“BIS [Bank of International Settlements] research suggests that the ups and downs of the dollar –

and the cycle of dollar liquidity – are what drive the world’s animal spirits and asset prices.

This liquidity spigot is clearly being turned off.

The Fed is not just raising rates, it is also reversing bond purchases (QE)

at a pace rising towards $50bn a month.”

– Ambrose Evans-Pritchard

“I don’t think any of us know what the implications are for a $50 trillion debt build

since the great financial crisis (of 2008). It is impossible to say.

We have never dealt with anything of this magnitude.”

– Danielle DiMartino Booth

“Every investment is simply a claim on a very long-term stream of cash flows

that will be delivered to investors over time. Your current starting conditions matter.”

– Steve Blumenthal

Liquidity spigot. $50 trillion. Starting conditions. Got it!

All buying and selling meets at a point of price. More buyers than sellers, prices move up. More sellers than buyers, prices decline. The dynamics of supply and demand we learned in Econ 101. True for all things. Current conditions? Liquidity, leverage, more buyers than sellers. The bull market advances on.

The market technicals look good. The NYSE cumulative advance-decline line continues to make new highs, confirming the rally (more stocks advancing in price than declining). As for the Dow Jones Industrial Average, the transportation stocks had been lagging the industrial stocks, but last week transportation stocks had a strong breakout to the upside. The economy is solid. Santa must be very busy.

If you look at the NASDAQ, the Dow and the S&P 500 Index, the bullish pattern of making higher highs and higher lows continues. My favorite indictor, the Ned Davis Research CMG U.S. Large Cap Long/Flat Index remains bullish. It is a weight-of-evidence approach to looking at the market measuring momentum and trend of 22 broad industry sectors. So, the good news this holiday season is that the bullish trend remains in place. Let’s feel good, be happy and grateful.

Most portfolios are broadly diversified for a reason. If you’re looking to switch to 100% U.S. equities, think twice and be aware of today’s starting conditions. David Rosenberg says, “Take profits and hedge. We are very late cycle.” I think he’s right. Valuations are near the highest levels in history. Higher than 1929, 1966, 2007 and nearly as high as the great tech bubble in 2000. The cyclical bull market move is the second longest in history. Stocks as a percentage of household assets (adjusted for pension assets) is at 41%. To put this in perspective, it was 37.7% at the top of the 1966 bull market. It was 37.5% at the top of the 2007 bull market. It is currently at the second highest level since 1951 surpassed only by the 47.6% percentage of household assets in 2000. Margin debt is at a record high. Global debt is insanely high. Pensions are a mess. You get the point.

It’s always about the Fed and it will always be about the Fed.

To be sure, it’s about the Fed and the other major global central bankers. So highest on my concern list is that the great central bank liquidity spigot is being turned off.

I’ve shared this quote from Stan Druckenmiller with you before and feel it’s worth sharing again, “Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

Stan is one of the greatest speculators of all time. Google him, follow him and listen to everything he has to say. We may most certainly melt higher, but we should remain aware of where we sit in the cycle and always keep risk front of mind. This recently from Stan:

Probably in my mind the poster child for a central bank mistake was actually the U.S. Federal Reserve in 2003 and 2004… we had great conviction that the Federal Reserve was making a mistake with way too loose monetary policy.

The problem with this is when you have zero money for so long, the marginal benefits you get through consumption greatly diminish, but there’s one thing that doesn’t diminish, which is unintended consequences.

So that’s why, if you look at today… I’m experiencing a very strong sense of deja vu… If you look to me at the real root cause of the financial crisis, we’re doubling down. Our monetary policy is so much more reckless and so much more aggressively pushing the people in this room and everybody else out the risk curve that we’re doubling down on the same policy that really put us there and enabled those bad actors to do what they do.

The trouble is we only discover the consequences once it’s too late for the Fed to really do anything about it: “I feel more like it was in ’04 where every bone in my body said this is a bad risk-reward, but I can’t figure out how it’s going to end. I just know it’s going to end badly and, a year-and-a-half later, we figure out it was housing and subprime. I feel the same way now.

