“For the first time in a very long time, there’s reason to be optimistic about fundamentals gaining enough traction to validate asset prices.”

“The world I’m describing is a world in which even the long-term investor has to have a tactical layer on top of the structural and secular layer.”

“We are coming out of one paradigm and going into another paradigm.”

“There’s more probability of success than failure, but it’s not overwhelming.”

> Mohamed El-Erian

Conferences can be great fun and the final evening usually ends with a gathering at the hotel bar. This year’s Inside ETFs Conference ended with a bang for me. Sitting outside on a couch, 72 degrees, clear sky and comfortably positioned between the hotel bar, pool and ocean, daughter, Brianna, snuck up on me and grabbed the wine from my hand. Politely she whispered, “Dad, your teeth are looking red. No more wine.” I’m claiming it was the lighting.

I call the hotel bar area “the great vortex.” It can pull you in and this past Tuesday night, the vortex won… Brie reminded me of my advice to her, “No more than two drinks. Stay on your game.” Let’s just say I was north of two.

At midnight, I glanced at my watch. Yikes. An introduction, an opportunity, important discussion, another cabernet and blink… it’s 2:00 AM. What seemed like minutes turned into hours. I escaped the vortex but the vortex won. With opportunity forged, I’m glad it did.

The Insides ETFs Conference in Hollywood, Florida was packed with more than 2,000 of the industry’s leaders. At dinner with Jan vanEck and the VanEck team, we debated the direction of interest rates. Consensus is that interest rates are headed higher. That’s bad news for bonds. I told the group that I’m fundamentally in that camp, but I can make a convincing argument that interest rates are moving higher, I can also make an equally convincing argument that rates are moving lower. “Really,” Jan said, “OK, hit me with it!”

In this week’s On My Radar, let’s first take a look at my high-level summary notes from Mohamed El-Erian’s presentation and DoubleLine’s (Jeffrey Gundlach’s firm) Deputy CIO Jeffrey Sherman’s rates-are-headed-higher presentation and weave their views into my “hit me with it” conclusion.

I like to hear everything El-Erian has to say and I have to say Sherman’s presentation was outstanding. I hope you find the information helpful… I try my best to keep it high and tight. So grab that coffee, find your favorite chair and jump in.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- “Are We in a Bubble?” by Mohamed El-Erian, Chief Economic Adviser, Allianz

- “Quantitative Tightening and Its Implications” by Jeffrey Sherman, CFA, Deputy CIO, DoubleLine Capital

- “OK, hit me with it!” — Steve’s Answer

- Trade Signals — Markets Reach New Highs with Extreme Investor Optimism

- Personal Note — Avoid The Vortex (A Few Photos from the Conference)

“Are We in a Bubble?”

Following, in bullet point format, are selected notes from Mohamed’s Inside ETFs presentation:

- El-Erian kicked off this talk with a rundown of just how extraordinary 2017 was for financial markets. Noting that last year featured six of the seven lowest readings for the VIX on record; the smallest peak-to-trough drawdown for the S&P 500 in any year; and strong returns for both stocks and bonds.

- Stocks, in particular, did much better than the fundamentals did.

- The result? A larger wedge between fundamentals and valuations. Meaning valuations went up while fundamentals (corporate earnings) did not.

- El-Erian said, “The wedge can last years at a time, but ultimately, the convergence will happen,” and added. “The question is, will it happen from above or below?” Meaning, do equity prices drop back down to fundamentals or do fundamentals grow up to justify current ultra-high valuations.

- If the convergence happens from above, it would entail a massive price correction that could overshoot to the downside (the bursting of the bubble). If it happens from below, it means that fundamentals would eventually catch up with valuations.

- Either way, expect low forward 7-, 10- and 12-year returns (SB comment).

El-Erian’s optimistic case:

- El-Erian said the global economy finally has a chance to break out after years of sub-par growth. He pointed out that economic growth is synchronized (every engine of growth is kicking into high gear at the same time) and real (it’s not about leverage or debt, but consumption, investment and trade).

- According to El-Erian, the reason for this improving backdrop is there is more focus on pro-growth policies, especially in the U.S., where there’s been deregulation, tax reform and the potential for increased infrastructure spending.

- Meanwhile, in Europe, there’s been “a natural healing process that is getting to critical mass,” he said, while adding that “the emerging world is also kicking into higher gear.”

- “It’s not the old type of growth that we had 15 years ago that was finance driven. It’s not about leverage or central banks; this is much more genuine.”

- In addition to the positive things that have transpired, El-Erian pointed to some things that didn’t happen that are also proving to be a boon for global economies.

- For example, there was no central bank policy mistake; there were no major disruptions to international trade; there was no surge in inflation; there was no surge in yields; there was no dollar appreciation; and there was no geopolitical shock to speak of. (Emphasis mine)

El-Erian’s pessimistic case:

- Either the paradigm of sub-par growth will end and “we’ll turn into a much better place that validates asset prices,” or, “we’ll take the wrong turn and end up in a much worse place where you’re worried about recessions,” El-Erian said.

-

What will determine which scenario comes to pass is policies. (Emphasis mine.)

- If pro-growth policies continue — including infrastructure spending, education and labor market reform, and more balanced fiscal and monetary policies — good things will happen: faster economic growth, a validation of asset prices and less complicated politics.

- If those policies don’t continue, “then low growth will become recession; artificial stability will become disorderly financial markets; and politics will get a lot more complicated,” he warned.

Three Big Risks

Regardless of which new paradigm becomes reality, El-Erian predicted that investors can expect more volatility in markets in 2018 than was seen during the unusually tranquil period of 2017.

- One risk investors should watch out for is geopolitics. “Geopolitics matter,” said El-Erian. “Markets cannot price in geopolitical shocks easily. If you get a shock, you could get a shift in markets that could be quite violent.”

- Keep an eye on North Korea and the Middle East, where Iran and Saudi Arabia are waging a proxy war.

- Another risk are Central Banks: How successful will they be at normalizing their unconventional monetary policies.

- El-Erian is confident the Fed can continue to normalize policy successfully.

- However, it remains to be seen whether the Fed, the European Central Bank, the Bank of Japan and the People’s Bank of China can all do it at the same time. That will prove exceedingly challenging.

- The third risk that El-Erian pointed out is the potential for a market accident, particularly from index funds and ETFs with exposures to illiquid underlying assets.

- A small proportion of these funds “have inadvertently overpromised liquidity to the users” and “the users have assumed much more liquidity than the underlying asset class can serve,” he said. (SB here: I agree.)

- El-Erian suggested areas such as emerging markets and high-yield bonds could be faced with a liquidity crunch in the future. “What happens if certain sectors have overpromised liquidity? Do you get contagion or not?” he asked. (SB: Let’s keep on our radars.)

El-Erian’s conclusion – A Beautiful Deleveraging is Probable

- “For the first time in a very long time, there’s reason to be optimistic about fundamentals gaining enough traction to validate asset prices,” he said.

- Investors just have to expect a bumpier ride this year than last:

- “The world I’m describing is a world in which even the long-term investor has to have a tactical layer on top of the structural and secular layer.”

- “We are coming out of one paradigm and going into another paradigm,” El-Erian added.

- “There’s more probability of success than failure, but it’s not overwhelming.

El-Erian began his presentation asking the audience to take a live poll. The question: How many of you feel we are in a bubble. Approximately 30% answered “yes” and 70% said “no.” He went on to present his case for why he believes we are not in a bubble. At the end of his presentation, he again asked the same question. 25% “yes” and 75% “no.” He laughed at himself for his inability to make an impact. For the record, I’m solidly in the “yes, it’s a bubble” camp. Not sure how we can disregard global negative interest rates and correspondingly record high equity market valuations. Doesn’t mean market crash, but it does mean ultra-low forward returns. Can central bankers land this puppy? Beautiful or ugly deleveraging? Beautiful is looking better. How we exit we just don’t yet know. Watch price, watch trend and keep a level of downside protection in place.

“Quantitative Tightening and Its Implications”

To me, the biggest bubble of them all is in the bond market. Rising inflation is a risk, rising defaults is a risk and rising interest rates will be the result of those events and be the pin that pricks the bubble. More on that in my “OK, hit me with it.” answer below.

But before we go there, let’s story through a few select slides from Jeffrey Sherman’s Inside ETFs keynote presentation. Many are self-explanatory. I’ll add comments where appropriate.

More than $36 billion has already flowed into bond funds in January, meaning U.S. retail investors are making the biggest bet on bond funds since October 2009, and at a time when many high-profile investors are sounding alarm bells about the end of the 30-year-plus bull market in bonds. Jeffery Sherman and Jeffrey Gundlach are two high profile names.

