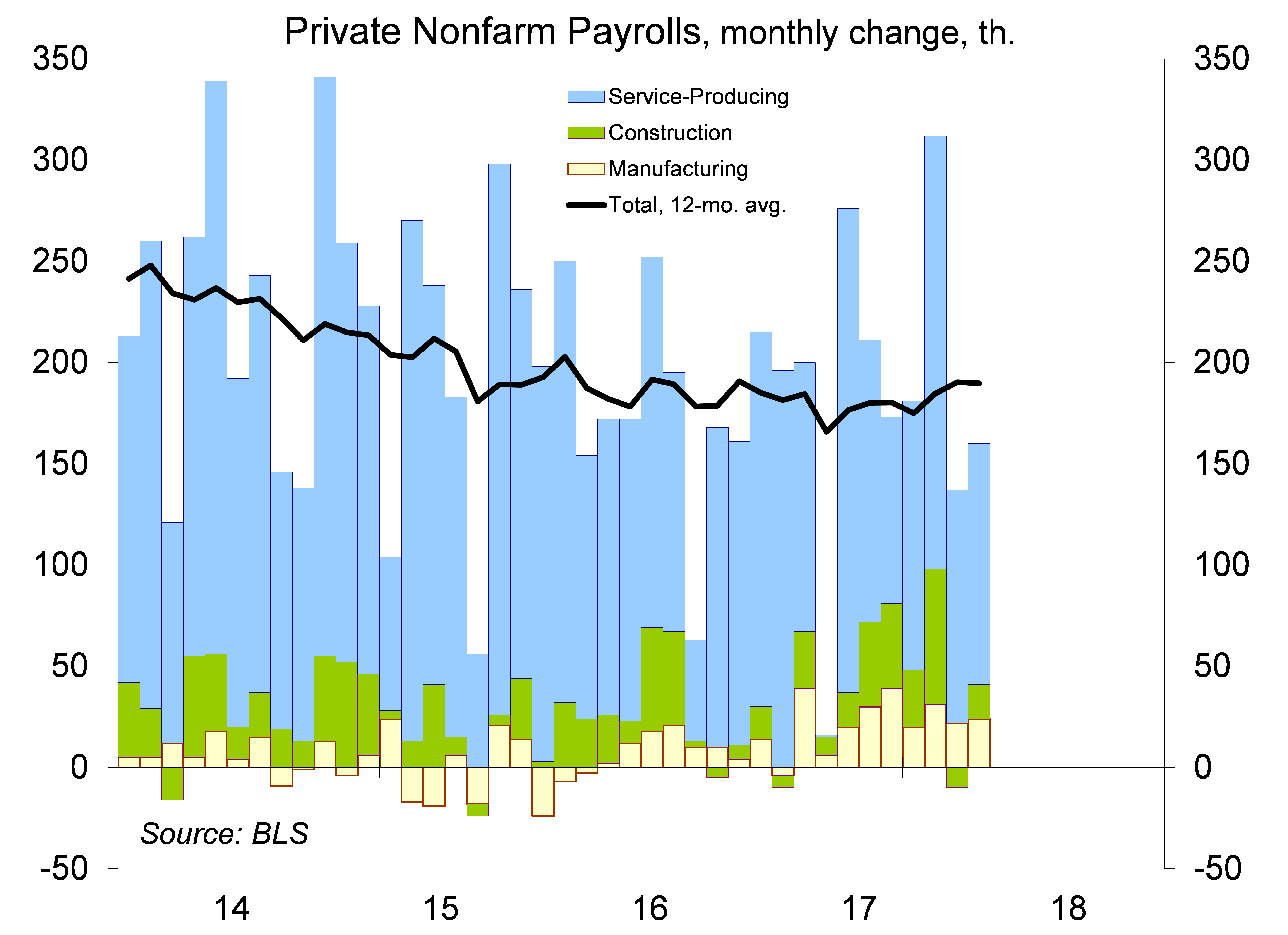

Nonfarm payrolls rose by a little less than one million in April – that is, prior to seasonal adjustment – up by 2.932 million from January to April (vs. +2.708 million for the same three months a year ago). Seasonally adjusted, the trend in private-sector payroll growth has remained strong in recent months. After six months at 4.1% (odd given the strong pace of payroll gains), the unemployment rate fell to 3.9% (essentially playing catch-up). Average hourly earnings rose modestly, but the trend (still relatively moderate) is what’s important.

There is a strong seasonal cycle in payroll growth. Following a sharp drop each January (reflecting the end of the holiday shopping season and some school year effects), unadjusted payrolls rise sharply from January to June. The pattern this year is in line with that, although mild weather helped in February.

