On My Radar: The Volatility Flash Crash Explained

Learn more about this firmMembership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“We are replaying an age-old storyline of financial bubbles that has been played many times before…”

“This market’s current temperament feels so much like either Japan in 1989 or the U.S. in 1999.

And the events that have transpired so far this January make me feel more convinced than ever of this repeating history.”

– Paul Tudor Jones, founder Tudor Investment Corp. (source)

“I believe the precipitous market drop in the last week has little to do with the projected course of interest rates or, for that matter, fundamentals.

It likely was a function of the distorted, dangerous world of new investment products and strategies….

[T]he proliferation of short vol, volatility trending and risk parity strategies when combined with an explosion of leveraged ETFs

and ETNs – many of which were derivatives of derivatives and had no business existing except to please gamblers – had altered the market structure…”

– Doug Kass

ETNs are “exchange-traded notes.” “…There is an interesting thing about ETNs. These are exchange-traded notes, and while I don’t want to get to arcane on you, a key feature of them is that there has to be a bank or a guarantor on the note. Even though we’ve had at least two shortfall ETNs literally blow up and go to zero, the investors in those funds are going to get “something.” If you put in your withdrawal request while there was still a price, there is an extraordinarily good case that you are due your money.

And, of course, the ETN fund doesn’t have any money. But the bank that guaranteed the ETN is on the hook. One of the ETNs was evidently backed by Credit Suisse. Credit Suisse made an announcement before the market opened yesterday morning that they had 100% of their liabilities hedged out in the marketplace. Of course, they didn’t say hedged out to whom, and that will make us all wonder about counterparty risk; but we won’t have answers on that for a long time, and while a significant amount of money is involved, it is not life-threatening to a bank the size of Credit Suisse. More like annoying than life-threatening.” My friend, John Mauldin, wrote in his Outside the Box letter.

It’s been a violent few days as you well know. John and I spoke mid-week and discussed the relative current calm in HY, the losses happening in the managed futures space, risk parity and how the naked “short” volatility trade is blowing up. We’ll try to make some sense of this today.

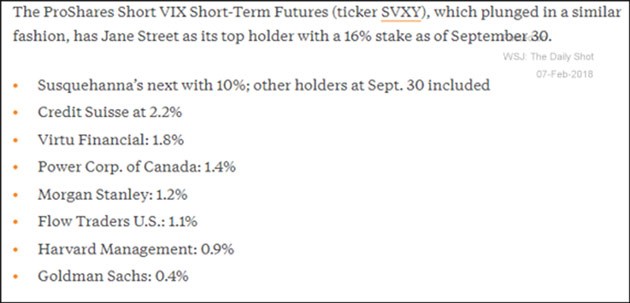

I shared the following list with John and he added with his customary flair, “I submit this list of the largest shareholders in SVXY, one of the short-vol VIX funds. Interesting to see Harvard Management in there. Really? Harvard is reaching for yield?”

Source: The Wall Street Journal, The Daily Shot

More from John:

I was probably making two calls a day to my go-to guys in the high-yield market, to see how high-yield bonds were responding. I think ultimately the collapse in high-yield will precipitate “the Big One.” You just can’t understand how much in high-yield bonds has been sold, how poorly the covenants are managed, and how badly investors are going to get screwed.

You watched this last week as the VIX fell out of bed. I am telling you that what is going to happen in the high-yield market is going to be more – much more – of the same. It’s going to seemingly fall out overnight. The bids are going to disappear, and high-yield bonds are going to be sold to what are essentially distressed-debt funds at distressed-debt prices.

Further, as we get into late 2018 and then into 2019 (not to mention 2020), the amount of high-yield debt that has to be “rolled over” becomes significant. And it is obviously going to have to be rolled over at higher interest rates. There will be some companies that will be able to handle those rates, and there are some companies that are simply way out over the tips of their skis, trying to schussboom down a double black diamond slope, and the outcome is going to closely resemble one of those “agony of defeat” moments from the old Wide World of Sports TV show. We’re talking some spectacular face plants. You do not want to be involved, unless from the short side, when that happens.

