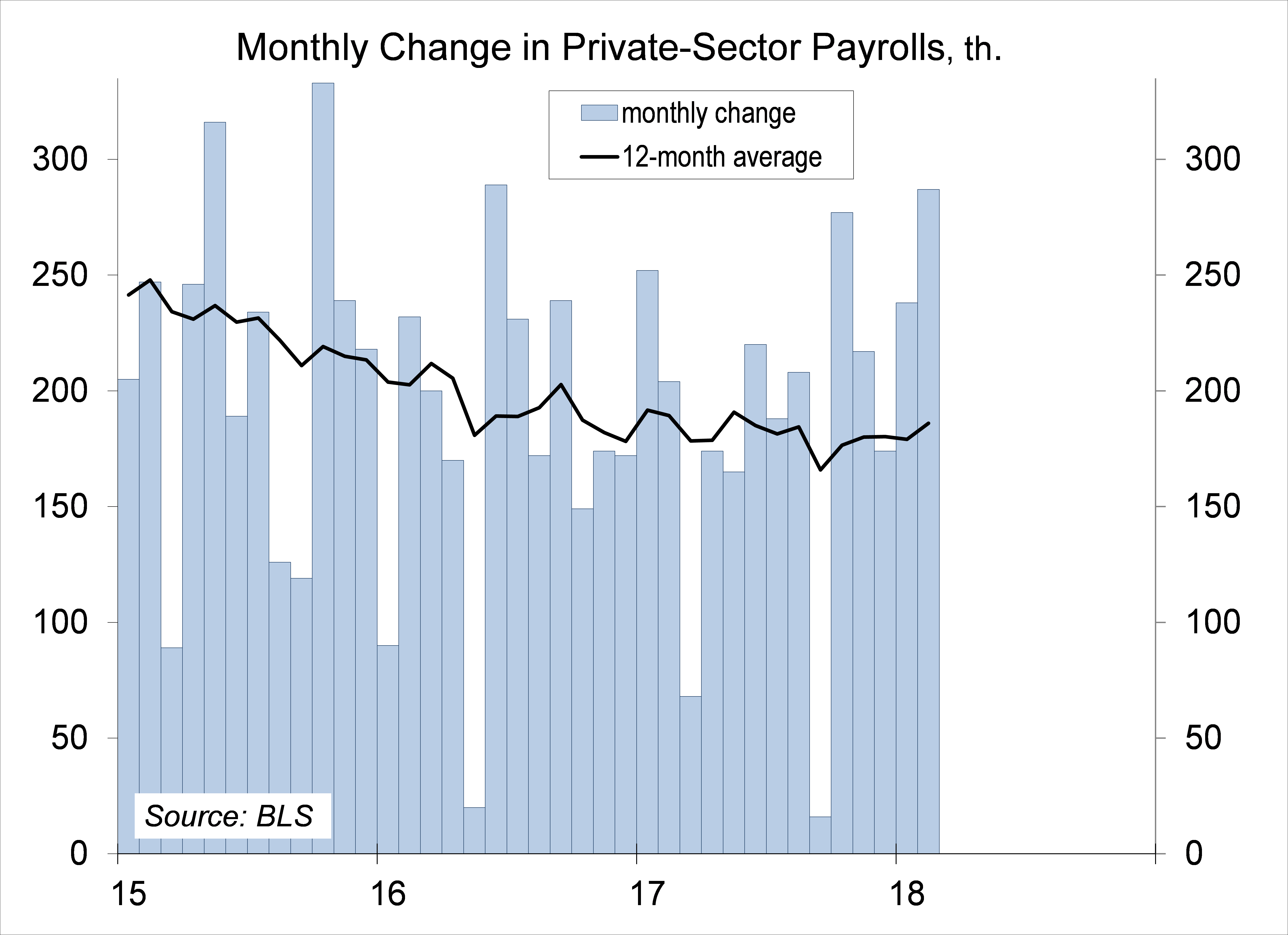

Nonfarm payrolls rose by 313,000 in the initial estimate for February, with a net revision of +54,000 to December and January. The unemployment rate held steady at 4.1%, despite a rise in labor force participation. Average hourly earnings rose a modest +0.1%, continuing along a moderate trend (3-month average up 2.7% y/y). What does this mean for Fed policy?

Click here to enlarge

There appear to be some seasonal quirks in the February payroll data. Prior to seasonal adjustment, retail payrolls fell by 130,000 (vs. -226,000 a year ago), while local government education rose by 250,000 (vs. 205,000). Still, there were solid gains in construction, manufacturing, and temp-help services.

