Financial market participants took the Fed policy meeting outcome as “dovish,” but the end result was a little more hawkish. The Fed’s revised economic projections weren’t much of a surprise, but they illustrate the thinking behind the expected monetary policy outlook. Of course, there are risks, notably a major misstep on trade policy. Gulp!

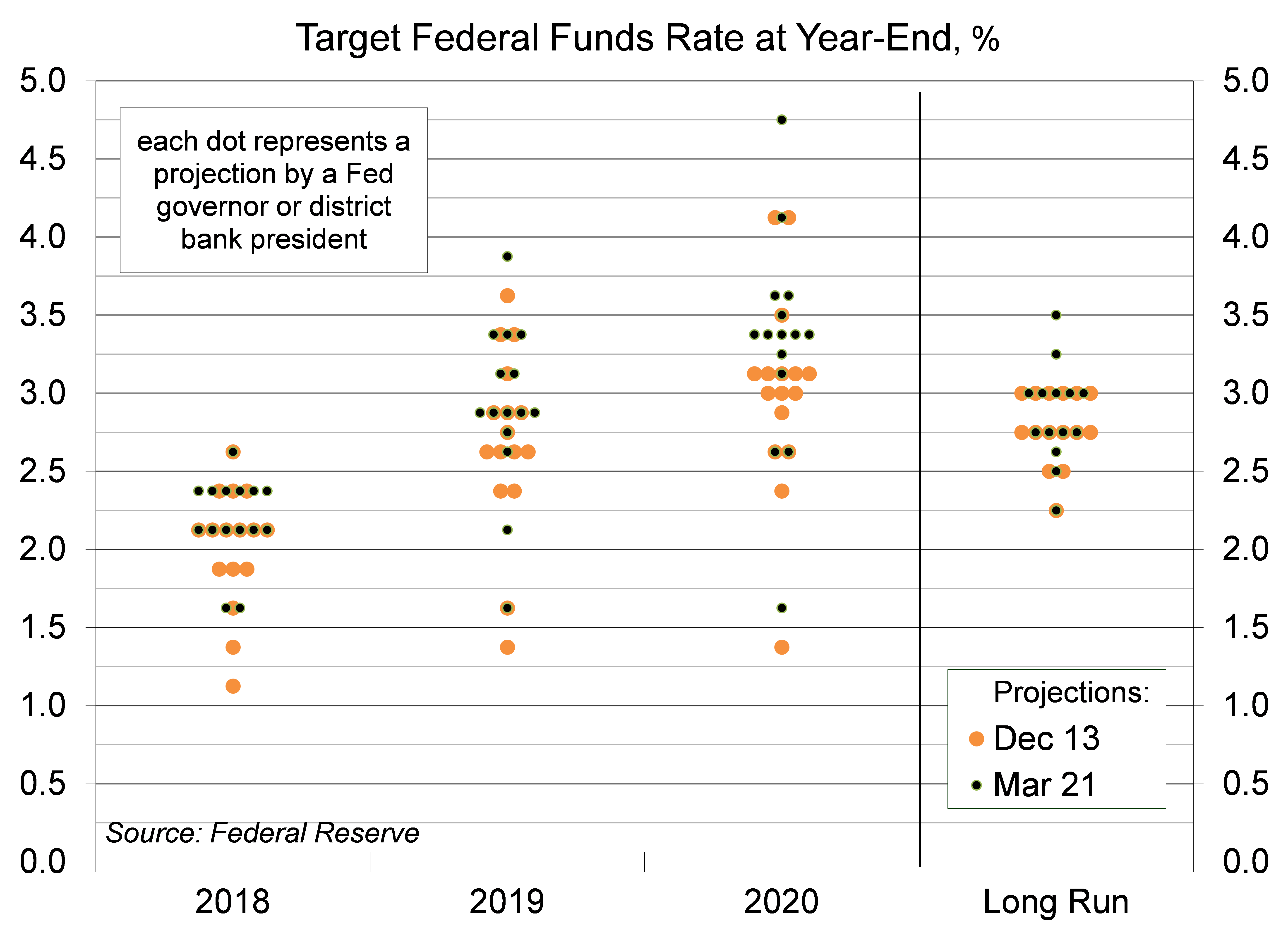

The Federal Open Market Committee raised the federal funds target by 25 basis points to 1.50-1.75%. The dots in the dot plot edged slightly higher, which likely reflected the fact that Janet Yellen is no longer one of the dots. While the median number of expected rate hikes for 2018 remained at three, most (12 of 15) Fed officials were evenly split between three and four.

