1. February Unemployment Report Showed Jobs Booming

2. A Quick Primer on the US National Debt – Almost $21 Trillion

3. China & Japan Are Reducing Holdings of US Treasury Debt

Overview

We’ll touch on several bases today which should make for an interesting E-Letter. We start with the fact that China and Japan are reducing their holdings of US Treasury debt. As the two foreign countries holding the largest amount of our debt by far, should we be concerned? Maybe yes, maybe no. I’ll give you my thoughts.

Before we get to that discussion, let’s quickly review last Friday’s much stronger-than-expected unemployment report which should make it a slam-dunk that the Fed will raise short-term interest rates by another 0.25% at its upcoming policy meeting next week on March 20-21.

February Unemployment Report Showed Jobs Booming

On Friday the Labor Department’s Bureau of Labor Statistics reported the US economy added 313,000 net new jobs in February, far more than the 200,000 expected. The official unemployment rate remained at a 17-year low of 4.1%. Jobs numbers for January and December were revised higher than previously reported.

The civilian labor force rose by 806,000 in February, and the labor force participation rate increased by 0.3 percentage point to 63.0%.

At the same time, average hourly earnings grew less than expected, ticking only 0.1% higher, or 2.6% on an annualized basis. That more modest wage growth tempered some market fear of inflation after stronger-than-expected wage growth in January helped trigger a sharp correction in stocks in early February.

With the much stronger-than-expected job growth last month, odds are above 90% that the Fed Open Market Committee (FOMC) will vote to increase the Fed Funds rate by another quarter-point at its policy meeting next week which concludes on March 21. If so, the Fed Funds rate target range will rise from 1.25%-1.50% to 1.50%-1.75%.

For some time, the thinking has been that the Fed will hike its key interest rate three times this year. However, new Fed Chairman Jerome “Jay” Powell hinted in congressional testimony last month that the FOMC may consider four rate hikes this year if the economy remains strong or if it looks like inflation is set to rise more than currently expected.

Now let’s move on to our main topic for today.

A Quick Primer on the US National Debt – Almost $21 Trillion

To begin this discussion, I should point out that the US national debt is rapidly approaching $21 trillion ($20.9 trillion), well over 100% of our annual Gross Domestic Product of $19.7 trillion as of the 4Q of 2017.

I should also point out that our national debt consists of two components: “debt held by the public” and “intragovernmental debt.”

Debt held by the public includes all US debt held by individuals, corporations, the Fed, state and local governments, foreign governments and other entities outside the US government. Debt held by the public was apprx. $14.7 trillion at the end of last year.

Intragovernmental debt includes obligations held by government trust funds including the Social Security Trust Fund, the Medicare Trust Fund, the Federal Financing Bank and other government accounts. Intragovernmental debt was apprx. $6.2 trillion at the end of last year.

Some observers believe that intragovernmental debt should not be counted toward the national debt since it is essentially money that we “owe ourselves.” I have never bought into that argument!

Intragovernmental debt is money that the US government has borrowed (robbed) from the various trust funds; it must be repaid at some point; or it must be rolled over at maturity – just like debt held by the public. So, it must be counted as part of the national debt.

The largest foreign holders of US debt are (in order): China, Japan, Ireland, Cayman Islands, Brazil, United Kingdom, Switzerland, Luxembourg, Hong Kong and Taiwan. China and Japan are by far the largest holders with apprx. $1.18 trillion and $1.06 trillion, respectively, at the end of last year. Ireland, the third largest, held only $326 billion at the end of 2017.

China & Japan Are Reducing Holdings of US Treasury Debt

Chinese holdings of US Treasury securities are 10.0% below their peak level which was attained in late 2013, according to recent data published by the US Treasury Department. US government debt held by entities in the People’s Republic of China peaked at $1.32 trillion in November 2013, according to the Treasury.

At that time, the total debt of the federal government was $17.2 trillion. That debt included both $12.3 trillion in debt held by the public and $4.9 trillion in intragovernmental debt.

Between November 2013 and December 2017, Chinese holdings of US Treasury securities dropped from their peak of $1.32 trillion to $1.18 trillion – a decline of apprx. $140 billion – or just over 10%.

Japan’s holdings of US government debt peaked at $1.24 trillion at the end of November 2014. As of December 2017, Japan’s holdings were $1.06 trillion – a decline of $180 billion – or 14.5% from their peak.

Should We Worry About China & Japan Reducing US Debt?

Speculation on why China and Japan are reducing their holdings of US Treasuries is literally all over the board. Some of the arguments are actually amusing, especially those claiming it is a lack of faith in President Donald Trump and concerns about his latest anti-trade policies.

Ditto for concerns that it’s due to the weak US dollar over the last year. China and Japan began reducing their US debt holdings in 2014, and the US dollar gained significantly in value from late 2014 until early last year. While the dollar has weakened over the last year or so, this is not the main reason China and Japan have been reducing their holdings of US debt since 2014.

The US dollar ended 2017 with its worst annual performance since 2003 on expectations that central banks around the world are preparing to end quantitative easing policy measures they adopted to combat the 2008 global credit crisis and the recession that followed.

Another theory which makes more sense is that China is reducing its holdings of US debt in order to counter its strengthening currency, the yuan. Most forecasters see the yuan stabilizing this year, in which case China would naturally cut back on its purchases of US debt.

The Japanese yen has been rising this year but for different reasons, and the Japanese government is not altogether happy about it. Japan’s fiscal year ends on March 31, and most forex analysts expect the yen to remain strong at least until then. Japan is also increasing its foreign currency holdings in Europe and India.

While overseas central banks are expected to roll back their Treasury exposure this year and next, private offshore investors have shown a growing appetite for US dollar-denominated investments such as stocks and corporate bonds amid an improving global economy.

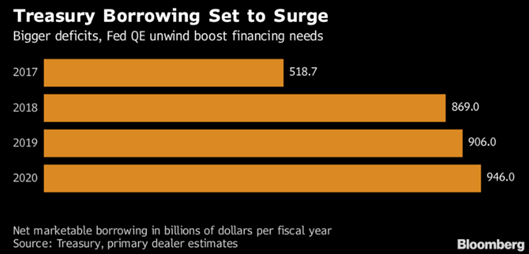

That’s a good thing since US government debt sales are set to increase significantly over the next few years as our annual budget deficits are projected to balloon as illustrated below. So, it will be essential that private investors – including hedge funds, US households and foreigners – step up their purchases of US Treasury debt, as is expected, over the next several years.

The bottom line is that I wouldn’t worry about the fact that China and Japan have reduced their holdings of US Treasuries modestly over the last few years. Both countries remain the largest foreign holders of our debt by far, and they have no incentive to disrupt the largest and safest sovereign debt market in the world by dumping dollars. If that changes, I’ll let you know.

All the best,

Gary D. Halbert

Forecasts & Trends E-Letter is published by Halbert Wealth Management, Inc. Gary D. Halbert is the president and CEO of Halbert Wealth Management, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, Halbert Wealth Management, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management