Retail sales figures for December showed a relatively strong trend in 4Q17, although part of that reflects a rebound from hurricane effects in 3Q17. Core CPI inflation was a bit higher than anticipated in December, but that doesn’t mean that the low inflation trend is over. However, eighteen states raised their minimum wages in January, and some expect this to flow through to higher prices. Perhaps. The market odds of a March rate hike by the Fed are rising (over 80% on Friday), but stock market investors are not too concerned. If the Fed is raising rates because the economy is strengthening, well, that’s a good thing. But what if that’s a mistake?

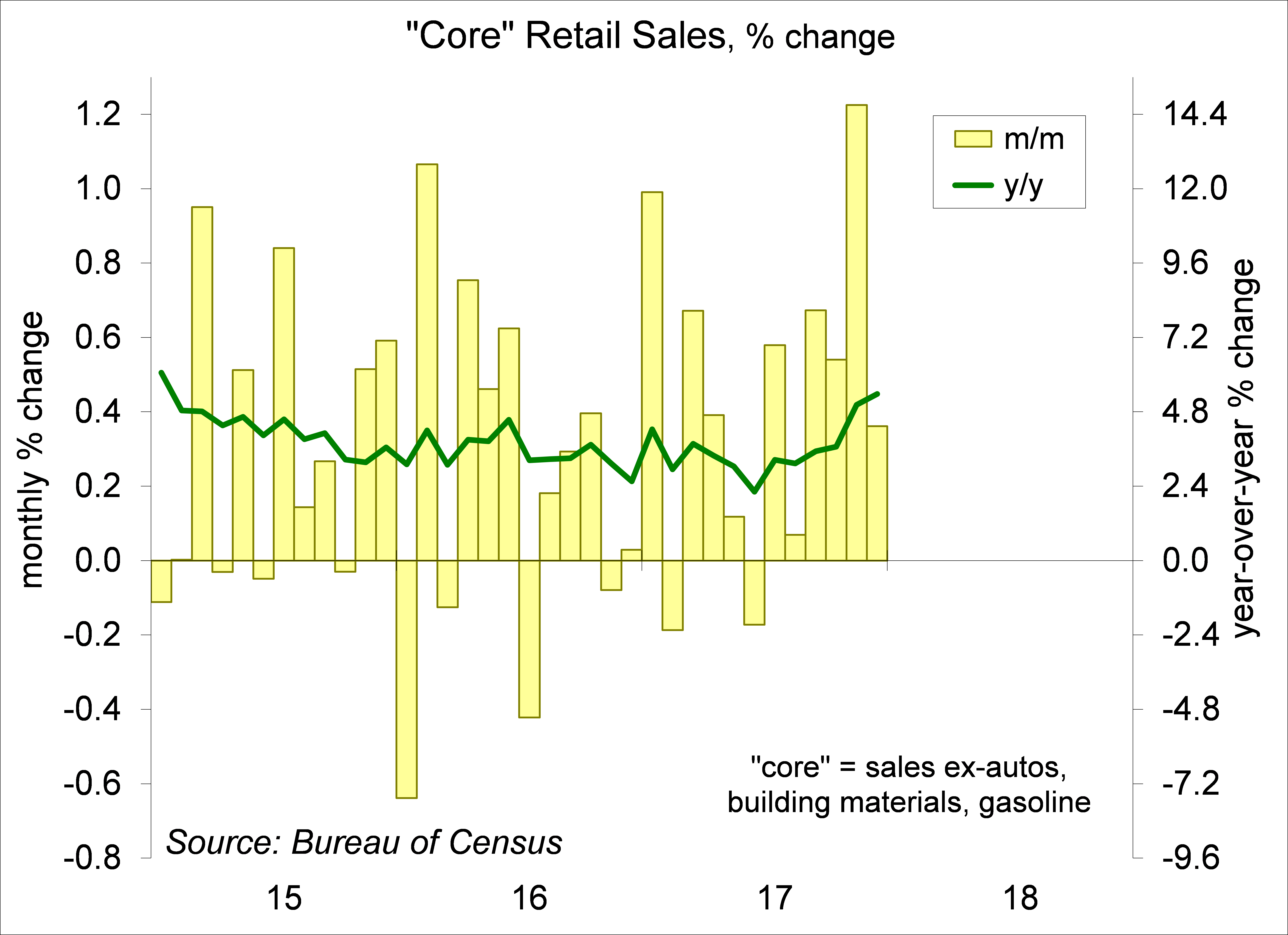

Retail sales exhibited a weakening trend through the first eight months of 2017 – not a sharp drop, more of a gentle slowing. Results for the final four months of the year were much stronger. This raises a number of possibilities. Consumer spending growth is often uneven across months and quarters. So, the 2017 pattern could simply be the normal variation around a moderate trend. We know that no matter their personal financial situation, consumers will spend during the holiday season. On the other hand, the consumer could be really picking up steam at this point, reflecting increased confidence about their ability to find jobs. Job growth, while expected to slow somewhat, has been supportive, but inflation-adjusted growth in average wages has been lackluster.

