Winter Quarterly Commentary

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“I can calculate the movement of stars, but not the madness of men”

- Sir Isaac Newton, 1642-1726 Mathematician, Astronomer, Theologian, Author, Physicist, Master of the Royal Mint, Speculator

Sir Isaac Newton’s magnum opus, Mathematical Principals of Natural Philosophy, established the laws of motion and universal gravitation which underpinned how scientists thought about the physical universe for centuries. Newton did not cover the laws of financial gravitation, which appeared not to apply in 2017 as the stock market soared to another 22% return... which was disappointing considering bitcoin returned more than 1,300% and other cryptocurrencies such as Ethereum soared by more than 9,400%. In remembrance of Newton, and inspired by his ~500 page tome, we thought we would write an unusually long letter in order to cover a special topic.

For the past three quarters, we’ve been receiving a number of inquiries regarding everyone’s new favorite subjects, bitcoin and cryptocurrencies. When it comes to investing our clients’ money (and our own, which is always alongside yours), we stick strictly to stocks and bonds and wouldn’t touch these “assets” with a ten-foot digital pole. However, we will now venture a short commentary on investing in cryptocurrency, a short introduction into what bitcoin is, and *gasp* a bullish investment case for bitcoin. Those who wish to skip straight to our usual stock and economic subject matter can jump to page nine.

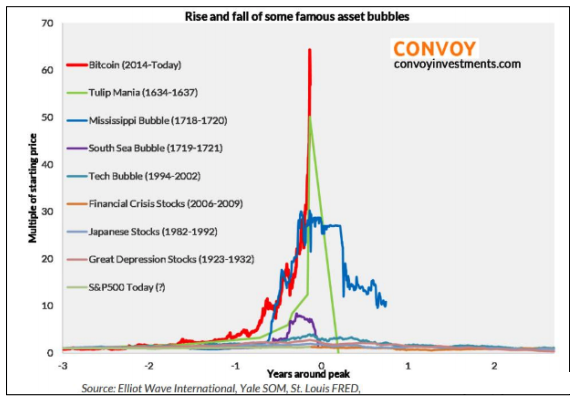

The most common and pressing question we receive around cryptocurrencies is, “Are these in a bubble?” That depends on how you define the term “bubble.” If we take as the definition, “Something that has risen rapidly in price, and will soon fall 80% or more never to recover,” then we can honestly say that we don’t know if bitcoin is in a bubble. (Here we will talk about bitcoin but the commentary goes for all cryptocurrencies). What we can say with confidence, is that even if it isn’t a bubble... is sure smells like one!

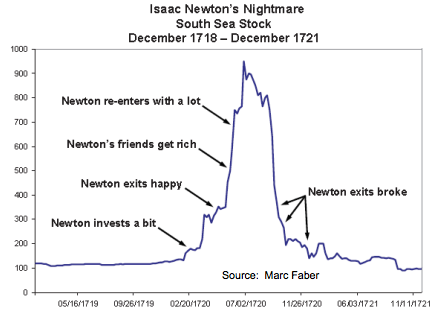

Bubbles are price action phenomena. They are a natural and regular occurrence throughout human history and they can be studied. Even the venerable Sir Isaac Newton succumbed to England’s South Sea Investment bubble. (See chart.) Unless you are smarter than Sir Newton (hint: you aren’t) we very seriously suggest that if you’re interested in cryptocurrencies, you spend a few hours studying bubbles in addition to studying the underlying technology. The whole episode has all the hallmarks of the price phenomenon where something’s price increases dramatically and then goes back down. To support our proposition that bitcoin looks like a bubble, we present three exhibits:

Source: Marc Faber

Exhibit 1: Fantastic price rise. In 2017 alone bitcoin rose approximately thirteen-fold. By itself, this dramatic price rise makes it a candidate for being in a bubble, as price increases of such magnitude are often not sustained. In Sir Isaac Newton’s day, shares in the South Sea Company rose eight-fold in about six months.

