The recent uptick in average hourly earnings (+2.9% y/y) and the surge in the government’s borrowing needs ($1 trillion plus in the current fiscal year) have had some implications for the underlying fundamentals. However, the outlook hasn’t been tumultuous enough to explain multi-100-point intraday swings in the Dow. Something else is clearly going on. Past market corrections have had two key elements. One is that many participants felt that the market was overvalued to begin with. The other is that people are selling mostly because other people are selling. Looking through the day-to-day noise, the recent market action is consistent with the two economic themes for 2018: 1) solid momentum across sectors to start the year; and 2) increased uncertainty regarding the intersection of corporate tax cuts, job market constraints, increased government borrowing, and more aggressive monetary tightening.

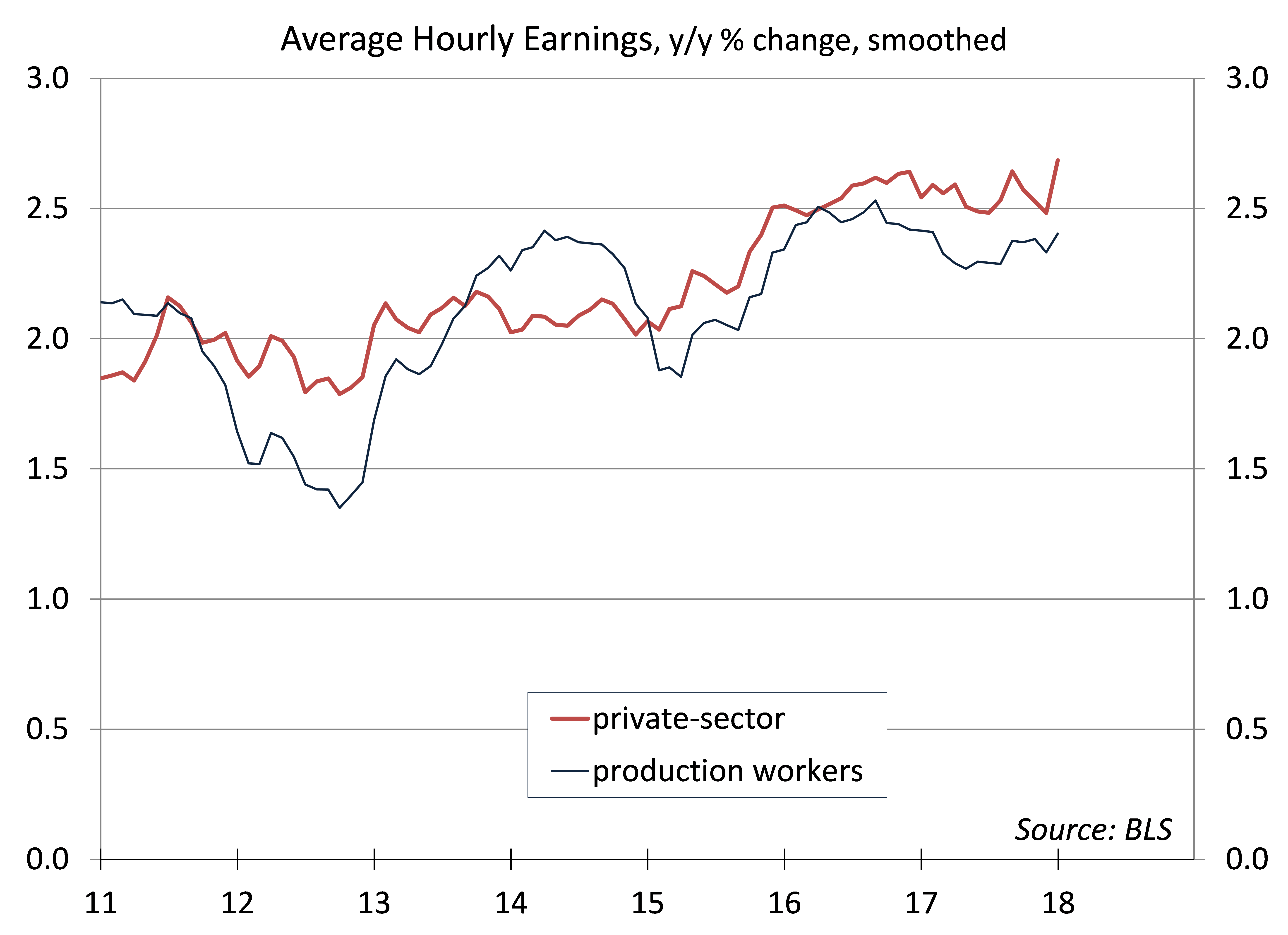

Let’s circle back and look at the average hourly earnings (AHE) data released on February 2 (recall that this report included benchmark revisions to the data, but that didn’t change the picture). AHE for private-sector workers were reported up 2.9% y/y, the highest in over eight years. However, monthly figures can be erratic. If we smooth the wage figures using a three-month average, wage growth was 2.7% – and if we restrict that to production workers, the pace was 2.4% (essentially unchanged over the last two years). Granted, wage pressures should build as the job market tightens, but the anxiety generated by that 2.9% AHE figure appears way overdone.