Click here to enlarge

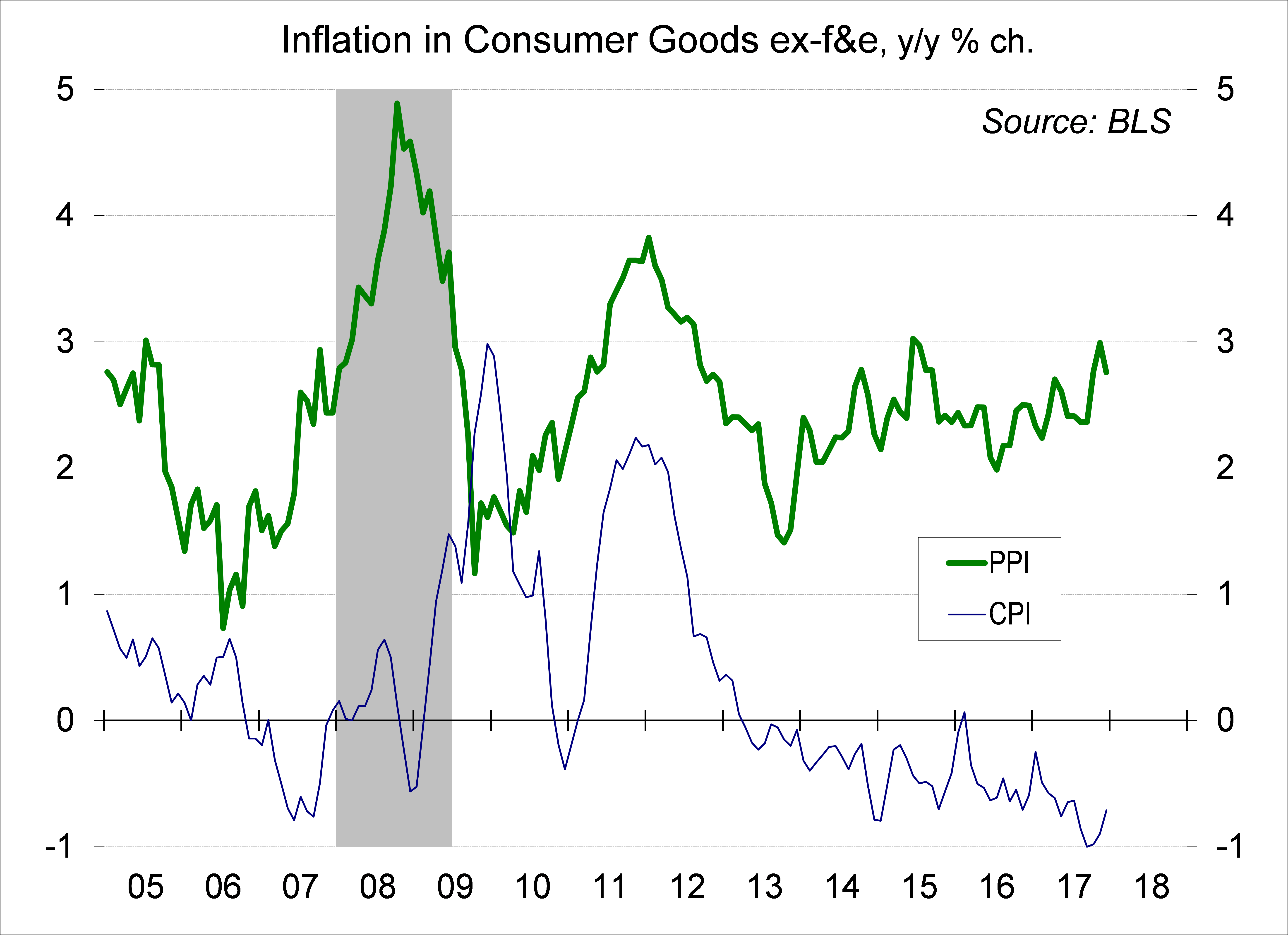

On the inflation front, the CPI rose 2.1% December to December, up 1.8% excluding food and energy. The core CPI increase is not far from the Fed’s 2% goal, but remember that the Fed’s gauge is the PCE Price Index, which is tracking 0.4 to 0.5 percentage point below the CPI year-over-year. The Producer Price Index showed some pipeline pressures in 2017, but we don’t see this as feeding through to the consumer. In fact, the CPI has continued to reflect a deflationary trend in consumer goods ex- food & energy.

