note yield continues to flirt with 3%. I view 3.07% as the line in the sand. Yesterday, JP Morgan’s Jamie Dimon said he would be surprised to see the 10-year going at 4%. That will shock the markets. Note that the next chart plots the yield and shows the current 2.995% yield as 29.95 (not sure why it is shown that way). Bottom line: we are flirting with a break in yields to the upside.

Wishing the very best to you and your family.

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group

Read more commentaries by CMG Capital Management Group