Click here to enlarge

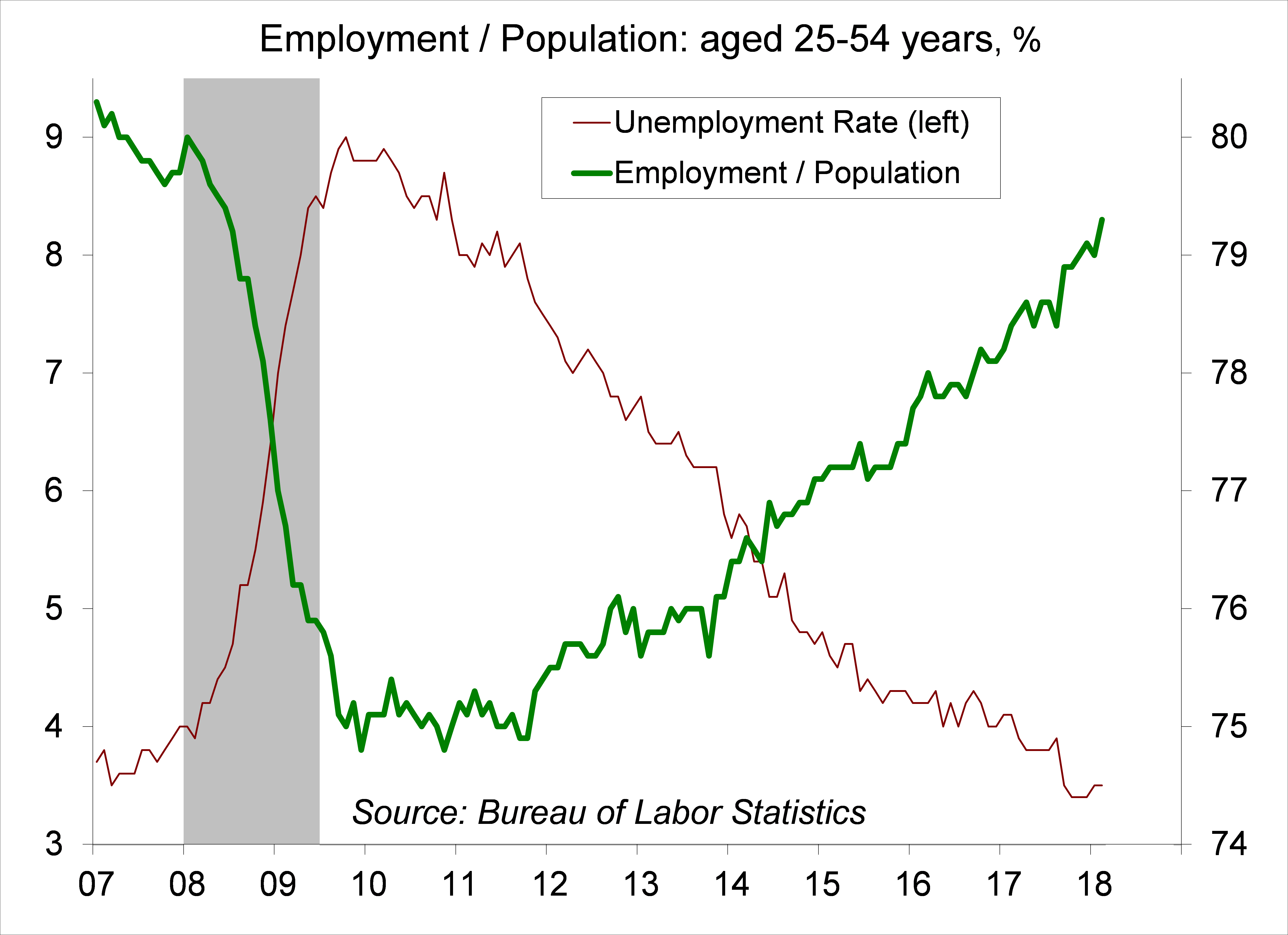

Despite strong job growth, the unemployment rate has been essentially unchanged since October. Labor force participation increased in February, suggesting that there may have been more slack in the job market than was commonly believed, but it’s only one month and the strengthening in the prime-age cohort data is clear (and for the Fed, unsustainable).

