Nonfarm payrolls rose less than expected in March (+103,000), but the trend remained strong, well beyond a pace consistent with the growth in the labor supply. Despite a strong trend in payroll growth, the unemployment rate held steady at 4.1% for the sixth consecutive month. Average hourly earnings, which tend to be choppy, rose 0.3%, up a moderate 2.7% from a year ago (for nonsupervisory workers, the trend was 2.4% – little changed over the last two years). By itself, this report was consistent with further gradual Fed rate increases (the market odds of a June 13 hike are about 70%). However, trade policy is likely to have some negative impact on growth, clouding the monetary policy outlook in the remainder of the year.

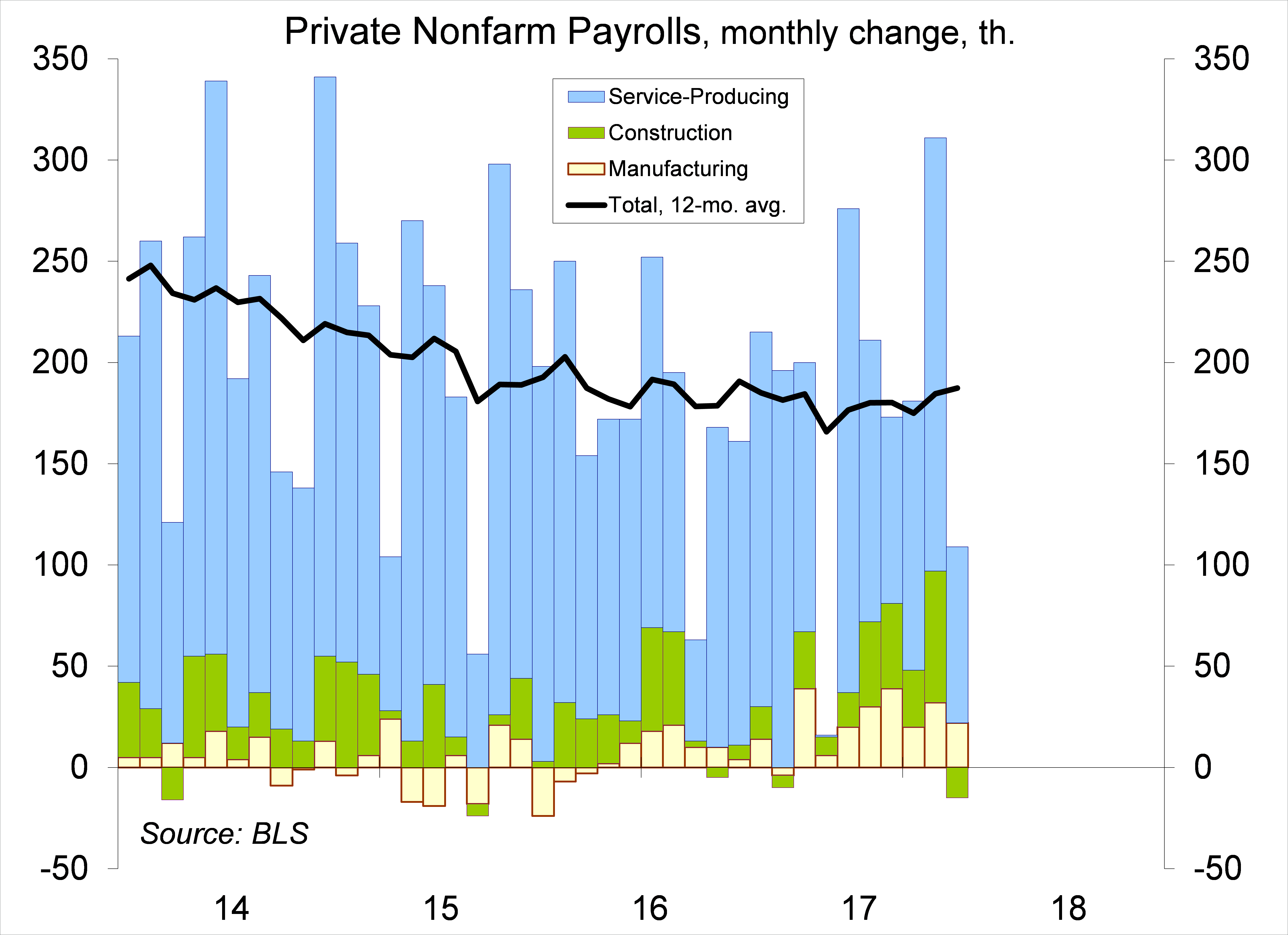

Mild weather boosted construction and retail payrolls in February. The weather was worse in March, trimming payrolls. Job growth for the first quarter as a whole was strong.

Click here to enlarge

We need a little less than 100,000 jobs per month to absorb new entrants into the work force. We’re well beyond that.

