The appointment of Jerome “Jay” Powell as Fed chair should result in a smooth transition for monetary policy into early 2017. However, other personnel changes mean greater policy uncertainty as one looks beyond the middle of next year. This comes at a time when the risks of a policy error are increasing.

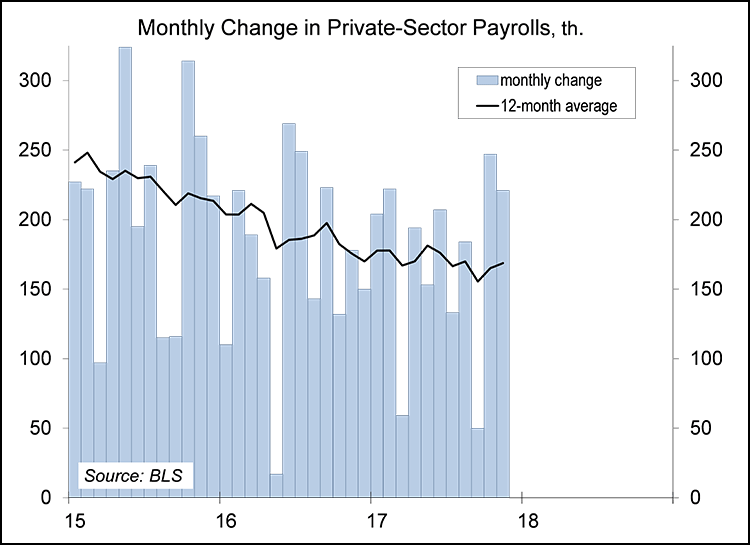

Nonfarm payrolls rose by 228,000 in the initial estimate for November (median forecast: +200,000). Unadjusted payrolls rose by 532,000 (vs. 424,000 a year ago). Unadjusted “holiday” payrolls (retail + couriers) rose by 521,600 (vs. 438,100 a year ago) accounting for much of the strength in the adjusted number. Seasonally adjusted, private-sector payrolls averaged a 173,000 gain over the last three months, vs. +170,000 over the first eight months of 2017, the same pace as in 2016. These figures are subject to revision (and the Bureau of Labor Statistics has indicated that the March 2017 level of payrolls is expected to be revised about 95,000) higher, but the longer-term trend appears to be lower, as one would expect if the labor market is tightening. Still, the payroll data for 2017 suggest that there was more slack in the labor market than was commonly believed at the start of the year. Remember, the growth in the working-age population is consistent with monthly growth in payrolls of a little less than 100,000. Eventually, a tight labor market will restrain the pace of job growth

Click here to enlarge

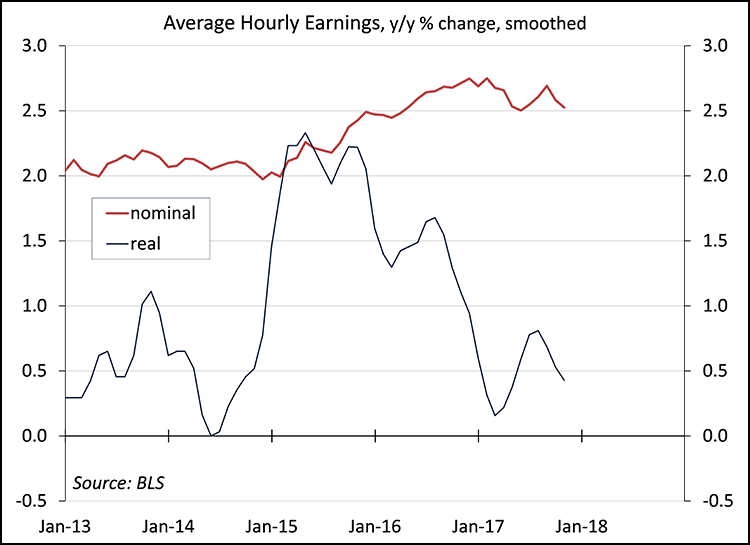

Average hourly earnings rose 0.2% in the initial estimate for November, as expected, but figures for September and October were revised a bit lower, leaving the year-over-year pace at 2.5% – not terrible, but not particularly strong either. Wage growth is thought to be restrained by a shift in bargaining power in recent decades (lower union membership, a greater concentration of large firms), but demographics could also be at play (older, higher-paid employees exit the labor force, while younger, lower-paid workers enter). Increases in minimum wages are expected to add to overall wage growth in early 2018.

Click here to enlarge

While nominal (current dollar) wage growth has been moderate in recent months, real (constant dollar) wage growth has been relatively lackluster. Inflation may be low, but it’s not trivial. Adjusted for inflation, aggregate wages and salaries were reported to have risen 2.1% over the 12 months ending in October. This is the main fuel for consumer spending growth, and consumer spending accounts for nearly 70% of GDP.

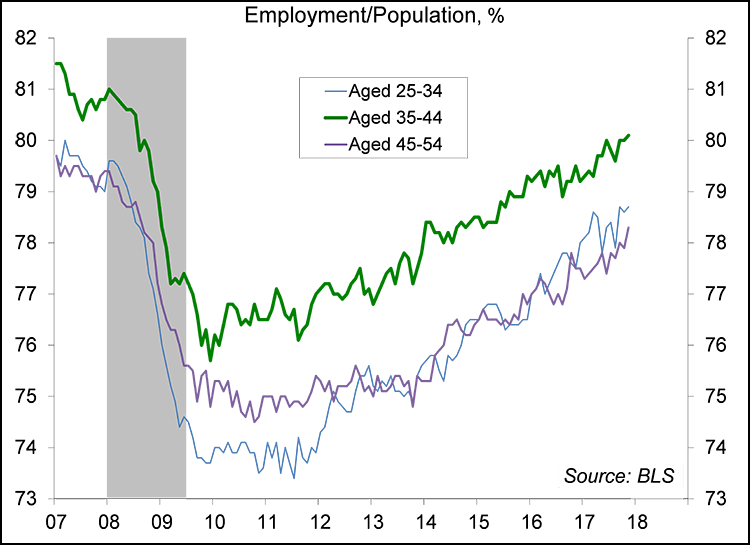

At 4.1%, the unemployment rate is low by historical standards. The employment/population ratio (the “employment rate”) is below pre-recession levels, but is trending higher.

Click here to enlarge

With slack remaining in the job market and wage growth relatively lackluster, why has the Fed been raising short-term interest rates? Rather than hitting the brakes, the Fed has been taking the foot of the gas pedal, moving monetary policy to a more neutral position. From here, raising rates too slowly risks overshooting, which would require even sharper rate increases later. Raising too quickly risks weakening the pace of the expansion and pushing inflation lower. The Fed has plenty of time, but will incoming Fed officials agree with that assessment?

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James