As David Santschi, CEO of Trimtabs, recently said on CNBC, “Bond funds are down in the past four months,” he said. “The biggest mispricings in the world today are in bonds, not stocks.” Reminds me a bit of the record high investor capital flows into stock funds in March 2000.

Conclusion: Sherman say interest rates will move higher with more growth. Let’s look at some slides:

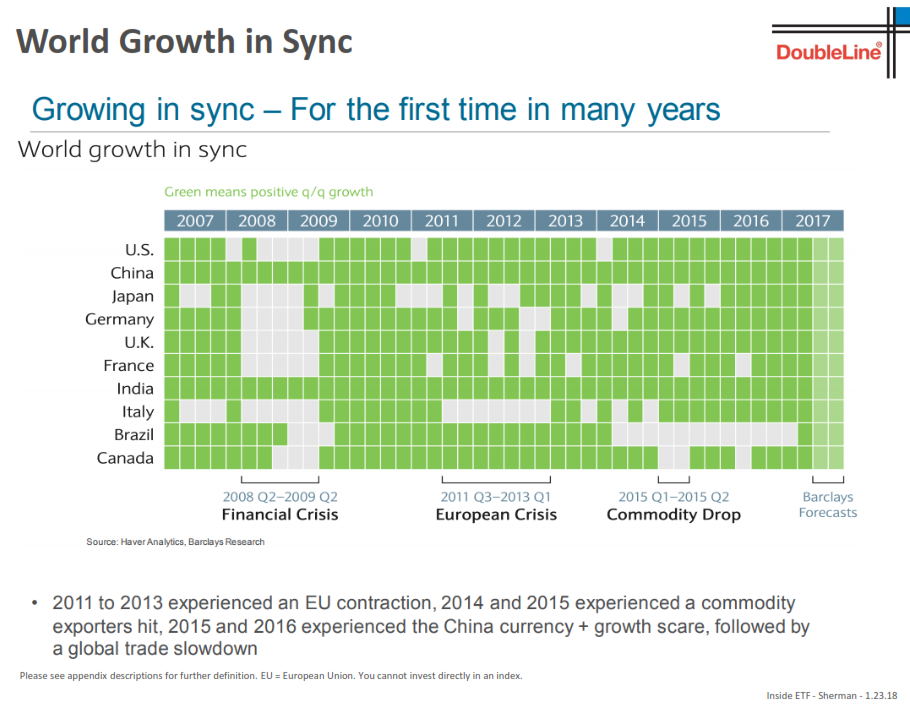

Similar to El-Erian, Jeffrey says the world is growing in sync for the first time in many years:

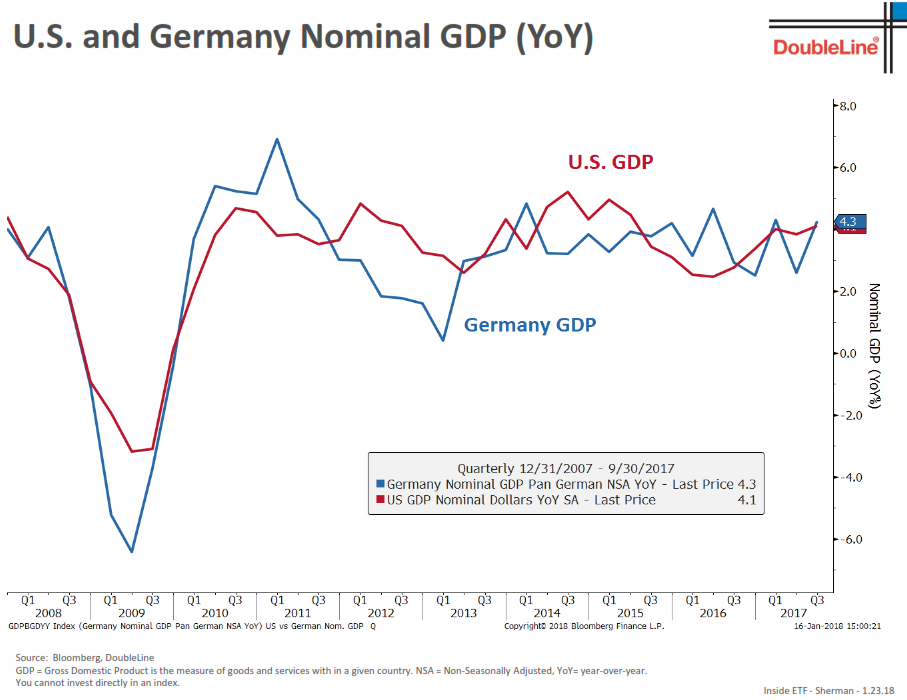

GDP growth in the U.S. and Germany before factoring in inflation is pointing higher:

The German labor market is getting tighter. Rising wage pressures are inflationary. Such growth and pressure will move ECB (European Central Bank) from QE to QT (quantitative tightening). Remove the unnatural central bank buyer of bonds will cause rates to move higher. Inflation pressures will cause ECB to raise rates. Thus, higher interest rates.

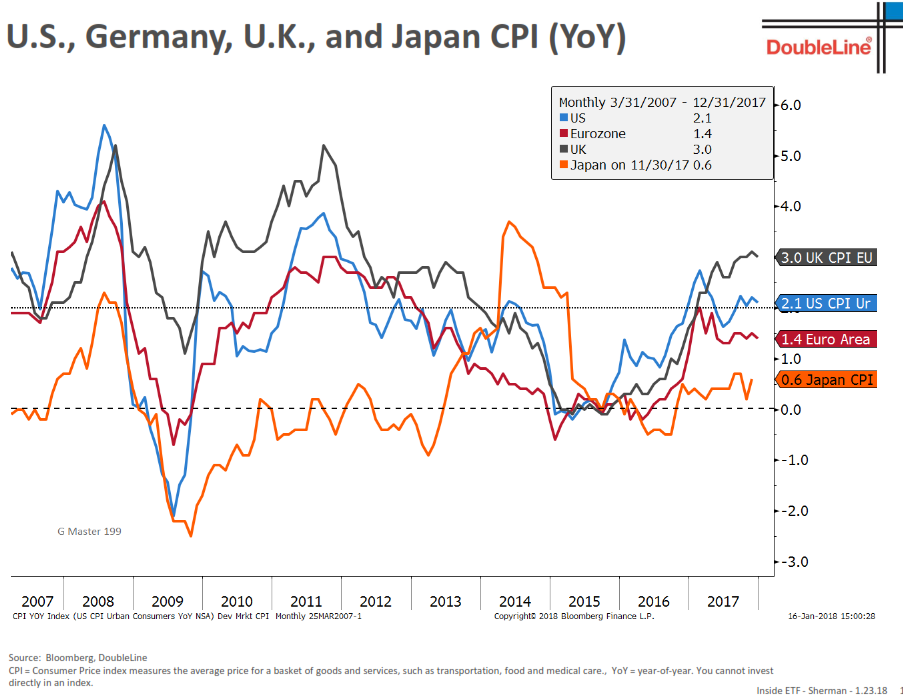

Next chart shows year-over-year CPI change. Inflation is picking up in the U.S. and UK. Inflation remains subdued in the Eurozone and Japan.

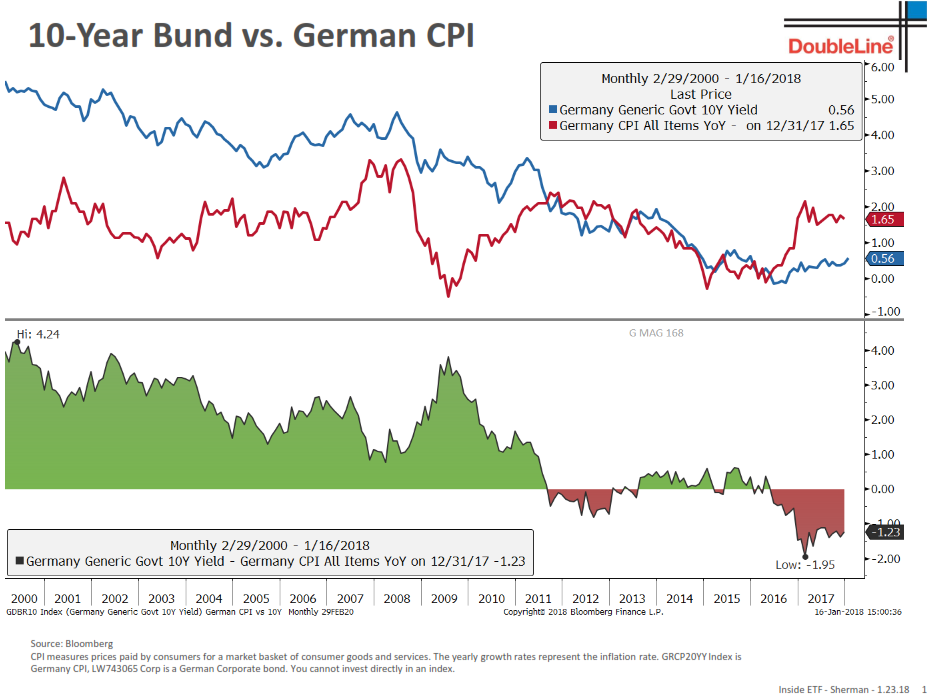

Watch for a pick-up in German CPI (inflation pressure). This next charts shows us that since 2000, the yield on the 10-year German Bund (blue line) has been higher than the YoY rate of change in CPI (inflation) most of the time. With German CPI running at 1.65% and the yield on the 10-year at 0.56%, something has to give. Expect higher yields (blue line to rise above the red line).

