USD Hedging Getting More Expensive: LIBOR-OIS Spread Heading Higher

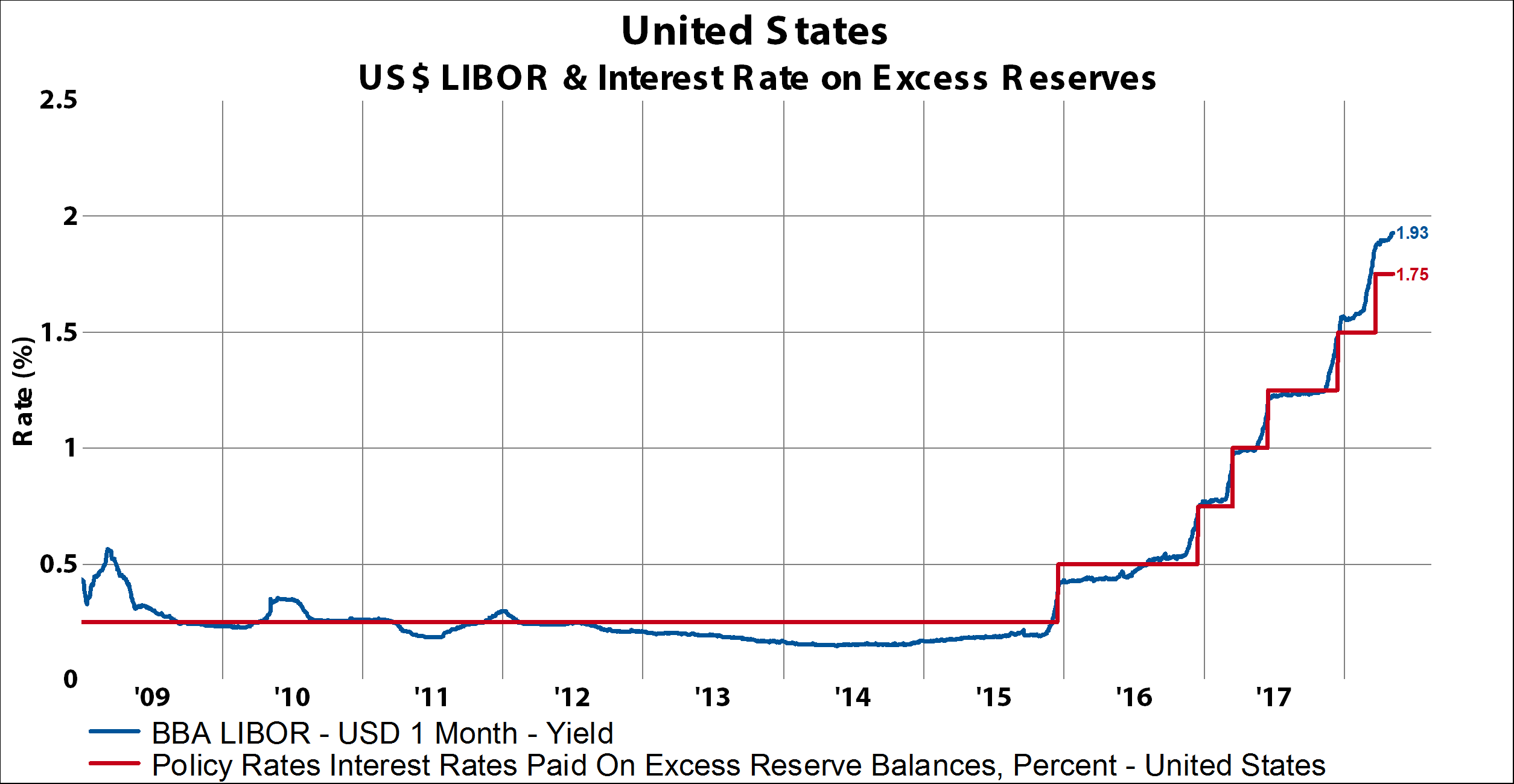

There are two basic drivers of the London Interback Offered Rate (LIBOR): 1) policy rates and 2) a variable premium. Starting with the policy rates component, in the chart below I compare the interest rate on excess reserves (IOR) and USD LIBOR. Because the IOR rate is purely policy directed, I am using the interest on excess reserves as a surrogate to the overnight index swap (OIS) rate. Since there are about six more 25bps rate hikes expected by the end of 2019, USD LIBOR should track rates higher.