What’s interesting with this quick 10% mini-crash (maybe more after today as the markets are heading south again midday) in equities is that high-yield spreads have remained stable. Spread is the difference in yield you get for high-yield bonds over the yield you get for high-quality bonds. High-yield bonds tend to act as a leading indicator for the equity market and do a good job at predicting oncoming recession. When things turn bad, HY prices decline and yields spike higher. HY tends to be a very good lead indicator for equities. The good news is we are not seeing HY yields spike.

Today’s environment reminds me a great deal of what was going on with subprime in 2006 when we first caught on to the craziness. In early 2007, an insider told us of the Bear Stearns hedge fund problems with mortgages. That news later broke. Those problems were the tip of a great big iceberg. One hedge fund way off-sides… His problem was symptomatic of a much larger problem. Few made the connection.

By 2008, there was so much capital exposed to the same risks. Banks were massively leveraged. Mortgaged Backed Securities, Collateralized Debt Obligations and slices and dices of various repackaged derivative products woven into an incestuous web of global counter-party risk that created endless liquidity, so much so that everyone could get financing to buy a home, take out a second mortgage. What could go wrong? Then boom.

Same today? I don’t think so, but with high valuations comes high risks. We sit just off record high valuations, record high margin debt and record high investor optimism. Some color on the last week:

- The DJIA and S&P 500 entered correction territory for the first time in two years on worries over rising interest rates and resurgent volatility. The blue-chip index Thursday ended 1,032.89 points lower and is now down 10% from its January high.

- A shaky day in the bond market appeared to cross paths with equities as they spent much of the session deep in the red. Stocks in Europe and Asia were on pace for their worst week in two years; in China, shares Friday suffered their biggest one-day drop since a 2015 rout.

- Critics blamed the week’s price swings on risk-parity funds, an obscure investment strategy pioneered by the world’s largest hedge fund, though some outperformed the broader market.

The immediate concern is all of the speculation around VIX futures and related products. The short volatility strategy. Even mom and pop can click and trade the exotic VIX and XIV ETFs. But it’s a game of picking up nickels in front of a steam roller and I bet they don’t fully understand the risks. Well, more like hundred dollar bills but same steam roller. Because of the way the volatility futures decay in value each month, it’s a pretty consistent win. XIV is the short VIX ETF that captures the monthly decay. Own it and you win, until you may lose it all in one day. It’s so easy, you make money most of the time until you get lulled to sleep and run over. All gone.

Imbedded in the ETF structure are notes tied to futures contracts. It should read, “For professionals only” and “Sometimes not even for some professionals.” Note this:

- There was over $660 million invested in the LJM Preservation and Growth Fund late last week. Investors lost 81.97% in a few short days. Preservation? Only if the swarming lawyers have their day, but how is the manager going to pay back $500-plus million. Where was the due diligence team?

Look away for a second and you get hammered. Investors have been herding into passive index funds the last few years. Much like the March 2000 high, record inflows into equity funds and ETFs marked the January 2018 high. Do investors have a quicker trigger today orare this week’s record outflows due to the forced selling of the volatility trade? I’m not sure retail is bailing out just yet. I suspect the latter. But it sure feels like the an early warning shot similar to the Bear Stearns hedge fund manager in 2007, except this time the concentration is in passive index products and volatility driven signals. Hope I’m wrong, let’s take note.

Where’s the bottom to this flash crash? I suspect we are close. I spoke with an advisor client this morning and suggested that the experienced traders and hedge fund managers know there are millions of stop-loss orders placed at the 200-day moving average line. I expect more than a few hedge funds might flood the system with short-sell orders, trigger the 200-day MA stop-loss orders and create a final washout. I think that is probable. Absent recession, that may release selling pressure and mark a short-term low. We’ll see.

