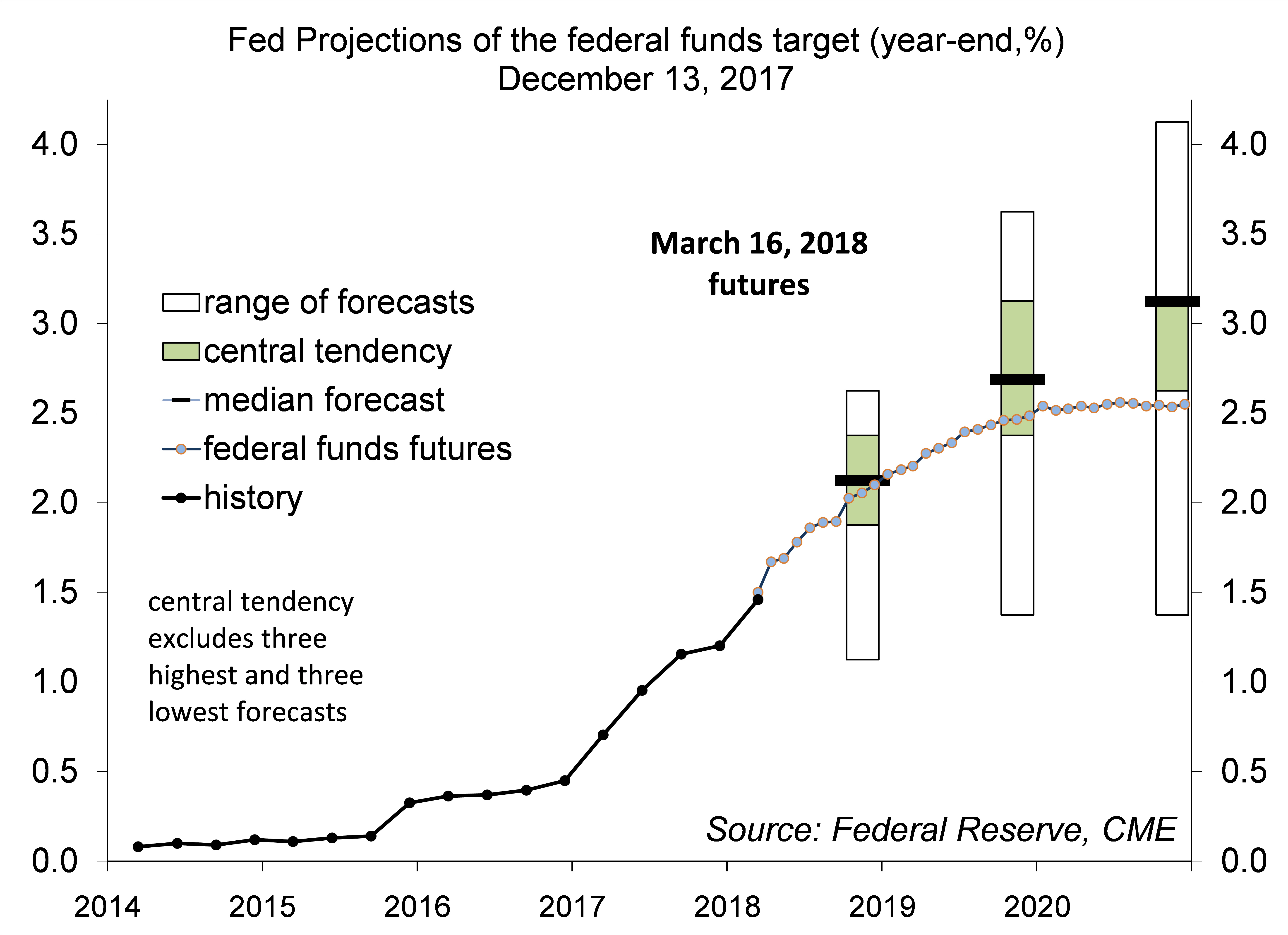

The Federal Open Market Committee is widely expected to raise the federal funds target rate on Wednesday (to 1.50-1.75%). For investors, the key question is the pace of tightening that will follow. We should get some clues in the wording of the policy statement, in the revised Fed projections (including a refreshed dot plot), and in Chair Powell’s post-meeting press conference. Monetary policy decision will certainly remain data-dependent. However, markets are likely to price in 25 basis points per quarter. Looking further ahead, pegging the rate of growth to a sustainable pace will be a difficult task.

Click here to enlarge

In late 2015, Fed officials generally expected to raise short-term interest rates a number of times in 2016, but moved only once. Then-Chair Yellen later indicated that low inflation readings and signs of a tentative slowing in job growth left the FOMC more cautious. While not on a preset path, the Fed raised rates once per quarter in 2017 and seemed set to continue, except for September. Hurricanes Harvey, Irma, and Maria had a significant impact on economic activity. The Fed anticipated a rebound from hurricane effects in 4Q17, but the lull allowed it a safer backdrop to begin its balance sheet unwinding (policymakers were unsure of whether the financial markets might over-react to the initial steps). The bottom line is that the central bank had a couple of excuses for taking a break from the 25-bp per quarter pace of tightening.

The economy was expected to show strong momentum at the start of 2018, with increased uncertainty building in the middle of the year (reflecting the convergence of fiscal stimulus, tighter monetary policy, and job market constraints). Surprise! Most of the major economic data reports for January and February (including retail sales) were on the soft side of expectations, leading to a general decline in economists’ forecasts of 1Q18 GDP growth. Much of that may be weather-related. Expectations for the remainder of the year remain strong.

