January 2018

During the fourth quarter, the stock market, as measured by the S&P 500 Index (the S&P 500), rose another 6.64%, propelling its full year 2017 total return to 21.83%. This reflects the continued low inflationary economic expansion, rising corporate profits and a very clear pro-business agenda in Washington. Whatever else one can say about the Trump administration and the Republican Congress, it is undeniable that the current regime has rolled back many regulations that business found onerous and has passed historic tax legislation that favored business by lowering the corporate tax rate from 35% to 21%.

The first order effect of a lower corporate tax rate is to increase companies’ after-tax profits. Since higher earnings reduce the market’s price-to-earnings ratio, the market is less expensive than before the tax cut. The second order effect will likely result in increased dividends and stock buybacks. The third order effect may be greater capital spending, but this will likely take time to play out. Finally, since taxes are a cost of doing business, a fourth order effect will be to lower corporate costs, thereby allowing companies to compete more aggressively by lowering prices.

This final point brings us to our favorite economic topic of the day, namely: How can inflation remain so low with an expanding economy and falling unemployment? Why are there not shortages driving up commodity prices, and why doesn’t labor have the power to demand higher wages? The answer lies in the combination of globalization, and more importantly today, technology.

Globalization has opened labor markets such that when U.S. workers demand higher wages, companies are able to move production to countries with cheaper labor costs, such as China. Likewise, as a company seeks to reduce labor costs, it can also replace workers with capital. This used to mean a machine but today more likely refers to a robot, artificial intelligence or some other device or process powered by information technology.

The growth of information technology has transformed the U.S. economy and is, in our opinion, the principal reason that inflation remains low. Because of the way the national accounts are calculated, it is hard to decipher exactly how pervasive information technology has become. This reflects the fact that tech is a combination of hardware or tangibles (e.g., computers) and intangibles (e.g., software), which companies can buy or develop themselves. To the extent it is developed in-house, software does not show up in the national accounts and so total tech spending is thus understated. While we, therefore, cannot get a clear picture of just how widespread tech has become by studying gross domestic product data, we can get a proxy by looking at how tech has grown as a percent of the stock market: The technology sector represents about 25% of the value of the S&P 500 today, up from 5% in the early 1990s, a 5-fold increase! In the U.S., intangible investment, which you can think of as a proxy for high tech spending, first exceeded tangible investment in the mid-1990s, smack in the center of the dot-com boom, and has continued to grow faster ever since. Technology has become pervasive.

Technology is subject to Moore’s Law, which states that computing power doubles about every 18 months through technological advances. This means the cost of many tech products is constantly falling. Moreover, the knock-on effects from the application of technology to business processes are to reduce costs throughout the system and, thereby, enable businesses to compete more aggressively on price. Vanguard recently published a paper* in which they estimated that technology has had an overall depressing effect on inflation of about 0.50% per year, chiefly by reducing businesses’ production costs and, ultimately, final prices.

In energy, thanks to advances in fracking and horizontal drilling, the breakeven costs for drilling new oil wells has fallen sharply from about $60/bbl a few years ago to around $30/bbl today. According to the EIA Drilling Productivity Report, new well oil production per rig has risen from under 100 barrels per day in 2008 to over 600 barrels per day in 2017.

Telecommunications have also been revolutionized through the application of digital technology and the emergence of mobile telephony. Some of us remember when the cost of a long-distance call was many times more expensive than a local call. Today there is no difference and all calls are a lot cheaper on a constant dollar basis. According to U.S. government statistics, the price of telephone equipment declined 5.7% per year from 1963-2009.

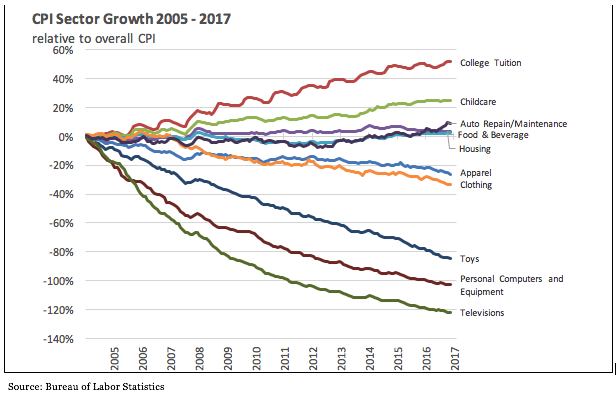

The cost of computing has plummeted, thanks to Moore’s law. Consumers have clearly benefited from lower prices that have been driven by technological advances. As you can see in the chart below, while the costs of labor-intensive activities such as education, health care and car repair have continued to rise, the costs of products and services with a heavy tech component have plummeted. This effect is particularly dramatic in computers and televisions. Moore’s Law is relentless.

We could go on and on with examples of technology’s impact in industry after industry, but we think the preceding examples make the point. Technology is inherently deflationary and is becoming an ever larger part of the economy. This explains the anomaly that first showed up in the 1990s as the economy enjoyed a long expansion but inflation failed to ignite. The same phenomenon has been apparent in the current post-2008 expansion.

While we are clearly among those who put a great deal of weight in the structural deflation argument, we do think at some point cyclical factors could prevail and cause inflation to rise. This could happen in the next year or two as low unemployment causes labor shortages and attendant wage increases. It could also occur if growth in demand for commodities pushes up commodity prices. We are seeing this in oil now.

Having said this, we believe the economy will continue to expand over the next year or two (and possibly longer), that corporate profits will continue to grow, that inflation will remain stable or grow modestly and that the Federal Reserve will therefore raise interest rates at a slow, steady pace, which will allow the stock market to move higher. At some point there will be a correction, but a true bear market appears more distant. It is also possible the market rallies substantially in a “blow-off” before correcting, making it important to remain invested.

Our focus will continue to be on strong companies with growing market share, robust balance sheets, growing earnings and, in many cases, rapidly growing dividends. In an ideal world, we would like to uncover such companies when their stocks have been battered by bad news or some other temporary setback that makes them cheaper than they should be, but after eight years of a bull market this is hard to do. So rather than buy lesser quality companies based on “bargain” valuations, we think it more prudent to buy leading companies at “reasonable” valuations. As we have pointed out in previous Outlooks, the economy is evolving in a way that favors leading players in each industry and penalizes second and third-tier competitors. Owning quality is a way of reducing risk and enhancing potential returns.

We wish all our clients much health, happiness and wealth in the coming year. We appreciate your loyalty and the confidence you have placed in us.

Sincerely,

John Osterweis

*Davis Ph.D., Joseph (October 2017) “Why is inflation so low? The growing deflationary effects of Moore’s Law”, Vanguard Research

____________________

Past performance is no guarantee of future results. Index performance is not indicative of fund performance. To obtain fund performance call (866) 236-0050 or visit osterweis.com.

This commentary contains the current opinions of the author as of the date above, which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed.

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large-cap U.S. stock market performance. One cannot invest directly in an index.

Moore's law refers to an observation made by Intel co-founder Gordon Moore in 1965. He noticed that the number of transistors per square inch on integrated circuits had doubled every year since their invention. Moore's law predicts that this trend will continue into the foreseeable future. Although the pace has slowed, the number of transistors per square inch has since doubled approximately every 18 months.

Price-to-Earnings (P/E) ratio is the ratio of the stock price to the trailing 12 months diluted EPS.

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country's borders in a specific time period.

[30571]

© Osterweis Capital Management

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management