Here’s the chart on the S&P 500 Index. The 200-day MA line is in red. Target is 2539.06… Not sure if today will mark the low but we are testing the line. Watch for a flush out around that 200-day MA line. All in all, I believe the worst is over. No guarantees, of course.

Source: StockCharts.com

As a final note on the 200-day MA line, I’m a fan of stop-loss risk management, but I’m not a big fan of the 200-day line because it is so widely followed. Too many professionals are poaching it. If you are trading the major indices, absent anything else, use it; however, I believe there are better processes. Find something you are comfortable with and stick with it and/or call your advisor for ideas. Systems and processes, systems and processes… always a good idea.

What happened this past week may or may not be the tip of the bull market top iceberg but it should cause us to take note and have a plan in place. Will “risk parity” be a word we will look back on? Volatility drives the weighting decisions. Will higher volatility cause massive selling of equity exposure at the same time? Will it trigger further selling from passive equity index investors? It’s a risk I’m not sure is accurately quantified.

Watch inflation, rising rates and high yield spreads (and the recession watch charts I’ll share with you from time-to-time… no sign of recession in the next six to nine months). I mentioned to Mauldin that if recession occurs next year and if it is higher rates that drive us there, then there is no way many of the high yield junk bond dependent companies will survive. They won’t be able to refinance their debt… life support ends. Game over. As I mentioned previously in OMR, the opportunity on the other side of the next default cycle will be epic. Likely the best opportunity since I began trading HY in the early 1990s. Stay tuned.

Grab that coffee and find your favorite chair. Let’s look a little deeper into the Vol Trade Flash Crash, touch on inflation, higher interest rates, the Fed and since I don’t want the letter to get too long, let’s bump our look at what the latest valuation metrics are telling us about coming returns (low) and potential downside risks (high) to next week.

I will try my best to translate this all in a way your clients might better understand.

Included in this week’s On My Radar:

- The Volatility Trade Flash Crash Explained

- Ken Griffin and Paul Tudor Jones on Higher Interest Rates

- Trade Signals — Fixed Income Trends Negative, Don’t Fight the Tape or Fed Signals Caution, Equity Trend Remains Bullish

The Volatility Trade Flash Crash Explained

One of my big risk concerns is the unknown amount of money in the risk parity trade. Essentially, volatility drives the weighting decisions. If equity market vol is low, then equities get a weighting. If equity market vol picks up, then, by rule, the risk parity strategies rebalance their exposures… in this case, reduce equity market exposure. They are mathematically-driven strategies and all essentially use very similar volatility measurements.

The more popular a strategy, the more money on the same side of the same trade and when you shift, you get more sellers than buyers all at the same time. I’m not saying it is a bad strategy… who am I to question Ray Dalio? I’m just saying I’m concerned that there is so much money, much of it levered, on the same side of the same trade. How the managers execute their rebalancing becomes more challenging.

Now with that said, I believe this past week’s rout was tied to the unwinding of the VIX trade. I touched on that in the intro above but do want to share with you several links offering varying opinions below. The inside baseball, via my industry connections, is that managed futures managers are taking a beating. We’ll see those partnership marks at February month-end.

Now put on your geek propeller beanie and read the following from two good friends and smart/experienced managers, Artie Grizzle and Charles Culver from Martello Investments:

Takeaways from Monday’s Move:

- We take some comfort in the fact that our tactical approach got us out of the trade. Monday was a classic panic. Those that tried to “buy the dip” without understanding the impact the move had on the underlying futures and the mechanics of the ETPs have likely experienced unrecoverable catastrophic losses in their positions. Our approach caught levels of increasing risk in the weeks leading up to Monday’s move. We feel this illustrates the benefit of using a data-driven, value-focused methodology to help manage risk, especially in these extremely risky securities.