Exhibit 2: Everyone is excited about getting rich, especially those not normally interested in investing. This exhibit is self-evident and requires no chart. The meteoric rise has prompted friends who have never bothered to ask us about stocks to ask us about bitcoin. We observe much hand-wringing at having missed out on bitcoin and resolve not to miss the “next one”. In the movie about the housing bubble, The Big Short, there is a scene where the protagonists realize that things have gone too far when they discover that Florida strippers have been buying multiple houses on credit. We were reminded of this scene when we saw an Australian news report of a pole dance instructor who was putting her day job on the backburner to focus instead on cryptocurrency. William Lecky described a similar scene in eighteenth century England, “Landlords sold their ancestral estates; clergymen, philosophers, professors, dissenting ministers, men of fashion, poor widows, as well as the usual speculators on ‘Change, flung all their possessions into the new stock.”

Exhibit 3: Emergence of lower-quality imitation investments. Here we quote from Charles McKay’s 1841 text describing the South Sea Bubble: “Inspired by the South Sea Company, other schemes based on speculative greed were spawned... Some of the schemes were plausible enough. In normal times they could have been to everyone’s advantage. But they were started merely with the view of selling shares in the market. The directors of each bubble company took the first opportunity of a rise in the share price to sell out and next morning the scheme was at an end... An unknown adventurer started the scheme that showed, more completely than any other did, the utter madness of the people. It was entitled ‘company for carrying on an undertaking of great advantage, but nobody to know what it is’.” For those worried they have missed out on bitcoin, coinmarketcap.com asserts there are 1,497 other cryptocurrencies with which one can hope to strike it rich. Unfortunately, even crypto-enthusiasts admit many (not all) of these are likely scams created for the same reason as the South Sea follow-on investments: to satisfy the massive demand to get rich quick. These scams and other dubious projects come in the form of ICO’s, or “Initial Coin Offerings”. Present day ICO promoters like Floyd Mayweather and Paris Hilton have an advantage over their 18th century counterparts though: while selling stock in fraudulent corporations can land you in trouble with the SEC, selling “coins” in an ICO obligates the seller to do... absolutely nothing. Coin holders have no rights and no recourse to the legal system. A good demonstration of this is “MarijuanaCoin” (thereby embodying the union of two over-hyped investment fads) which launched in February 2017, raising some $60,000, after which the lead developer/promoter promptly disappeared, leaving not even a website behind, and was found a week later promoting the ICO of “Marijuaneum”. Amazingly, the actual “MarijuanaCoins” still exist and, in a sign of new “investors” continuing to pour in, are now worth $450,000 in aggregate. If that “investment” doesn’t suit your fancy, don’t worry, there is also PotCoin, CannabisCoin, DopeCoin, HempCoin, and Cannacoin, most worth in the tens of millions of dollars. The excitement, demand, and irrational exuberance isn’t limited just to new issues; there are numerous examples of existing companies putting the word “blockchain” in their name, and then seeing their stock price double or more1. These altcoin anecdotes don’t tell you anything about bitcoin, but they do speak volumes about investor attitudes.

Given the above exhibits, let us introduce a new definition of “bubble”: “when people are mostly buying something 1) because it has gone up in the past and 2) because they expect it to immediately go up in the future”. Under that definition, bitcoin is definitely in a bubble. No one is buying bitcoin or other cryptocurrencies for their intended use, they are buying them to speculate on a price rise. Note that we so far haven’t spent one moment writing about what bitcoin is; it’s kind of irrelevant! The bubble has nothing to do with bitcoin itself, the bubble has to do with the human attitudes and enthusiasm and expectations that surround bitcoin.

Here the dotcom bubble serves as an excellent example. The internet wasn’t a fad; the promise of the internet was real and it went on to become hugely important in all of our lives... but that did not prevent internet stocks from being in a bubble and falling 90% or more. Bubbles can form around largely useless assets like Beanie Babies or tulips, but they can also form around very good assets...and the second type is hardly less dangerous. Do not let arguments about the wonders and adoption of digital currencies sway you into thinking a crypto investment will succeed; technological adoption and investment success are not the same thing. Take Amazon for example. From 1998 to 2001, stock in the now-ubiquitous online retailer went from $5, to $105, and then back to $8! A disaster! As we all know, those who bought at $105 would have eventually done well because Amazon was a good asset and the stock is now worth ~$1,350. But, for the vast majority, there is approximately zero chance those who bought at $105 actually did hold on, because they were buying 1) because it had gone up in the past and 2) with the expectation that it would immediately go up in the future. $105 to $8. For Amazon.