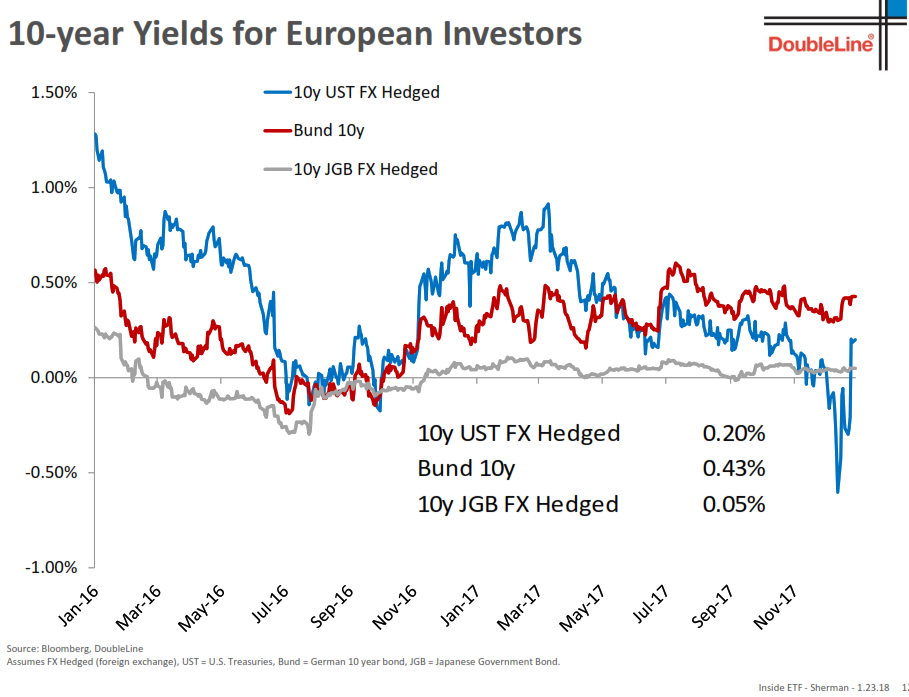

Now, with the U.S. Treasury 10-year yield at 2.60% and the 10-year German Bund yield at 0.56%, you and I would expect money to flow from Europe to dollars to Treasurys, but that hasn’t meaningfully happened. Why? This next chart tells the reason (I was surprised to see it and had been wondering why the dollar hasn’t been stronger – in fact it’s been weak – so this next chart makes sense). What it shows is that if a European investor exits Bunds (priced in Euros) and converts to dollars to buy Treasurys, they hedge their currency exposure. Or they are taking two bets. One in yield and the other in currency risk.

The chart shows that after hedging costs, the yield on the 10-year in Euro terms (hedged dollars vs. Euros) is just 0.20%. So not enough “vig” to make the investment. Thus, the yield spread differentials from the European investor’s perspective are not yet attractive enough to buy Treasurys. Let’s keep an eye on this as time steps forward.

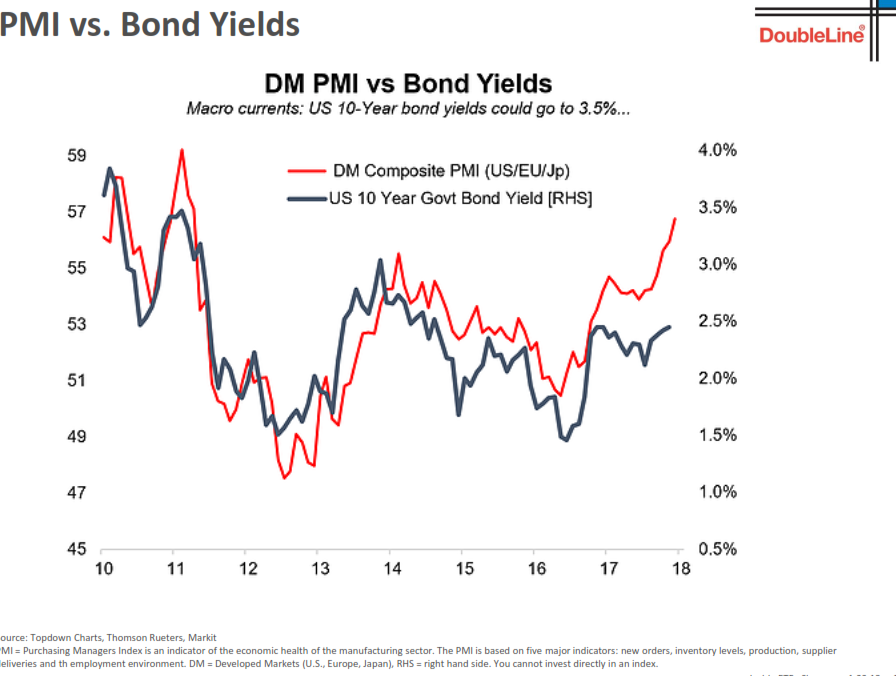

A more global look at inflation is this next chart. It looks at a composite of the developed economies (U.S., Europe and Japan) Purchasing Managers Index or “PMI” and plots it against the U.S. 10-year Treasury. Note the high correlation that the blue line (Treasury yields since 2010) has to the red line (Developed Market PMI). Conclusion: the 10-year Treasury yield could go to 3.50%.

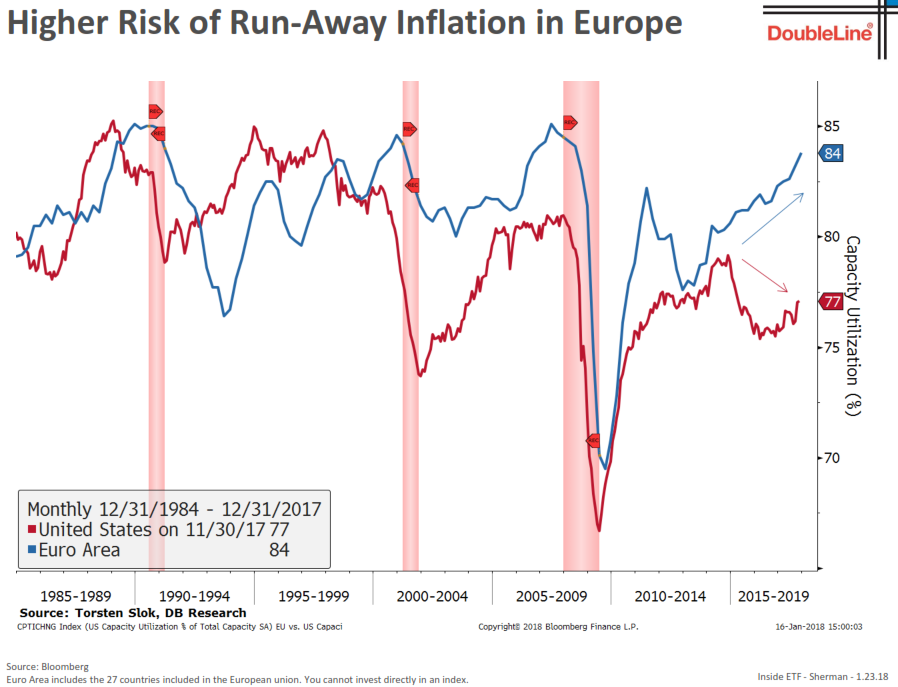

And Sherman sees a higher risk of runaway inflation in Europe (blue line next chart) than in the U.S. (red line).

