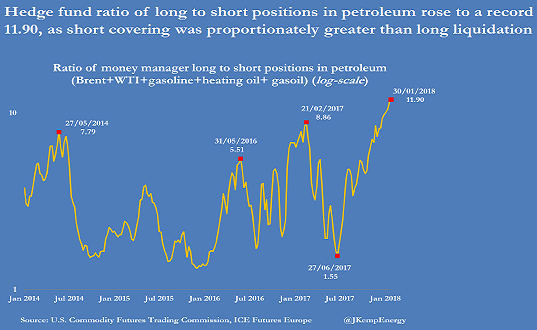

Oil and commodity markets long ago lost contact with the real world of supply and demand. Instead, they have been dominated by financial speculation, fuelled by the vast amounts of liquidity pumped out by the central banks. The chart above from John Kemp at Reuters gives the speculative positioning in the oil complex at its recent peak:

- It shows hedge fund positioning in terms of the ratio of long to short positions across the complex

- The ratio had been at a near-record low of 1.55x back in June last year, before the rally took off

- On 30 January it had risen to a record 11.9x – far above even the 2014 and 2017 peaks

The size of the rally has also been extraordinary. At its peak, the funds owned 1.5bn barrels of oil and products – equivalent to an astonishing 16 days of global oil demand. They had bought 1.2bn barrels since June, creating the illusion of very strong demand. But, of course, hedge funds don’t actually use oil, they only trade it.

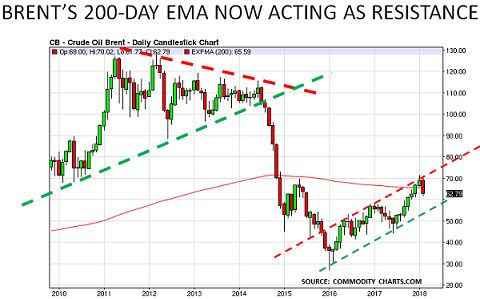

The funds also don’t normally hang around when the selling starts. And so last week, as the second chart shows, they began to sell their positions and take profits. The rally peaked at $71/bbl at the end of January, and then topped out on 2 February at $70/bbl. By last Friday, only a week later, Brent was at $63/bbl, having fallen 11% in just one week.

Of course, nothing had changed in the outlook for supply/demand, or for the global economy, during the week. And this simple fact confirms how the speculative cash has come to dominate real-world markets. The selling was due to nervous traders, who could see prices were challenging a critical “technical” point on the chart:

- Most commodity trading is done in relation to charts, as it is momentum-based

- The 200 day exponential moving average (EMA) is used to chart the trend’s strength

- When the oil price reached the 200-day EMA (red line), many traders got nervous

- And as they began to sell, so others began to follow them as momentum switched

The main sellers were the high-frequency traders. Their algorithm-based machines do more than half of all daily trading, and simply want a trend to follow, milli-second by milli-second. As the Financial Times warned in June:

“The stock market has become a battlefield of algorithms, ranging from the simple – ETFs bought by retirees that may invest in the entire market, an industry, a specific factor or even themes like obesity – to the complex, commanded by multi-billion dollar “quantitative” hedge funds staffed by mathematicians, coders and data scientists.”

JP Morgan even estimates that only 10% of all trading is done by “real investors”:

“Passive and quantitative investors now account for about 60% of the US equity asset management industry, up from under 30% a decade ago, and reckons that only roughly 10% of trading is done by traditional, “discretionary” traders, as opposed to systematic rules-based ones.”

Probably prices will now attempt to stabilise again before resuming their downward movement. But clearly the upward trend, which took prices up by 60% since June, has been broken. Similar collapses have occurred across the commodity complex, with the CRB Index showing a 6% price fall across major commodities:

- Typically, inventory build ahead of price rises can add an extra month of “apparent demand” to real demand

- This inventory will now have to be run down as buyers destock to more normal levels again

- This means we can expect demand to slow along all the major value chains

- Western companies will now see slow demand through Easter: Asia will see slow demand after Lunar New Year

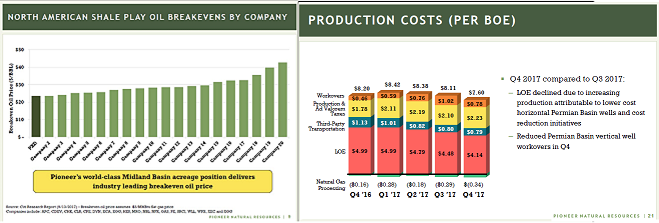

This disappointment will end the myth that the world is in the middle of a synchronised global recovery. In turn, it will cause estimates of oil demand growth to be reduced, further weakening prices. It will also cause markets to re-examine current myths about the costs of US shale oil production:

- As the charts from Pioneer Natural Resources confirm, most shale oil breakeven costs are below $30/bbl

- Pioneer’s own operating costs, typical of most of the major players, are below $10/bbl

- So the belief that shale oil needs a price of $50/bbl to support future production is simply wrong

PREPARE FOR PROFIT WARNINGS AND POTENTIAL BANKRUPTCIES BY THE SUMMEROver the summer, therefore, many industrial companies will likely need to start issuing profit warnings, as it becomes clear that demand has failed meet expectations. This will put stock markets under major pressure, especially if interest rates keep rising.

Smart CIOs will now start to prepare contingency plans, in case this should happen. We can all hope the recent downturn in global financial markets is just a blip. But hope is not a strategy. And the risk of profit warnings turning into major bankruptcies is extremely high, given that global debt now totals $233tn, more than 3x global GDP.

© The pH Report

Read more commentaries by The pH Report