This is the second of a five-part series presenting 50 dividend growth stocks that I have screened for current fair value. With this article I will be covering 10 additional dividend growth research candidates in addition to the initial 10 that I presented in part 1 found here.

Furthermore, I wanted to be clear that these are not necessarily my favorite, nor what I consider the best dividend growth stocks out there. Instead, I believe these 50 research candidates currently represent the small minority of attractively valued dividend growth stocks in today’s highly valued market place. Simply stated, I believe it’s extremely difficult to find good value, especially in high quality dividend growth stocks, considering today’s low interest rate environment.

Nevertheless, that is also not to say that there are not any high-quality dividend growth stocks available. Many of the dividend growth stocks I will be covering in this series are of high quality. Some are Dividend Aristocrats, Dividend Champions and Contenders, etc. Additionally, there are many different flavors of dividend growth stocks I will be presenting in this series. Some are higher yield as we’ve seen with parts 1 and this part 2, however, all 50 possess their own unique characteristics regarding growth and the ability to generate above-average total returns. Therefore, I suggest that the reader pick and choose among the companies presented that will meet their own specific and/or unique goals and objectives.

Price and Value Are Not the Same Thing

The number 1 rule to follow when investing in common stocks is “buy low and sell high.” This rule seems simple enough at first glance, but the seminal question is: how do you know when a stock is low and conversely, how do you know when high is high enough to sell? Of course, the straightforward answer is to apply prudent or sensible valuation principles when evaluating any stock that you are interested in buying or selling.

Moreover, it is also important to understand a couple of additional principles. For starters, a low price does not always indicate a low valuation. Conversely, a high price does not necessarily indicate a high valuation. It always comes down to price relative to fundamental value – past, present and perhaps most importantly future. However, it’s imperative to consider that past is easy enough to examine as is the present, however, the future always contains a level of uncertainty.

The key point in the above paragraph is that price and value are not the same thing. As I will illustrate with a few following examples, it is possible to find a company with a very low market price but a high valuation relative to fundamentals (i.e. earnings). Note: these are just 2 examples illustrating that price and value are not the same. They are not part of the 10 dividend growth stocks I will be covering later in the article.