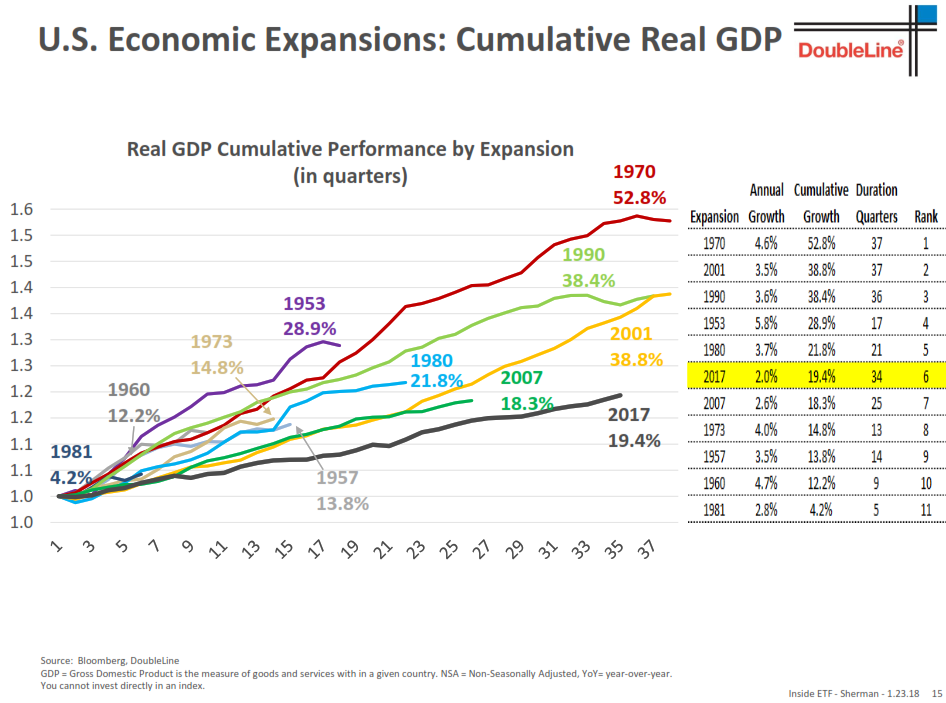

Hold this next chart in the back of your mind for when we get to the Steve argument. This chart shows all of the post-WWII economic expansions on one chart. Note, we are experiencing the worst post-recession expansion (green line). Also note that this expansion is getting old.

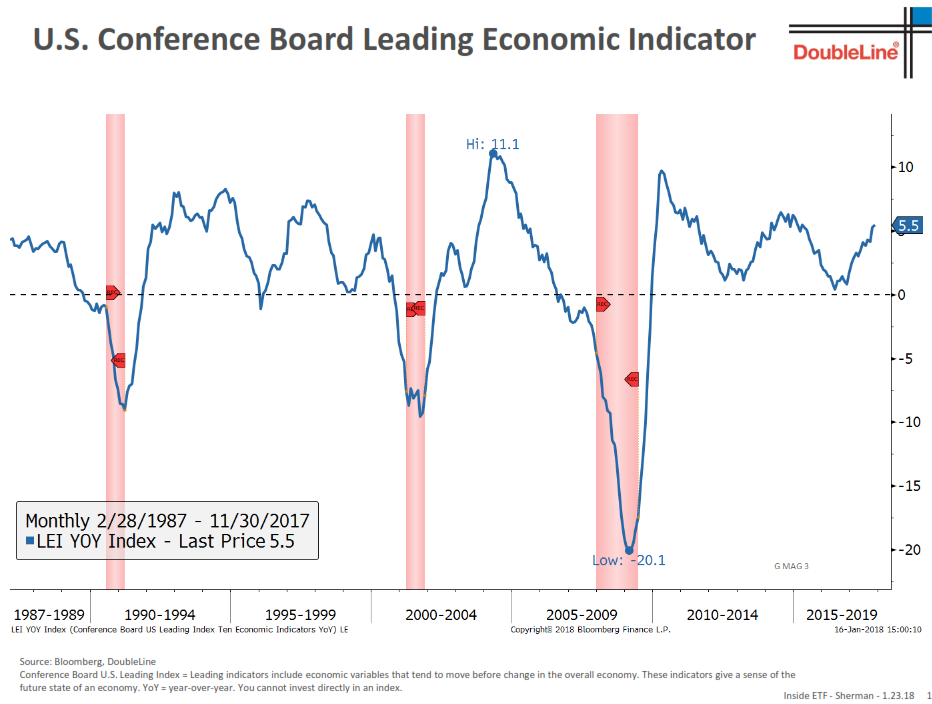

The U.S. economy looks good and is trending higher. Note history of recessions (pink vertical lines) when the blue line drops below the dotted mid-line (0). Not perfect, tends to lead… so when it crosses, we should take note.

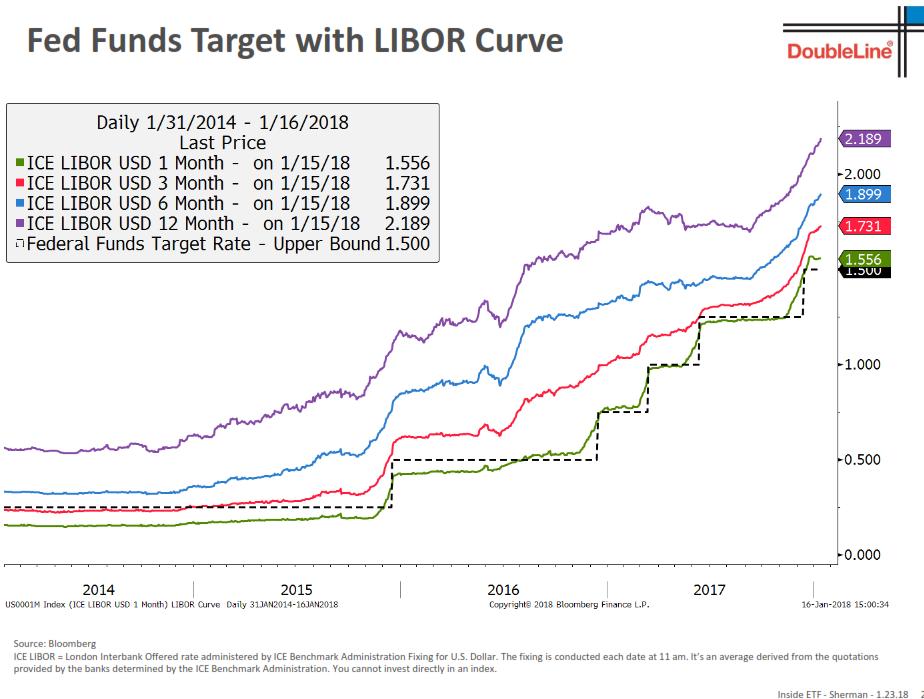

Next note the move up in the base cost of capital as measured by LIBOR. Rates are moving higher. Means cost of funding is moving higher.

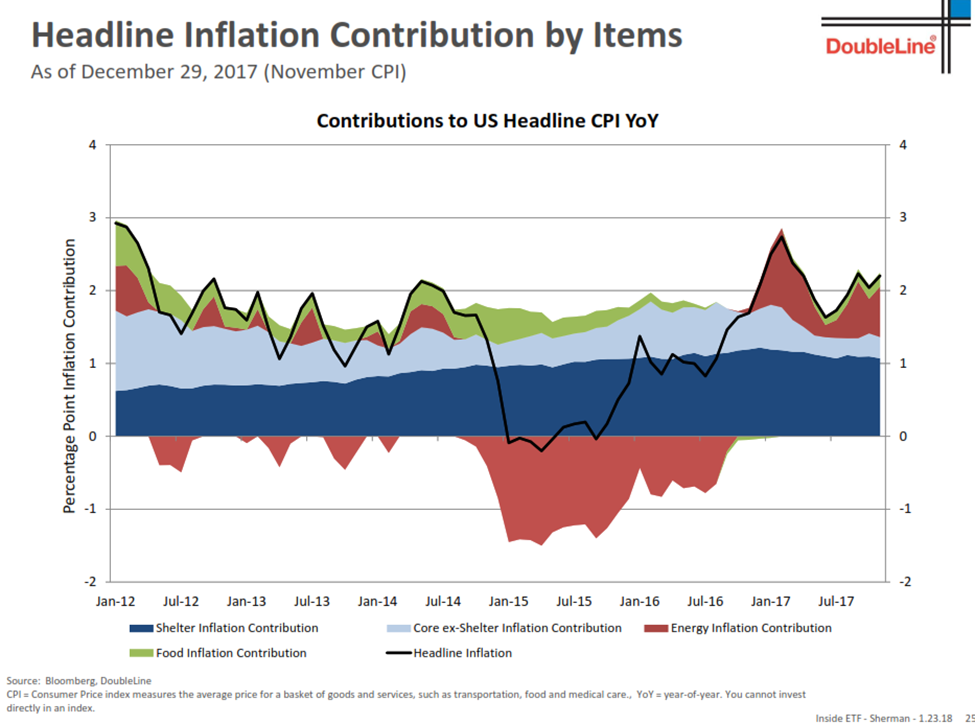

Next is a pretty cool chart. It shows headline inflation and the inflation contributions by categories (Shelter, Food, Core inflation ex-Shelter and Energy). Since 2012, the big contributors are coming from Shelter and Energy. Overall, nothing too concerning on the inflation front just yet.