With that out of the way, we owe readers a very quick and dirty explanation of what bitcoin actually is. Initially dismissive, after we heard a few smart people say this was the biggest thing since the internet, we decided to take a look. Surprise, surprise, we actually think there might be a good asset at the heart of this bubble (which, by the way, is perhaps in the process of popping as the price of many crypto-currencies including bitcoin have declined close to 50%).

Blockchain (more formally, distributed ledger technology), is the technology that underlies bitcoin. It allows programmers to create what we call “magic ledgers”2. They’re “magic” because the ledger is stored on many different computers at the same time, is therefore available to the public to read, and is completely trustworthy even if you can’t trust any of the people who have the computers on which the ledger is stored. Magic! Ok, it’s not really sorcery, but rather an extremely clever combination of cryptography and incentives that results in the ledgers working as advertised above and below3.

So what is bitcoin? Bitcoin is just one of these magic ledgers that pretty much does just one thing: records who owns the bitcoins4. If the ledger says you own a bitcoin, and you change the ledger to say another person owns it, well, you’ve just paid that person a bitcoin.

So what does it mean to “own” a bitcoin? Really this just means you control a special password called a “private key” that lets you move bitcoins out of your ledger account and into someone else’s. The ownership of this password is almost physical, almost like owning real coins. The bitcoins won’t move without the passwords, so if you lose them, the bitcoins are effectively lost forever, just as if you dumped gold coins into the ocean. There are numerous stories of people maintaining their bitcoins (i.e. special passwords/private keys) on old computers that they threw out when each bitcoin was worth just two cents. Now that each bitcoin is worth more than $10,000, these lost passwords are worth millions. One person has attempted to buy the garbage dump that contains his old PC in hopes of recovering a seven digit bounty. This demonstrates well the “magic” behind the technology. The bitcoins won’t move without the passwords, full stop. There is no coaxing the source code, there is no appealing to an authority figure. The computers running the bitcoin program cannot be studied to yield the answer. Really. No one is in charge.

What are these miners we’ve been hearing about? A miner is basically someone who dedicates their computer to running the day-to-day business of the bitcoin network, processing transactions and keeping the ledger up to date. As a reward for these “mining” efforts, they get to enter a lottery where bitcoins are awarded based on a set schedule. The schedule is set such that only a finite number of bitcoins will ever be created.

That’s it! That’s it? What’s this potentially “good” asset at the heart of bitcoin useful for? We suggest it is potentially useful as digital gold (i.e. a trustless store of wealth). The best way to explain this is to take some of the many criticisms levied against bitcoin and apply them to gold.

Criticism: bitcoin has no intrinsic value. This is true, bitcoin has no use other than to sell to someone else; no value other than what someone else will pay for it (well, maybe you could brag about your coin at a cocktail party). Contrast this with a stock, which can be held for its dividend, or to exert control over a company. While true you can use gold to make jewelry and a few other things, the vast majority of gold’s value comes from the fact that other people believe it has value. In fact, that’s probably why we make jewelry out of it in the first place: to display wealth. Gold continues to shine despite the criticism of having no (ok, little) intrinsic value.

Criticism: you can’t really use bitcoin for payment or transactions. This is true, though bitcoin was initially intended to be used as payments in everyday transactions, the processing times have become too long as the network gets jammed with transactions. However, the same is true for gold. You can’t buy a cup of coffee with gold, and yet it still has value.

Criticism: bitcoin is untraceable and used for criminal transactions. Both gold and cash can be used for criminal transactions and are actually untraceable. Bitcoin, on the other hand, isn’t exactly untraceable or completely anonymous (there is a record of every transaction ever!) but the point is any tool is subject to abuse.

Criticism: bitcoin can be hacked and stolen. Bitcoin itself has never been hacked... however, the websites that hold the passwords have been hacked on occasion, just like banks have occasionally been broken into and the dollar bills absconded with. For those who wish to “store” bitcoins securely, it is as easy as writing down the passwords and putting them in a secure place like a safe deposit box... just like you would with gold, which is of course also vulnerable to theft.