We sit late cycle. Stay on your toes.

The following caught my eye this week. From my friend Harry Whitten’s morning Virtu ETF letter:

Sandler O’Neill put out an estimate that online brokers will see a 18% to 20% increase in earnings in 2018 with the new tax plan and rising interest rates. But there is something also driving this, activity is up, it is pretty well known that the average retail investor has missed much of this market, but the online firms are starting to see that shifting, as bitcoin mania and a strong 2017 is pushing people back into the market.

I keep hearing that retail investors have missed the rally and I’m having trouble reconciling that with the data on stocks as a percentage of household equity shared above (second highest level since 1951), but I think there is something to the late stage speculative fever of periods past and the retail fever is ramping back up.

Whitten concluded his post, “I guess I have ask, is it too late?”

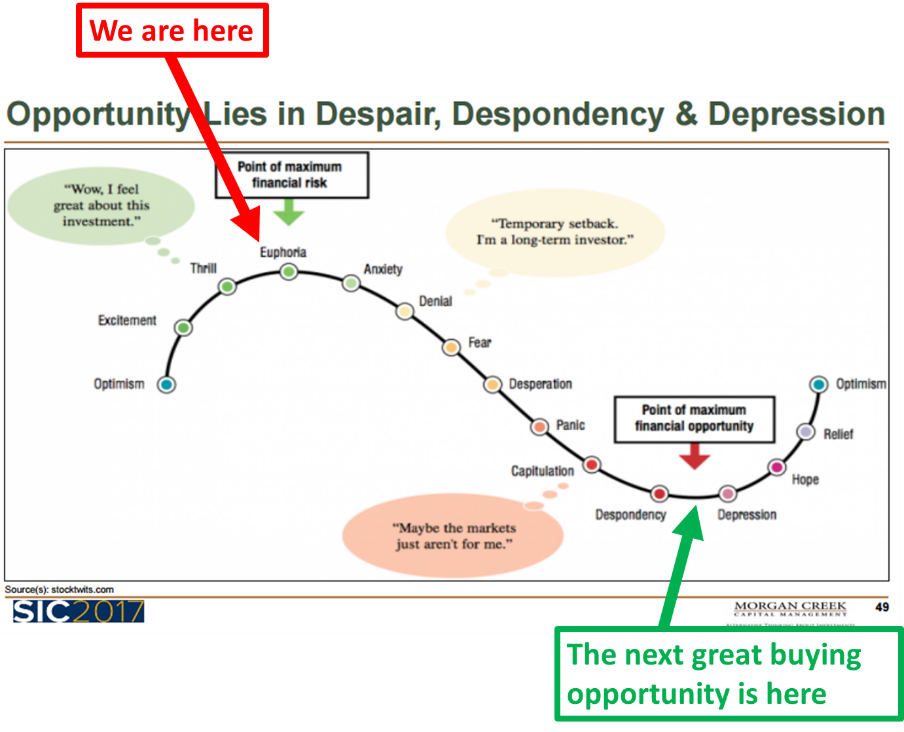

How about this for current starting position? Nearing “Euphoria.”