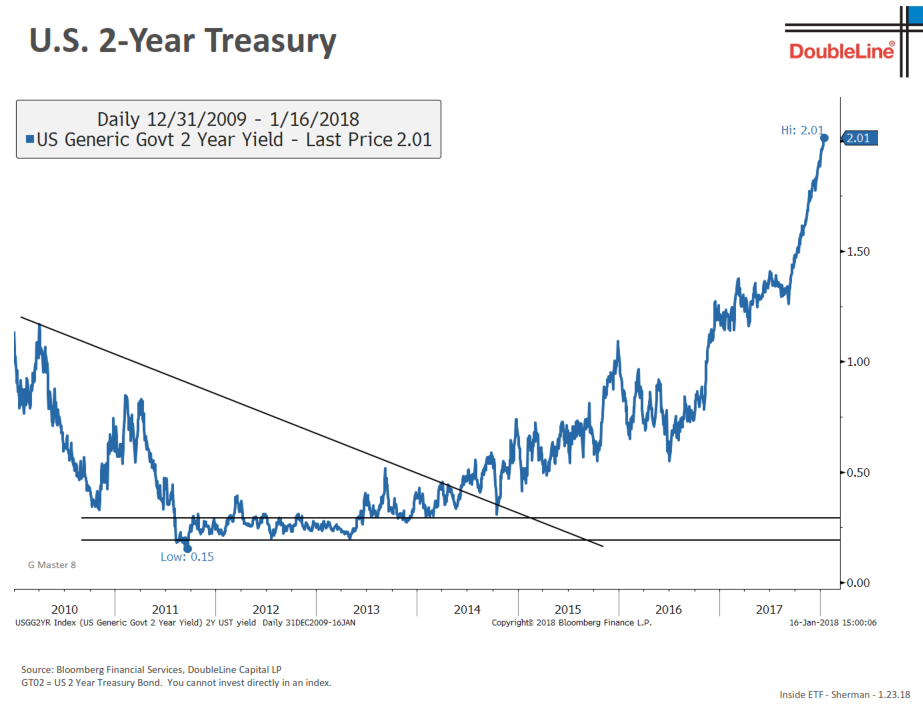

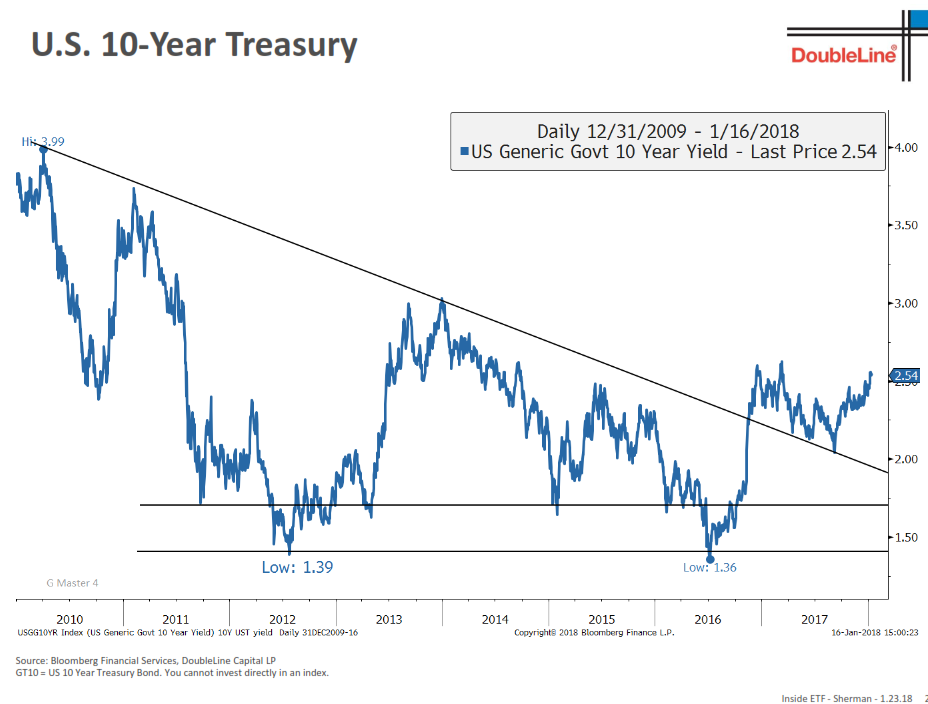

But rates have been moving higher. Note how the 2-, 5- and 10-year yields have crossed above their longer-term trend line (the black line descending from upper left to lower right in the next three charts). The breach of the long-term trend is a technical sign that the long-term bull market in bonds is over…

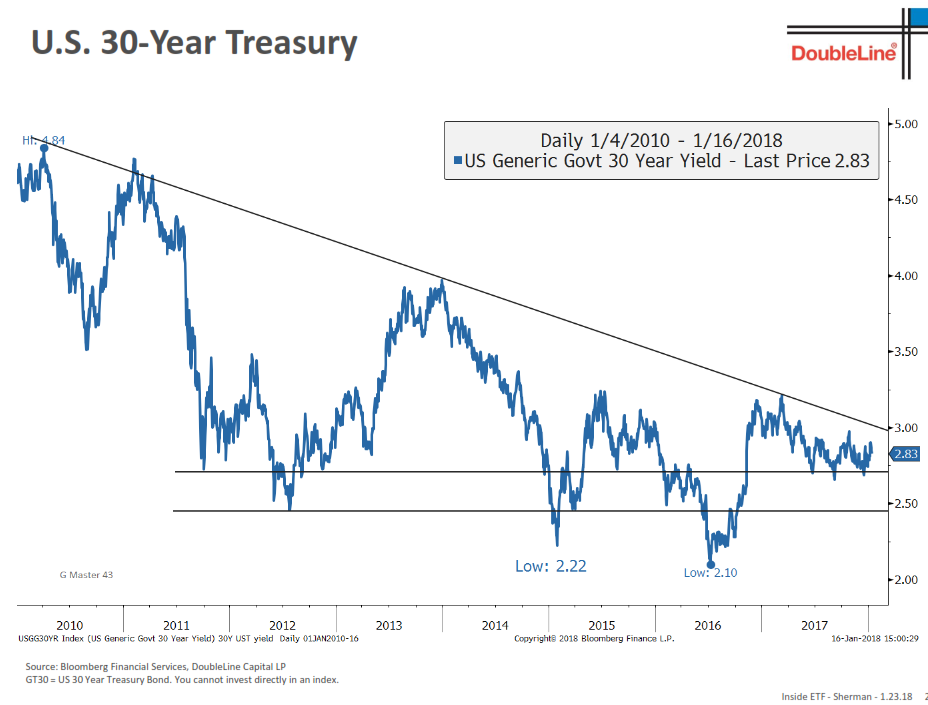

However, the 30-year has yet to move above its long-term downward sloping trend line. Keep an eye on the 30-year yield moving above 3%.

Sherman and DoubleLine believe rates are heading higher. But what categories of the bond market are most at risk? The next few slides are scary to some, but boy do I see coming opportunity.