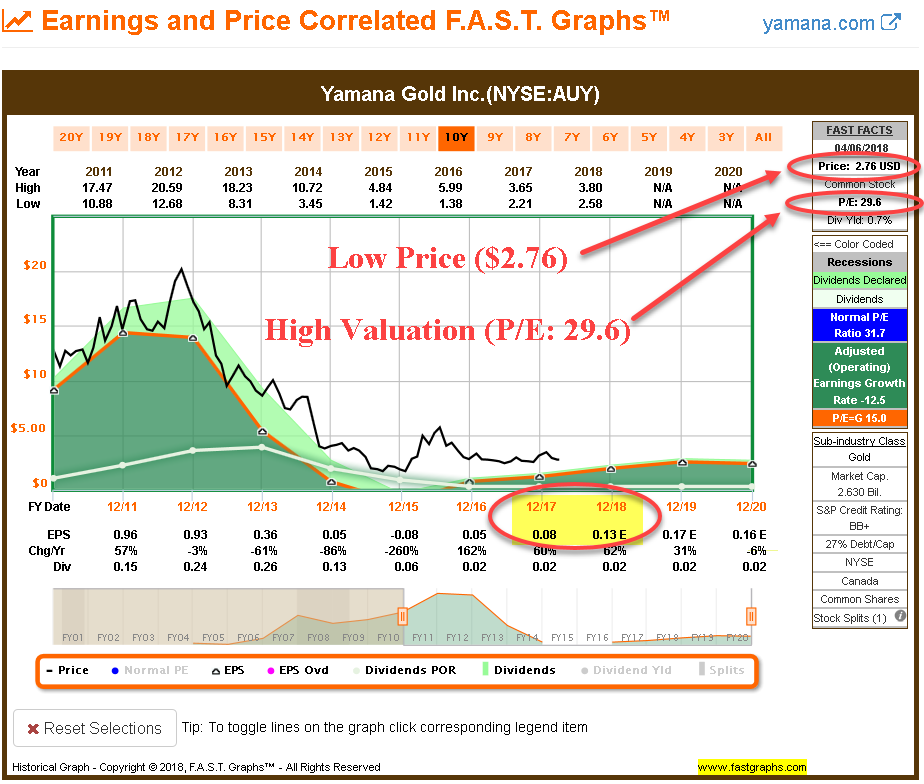

Yamana Gold Inc. (AUY) is a case in point. As you can see from the following historical FAST Graph, Yamana Gold Inc. is expected to earn a mere $.13 per share in fiscal 2018 versus only earning $.08 per share in 2017. Since we are still early in the year, the blended P/E calculation is high at 29.6. Consequently, even though Yamana Gold’s stock price is less than $3 per share, the multiple of earnings you must pay to buy the stock is very high and reflected as a blended P/E ratio of 29.6. As an aside, this number is approximately twice the P/E ratio of 15 that I would be comfortable with.

(Note: In order to determine the level of earnings that the blended P/E ratio calculation is derived from, simply divide the current price of $2.76 by the reported blended P/E of 29.6 and you will get $.0932, or earnings of $.09 per share rounded. This earnings number is simply an extrapolation between last year’s earnings of $.08 per share potentially heading towards the expected earnings of $.13 per share for 2018.)

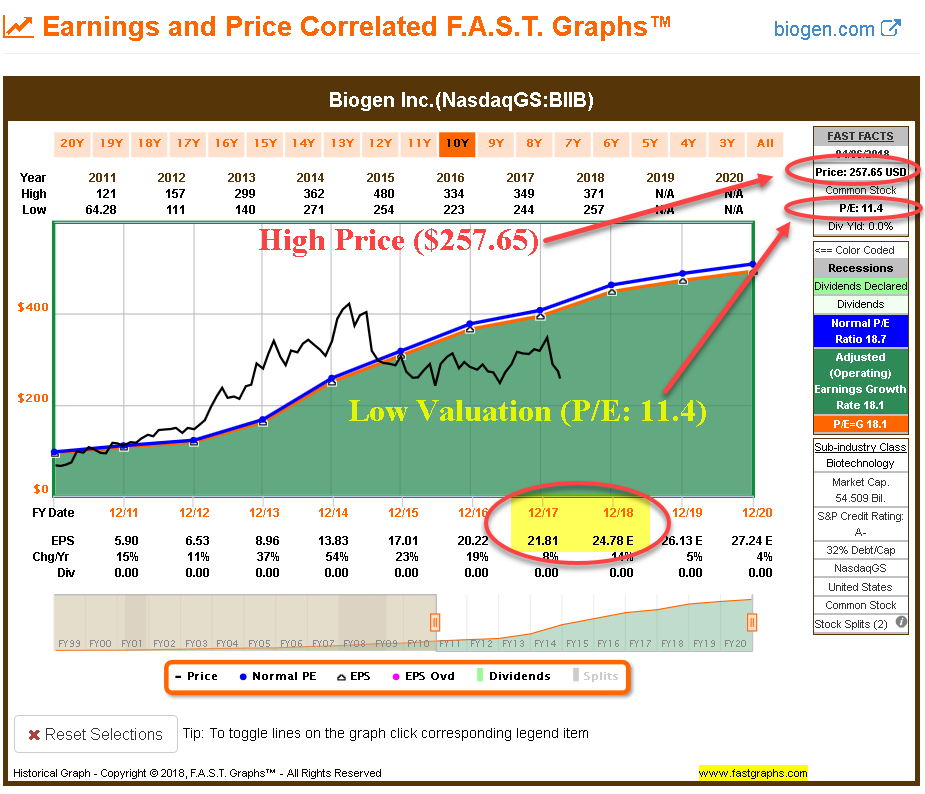

In contrast, let’s look at the biotechnology company Biogen Inc. (BIIB) which trades at a very high price per share of $257.85 per share, which is roughly 100 times higher than we saw with Yamana Gold Inc. above. However, Biogen earned $21.81 in 2017 and is expected to earn $24.78 in 2018. Consequently, Biogen’s earnings are 275 times more than Yamana Gold’s $.09 per share of earnings. Therefore, Biogen can be purchased at a low blended P/E ratio of only 11.4.