Click here to enlarge

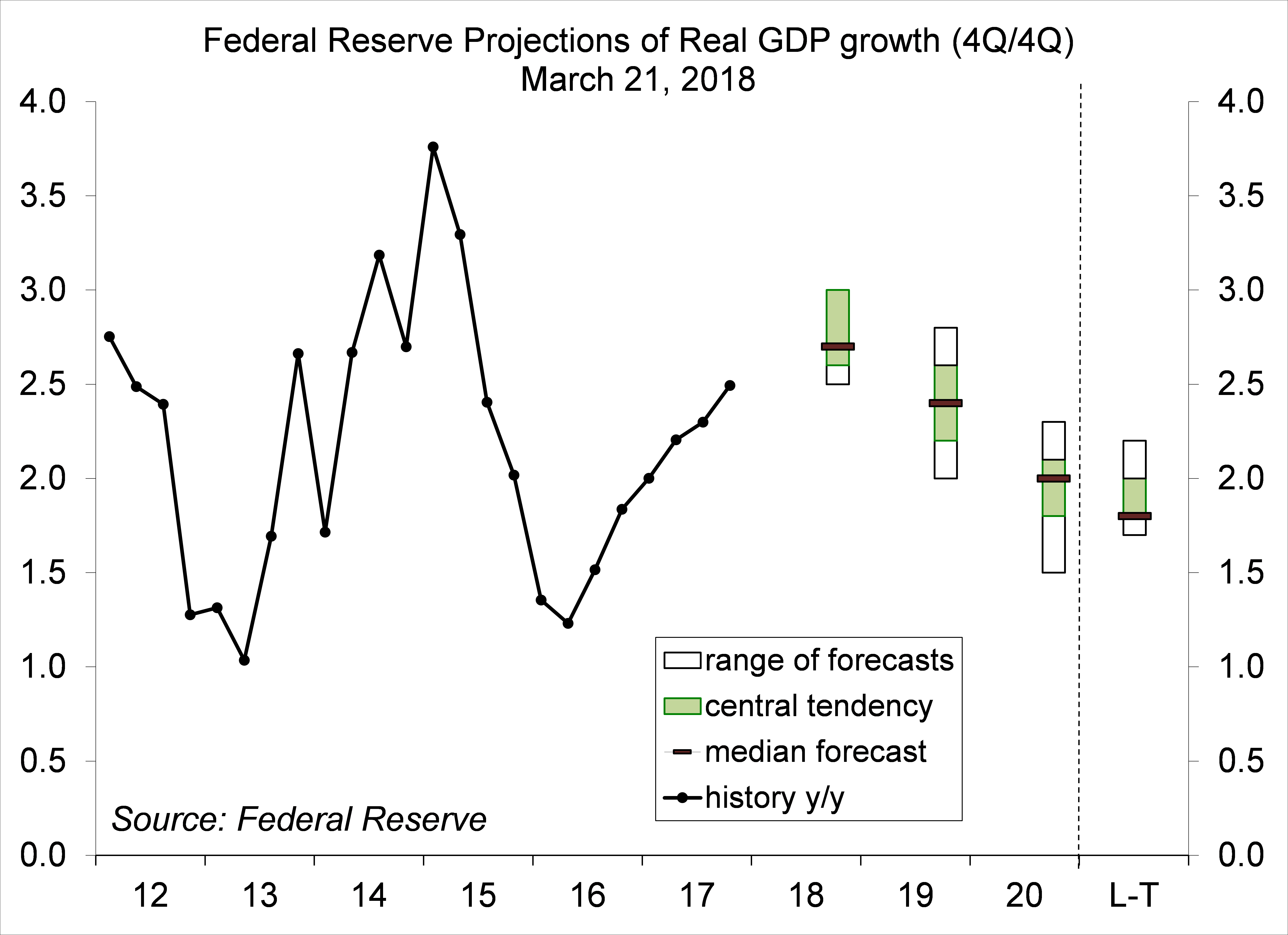

Despite signs of moderation in the pace of growth in consumer spending and business investment at the start of this year, Fed officials expected strong GDP growth in the remainder of the year and into 2019. Growth is then expected to slow to trend as job gains move down to a sustainable pace.

Click here to enlarge

For near-term growth to exceed the longer-term trend, the unemployment rate is expected to fall further. Implicitly, the Fed assumes a relatively flat Phillips curve. Fed officials expect inflation to move toward the Fed’s 2% goal in 2018 and slightly exceed it in 2019 and 2020. This moderate inflation outlook allows the Fed to be gradual in raising short-term interest rates.

