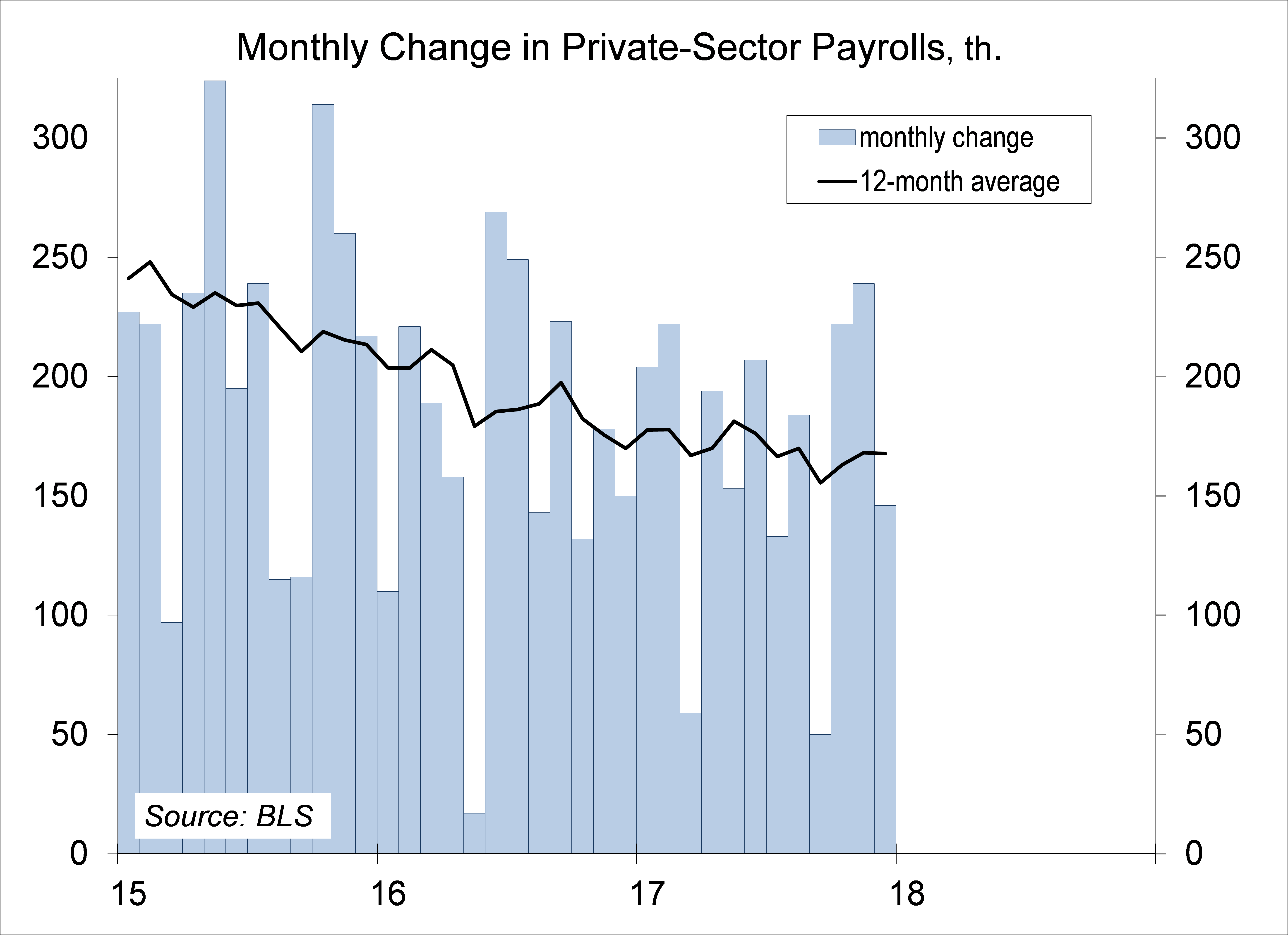

Nonfarm payrolls rose by 148,000, less than expected, in the initial estimate for December, but the increase was hardly “weak.” There is a fair amount of noise in the monthly figures, but the underlying trend is lower. Despite a tight job market, average hourly earnings were up just 2.5% year-over-year.