Clearly, although Yamana Gold’s price appears very low at less than $3 per share, its valuation relative to fundamentals (earnings) is very high at almost 30 times earnings. Conversely, Biogen’s stock price appears high at over $257 per share, but since it earns between $21 and $25 per share, it’s blended P/E ratio is very low at only 11.4.

Price and value are not the same thing! Price can be high while valuation is low, as we see with Biogen below, and price can be low while valuation is very high as we saw with Yamana Gold above.

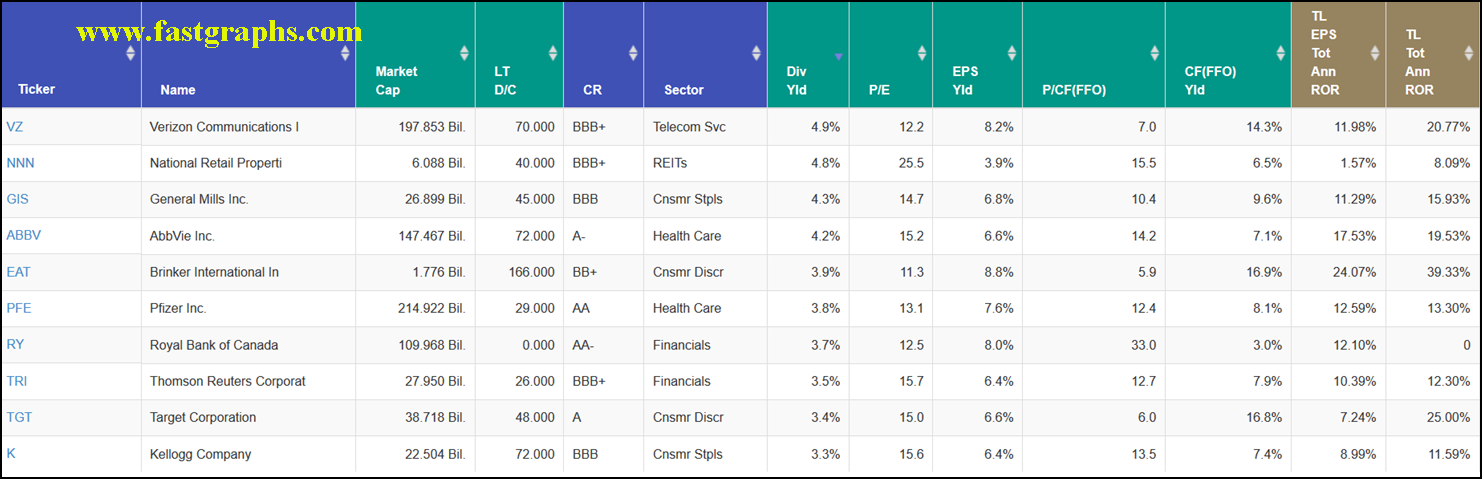

FAST Graphs Portfolio Review: Next 10 (11 through 20 of 50) by Yield

The following portfolio review provides a summary of important metrics for the next 10 highest yielding fairly-valued research candidates. The reader should note that the last 2 columns (light brown) provide annualized total return estimates based on the consensus 3 to 5 years trend line analyst estimates of either cash flows or earnings. The first light brown column provides annual return estimates based on earnings, and the second light brown column provides annual return estimates based on cash flows or FFO (funds from operations) for REITs.