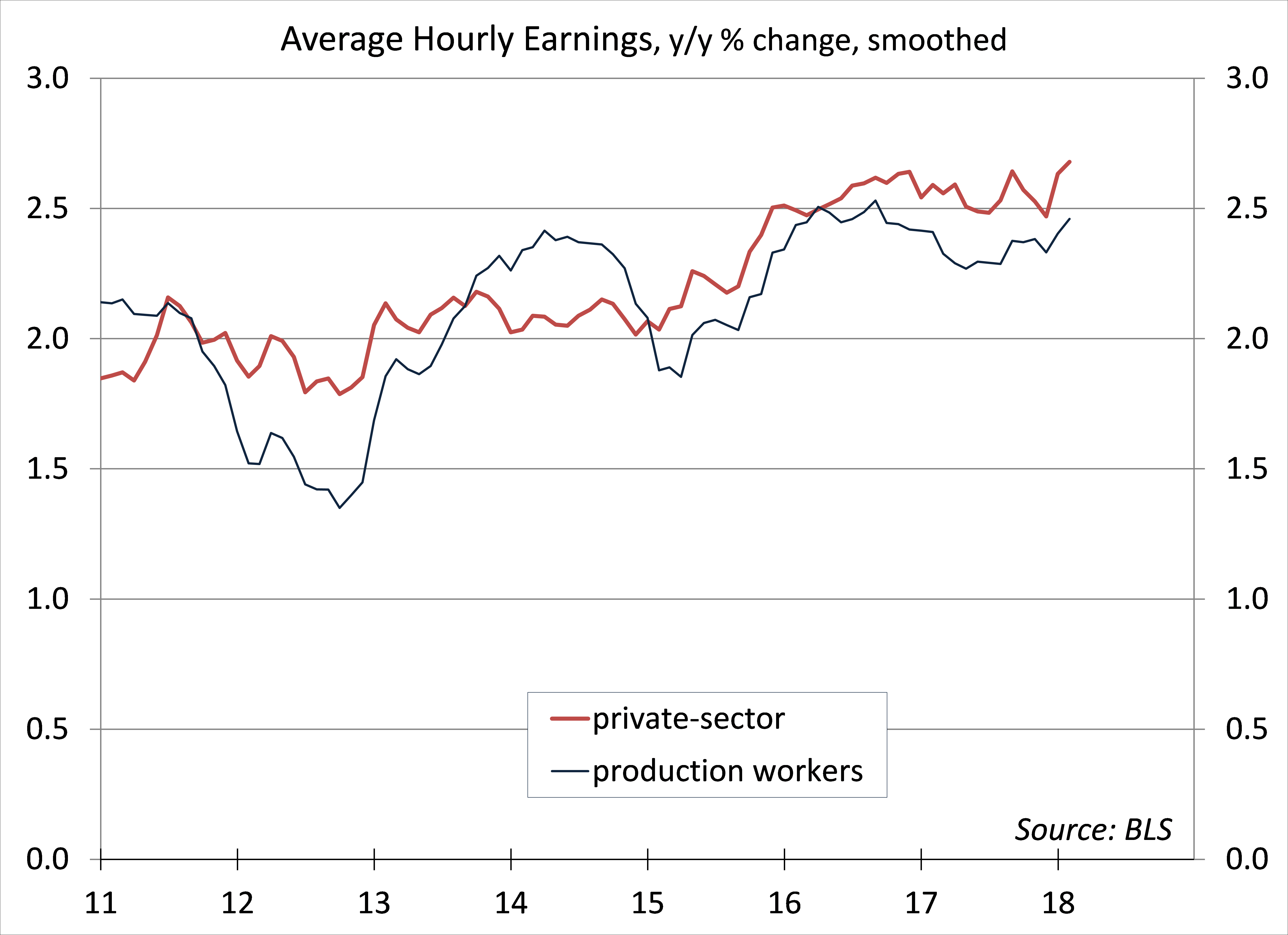

A tight labor market should lead to faster wage growth. Average hourly earnings (AHE) rose only slightly in February. While labor cost pressures are an important factor in the Fed’s policy outlook, financial market participants put far too much emphasis on the monthly figure, which is often revised. Smoothing the data by taking the year-over-year change in the three-month average reduces a lot of the noise. Wage inflation here is moderate over the last year: +2.7% for private-sector employee and +2.5% for nonsupervisory workers, with no sign of a sharp acceleration. That likely reflects a decades-long shift in wage bargaining power away from labor and towards firms. The Fed sees low productivity growth as a likely factor as well.

Click here to enlarge

Whatever job gains we see in steel and aluminum production will be more than offset by losses in downstream industries. The inflation impact will be small if trade conflict remains limited.

Click here to enlarge

A strong job market is good, and inflation pressures remain moderate, but the Fed will see the current pace as unsustainable. You can’t count on reducing the unemployment rate and a widening trade deficit forever.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James