Source: Morgan Creek Capital Management

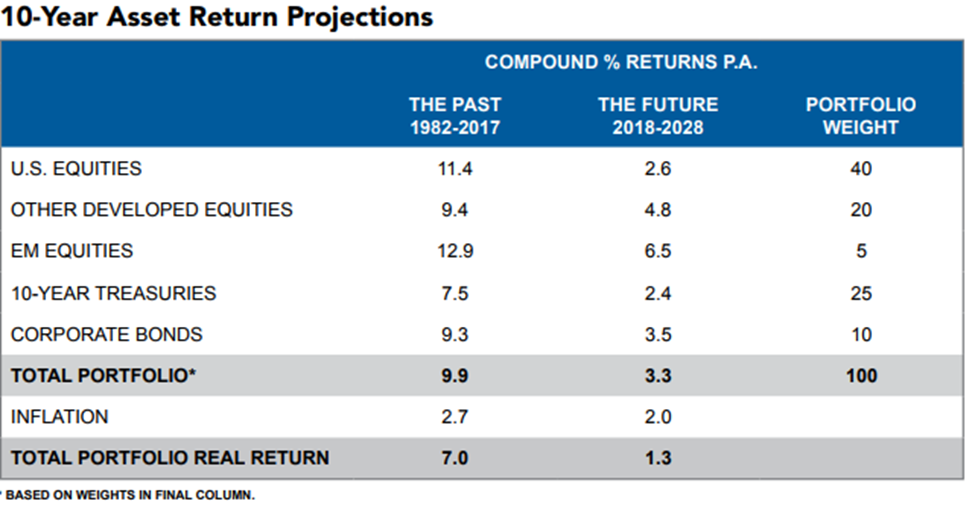

Finally, this too caught my eye this week. Martin Barnes of BCA Research estimates 10-year returns at 1.3% annualized real return – after inflation. I think he is right and consistent with what I’ve been sharing with you.

I’ve followed Martin for years and enjoyed spending time with him last August fishing at David Kotok’s famous Camp Kotok in Maine. It’s a gathering of top economists, investors and several former Fed officials. Martin is one of the most optimistic people and he’s good.

In a 2018 outlook piece published in The Bank Credit Analyst, Martin concludes in fun form with a hypothetical discussion with Mr. X and Ms. X. A discussion you are likely having with your clients.

Mr. X: This seems a good place to end our discussion. We have covered a lot of ground and your views have reinforced my belief that it would make good sense to start lowering the risk in our portfolio. I know that such a policy could leave money on the table as there is a reasonable chance that equity prices may rise further. But that is a risk I am prepared to take.

Ms. X: I foresee some interesting discussions with my father when we get back to our office. At the risk of sounding reckless, I remain inclined to stay overweight equities for a while longer. I am sympathetic to the view that the era of hyper-easy money is ending and at some point that may cause a problem for risk assets. However, timing is important because, in my experience, the final stages of a bull market can deliver strong gains.

BCA: Good luck with those discussions! We have similar debates within BCA between those who want to maximize short-run returns and those who take a longer-term view. Historically, BCA has had a conservative bias toward investment strategy and the bulk of evidence suggests that this is one of these times when long-run investors should focus on preservation of capital rather than stretching for gains. Our thinking also is influenced by our view that long-run returns will be very poor from current market levels. Our estimates indicate that a balanced portfolio will deliver average returns of only 3.3% a year over the coming decade, or 1.3% after inflation.

That is down from the 4% and 1.9% nominal and real annual returns that we estimated a year ago, reflecting the current more adverse starting point for valuations. There is a negligible equity risk premium on offer, implying that stock prices have to fall at some point to establish higher prospective returns.

In terms of the outlook for the coming year, a lot will depend on the pace of economic growth. We are assuming that growth is strong enough to encourage central banks to keep moving away from hyper-easy policies, setting up for a collision with markets. If growth slows enough that recession fears spike, then that also would be bad for risk assets. Sustaining the bull market requires a goldilocks growth outcome of not too hot and not too cold. That is possible, but we would not make it our base case scenario.

Here’s a chart showing how he came to 1.3% for a balanced portfolio:

Source: BCA Research

Further to Stan’s point on the Fed, Danielle DiMartino Booth, former Fed insider and author of the book Fed Up says, “2017 is the record for quantitative easing (money printing) globally. Central banks have never, not even in the darkest days of the financial crisis, injected as much money as they have into the markets.” (Source)

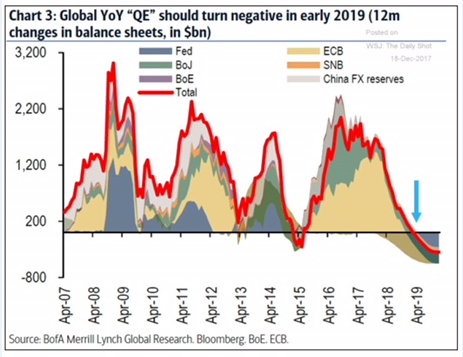

Bank of America Merrill Lynch Global Research says quantitative easing should turn negative in early 2019. Their logic makes sense to me. Is that the tipping point? My best guess is the tipping point comes sooner – perhaps mid-2018 into early 2019.