It’s also important that the reader understands that the primary attributes that each of these 10 research candidates have in common is fair valuation coupled with a higher yield than the average company. Moreover, each individual candidate will not necessarily be an appropriate investment for every dividend growth investor. I believe is vitally important that each investor builds portfolios according to their own unique goals, objectives and risk tolerances. For example, some of these candidates might be appropriate to boost the yield of an existing portfolio while others might be more appropriate for investors seeking a higher total long-term return. Therefore, I suggest that readers might pick and/or choose to examine only those that meet their own personal needs. I will be elaborating more on this important aspect in the FAST Graphs analyze out loud video to follow.

FAST Graphs Portfolio Review: Verizon (VZ), National Retail (NNN), General Mills (GIS), AbbVie (ABBV), Brinker (EAT) (PFE) (RY) (TRI) (TGT) (K)

What Are You Investing For?

I believe that every investor should constantly be asking themselves this simple question regardless of whether they are initially constructing their portfolios or managing them on an ongoing basis. This segment was inspired by comments made in part 1 of this series.

The comments I’m referring to were related towards whether my suggestions were outperforming the S&P 500 or not. To these readers it appears that beating the S&P 500 is the only reason to ever invest in a stock. Personally, I consider that a very myopic view of common stock investing. This is especially true for prudent dividend growth investors that are primarily seeking a growing stream of dividend income.

There are many valid reasons for investing in common stocks that are not directly related towards beating the stock market or any other benchmark. For example, if beating the stock market was the only reason to invest then why would people ever invest in fixed income? Investments such as bonds, CDs or other “loaner-ship” investment options are rarely made to beat a benchmark. Instead, fixed income instruments have historically and primarily been used to produce predictable income or to provide safety of principal.

Therefore, to be crystal clear most of the research candidates so far presented in parts 1 and this part 2 are primarily selections offering higher yields than currently available on the S&P 500. However, that is not to say that none of them can outperform the S&P 500 on a total return basis. Some will be, and others won’t. However, I contend that all of them are poised to dramatically outperform the S&P 500 on a current and/or cumulative level of future dividend income.

Therefore, most of the candidates in part 1 and part 2 of this series are offered to those investors that have accumulated large enough portfolios that enable them to live comfortably off their dividend income alone. In other words, they can meet their desired standards of living without ever having to harvest principle. This last statement is supported by the reality that dividends are paid on the number of shares they own regardless of stock price volatility. Investors who find themselves in this enviable position can sleep well at night on the assurance that their income streams are well defined and capable of growing in the future whether their stock prices are rising or not.

FAST GraphsAnalyze out Loud Video

In the following video I will briefly illustrate why I believe each of these 10 research candidates are currently fairly-valued. Additionally, I will provide commentary on what type of portfolio or dividend growth investor they may be appropriate for. Furthermore, a word of caution relative to recent market volatility is also in order. With the stock market fluctuating as much as it recently has been, valuations and current dividend yields are presently very dynamic.

Summary and Conclusions

As I illustrated in the video, the only metrics that each of these higher-yielding research candidates have in common is that they are all currently fairly-valued relative to fundamentals and they are all providing current dividend yields that are higher than the S&P 500. Outside of that, they each possess their own unique attributes and characteristics. Therefore, my suggestion is that the reader focuses their attention primarily on those research candidates that meet their own goals or needs.

Furthermore, I believe that all investors, regardless of their goals and objectives, should apply a disciplined valuation strategy. Being fiercely disciplined to only be willing to invest in any type of stock when valuation is sound is and should be a universally applied principle. Executing a prudent valuation discipline will reduce risk while simultaneously enhancing future returns. However, fair value is only one aspect of a successful investment strategy. When it comes to achieving a certain long-term total return each company’s potential future growth will also be a driving factor.

That last statement will become clearer as I present each of the next three articles in this series. As a rule (and there are always exceptions to every rule), investors generally face a trade-off between growth and income. This same principle applies to risk. In theory, investors must be willing to take on greater risk to achieve higher rates of return. These principles speak directly to why investors need to invest according to their own goals, objectives and risk tolerances.

Disclaimer: Long VZ,GIS,ABBV,EAT,PFE,RY,TGT at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.