- The move on Monday drives home the idea that sizing positions appropriately is critical, appropriately reflecting the risk in the trade. Investors that utilized a static allocation to XIV in their portfolios without active trading may now, in retrospect, know fully why position sizing was crucial to limiting the damage from this violent move. Paraphrasing our December commentary:

The role of short-volatility strategies as a portion of a total portfolio must be properly framed. We think about short-vol exposure as equity-replacement; as the VIX is based primarily on the price of S&P put options, short-VIX exposure is inherently equity-sensitive. From 2011-2017, the XIV’s beta to the S&P was over 4.5. This means that you can potentially use a 1% position in XIV to replicate a 4.5% equity position. Using this logic, a small portion of XIV in the equity portion of a portfolio (5% or so) can impact the total portfolio similarly to a 22.5% position in a stock index. Using short-vol as an equity-replacement strategy, then, would allow investors to free up additional capital and invest more defensively, putting less capital at risk and potentially limiting total portfolio risk and drawdown, while keeping the same return potential as a higher equity portfolio.

- XIV has been terminated. We reached out to VelocityShares (the company behind XIV) to gauge the probability that they would relaunch the strategy in the future. So far, we have not heard back from them, as we’d imagine they are dealing with a lot over there. As of the time of this writing, ProShares has signaled its intent to keep SVXY open.

- The move Monday is a reminder of the power of the reflexivity of volatility, the impact of leverage in the system, and the prevalence of vol-based strategies in the market. It is probably not coincidental that this move took place after one of the worst weeks for risk parity strategies in the last several years. From our December commentary:

In addition, we have discussed in other commentaries the reflexive nature of low equity volatility, meaning that falling volatility is a positive feedback loop that begets even lower volatility. Strategies that use volatility as a portfolio weighting mechanism — some examples include risk-parity, trend-based strategies, and VAR-focused approaches — continue to add to positions as volatility falls, further lowering volatility. This reflexive nature of volatility increases shock risk, particularly with the amount of leverage in the system, because rising volatility forces selling to decrease risk, which potentially begets even higher volatility, causing more selling, and so on.

And our May 2017 Commentary:

Low volatility does present inherent risks to portfolio construction, particularly for certain types of strategies that use backward-looking volatility metrics for position sizing and risk management. A well-known version of this is a metric known as Value-at-Risk (VaR); VaR’s role in the 1998 LTCM downfall and 2007-2008 credit crisis has been widely covered. Essentially, these types of models rely on, among other things, trailing historical volatility to infer how much a portfolio can lose in a given period. With such a prolonged period of benign markets, these strategies are susceptible to volatility shocks, as complacent investor behavior causes an undervaluation of the real potential losses of the portfolio. The real risk in the portfolio is only realized ex-post, when the volatility environment changes and a market shock occurs. Particularly for strategies with leverage, this could potentially lead to a cascade effect, whereby increased volatility causes further selling pressure, further raising volatility, and so on.

Volatility shocks indeed. Here are a few links:

- “Volatility: Tempest or Tool?” A. Grizzle and C. Culver, Martello Investments (December 2017).

- “Monday’s Market Volatility and its Impact on Inverse-VIX ETPs,” A. Grizzle, CFA and C. Culver, Martello Investments (Feb. 7, 2018).

- “Risk Parity Derangement Syndrome,” C. Asness, AQR Capital Management (Feb. 7, 2018) (explaining why risk parity and trend following are not to blame). See also, “Risk Parity: The Dog That Did Not Bite,” C. Asness, AQR Capital Management (Sept. 21, 2015).

- Mauldin’s Outside the Box featuring Doug Kass from Seabreeze Partners Management, February 6, 2018, Once Again: “Kill the Quants (and the Levered ETFs and ETNs) Before They Kill Our Markets.”

- One last thought, I’m not opposed to liquid tools that allow us to target our investment exposures, but I’m not a fan of super-high risk professional products packaged that mom and pop can trade. My friends, Artie and Charlie from Martello Investments, expressed to me that these tools should come with a bold warning that says “For Experts Only.”

