Walmart’s stock price took a bath early last week, and there are a lot of opinions regarding where the stock price now sits. The catalyst was their 4th quarter and fiscal year-end 2018 annual report (note: Walmart has a January 31 fiscal year end). The following headlines courtesy of “Google Finance” illustrate the variance of opinions referenced above:

Walmart Financial Headlines Week of February 19, 2018:

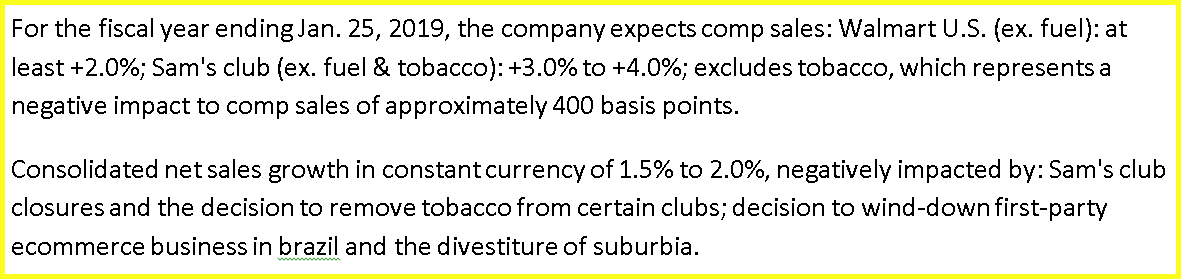

As you can see (from the above), investors reacted both positively and negatively towards the company’s financial release. I personally reviewed the company’s financial reports and drew mixed conclusions. The following “Situation Report” courtesy of S&P Capital IQ provides a synopsis of Walmart’s recent financial statements. I have color-coded each segment according to whether I saw it as positive (green) or negative (red) and if I saw it as neutral I highlighted it in yellow. Therefore, a quick scan of the colors alone clearly illustrate that there were both positive aspects and negative aspects regarding what Walmart reported.

“Situation(courtesy of S&P Capital IQ):

Wal-Mart Stores Inc. reported unaudited consolidated earnings results for the fourth quarter and year ended January 31, 2018.

Why We Sold Walmart

However, as the old adage goes, the devil is in the details. On the other hand, I have often offered a corollary to this old adage that states the “Angels” are also in the details. I feel this is important because if you are only looking for the negative, you are sure to find it. In contrast, if you are only looking for the positive, you are also sure to find it. I believe a balanced approach is more rational where you weigh both the negative and positive aspects of whatever it is you are evaluating.

Therefore, regarding the color-coded results referenced above, Walmart’s fiscal year 2018 financial report came in pretty much as we expected. In summary, we considered Walmart’s financial report rather benign. The company continues to be massively profitable even though the last couple years are showing negative earnings and cash flow growth. Consequently, although the dividend has continued to increase, the rate of growth of that dividend increase has slowed down considerably. The point being that we continue to believe that Walmart (WMT) is a formidable retail giant and possibly one of the few with the resources capable of challenging Amazon.

So if we feel that way, why did we sell Walmart? The answer is simple – we believe Walmart’s current valuation is excessive regardless of the recent significant price drop. Unfortunately, they do not ring a bell at market tops or bottoms. Nevertheless, due to its rapid run-up in price in calendar 2017, we placed it on our “sell watch list.” Therefore, we were poised to take action after we had the chance to review the fiscal 2018 (Walmart’s fiscal year ends in January) financial results.

At this point, it’s important to share that my general policy and philosophy regarding stocks on my “sell watch list” are to wait for the quarterly (or in this case annual) financial results are published. Frankly, there is an undefinable risk and reward potential with the execution of that policy. From my point of view, I feel I only get real information when the financial reports are published. In between those 3 month periods of time, most of what is available is mostly either speculation or mere opinion. Of course, this excludes any pre-filing material event that may occur such as spinoffs, mergers, etc. But in the absence of anything material happening, the company’s quarterly and annual filings are where the most relevant information and insights into the company’s financial strength and/or weakness can be found.

The risk reward potential cited above relates to how Mr. Market might respond to a company’s financial releases. Over my career, I have seen what I considered great financial reports stimulate a significant selloff, and I have seen what I considered weak or poor financial reports stimulate a significant rally in the price of the shares. Consequently, there is always a “crapshoot guess-timate” of how the market might react. In the case of Walmart’s recent report, the reaction was negative, and it could be argued that I should have sold before the report was published. In 20/20 hindsight, that would be a true statement.

However, as I will clearly illustrate later in the video portion of this article, Walmart’s stock price carried great momentum since the beginning of 2017. Therefore, it seemed like a good idea to hold on until the report was published. Of course, from a short-term perspective, that was a bad decision. On the other hand, from a longer-term perspective I was still able to exit the position with a positive long-term rate of return.

Over the years, I have been rewarded many times, and I’ve also been punished many times for waiting for the financials to be actually released on a “Sell Watch” holding. Nevertheless, I feel my decision was a good one even though it wasn’t a perfect one. On February 22, 2018 we sold Walmart from our entire client portfolios solely based on what we considered excessive overvaluation.

FAST Graphs Analyze Out Loud Video: Walmart

There are many so-called investors who eschew reviewing historical fundamental operating results on the notion that history is merely rear-view mirror thinking or 20/20 hindsight. I believe they are drastically short-changing themselves. Although it is true that we can only invest in the future, it is equally true that we can learn a great deal from carefully examining the past. Because, as Sir Winston Churchill so eloquently put it:

“Those who fail to learn from history are doomed to repeat it.”

Furthermore, they say that a picture’s worth 1000 words, but if true, then how many words is a video worth? I don’t have an exact answer, but I assure you that a well-produced video analyzing a company’s fundamental strengths and weaknesses is worth many many more. With the video format and the utilization of FAST Graphs (the fundamentals analyzer software tool) I know that I can provide a more comprehensive fundamental evaluation and analysis than I could with a long article comprised of thousands of words. Therefore, the following video highlights the current valuation of Walmart relative to its recent fall in stock price.

Summary and Conclusions

In conclusion, I feel it’s important to state that my general opinion of Walmart as a business and as an investment opportunity has not changed. What has changed is the high valuation that occurred in the height of concerns over retail due to the real and/or potential Amazon effect. As I stated previously, Walmart is one of the few retailers big enough and strong enough to take on Amazon. However, that is not to say that they will succeed. On the other hand, the future growth and value of Amazon itself is also under question.

Finally, my original decision to invest in Walmart was based on a reasonable valuation at the time and a growing dividend income stream. As I indicated in the video, I liked their financial strength and the long-term record of growth. But as I have stated many times before, even the best companies can become overvalued or undervalued. Therefore, no matter how much I believe in a business, I will not invest – and if it gets bad enough I will sell if I think valuation is excessive. If Walmart were to move back into fair valuation – I might reconsider initiating a new position. However, that would only happen after a comprehensive research and due diligence process was conducted at the time.