Click here to enlarge

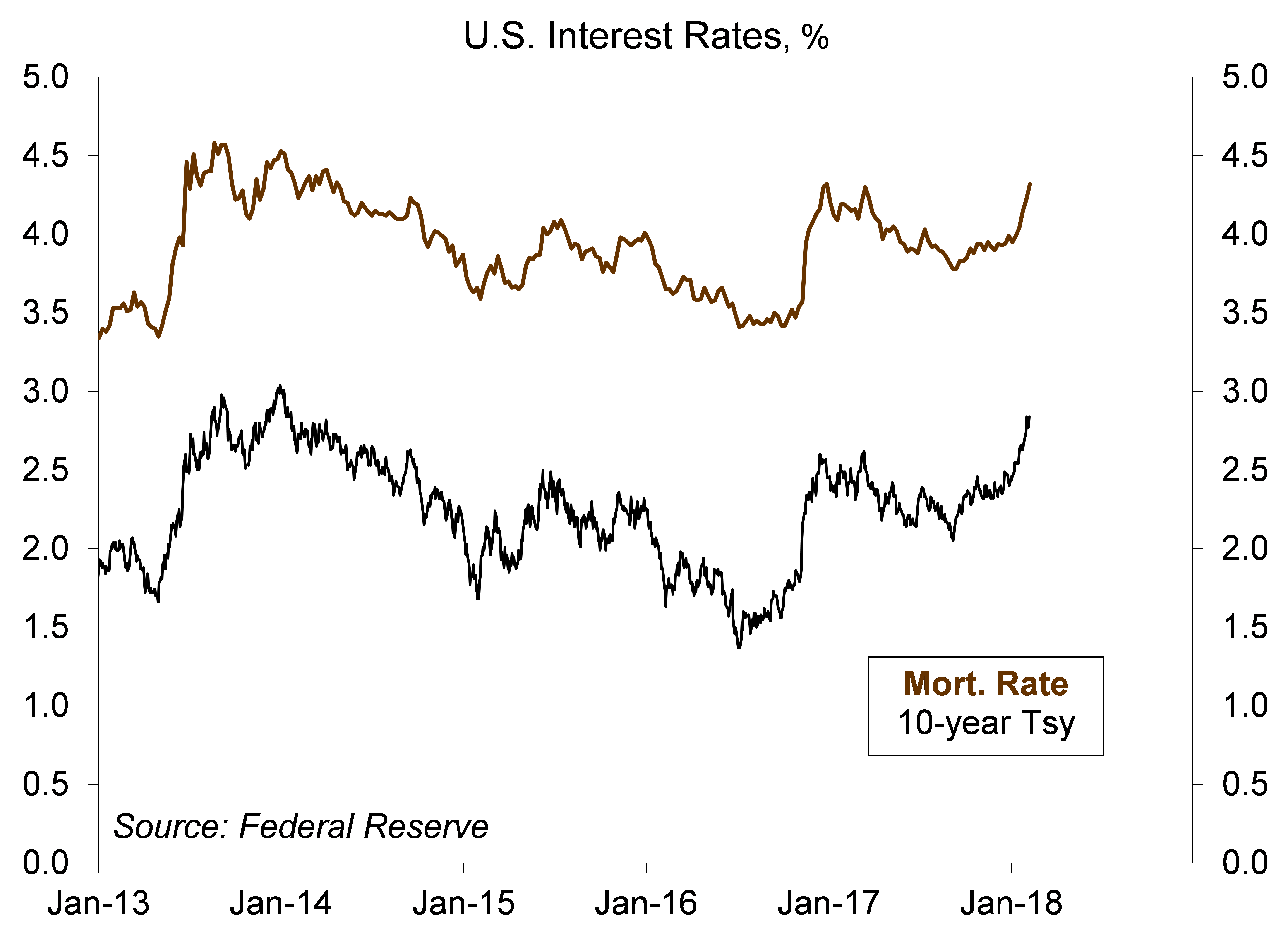

The government borrowing outlook grew worse last week. Recall that Treasury reported a sharp rise in its borrowing need on January 29 and announced increases in the sizes of the regular monthly auctions of notes and bonds on January31. Last week, Congress approved, and the president signed, a two-year budget agreement that boosts spending for FY18 and FY19 about $300 billion over the previous spending cap. That additional spending qualifies as “fiscal stimulus,” on top of the near-term stimulus of the Tax Cut and Jobs Act approved in December. However, the impact is going to be unclear given the limitations of the job market and the fact that monetary policy would likely be even tighter.

Click here to enlarge

Higher interest rates should have a detrimental impact on economic growth, especially in business investment and in housing. Capital spending is unlikely to be affected much, given the cut in corporate tax rates. However, the tax changes will have significant effects on whether to finance investment through debt or equity – and it’s likely to take a year or more before the IRS fine tunes its interpretation of tax law changes. Higher mortgage rates will price a lot of potential homebuyers out of the market, especially at the bottom half of the market, which has struggled to recover from the housing collapse.

The stock market should settle down at some point, but the extreme volatility could be with us for a while. Nauseous investors are unlikely to be comforted by the notion that they are in it for the long haul, that corrections are healthy, and that the fundamentals haven’t really changed all that much. Go outside. Look at the horizon. Maybe try some ginger root.

If only we had a hero. Like Clark Kent, Jay Powell is a quiet, unassuming man. The new Fed chair will present his semi-annual monetary policy testimony to the House Financial Services Committee on February 28. In his nomination hearing, Powell played it close to the vest. This time, he will have to be more explicit in his monetary policy outlook (actually not “his” alone – he’s there to represent all of the Fed’s decision makers). Will he step out of the phone booth and save the day? Depending on what transpires in the financial markets, he may not have the luxury of waiting. The Fed is not expected to ease policy to counter stock market weakness, but a strong, comforting statement may be needed relatively soon.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James