Prior to seasonal adjustment, holiday payrolls (retail, couriers) rose by 202,100 (vs. 283,200 a year ago), but November was a lot stronger (+531,500 vs. 2016’s +438,100). Private-sector payroll growth in 2017 was about the same as in 2016, but that was due largely to a decline in the unemployment rate (to 4.1%, from 4.7% a year ago). The unemployment rate cannot fall forever. A steady unemployment rate would be consistent with monthly growth in nonfarm payrolls of less than 100,000.

Click here to enlarge

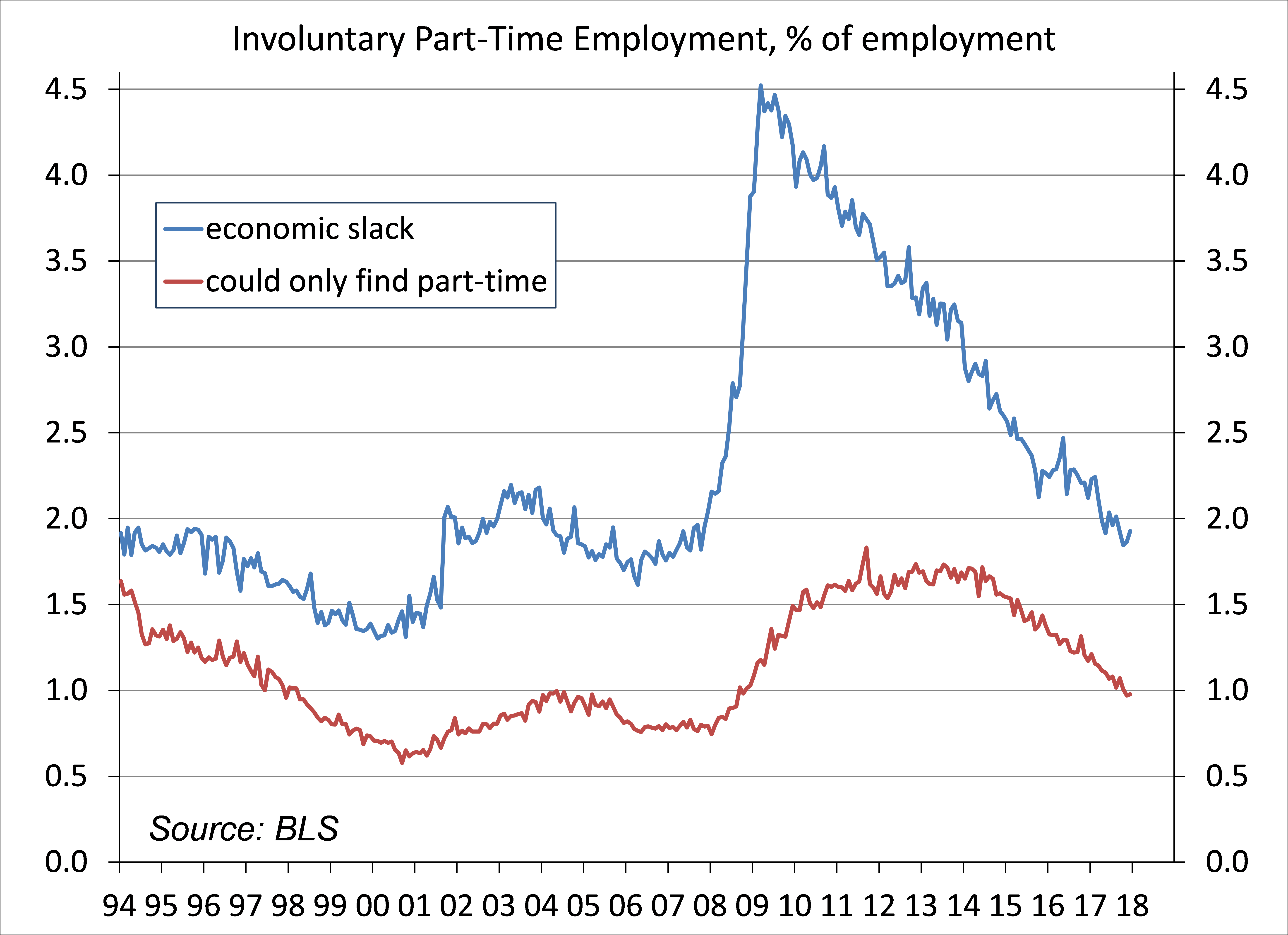

Other signs of labor market slack, such as involuntary part-time employment, have continued to improve, consistent with tighter job market conditions. More firms are reporting difficulties finding qualified workers.