Criticism: bitcoin isn’t environmentally friendly. This is true, the amount of electricity the bitcoin mining network uses rivals that used by the country of Argentina. It’s not very efficient. However, digging giant holes in the ground in Africa and Australia and Nevada to get at gold and then leaving tons of slag (mining waste) behind isn’t exactly environmentally friendly either... and yet gold is still used.

Criticism: bitcoin can be outlawed by the government. This is true! But then again, the U.S. government also outlawed private ownership of gold during the Great Depression. However, this did not stop people from owning or placing great value on gold, and eventually it was the government that relented. The U.S. can and may eventually outlaw private ownership of bitcoin as well... but that will not cause the bitcoins to disappear5.

Criticism: bitcoin is too volatile to be a store of wealth. Well that’s true for the time being, but volatility will probably diminish over time. Besides, it’s not like the price of gold is always very stable.

If you accept that the “value” of bitcoin is in being used like gold (as a store of wealth), then criticisms which appear also to apply to gold, shouldn’t hold much weight. The ideal candidate for the holder of bitcoin is the prosperous Chinese industrialist or Arab prince who has the very real fear his wealth might be confiscated by the government. A foreign government or bank CEO might succumb to political pressure to give up assets stashed with them... the bitcoin code will not. All that is required is that you keep the passwords safe, which isn’t too hard. But forget the ideal candidate; the rank and file candidate for the holder of bitcoin is the rank and file holder of gold. Just like bitcoin, gold too has all sorts of detractors who argue that it is irrational to hold gold as a financial asset. However, these arguments seem to fall on deaf ears as people throughout the world continue to value gold quite highly. For now, the same appears to be true of bitcoin.

Surely, there are more than a few differences between gold and bitcoin. We will grossly oversimplify by saying the most important advantage of gold is that it is time-tested, and the most important advantage of bitcoin is that it is easier to store and transact with. You may not be completely sold, but if you’re ready to accept the premise that bitcoin can become something like gold, you’re ready to hear the investment case. Estimates vary, but at current prices all the gold in the world is thought to be worth between six and eight trillion dollars. At current prices of around $11,000, all bitcoins in total are worth “only” around $180 billion. If you believe that bitcoin’s value as an asset class can approach gold and reach, say, a “mere” one trillion dollars (versus six to eight for gold), that implies $60,000 per coin. If you further imagine this takes ten years to happen, and then you discount that future value back to the present at, say, a relatively risky 15%, you get a value of $14,8316,7. ($60,000/1.1510 = $14,831.) Not that far from today’s price!

Now, the numbers used in this example aren’t necessarily ones we actually believe in, but we don’t think they’re completely crazy either. The analysis can be a sort of framework to come up with different estimates of bitcoin’s value. For example, if, say, a 30-year rather than a ten-year horizon to get to the Promised Land was used, it would result in a much lower estimate of $906 per coin. ($60,000/1.1530 = $906.) Alternatively if you keep the ten-year horizon but forecast bitcoin can rival gold’s total market value of eight trillion, the implied value per coin is $476,000 ten years from now, and $117,000 today. Someone who bought bitcoin on this or a similar analysis, would not be buying simply because it had gone up in the past, and was immediately expected to go up future.

OK phew! Now hopefully our readers have some idea of what everyone is so excited about, as well as the inherent risks of investing in something that everyone is so excited about. We do not recommend readers invest in cryptocurrencies as a way to increase their wealth, though we will note there are some who we respect who do recommend people put up to one percent of their wealth in the space. We mostly mention this to point out that even for cryptocurrency believers, the responsible recommended allocation is quite small. We now return you to your regularly scheduled investment programming.

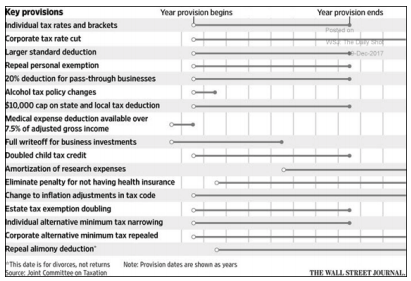

Much more important for our day-to-day investment considerations is the passage of the absolutely giant tax bill. The importance is difficult to overstate. The bill is wide ranging and has a huge number of implications, some beyond just taxes, but the most substantial and consequential change is the reduction in the corporate tax rate. Not only is the magnitude of the corporate tax cut large, but unlike most of the other provisions, the reduction in the corporate rate isn’t set to expire in five to seven years. The corporate cut is a big cut and likely to be permanent not just because the bill was written that way, but also because that portion was backed by some bipartisan support.