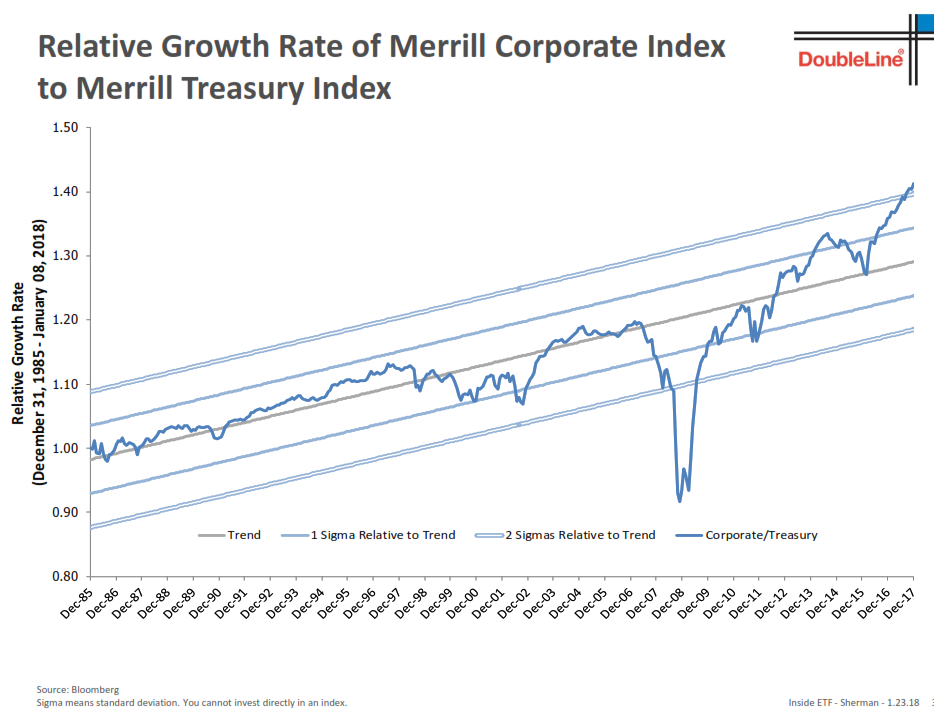

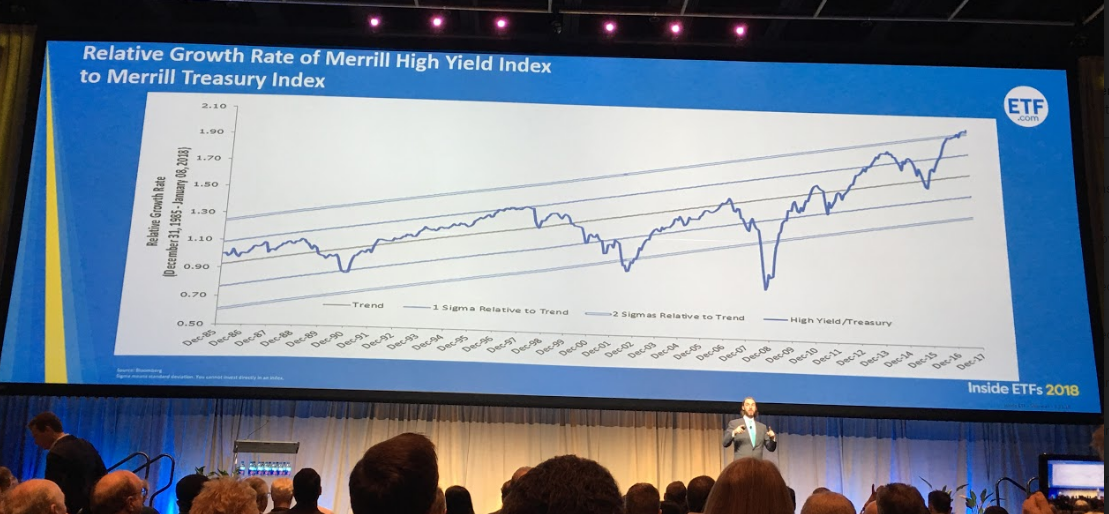

The first is a look at a comparison of trend in the relative growth rate of the ML Corporate Bond Index to the ML Treasury Index. I know this gets a little “geekish,” but let’s see if I can put the risk and opportunity into plain English.

Here is how you read the chart:

- Data is from 1985 to December 2017.

- The gray line plots the trend line of the relative growth rate of Corporate Bonds to Treasurys. What it is doing is identifying if corporate bonds are overvalued or undervalued relative to safer Treasurys.

- The darker blue line plots the difference over time. Note for example in 2008 how undervalued corporates were to Treasurys.

- The light blue lines plot something known as Standard Deviation. It is simply a measure of how far something is from its trend line. Some geeks call it “sigma.” Sigma does sound a bit cooler.

- A 1 sigma move is a rare event. You can see how few times the dark blue line breached the upper and lower 1 sigma lines.

- A 2 sigma move is even rarer. Since 1985, the high grade corporate bond market has never been above a 2 sigma line. Not once.

- It breached the 1 sigma line just once and that was in 2013.

- If you are looking for a big bubble, you can find it in corporate bonds.

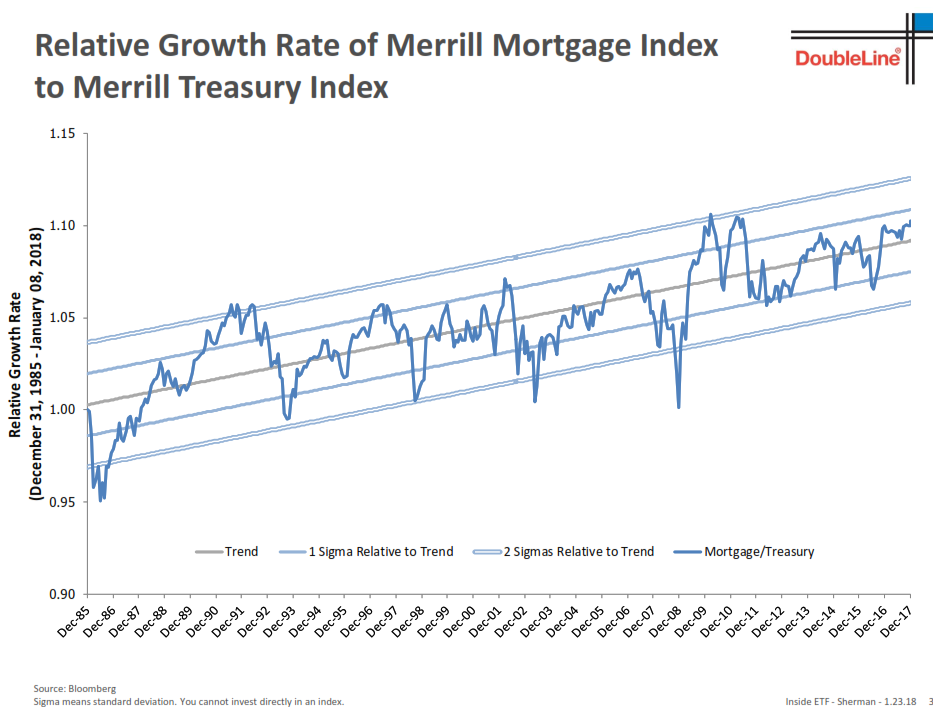

What about mortgage bonds? They were an issue in 2007. Big bubble then. Not an issue today. Note how close to the long-term gray trend line the dark blue line is today (upper right side of chart).

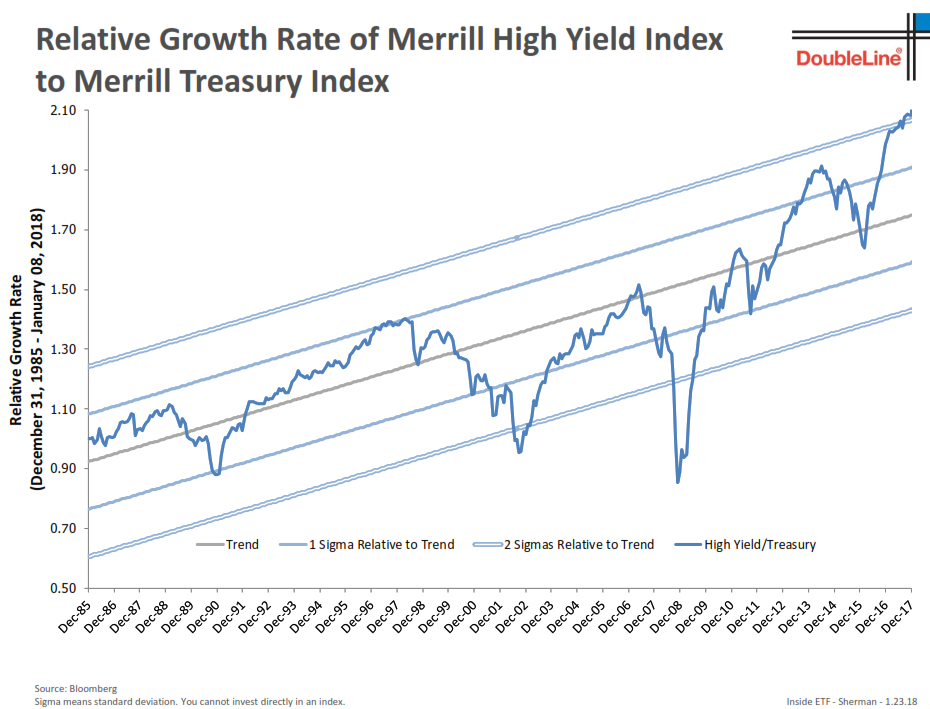

The same is true for non-agency MBS (mortgage-backed security bonds) but not so for high yield junk bonds. And this is an area I know much about and thus my excitement.

Read this next chart that same sigma way. Gray line is the trend line. Note the upper right-hand side of chart… the breach above a 2 sigma move. First time ever!

Why the excitement? In 1991, I was really scared. I ran a big book trading the trend in the HY junk bond space. I grabbed my nose and jumped in when the trade signal said buy. By 1997, HYs hit the 1 sigma line. Overvalued, I expected a correction and wrote about the craziness of the tech bubble. However, HYs partied on until 2000. We made money but not like tech. And made about 30% from 2000-2002 when tech went down 75% and the S&P 500 went down 50%. But we made really big money in 2003 and 2004. Why? We moved to cash and side-stepped most of the HY crash. Note the 2 sigma breach to the down side. Investors panicked out, defaults spiked in recession and yields went towards 20%. On the other side of the recession/selling was great opportunity. That’s when we bought back in. Same story but even better in 2007/08. Yields in early 2009 reached 22+%. We were buyers and taking advantage of the panic.