Click here to enlarge

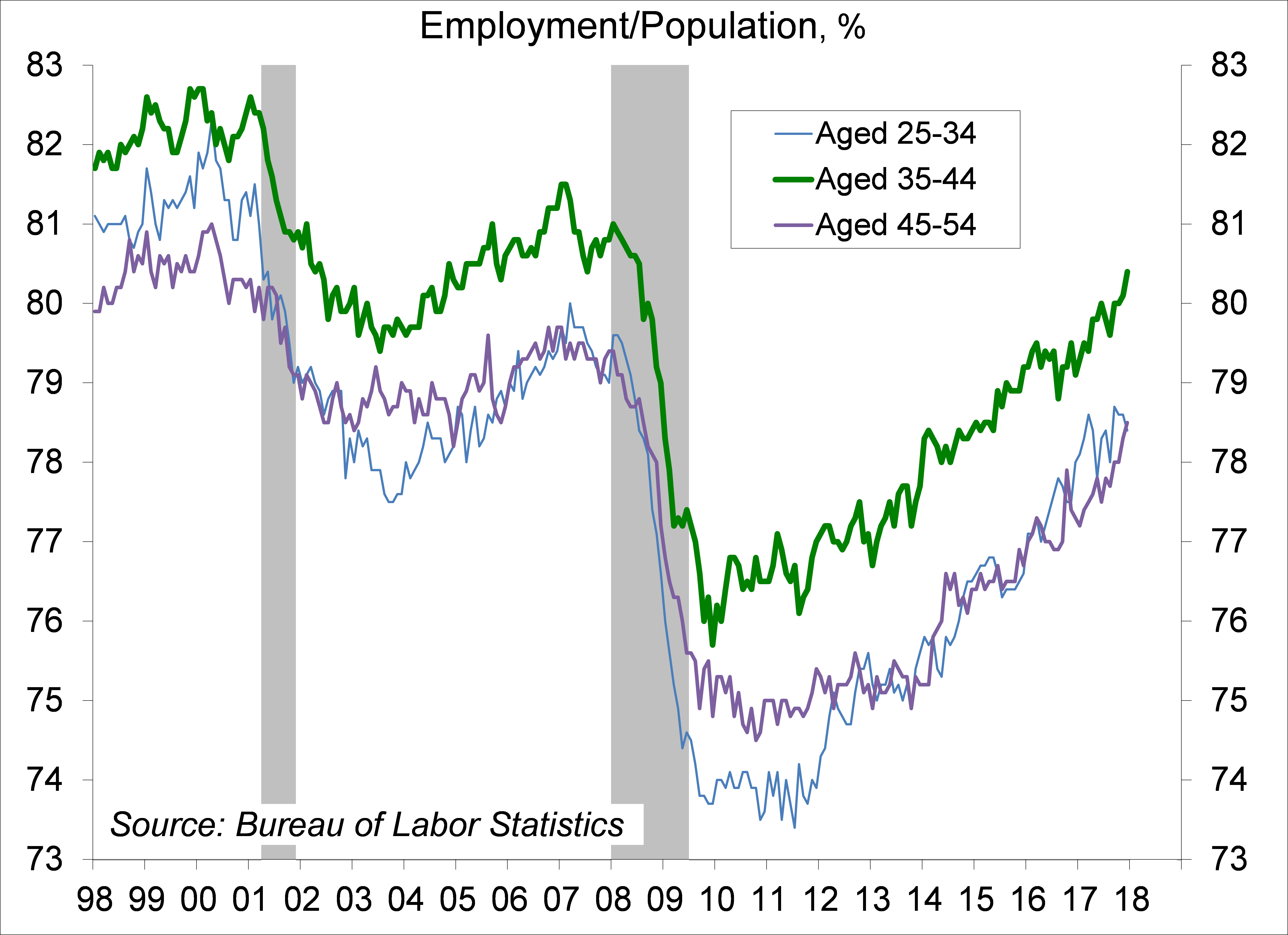

Labor force participation in December was the same as a year ago, but the employment/population ratio for prime-age workers is nearing pre-recession levels.