Click here to enlarge

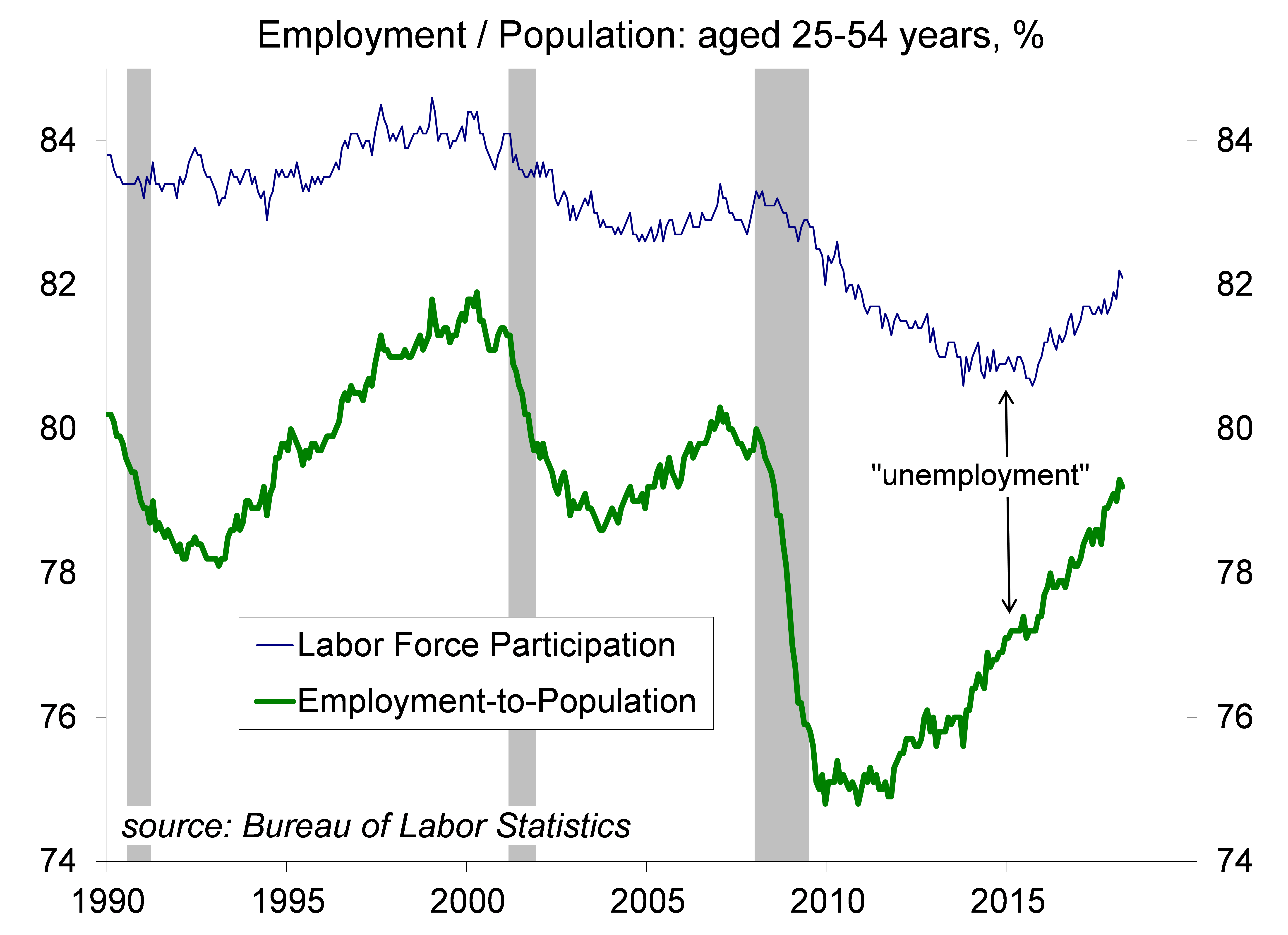

The unemployment rate has been flat over the last six months. The labor force participation rate has been little changed over the last year, but has risen somewhat for the prime age cohort (those aged 25-54). In a late-cycle economy, labor markets tighten, but conditions can be expected to vary across the country. In some areas, the unemployment rate is extremely low, promoting employers to work harder to find qualified workers. In other areas, there is still some slack, but it becomes difficult for workers to relocate as the population ages.