Click here to enlarge

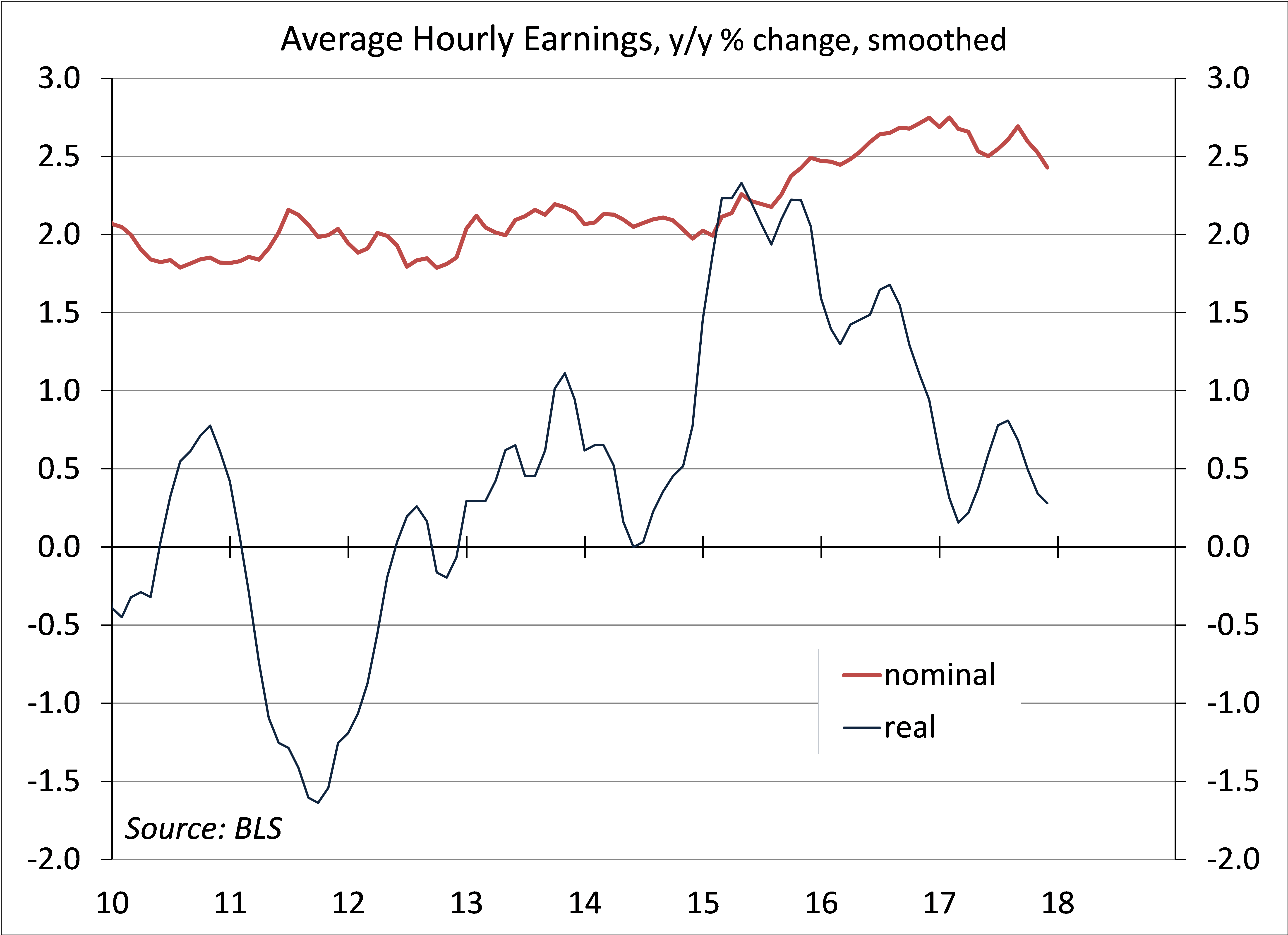

More importantly, the labor market is the widest channel for inflation pressure. We should see a pickup in average hourly earnings growth in January (to be reported in the February 2 employment report, which will include annual benchmark revisions). If not offset by faster productivity growth, wage increases could be passed along to consumer prices, but there’s no guarantee that will happen.

Click here to enlarge

Up until now, Fed rate increases have been about “taking the foot off the gas pedal,” not “hitting the brakes.” Monetary policy is close to neutral and the labor market is at or near full employment. There’s a good argument for the Fed to hold its fire, to facilitate a reallocation of labor toward its more efficient use. There may be more slack in the job market than we think there is. Raising rates to curb wage growth, as a means to contain consumer price inflation, could be a mistake. Conversely, the cost of waiting too long to tighten is potentially destabilizing rate increases later on, especially if accommodative policy fuels a financial bubble over the intermediate period. This is the dilemma Fed policymakers face in 2018.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James