Fast forward to today. In my 28 years trading HY, never have I witnessed a 2 sigma overvalued breach. Stay tactical and risk minded. The other side of the next reset will be awesome, like the late 1990s. Until then the trade limps along.

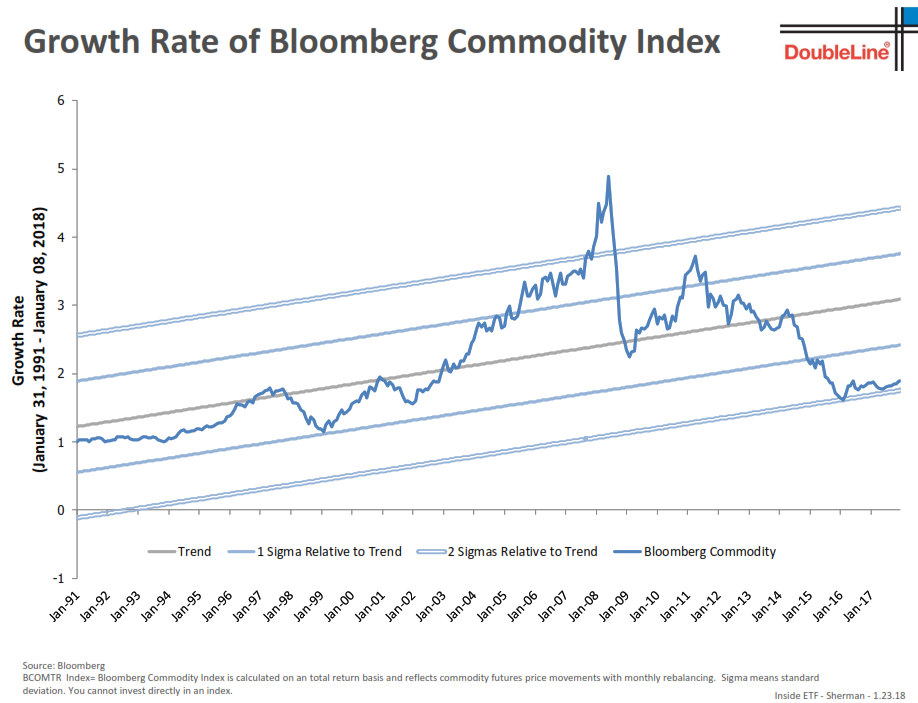

OK, back to Jeffrey Sherman. There were more slides but I’ve hit you with enough for now. DoubleLine sees opportunity in commodities. That makes sense to me. Especially, if you are looking for underappreciated out of favor risks. In “sigma language” it looks like this:

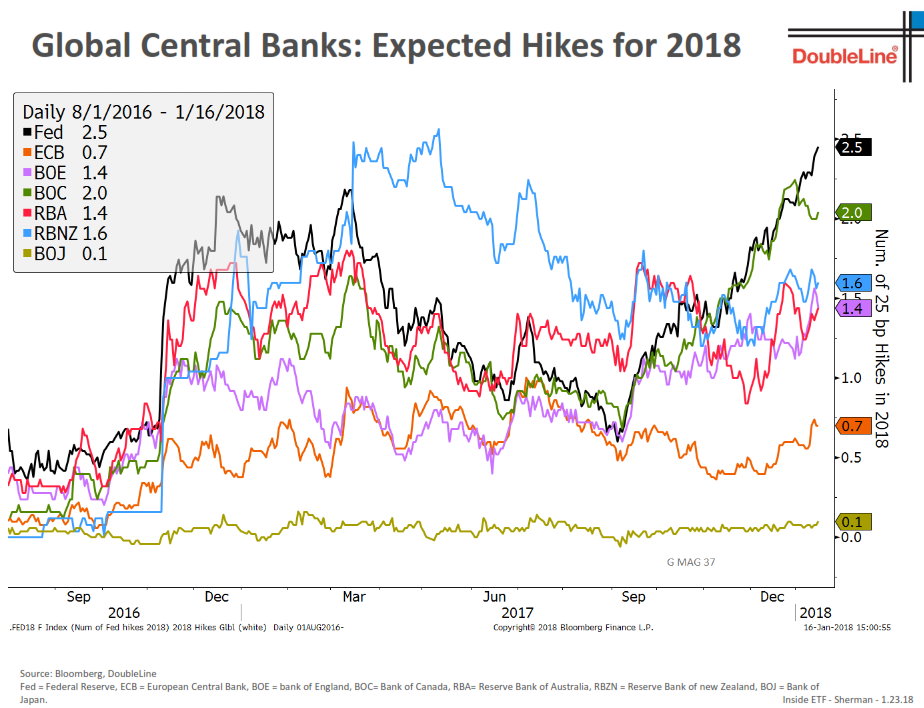

And one last nail in the rates are moving higher category. Global central banks are expected to hike in 2018. Let’s hope they don’t all exit QE at the same time.

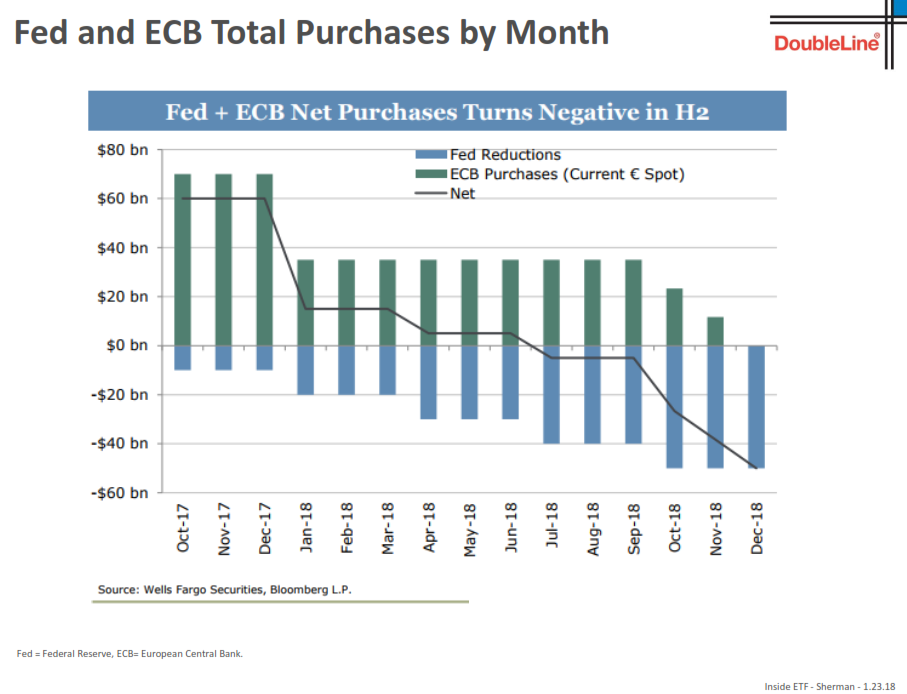

But that seems to be the plan. The Fed and the ECB go negative in terms of net purchases in June 2018. We will soon learn if the markets and economies can handle the loss of our extremely well-funded patriarchs.

Importantly, here are DoubleLine’s disclaimers:

OK, Hit Me with It!

Market gurus, including Jeff Gundlach and Ray Dalio, recently have sounded sour notes on bonds, with Gundlach’s firm, DoubleLine Capital, saying that, among stock market hedges, it’s commodities that look like a good bet for 2018 and that bond yields, which move inversely to bond prices, will continue to rise.

Bill Gross said, after more than 30 years, the bond bear market has begun. Investing legend Bill Miller said in his latest letter to investors this week, “Bonds, in my opinion, have entered a bear market,” Miller wrote, but he added, One that is likely to be benign for the next year or so.”