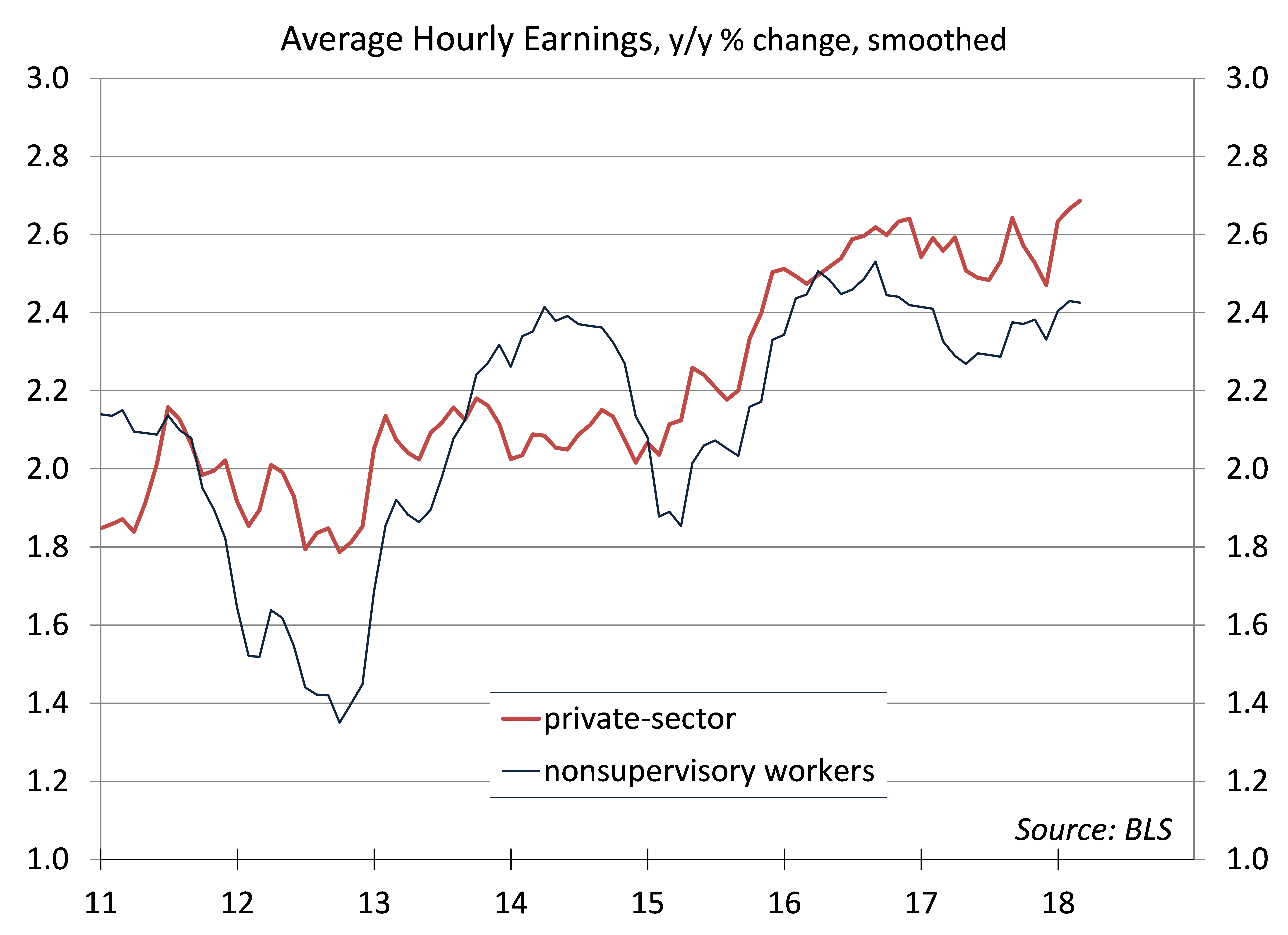

The concern of many Fed policymakers is that tighter labor markets will lead to significantly higher wage growth, which is likely to be passed along to consumer prices. However, trend growth in average hourly earnings has remained moderate, especially for nonsupervisory workers (+2.4% y/y). Still, better safe than sorry, and the Fed can be expected to continue raising short-term interest rates until something interrupts the outlook.

Click here to enlarge

The trade conflict with China has continued to escalate. The country announced retaliatory tariffs against U.S. goods last week and President Trump doubled down on tariffs against Chinese goods. National Economic Council Director Larry Kudlow has tried to downplay the situation. There’s a 60-day waiting period before tariffs go into effect and they may not come to pass if an agreement is reached. However, proposed tariffs are already having an impact, raising input costs and increasing the level of uncertainty for business investment.

Will trade policy uncertainty lead to an adjustment in the Fed’s expected policy trajectory? It depends. Recall that the 25-basis point per quarter pace was interrupted in September due to the hurricanes. Trade policy could have a similar temporary impact (if a bilateral agreement is reached) or it could be a lot worse. Imposing tariffs is equivalent to shooting yourself in the foot. U.S. consumers and businesses will face higher costs and greater uncertainty. Despair is easy. Hope is hard.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© 2018 Raymond James Financial, Inc. All rights reserved.

© Raymond James

Read more commentaries by Raymond James