The unemployment rate fell to 3.9% in April, the lowest since October 2000. Labor force participation edged lower, little changed over the last 12 months. That’s actually a sign of strength in the job market, as the demographics (an aging population) implies a natural downtrend in the participation rate. Measures of underemployment continued to improve, consistent with a further tightening in labor market conditions.

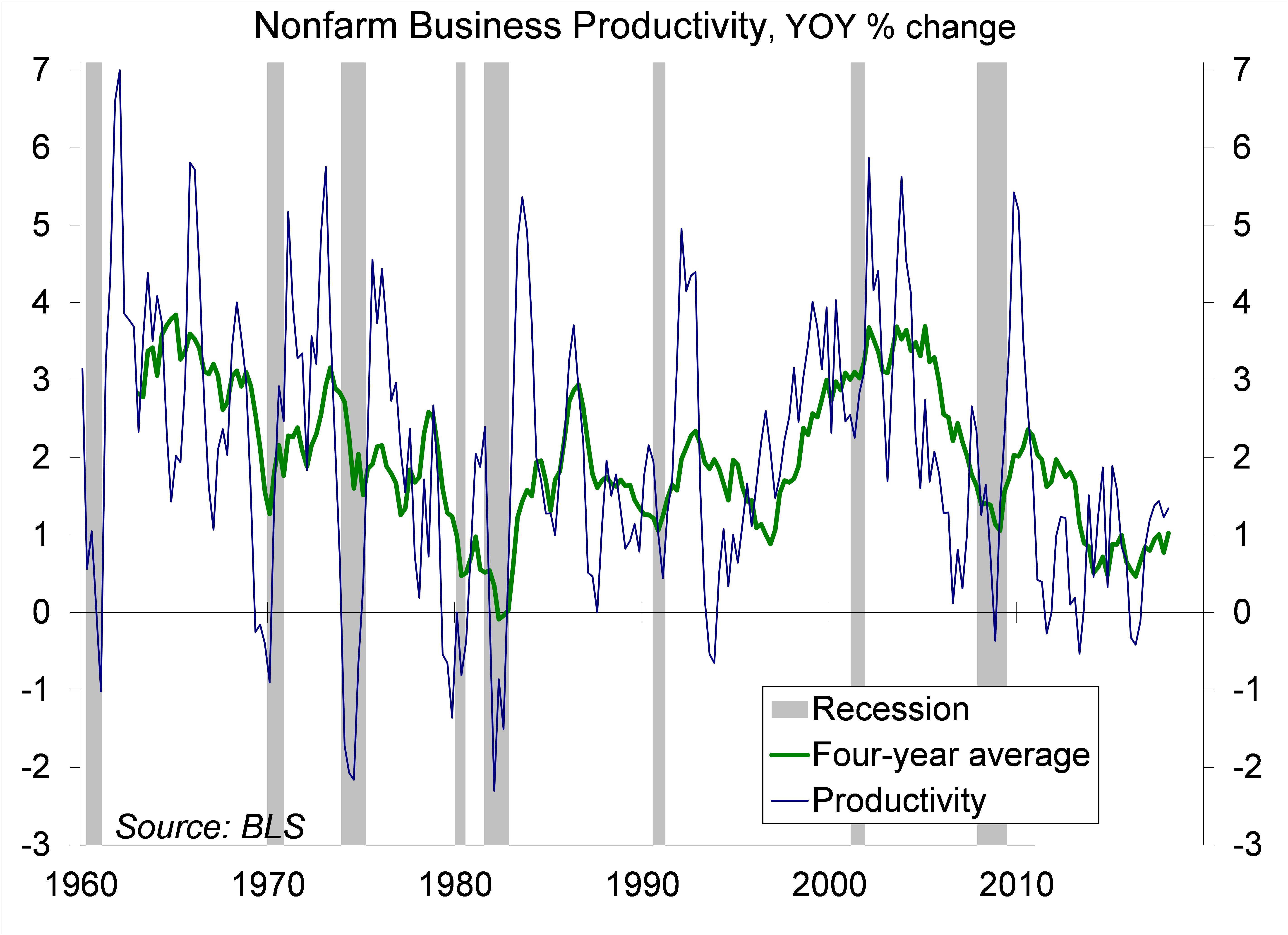

Despite tighter labor market conditions, wage growth remains moderate. Firms, many of which are struggling to find qualified people, are reported to be using creative means to attract workers (perks, signing bonuses), rather than blanket salary increases. One hypothesis is the wage growth is muted because productivity growth is still relatively slow by historical standards. Productivity growth is the single most important variable in the economy, but it’s one of the more poorly measured. You can’t fault the government statisticians for that. Anyone trained in the hard sciences know that once you start multiplying or dividing statistical estimates, the uncertainty rises substantially.