Every year seems to begin with an inflation scare for the financial markets. CPI inflation figures can be misleading in the early part of the year, partly due to difficulties in the seasonal adjustment. Moreover, the Fed isn’t worried about past inflation. The policy focus is on future inflation. Pipeline pressures in supplies and raw materials remain somewhat elevated, and tariffs aren’t going to help, but this isn’t a major threat to the outlook for consumer prices (as raw materials represent only a modest contribution by the time you get to the consumer level). The bigger concern for the Fed is labor cost pressures. Tight job market conditions haven’t led to a big increase in wage pressure, but the Fed believes that may simply be a matter of time if the job market continues to tighten (and there is plenty of evidence that that is the case). Hence, the Fed remains in tightening mode, but the low inflation readings allow the central bank to be gradual.

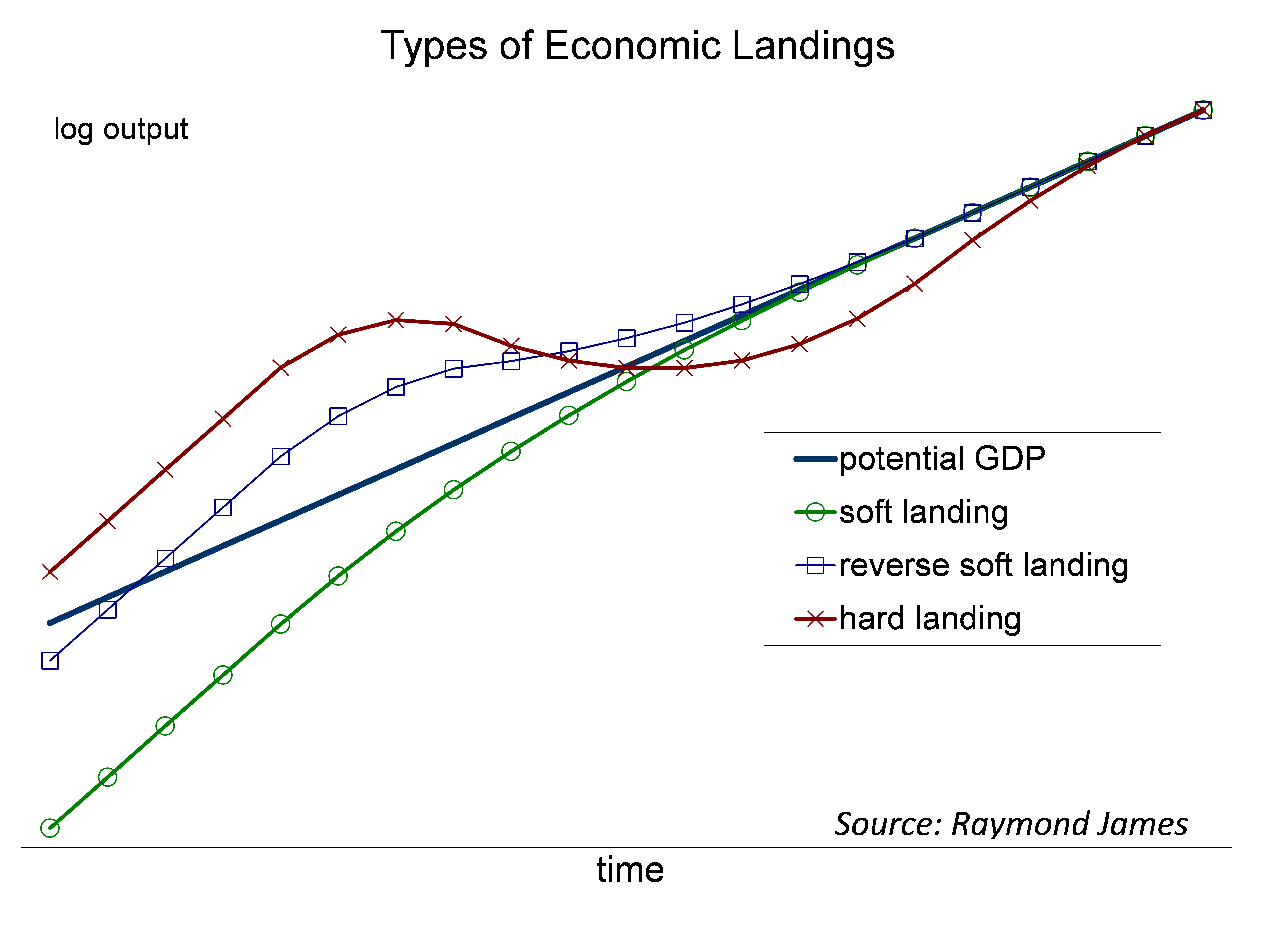

The late MIT economist Rudi Dornbusch once noted that economic expansions never die of old age “asleep in their beds.” Rather, “they are murdered by the Fed.” The Fed seeks to get the economy on a long-term sustainable path. If the economy operates above its potential, inflation will increase. In a soft landing, the Fed raises rates until growth slows to its potential. In a reverse soft landing, where the economy is operating beyond its potential, the Fed attempts to push the economy on a slower path to get back to its potential. In a hard landing, the Fed works harder to slow the economy, resulting in a decline in economic activity (possibly, a recession), and undershoots.

Click here to enlarge

Needless to say, it’s unclear where we may be relative to potential, but as long as job growth remains beyond a sustainable pace (that is, consistent with the growth in the labor force), the Fed is expected to tighten further. Additionally, the economy is likely to be hit by unforeseen developments, such as a potential trade war. Monetary policy uncertainty will remain a key concern for the financial markets in the months ahead.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James