Click here to enlarge

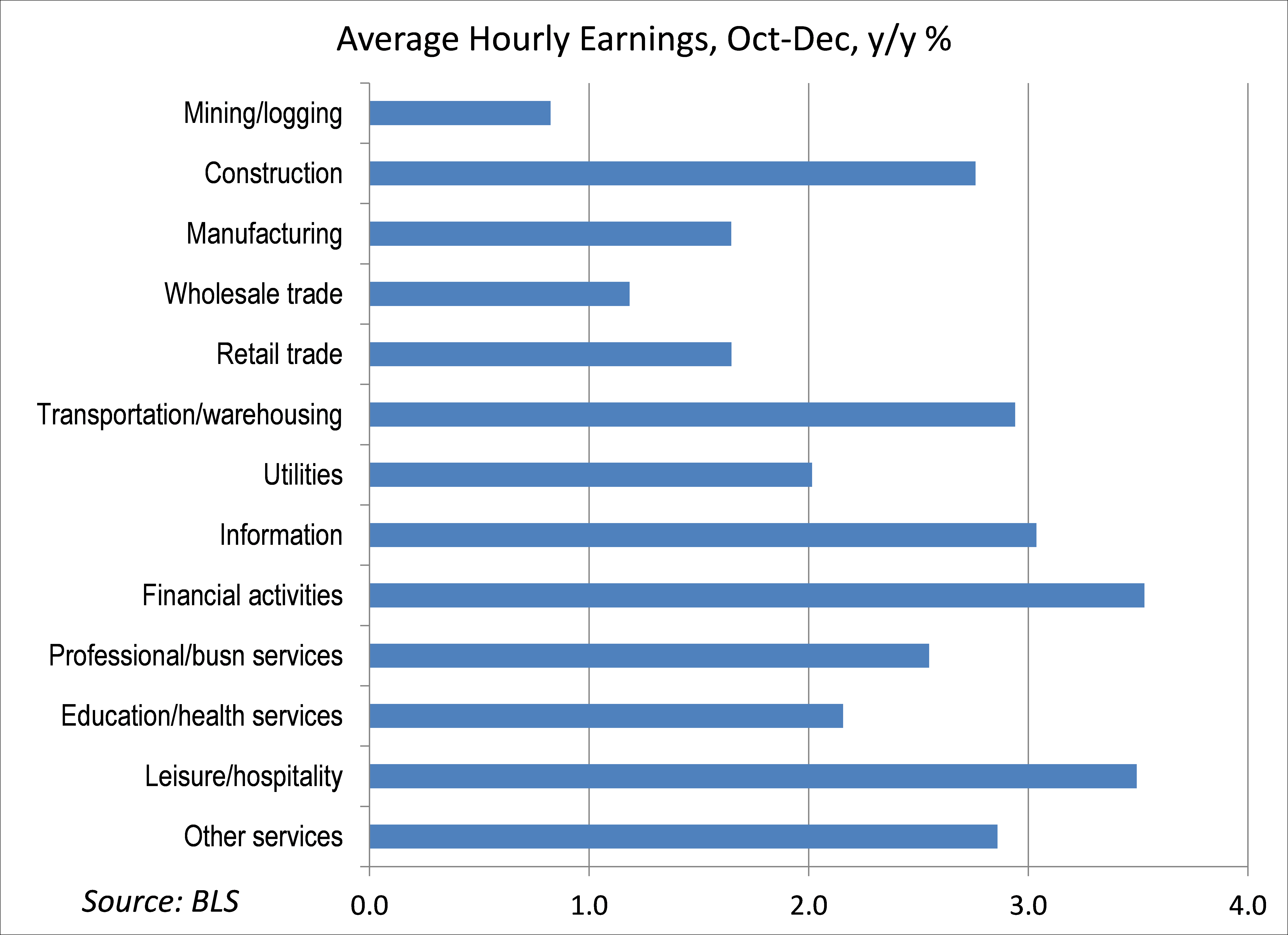

Despite tighter job market conditions, wage pressures have remained moderate. Average hourly earnings for the fourth quarter were up 2.4% y/y. Eighteen states increased their minimum wages this month, which ought to boost average hourly earnings growth in the near term (and typically, increases in the minimum wage echo up the income scale).

Click here to enlarge

The Yellen Fed was more likely to let the job market run. Improvement disproportionally favors those at the low end of the scale (the African American unemployment rate hit a record low in December). Rising wage pressures should lead firms to allocate capital more efficiently, boosting productivity growth. However, personnel changes are expected to leave the Fed a little more hawkish in 2018, inclined to raise rates sooner rather than later. Some lawmakers want to change the Fed’s directive to inflation only, instead of the current dual mandate of steady prices and maximum sustainable employment.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James