Click here to enlarge

The base scenario is for the Fed to continue raising short-term interest rates 25 bps per quarter. There is little chance that it will accelerate that pace, but a number of things could prompt the central bank to pause. An external event, such as the third quarter’s three major hurricanes, is one possibility. A breakdown in the international trading system is another.

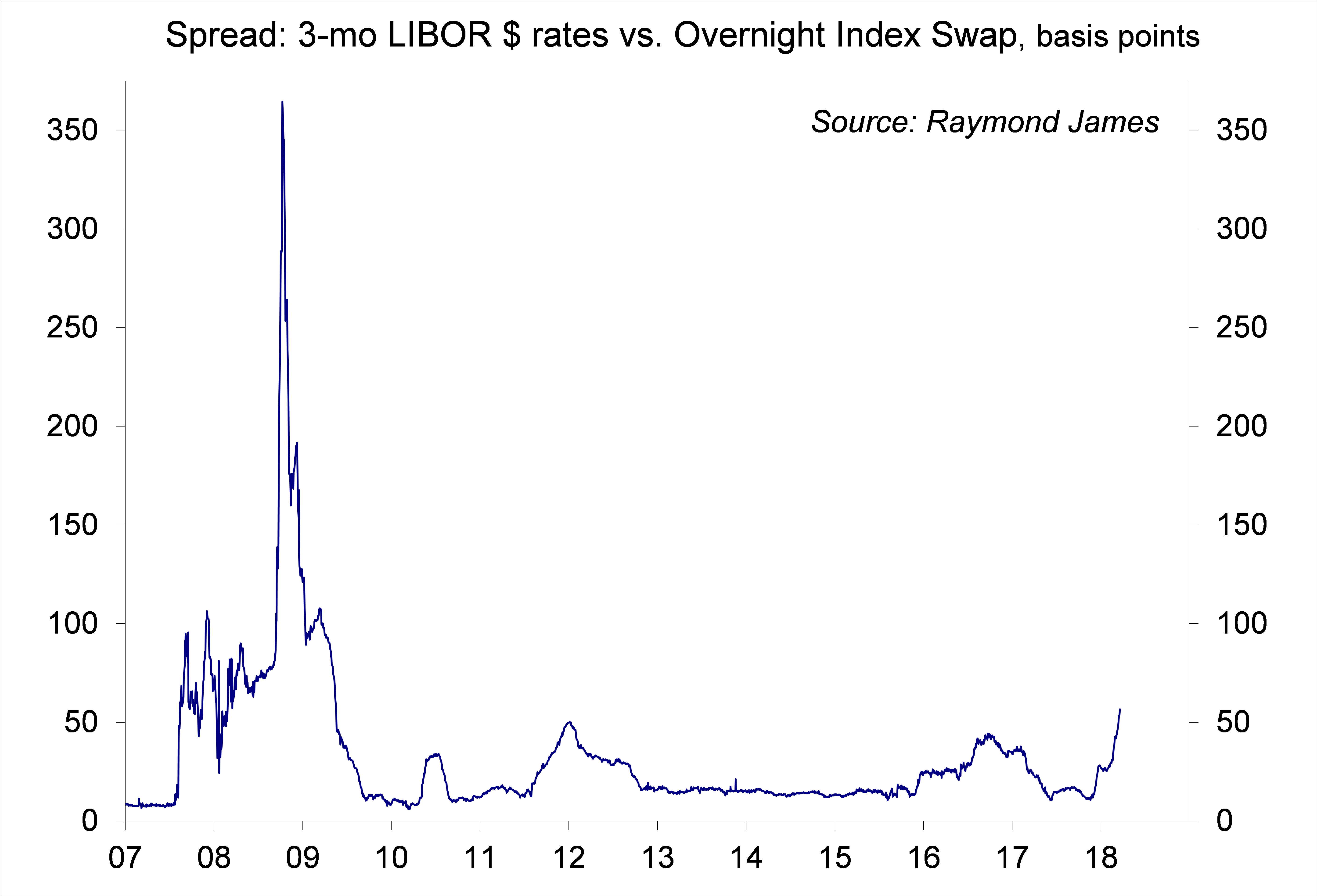

In past years, the Fed looked to the LIBOR-OIS spread as an indicator of financial stress. However, the Fed made no reference to it following the LIBOR scandal of 2012. The spread has been widening and investors should keep an eye on it.

Click here to enlarge

President Trump’s decision to impose tariffs on Chinese goods was not taken well by the financial markets. More importantly, Trump added that “this is the first of many,” suggesting that trade policy worries aren’t going to go away anytime soon.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James