How does a fund lose 82% overnight? Picking up nickels in front of a steam roller. Harvard Management stretching for yield too, but they properly sized their risk exposure. I have no idea as to who ran the LJM Preservation and Growth fund but I bet they lacked enough real life lashings. I also bet they are on the phone with their attorneys this morning.

Ken Griffin and Paul Tudor Jones on Higher Interest Rates

From Bloomberg:

… Jerome Powell was sworn in Monday as chairman of the Fed, inheriting a U.S. economy in its third-longest expansion on record, with unemployment and inflation near historically low levels. U.S. stocks have tumbled amid concern that quickening inflation will force interest rates higher.

Paul Tudor Jones, in the 10-page letter seen by Bloomberg, hinted at a parallel between Powell and former Bank of Japan Governor Yasushi Mieno, who took to the helm in December 1989 amid a boom driven by speculative investment in land and stocks. Within a week, he began raising interest rates.

Mieno “was ultimately blamed for pricking a bubble over which he had no control,” Jones said. “While the messenger always gets the blame, the real fault lies at the feet of the policymakers of the late 1980s who allowed systemic imbalances to build up in the Japanese stock and real estate markets.”

Ken Griffin, founder of Citadel, said on February 2 that he’s concerned about quickening inflation globally amid “general complacency” around the risks of such a shock. He said his $27 billion hedge fund was “carefully positioning for the possibility that inflation surprises to the upside.”

[Jones and Griffin are extremely savvy and successful traders.]

Jones and Griffin’s views on inflation run counter to those of most economists. Unemployment has dropped to 4.1 percent from 10 percent at the height of the last recession without provoking any significant jump in wages or overall prices. At the Fed, not a single policy maker is predicting inflation higher than 2.1 percent in 2018, or 2.3 percent in 2019.

When President Trump talked about tax reform during last week’s State of the Union address, Jones said, he didn’t mention that Treasury auctions will increase this year from the current projection of $583 billion to almost $1 trillion.

“It is incredible that at full employment we have passed a tax cut that will push our deficit to 5 percent of GDP,” Jones said. “Can you imagine what will happen to the deficit and debt in the inevitable downturn? This is what the dollar is sensing.”

Jones founded Tudor in 1980 and became one of the famed macro managers trading everything from currencies to commodities. In recent years he has posted middling returns and saw clients pull billions of dollars from his hedge fund. Jones was among the macro managers who staged a comeback last month, with his main fund climbing 4.8 percent after losses last year.

Jones described central bank policies that led to low volatility as the “photo negative of my career starting out and an archenemy of my style of trading.” He said 2018 brings “a new fact set and a field of dreams for macro” and cited the Bible: “To everything there is a season and a time to every purpose.”

Keep inflation, higher rates and tightening Fed policy on your radar. 290% global debt-to-GDP… inflation and higher rates are the sparks that ignite a fire. Risk has returned.

Trade Signals — Fixed Income Trends Negative, Don’t Fight the Tape or Fed Signals Caution, Equity Trend Remains Bullish

S&P 500 Index — 2,698 (02-07-2018)

Notable this week:

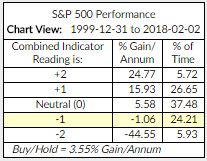

A little more red on the “dashboard” this week. Notable is the move in the Don’t Fight the Tape or the Fed indicator to -1. Put that on the caution list. It is signaling a period of low annualized returns. Historically, returns since 1999, when in the various zones, look like this:

Let’s watch out for -2 readings. Don’t Fight the Tape (trend) or the Fed – returns are worst at -2. Overall, the bullish trend for equities persists as measured by the NDR CMG U.S. Large Cap Long/Flat Index (indicator) and the 13- vs. 34-week MA of the S&P 500 Index (charts below). Volume demand (buyers) is higher than volume supply (sellers) but the trend is weakening and bears watching. The Zweig Bond Model (a trend model for the bond market) moved to a bearish reading this week. HY is also in a sell signal. The trend in Gold remains bullish.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits