4th Quarter 2017

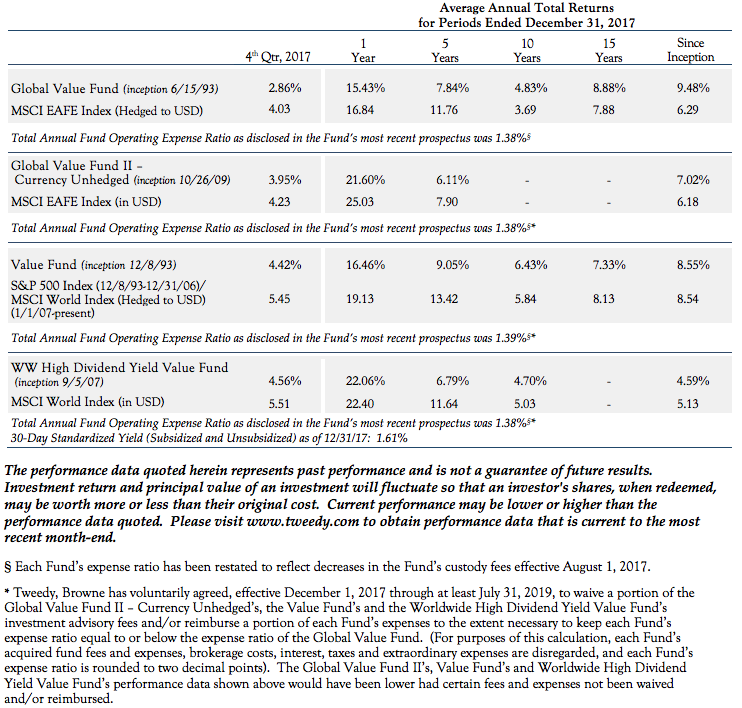

“Animal spirits” were once again at large in global equity markets during the fourth quarter of 2017 as economic growth perked up in many parts of the globe and equity market returns followed in kind. All four Tweedy, Browne Funds made considerable financial progress during the quarter and the full calendar year, but trailed their respective benchmark indices due in large part to a healthy allotment of cash reserves and their continued low weighting in Japanese equities. For the full calendar year, the Funds produced absolute returns between 15.43% and 22.06%.

With the unabated advance in global equities continuing during the fourth quarter and into the first several weeks of the new year, equity valuations are now at levels that are likely to have a dampening effect on future return expectations. While it is possible that the current environment of synchronous economic expansion allows many companies to “grow” over time into their current lofty valuations, many uncertainties remain, not the least of which is the likely sustainability of this recent pick up in economic growth, and the impact that global monetary tightening will have on interest rates in both the short and longer term. Should surprises occur on either of these fronts, or a macroeconomic “black swan” suddenly and unexpectedly appear, equity valuations could come under intense pressure rather quickly.

While bargains on the whole remain difficult to come by in this rather exuberant environment, we continue to uncover a few new ideas, as evidenced of late by AutoZone and WPP, among others. We believe our Funds remain well positioned for future growth, with reasonable cash positions that should serve as ballast and allow us to take advantage of opportunities should the investment waters become turbulent.

The Funds do not impose any front-end or deferred sales charges. However, the Global Value Fund, Global Value Fund II and Worldwide High Dividend Yield Value Fund impose a 2% redemption fee on redemption proceeds for redemptions or exchanges made less than 15 days after purchase. Performance data does not reflect the deduction of the redemption fee, and, if reflected, the redemption fee would reduce any performance data quoted for periods of 14 days or less. The expense ratios shown above reflect the inclusion of acquired fund fees and expenses (i.e., the fees and expenses attributable to investing cash balances in money market funds) and may differ from those shown in the Funds' financial statements.

Please note that the individual companies discussed herein were held in one or more of our Funds during the quarter ended December 31, 2017, but were not necessarily held in all four of our Funds. Please refer to the footnotes on page 13 for each Fund’s respective holdings in each of these companies as of December 31, 2017.

In terms of portfolio attribution, the banking, energy related, media, beverage and industrial components of the Funds led returns for the quarter. With interest rates on the rise in the U.S. and the UK, a pull back in quantitative easing in Europe, and a friendlier regulatory environment in the U.S., the prospects for rising net interest margins helped to drive all of the Funds’ bank stocks higher, particularly DBS Group, United Overseas Bank, Standard Chartered, and Wells Fargo. Not far behind the bank holdings were the Funds’ energy related holdings, which responded quite strongly to the rise in oil prices. This included robust returns in Devon Energy, Royal Dutch, ConocoPhillips, and Halliburton. Our media holdings including Axel Springer and Schibsted continued to thrive in a rapidly changing digital environment, while beverage holdings such Diageo and Heineken had another solid quarter. Key industrial holdings such as Emerson Electric, 3M, LG Corp, and Ebara also advanced during the quarter.

While most of our Funds’ holdings made good progress during the quarter, not all stocks pressed forward. Leading the decliners were insurance holdings such as SCOR and CNP Assurances; pharma holding GlaxoSmithKline; defense holding BAE; industrial holding G4S; and Baidu, the Chinese internet search business. Baidu had a modest pullback after a rather aggressive move up in its stock price earlier in the year.

Portfolio activity for the quarter was overall relatively modest. We took advantage of pricing opportunities to sell the Funds’ remaining holdings in Akzo Nobel and British American Tobacco, and sold the Global Value Fund II’s positions in AGCO and Teleperformance, all of which, for the most part, had performed well and were trading at or above our estimates of intrinsic value. We decided to finally sell the Funds’ position in Akzo after it made a failed bid for a US-based coatings company at prices we felt were too high. This behavior, coupled with their past unwillingness to engage with PPG, caused us to lose confidence and to take our profits while the stock was elevated. We also sold the Funds’ remaining shares in Provident Financial, whose stock price faced a significant comeuppance, in part due to its ill advised attempts to bring technological efficiencies to what was a proven business model. Concerns about possible shortfalls in future funding led us to sell our remaining shares. In addition, we sold out of IBM at a modest profit, due to the company’s continued declining revenue and profitability, our difficulty in getting a handle on its base level of earnings power going forward, its suspect earnings quality, and what would likely be less cash flow available for share repurchases.

With equity market pricing continuing to gain momentum during the quarter, new buys were few and far between; however, we did establish one new position across all of our Funds: UK-based WPP, the world’s largest global advertising holding company. Its various agencies provide traditional advertising services, digital marketing, communications planning and media buying, public relations as well as other marketing services. WPP has several highly renowned global ad agencies in Ogilvy & Mather, Young and Rubicam (Y&R), J. Walter Thomson and Grey. Its clients include P&G, Ford, Colgate, Unilever and various other global multinationals. Over the past year, growth rates have come down at the company reflecting a slowdown in spending by several of the large global branded consumer products companies, some of which are being prodded by activists to cut costs in an effort to increase their profitability. There is also concern that technology giants such as Facebook and Google could possibly disintermediate the advertising business over time. We believe that fears of disruption by the technology companies are overblown, and that the near-term slowdown in growth will prove to be temporary. While growth has been about flat for this past year, the stock price was down over 30%, which presented us with a pricing opportunity. At purchase, the company was trading at a single digit price/earnings multiple1 and paid a dividend yield north of 4%. People have long predicted the “death of the advertising agency,” yet these businesses have, over time, tended to thrive in times of change. There is no evidence that it should be different now. These companies have adjusted extraordinarily well to the new, more digitally-oriented operating environment, and we believe they will continue to thrive in the years to come.

As a reminder, during the quarter we established a breakpoint in the fee schedule for the Tweedy, Browne Global Value Fund, reducing our annual fee on assets greater than $10.3 billion to .75%. This represents a 40% reduction in the Global Value Fund’s fee rate on assets over that amount. As we write, we have crossed the $10.3 billion level in assets, and our shareholders are now receiving some benefit from the breakpoint. Over time as the Fund grows, we expect the Global Value Fund’s shareholders to receive a material benefit from this reduction in the Fund’s fee schedule. We have also agreed voluntarily to waive fees and expenses on our other three Funds going forward in an amount necessary to keep their expense ratios in line with that of the Tweedy, Browne Global Value Fund.

Thank you for investing with us and for your continued confidence.

Tweedy, Browne Company LLC

William H. Browne

Thomas H. Shrager

John D. Spears

Robert Q. Wyckoff, Jr.

Managing Directors

Dated: January 24, 2018

1 Price / earnings multiple is a comparison of the company’s market value less the value of its equity investments divided by our estimate of the company’s 2018 net income.