On a political side note, the expiration of most provisions as shown in the accompanying chart explains how Republicans can say the average person’s taxes will be lower, and Democrats can say the average person’s taxes will be higher, and they can BOTH be correct. The difference is timing. In 2018, when all the provisions are in force, the average person’s taxes will be lower. Seven years from now, when many of the provisions have expired, the average person’s taxes will be higher. Ahh, politics. The devil, as always, is in the details.

The corporate tax cut is one of the key reasons the stock market has been so strong recently. If you had a company which was earning 100 dollars pre-tax, the government was taking 35 of those dollars, it would leave only 65 dollars for shareholders. Now, the government is only taking 21 dollars, leaving 79 for shareholders. That’s a 21% increase for shareholders!

Of course, most corporations weren’t actually paying 35% because of all the deductions and loopholes. The Wharton School at the University of Pennsylvania has released a report indicating the average effective tax rate (what companies actually pay, as opposed to the statutory rate) will fall from a previous 21% to only 9% in 2018 under the new tax bill. Thus, it’s important to note that companies can still benefit from the new, lower 21% rate even if they were paying less than 21% to begin with. With some of their tax deductions expiring after 2022, the corporate effective tax rate is projected to then rise to 17% (still a reduction from the previous effective rate).

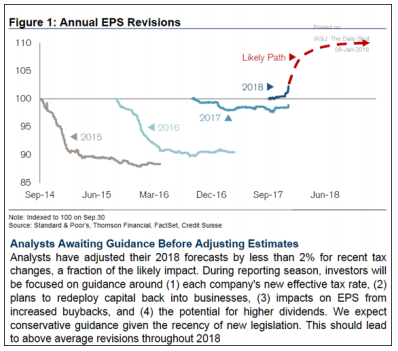

We believe that the stock market tends to underreact to large changes and we think this is happening with corporate taxation. As companies release expectations for 2018 earnings at now lower tax rates, and analysts update their models, we expect to see Wall Street increasing earnings per share (EPS) estimates. Normally, Wall Street puts out very optimistic future estimates, and then has to reign them in as reality approaches. For once, as the adjacent chart suggests, Wall Street’s original estimates are being raised.

Who benefits most from the corporate tax cut? The long-term effects are subject to many complex and interacting factors and only time will tell, but we tend to think the largest beneficiaries will be those who benefit most directly. Those benefitting from second and third order effects will benefit to a smaller degree. The corporations and those who own them are the most direct beneficiaries (that means you, our client, but more on this later).

Unfortunately for some stock holders, the benefits from the tax cut will not be evenly felt across industries. We believe the benefit to corporations (and shareholders) will be fleeting in industries to the extent they compete aggressively with their peers on price. In the highly competitive retailing industry for example, on day one retailers will see higher profit margins from lower taxes, and on day two they will see Walmart lowering prices and the sorry retailer will have to follow suit, destroying those briefly higher margins and passing most of the gain from lower taxes on to the consumer. Contrast this with a provider of a unique, installed software program, that doesn’t have many competitors, and where customers find it a hassle to switch products to save a few bucks – in short, a sub-industry which does not compete heavily on price. On day one, these software providers will have higher margins, and on day two, their competitors will likely they have little to gain from slashing prices, so they won’t, and everyone will enjoy those higher margins. Also consider a utility, whose allowable profit margin is regulated. On day one these utilities will enjoy higher margins, and on day two their regulators will demand that they lower electricity rates charged to customers and those margins will come right back down. Recognizing these distinctions, and looking to take advantage of the under-appreciated changes in the tax code, we are looking to invest in companies which are 1) in the U.S. and 2) don’t compete heavily on price or otherwise have their margins regulated.