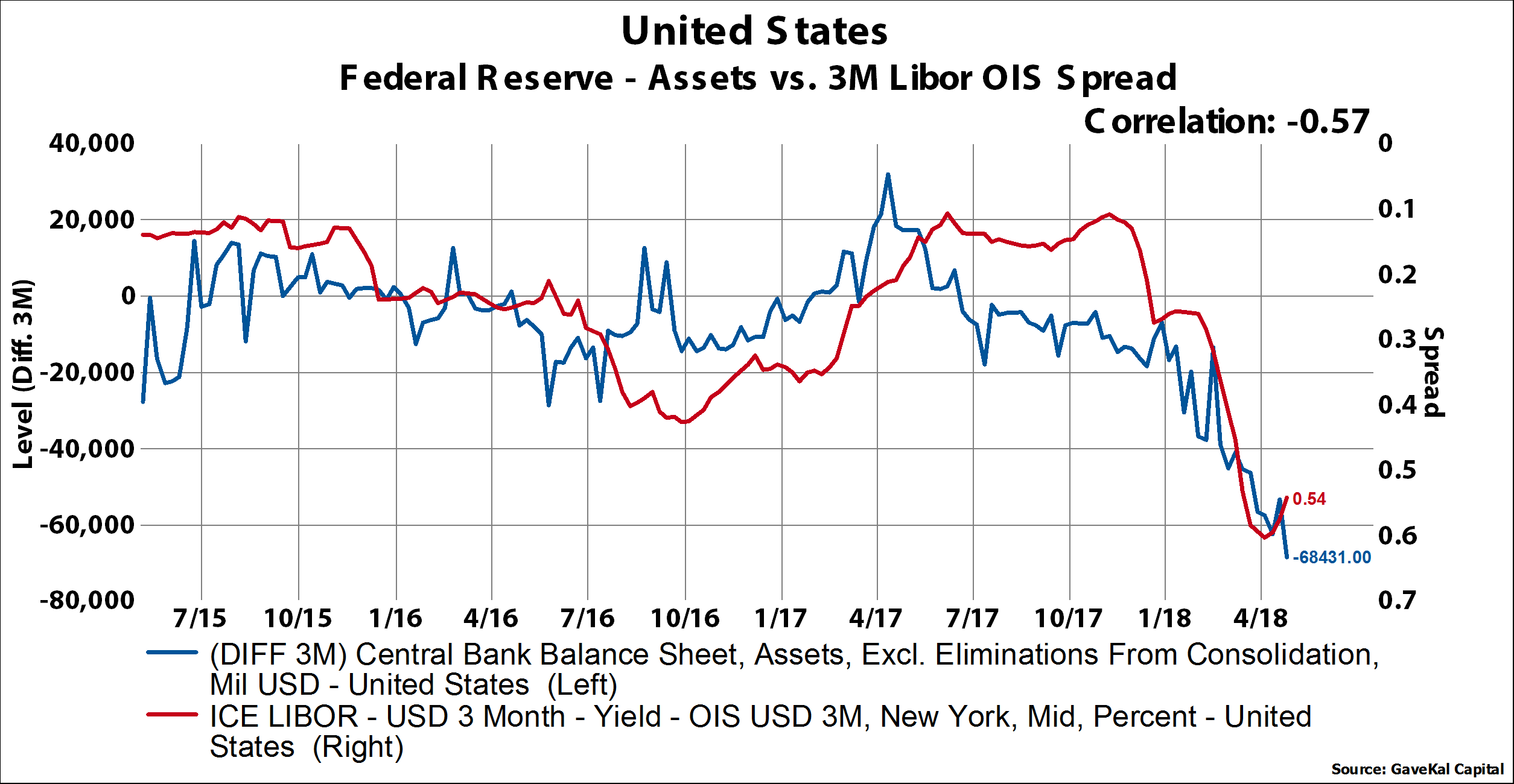

The second component of the LIBOR-OIS swap is a variable premium. Our work suggests the biggest driver of the variable premium is monetary driven also. So-called “quantitative tightening” is the term that has been adopted to describe the process of balance sheet roll-off at the Federal Reserve. In the chart below, I compare the 3-month change in the Federal Reserve’s balance sheet to the LIBOR-OIS spread. In the last few months, as the Fed has held to its accelerated pace of run-off, the LIBOR-OIS spread has widened considerably.