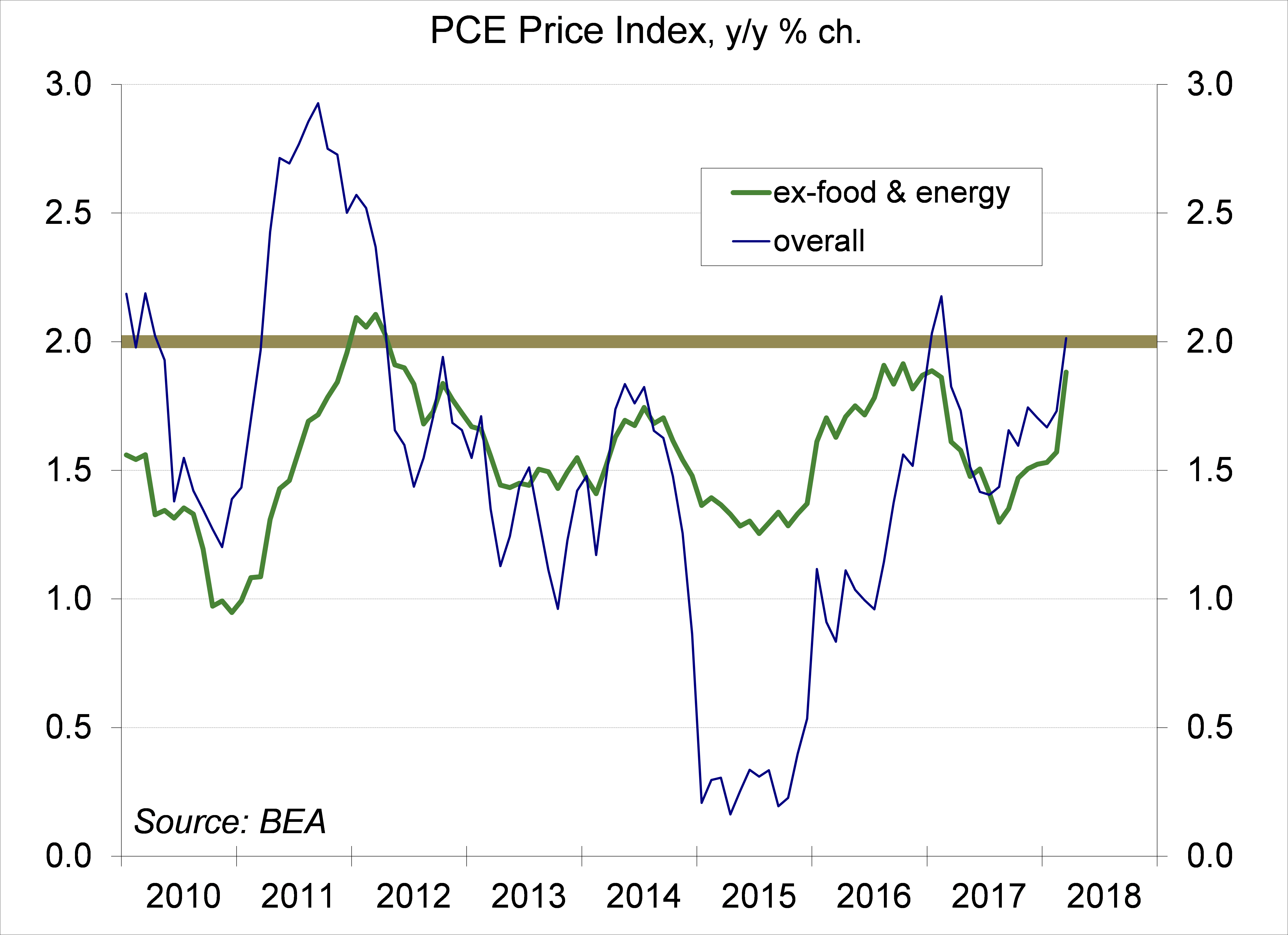

Much was made last week of the pickup in the year-over-year increase in the PCE Price Index. This was not news. The March 2017 drop in wireless telecom services fell out of the 12-month calculation. This should have been well known. The drop in telecom services had biased the headline y/y core inflation figure lower. Fed officials were well aware of this. In fact, former Fed Chair Janet Yellen had talked about it regularly.