What does the corporate tax cut mean for you? You can expect a big increase in share buybacks and dividends, as companies repatriate some of the trillions of dollars held offshore at a discounted tax rate. That’s what occurred following the 2004 repatriation tax holiday, which is estimated to have produced $0.60 to $0.92 cents of share repurchases and dividend payments for every one dollar repatriated. For example, one of our portfolio holdings is paying a one dollar special dividend on January 31st, bringing their 2018 expected total dividend yield to eight percent. Increased repurchasing of shares should serve as an upward force on the stock market, as investors turn around and put received cash right back into the stock market. More specifically, you, our client, might be getting a bigger tax cut than you realize. A $500,000 account holder, as an example, owns shares of companies with annual pre-tax earnings of $27,000. Under the previous tax bill, our companies paid $7,200 of tax, whereas under the new tax bill we expect they will pay $3,900 in tax. Hence, the $500,000 Knightsbridge account holder is receiving a $3,300 tax cut from the lower corporate rate. Corporations may not send this money to you, but will at least invest it on your behalf. So dear clients, probably the biggest reduction in your taxes won’t be showing up in your annual income tax returns, but rather in your brokerage account statements.

The tax bill may or may not be smart policy long-term but the short-term effect is unequivocal: an already strengthening economy will be stronger (and though the stock market isn’t the same thing, we think it will be strong too in the short-term). Tax cuts are stimulative; the end.

As you will recall from our last letter, our previous position that “rates are never going up ever” is dead. We now are preparing for and expect moderately rising rates across both the long and the short-term for a number of reasons:

• The U.S. economy is getting stronger.

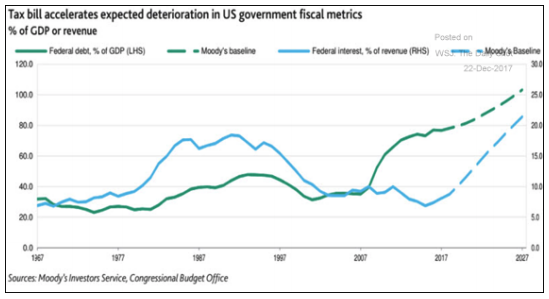

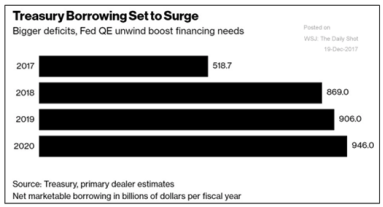

• Deficits are getting bigger, both because of the tax bill lowering revenue but also because entitlement spending is set to rapidly increase. Higher deficits mean more bonds are issued and this increasing supply of bonds is a force for driving prices down and yields up.

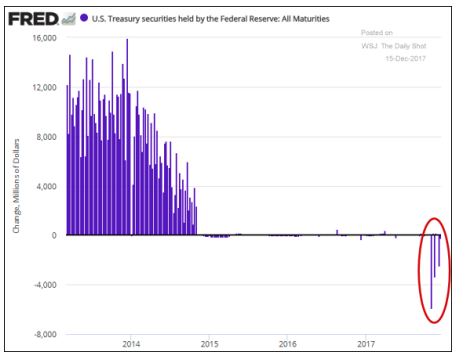

• There is another source of increasing bond supply: the Fed is reversing its policy of QE by selling its enormous horde of bonds back in to the regular market. We once said the Fed was not exactly “printing money”, but rather was “loaning it into existence”. Now, that money is being“repaid into oblivion”. By selling bonds, the Fed is putting bonds into the system, and taking dollars out. The greater supply of bonds in the system is again a force for lower bond prices and higher rates.

- Taking these two aforementioned points together (the combination of bigger deficits and the unwinding of QE) is projected to increase the net supply of new bonds issued by 67% in 2018.

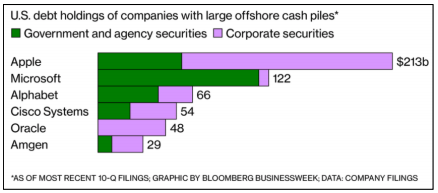

- As a result of the tax bill, large corporations, which had previously been stashing their profits “overseas” will now begin “bringing them home”. Why would this raise interest rates? Well these enormous cash piles were only “overseas” for U.S. tax purposes... in fact as the chart shows the cash was very often invested in U.S. dollar corporate and government bonds. Now that corporations can safely return their profits to the U.S., they will be selling these bonds, which lowers demand, lowers bond prices, and increases rates.

