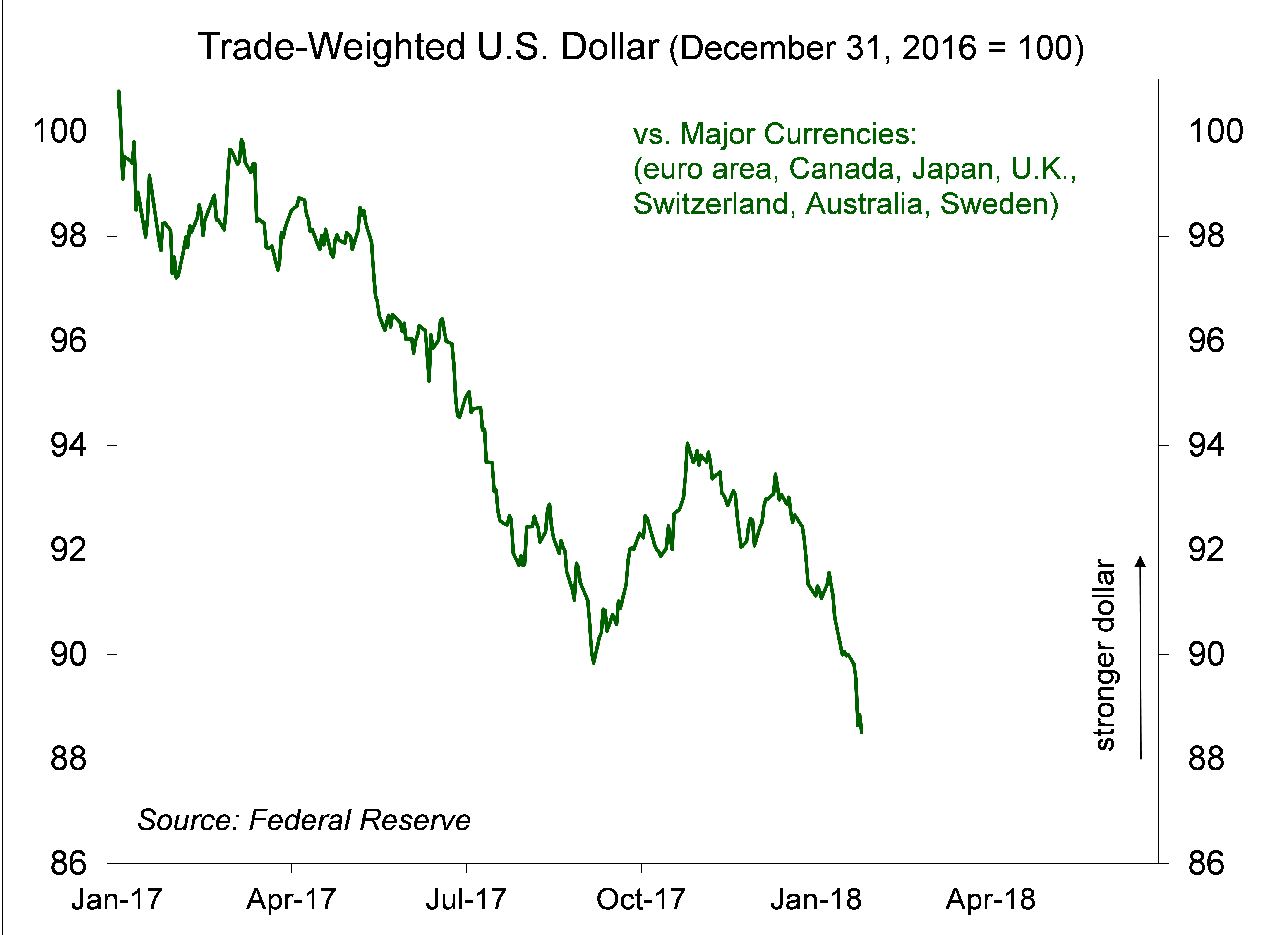

A strong economy, a booming stock market, and tighter monetary policy are all dollar positive. So why is the dollar down more than 12% since the start of 2017?