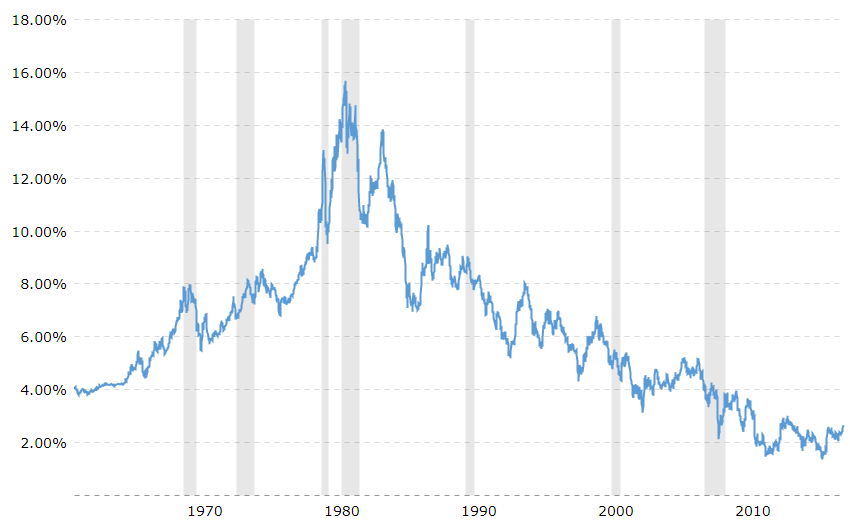

At dinner last Tuesday night with Jan vanEck and the VanEck team, we debated the direction of interest rates. Consensus is that interest rates are headed higher. That’s bad news for bonds. For 35 years the direction of interest rates has been down. It looks like this:

30-Year Treasury Bond Yield (from a high yield of almost 16% in the early 1980’s to 2.90% today):

I told Jan and his team that I believe interest rates are going higher over the near term but I can make an equally convincing argument that interest rates going to make one more challenge at the low. To which Jan said, “Really,” Jan said, OK, hit me with it!”

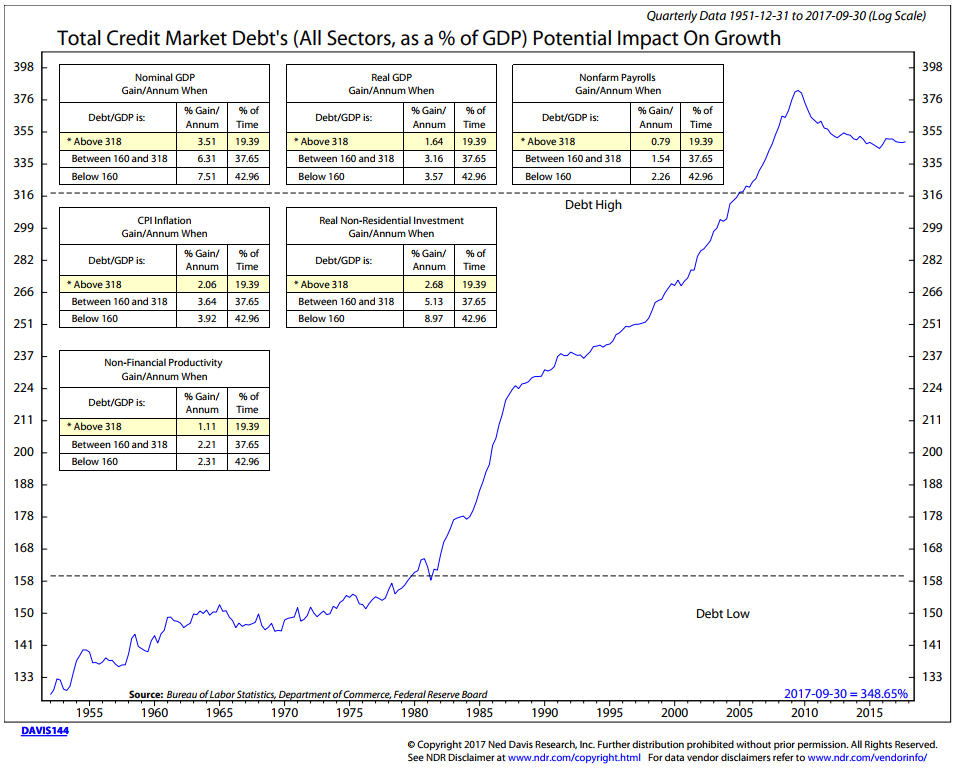

I believe rates move higher then make one last dive towards the 2016 yield lows. The problem is that global debt is over 275% of global GDP. Much of it is short term in nature. The move higher in rates is asymmetric, meaning that a move higher in rates will quickly hit governments, corporations and individuals in the wallet. Consumer credit card and student loan debt is once again off the charts. Significant historical research shows that countries run into slow growth problems when debt-to-GDP rises above 90%.

Global debt hit a record high $233 trillion in Q3 2017. Up more than $16 trillion since the end of 2016. The ratio of global debt-to-GDP (debt-to-growth) is 294%. Folks, we are at historical high levels.

High debt impacts growth. In the U.S. alone it looks like this:

- Note that when debt is high, global grow is slow.

- Add rising rates to the equation and the problem becomes more severe.

Source: Ned Davis Research

So I contend that high interest rates will have an immediate impact on growth. I argue that the Fed will raise interest rates supported in part by a pick-up in short-term growth and modestly rising inflation and that like every time since the 1950’s, their rate hike game plan will put us more quickly into the next recession.

My friend John Mauldin told me this morning that BCA Research’s Bank Credit Analyst is forecasting recession in 2019. Will that change the interest rate glide path? I think it is probable. Recessions are an important part of the business cycle, we do get them and we’ll get another. We have had one or two recessions each decade in the last 100 years. If we don’t get one by 2019, it will be the first time since the Fed was born (early part of last century) that we didn’t experience a recession.

Yes on infrastructure spending, yes on deregulation and a big yes on the bump the tax cuts are giving the economy. Animal spirits indeed! But I believe the current up move in rates will be quickly capped due to the Fed raising rates (higher interest rates) and the Fed exiting QE and due to the massive level of debt, the Fed will drive us into recession. El-Erian is right with his risks. If all four major central banks raise rates and reverse gear on QE (move to QT), then the economy hits the skids.

Thus, you may just get one more shot at refinancing that mortgage when the 10-year Treasury yield dips below 2%. I see 3% first, maybe a quick jump to 3.5% then one more dive below 2%. Depends on global central bank policy. Timing is unknown. Keep a close eye on what trend evidence is telling us. That’s my base case. We’ll see.

Trade Signals — Markets Reach New Highs with Extreme Investor Optimism

S&P 500 Index — 2,839 (01-24-2018)

Notable this week:

Broad market indexes continue to set new record highs. Bullish trend continues for equities. The Don’t Fight the Tape or Fed moved from a +1 (bullish) reading back to a neutral “0” reading. The Ned Davis Research CMG U.S. Large Cap Long/Flat Index remains 100% invested in large-cap equities. Despite recent moves higher in interest rates, the Zweig Bond Model remains bullish on fixed income. HY remains in a buy signal. We continue to monitor our inflation and recession indicators. Despite extremely high equity valuations, the trend evidence remains bullish.

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note — Avoid the Vortex (and a Few Photos from the Conference)

As conferences go, the Inside ETFs Conference is an important one for me and my team. The idea flow and networking is invaluable. Perhaps the biggest take-away for me is the pure entrepreneurial spirit that exists in the industry. I saw a few new ETFs that we’ll be considering within our portfolios and a few where I scratched my head and whispered to myself, “What are they thinking?” But in the end it is you and me that benefit. ETFs remain a growing, viable tool for you and me to use to make money.

The sponsor hall was huge. I grabbed a few pens and golf balls but right next to my daughter’s firm’s booth was the MSCI booth and they were giving away eagles dressed with a blue MSCI scarf. Well everyone in Philadelphia is excited about our Eagles making the Super Bowl so I grabbed an eagle and removed the scarf. We bleed GREEN.

Go EAGLES!

Dad and Brianna

Serena Williams and Barry Ritholtz (Serena was awesome!)

Good friend Russ Brooks

Jeffrey Sherman and his HY 2 Sigma Chart

Steve, John, Carly, Jon, Brie, Omino and Rory

I board another flight this coming Tuesday afternoon for a day of skiing at Snowbird on the 31st. Then to Park City for a conference with about 80 industry friends. I promise I’ll avoid the vortex around the bar.

It looks like a quick trip to Dallas in late February, a trip to Austin on May 5, then on to San Diego for the Mauldin Strategic Investment Conference on March 6-9. It’s an outstanding event. I’m going to try to sit down with Dr. Lacy Hunt and Jeffrey Gundlach or get John and his Mauldin Economics team to put them together on a panel. Both with strong convictions: Lacy in the rates-are-ultimately-headed-lower camp. The great bond bull market lives on. Gundlach, as noted, is on the other side of that trade. It is the type of high impact, brilliant mind stress testing that goes on at the Mauldin Conferences. Hope to see you there… sign up information is below (I don’t get a dime… just a big fan).

MAULDIN SIC INFORMATION: Registration and agenda information for the Mauldin SIC can be found here. Dr. Lacy Hunt, David Rosenberg, George Friedman, Mark Yusko and Jeffrey Gundlach are but a few key names who will present. Gundlach is saying the great bond bull market is over. More note taking to share with you.

Wishing you the very best! Have a wonderful weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group