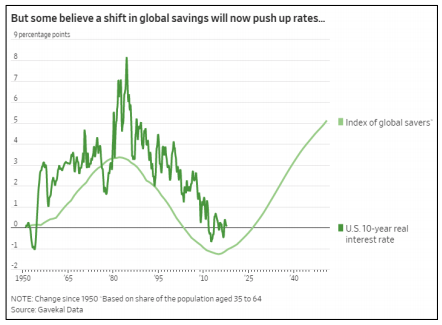

- We have long talked about the “mysterious force” that has been keeping interest rates down for so long. We haven’t seen the detailed analysis but recently we were introduced to the idea that there had been huge saving demand (leading to high bonds prices, and low rates) due to the the relatively large proportion of “saving age” persons in the economically important developed world. This is one of the best candidates we’ve seen for the rate-lowering “mysterious force” that has been keeping interest rates down... and it is starting to be removed as the bulge in the saving-age population (35-64) becomes a bulge in the no-longer-saving age population (65+).

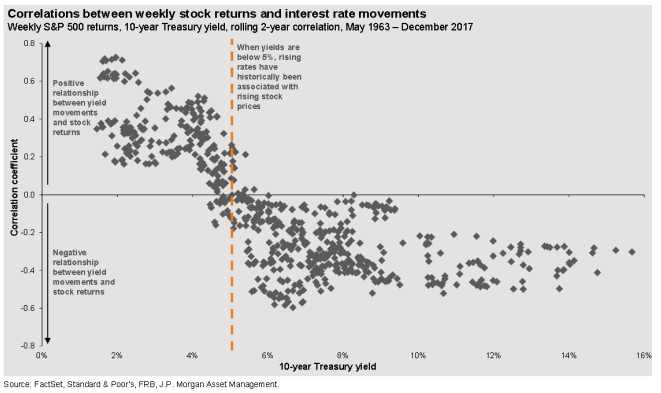

For some time, we have pointed to the low prevailing interest rates as the justification for what has been an unusually expensive stock market. So, if we are right that we are in an interest rate uptrend, is it then time to avoid stocks? We do not think so, at least not quite yet. Basically, the historical record shows that rising rates are ok for the stock market... at first. The below chart shows the correlation (related movement) between the S&P 500 (stocks) and the ten-year Treasury yield (interest rates). The correlation is positive when the ten-year Treasury yield is below about 4.5%, meaning a rising rate environment is actually a positive for stocks below this 4.5% rate threshold. With the ten-year Treasury presently yielding 2.7%, there should be room for rates to rise without ending the party. What would end the party? An inflation surprise. We haven’t seen evidence of that, but we are watching out for it.

We appreciate the patience of those who made it all the way through this unusually long letter and as always, we thank you for the trust you place in us.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 The quintessential example is the small Long Island Iced Tea company changing its name to Long Blockchain. Their stock rose 350% in the next two days.

2 Actually, the technology can be used to build applications that aren’t necessarily just ledgers, but to keep it simple we will stick with just ledgers for now.

3 Again, a big part of what makes this technology interesting is that you don’t have to trust the people with the computers running the ledger, you just have to trust the source code. To really trust this technology, you have to study it, and we invite you to do so.

4 Again, we’re simplifying and glossing over more than a few details, but we’re trying to keep it accessible.

5 It would be difficult for any entity, even the U.S. government, to completely extinguish the bitcoin network, as all it takes are a few anonymous computers running the software. However, without getting into it, we believe shutting down the network would not be impossible.

6 The choice of discount rate used (which reflects the time value of money) will heavily influence the final value of this analysis. One way to look at it would be to say the higher the discount rate, the less sure you are that bitcoin will end up a success. If you were absolutely sure the “good” scenario of $60,000 per bitcoin is going to result in ten years, you might discount your future estimate of value at the low current risk-free rate of about 2.7%. This would result in a present value of about $46,000. We used a discount rate of 15%, reflecting our view that there is a good chance this scenario does not result, and our result was about $15,000, or about one-third of $46,000. Thus, using the 15% discount rate implies something along the lines of believing there is only a one-third chance bitcoin ends up at $60,000 per coin, and a two-thirds chance it ends up worthless.

7 For the record we do believe there are substantial barriers to bitcoin receiving this kind of wide adoption. The largest of which are the possibility of another crypto-asset replacing it, and interference from governments who don’t want to lose control over payment systems.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All