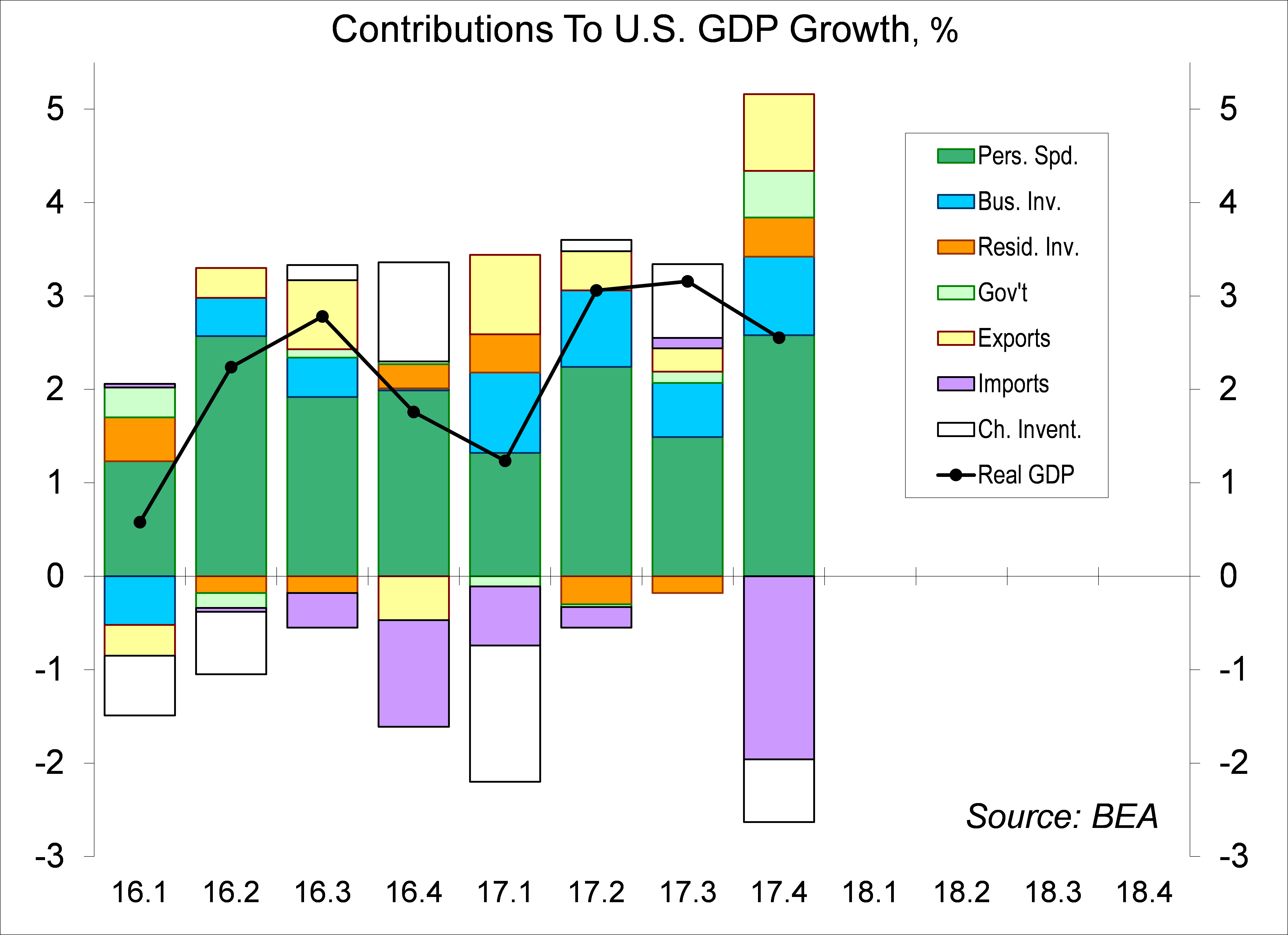

Real GDP rose less than anticipated in the initial estimate for 4Q17, but it was a very strong report. As expected, consumer spending, business fixed investment, and residential homebuilding each picked up following the third quarter’s hurricane-related weakness, and each appeared to be relatively strong when the third and fourth quarters were averaged together. Inventories rose more slowly, subtracting from the headline growth figure. Exports rose sharply, but imports (which have a negative sign in the GDP calculation) were even stronger.

Click here to enlarge

The GDP figures will be revised and revised, but the underlying story (a rebound from hurricanes, on top of underlying strength) shouldn’t change much. Momentum is expected to remain strong in early 2018, supported by enthusiasm for the tax bill changes. However, strong growth can only be accomplished through a further drop in the unemployment rate, which will be difficult since we are at or near full employment. Tighter job conditions will likely motivate Fed officials to raise short-term interest rates a little sooner and faster than they would otherwise, potentially choking off economic growth later this year or in 2019.

There was one major area of concern in the GDP report. While (inflation-adjusted) consumer spending growth rose at a 3.0% annual rate in the second half of the year, disposable income rose at a 0.8% rate. The savings rate fell to 2.6% in 4Q17, vs. 3.7% in 3Q17. It looks as if spending has been fueled by borrowing, which could be a problem down the line. However, the savings rate is a terrible statistic. The government doesn’t measure savings directly. Rather, savings are calculated as a residual (income less taxes and spending). Capital gains are not counted as income in the national accounts, but they do get spent. Income figures are often revised. Remember all the hand-wringing over a negative savings rate about 12 year ago? Never happened. At the same time, we’re sure that many Americans do not save enough. Debt never matters until it does. That is, high consumer debt levels are not a catalyst for economic weakness, but they would make a recession worse.

A booming stock market, a strong economy, and tighter monetary policy would normally send the dollar higher, but the greenback has fallen over the last year. Treasury Secretary Mnuchin recently noted that, all else equal, a weak dollar helps U.S. exporters. Not an outrageous observation, but officials need to be very careful in their public comments. President Trump, in noting that he favors a strong dollar, got the administration back on track a day later, but that seemed to provide only a temporary pause in the dollar’s decline.

Click here to enlarge

During the economic recovery, the Fed was more active (relative to other central banks) in its attempts to support growth. Government austerity dampened the pace of recovery, but the U.S. tightened fiscal policy a lot less than other major economies. The emerging economies had a great story, but many stumbled during the global recovery, leaving the U.S. as a more attractive location for investment. As the IMF noted in its upgraded World Economic Outlook, global growth surprised to the upside in 2017 and the prospects for 2018 and 2019 are brighter. Hence, the dollar’s decline may simply reflect global investors’ increased enamoration with the rest of the world.

Note that the exchange rate of the dollar is the Treasury’s responsibility, not the Fed’s. Policymakers need to be aware of the inflationary impact of a softer dollar, but the Fed will not raise rates to defend the dollar. Oddly, the strengthening global outlook arrives at a time when the U.S. is disengaging from global trade – and that’s not helping the dollar either.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James