This takes us back to Stan Druckenmiller. When you have some downtime this weekend, watch the 30-minute CNBC video interview of Druckenmiller (link below). It’s awesome. He talks Fed, bitcoin, stock ideas and forward outlook. He is one of the greatest traders among us. You’ll be surprised, as was I, that his returns this year are in the single digits.

Grab that coffee and jump in. There are no material changes in Trade Signals. Do spend some time and watch the interview with Stan.

A quick plug: we’re co-hosting a complimentary webinar with Ned Davis Research called “How to Invest in a Runaway Stock Market” on Wednesday, January 3 at 2:00 pm (ET). During this webinar, you will learn:

- How to identify key turning points in bull and bear markets.

- How to avoid emotional decision-making.

- How CMG and NDR use a rules-based strategy designed to participate in bull markets and avoid bear markets.

Click HERE to register.

Most importantly, enjoy the time with the people most important to you in your life. Here is a wish from my family to yours: Merry Christmas, Happy Chanukah and endless joy in your life.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- CNBC Interview of Stan Druckenmiller

- Trade Signals — Wishing You a Merry Christmas, Happy Chanukah and a Healthy and Prosperous New Year

- Personal Note – Family!

Stan Druckenmiller on CNBC – Central Banks are the Financial World’s Darth Vader

Some wisdom from the Sage. A short two-minute video:

If you want to go deeper, here’s the full 30-minute interview. He talks about bitcoin, his single-digit performance in 2017 and his outlook for 2018. I believe it is well worth your time.

Trade Signals — Wishing You a Merry Christmas, Happy Chanukah and a Healthy, Prosperous New Year

S&P 500 Index — 2,682 (12-20-2017)

Notable this week:

Broad market indicators — The bullish trend continues intact for equities. Despite the recent move higher in interest rates, our models remain bullish on fixed income. HY remains in a buy signal. The weight of trend evidence remains moderately bullish. The “trend is your friend.” But as the great Art Cashin says, “Stay alert and very, very nimble.” Not lost on us is the extremely high levels of equity valuations and ultra-low interest rates.

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note — Family!

Tyler, Steve, Kyle and Matt (left to right). Yesterday at Snowbird with 7 inches of fresh powder.

I love this time of year. Family! Grandma Pat is coming for Christmas and so is my sister, Amy, and her family, along with my brother’s daughter Ashley. I hope you are able to be with the most important people in your life this holiday season.

Boston is up next. A quick in and out next Wednesday to visit the teams at 3Edge and Shepherd Kaplan along with good friend, Ed Ryu. A conference in Vail follows on January 7-10. For a skier, that’s a fun conference to attend. The ETF.com Conference in Hollywood, Florida is in late January. Several thousand of the most important players in the ETF business attend. A lot to learn. One last winter conference in Utah in February and, yes, there will be more skiing involved. This business really is fun. And the Mauldin Strategic Investment Conference is in San Diego on March 6-9. The structure of John’s annual conference is frankly my favorite. I’d love to see him add Stan Druckenmiller to his already outstanding lineup of speakers. No small wish.

Speaking of wishes, I hope you get yours this holiday. With six kids in the house, it is really the giving that lifts me most. To which, I am most grateful for Susan. She really does all of the heavy lifting. Gift wrapping awaits… with a fine glass of wine in hand.

Wishing you peace, happiness and the very best life can bring!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Wishing you peace, optimism and the very best!

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group