To explain the intuition and use for five style factors, we tell the story with the five Ws (and one H): who, what, when, where, why and how.

I was a professor for 15 years, and ended my time in academia as Chair of the Finance and Economics Division at Columbia Business School. During my time as an academic, I wrote close to a hundred scientific papers — with technical details that most people would find impenetrable. At the same time, I taught talented MBA students destined for general management, and worked with many non-investment professionals in different types of financial institutions.

These are quite different types of communications and audiences. What is common to the best communication — from technical research to regaling a tale to a friend over a beer — is that we tell a story. And that story must involve answering the five Ws (and one H). To fully understand and develop intuition for the true, underlying explanations, we all need stories.

What factors are and why they have worked

What is a factor? Factors are broad and persistent drivers of return that research has proven to be historically enduring. The most important part of this investment philosophy is why factors have worked and the intuition that drives them. I wrote earlier about the checklist for robust factors, which includes three economic rationales for why they have worked historically:

-

Rewarded risk - Some factors have earned higher long-term returns as a reward for taking on more risk.

-

Structural impediment - Market rules or other constraints can place restrictions on certain investors, such as pension funds. Those off-limits investments can become opportunities for others.

-

Investors’ biases - Over time, opportunities are generated by investors not behaving perfectly rationally. Taking a contrarian view can be beneficial.

When they might shine

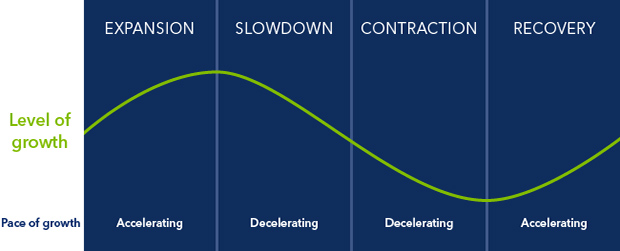

Let’s pair this economic intuition with when five style factors tend to be rewarded during the economic cycle — expansion, slowdown, contraction and recovery.

Stages of the economic cycle

Value. The intuition behind the value factor is that securities priced at a discount to their fundamental value have historically outperformed those priced at a premium. It’s worked due to rewarded risk (traditional manufacturers are less flexible than firms that can pivot) and investor bias (staid value stocks are overlooked by investors dazzled by growth). The value factor may perform best when the economy is in recovery mode and growth is accelerating from a trough.

Momentum. The intuition of momentum is simple: prices moving upward tend to continue moving in that direction. It’s worked due to rewarded risk (when price trends reverse, the crash may be big) and investor bias (investor behavior tends to exacerbate existing trends). Momentum may perform best during expansion mode, when growth is accelerating and trends persist.

Quality. The intuition is that financially healthy companies tend to outperform less-efficient peers. Quality has worked due to investor bias: superficial investors are attracted by high headline earnings, while diligent contrarians investigate the underling composition. Quality may perform best during slowdown and contractionphases when growth is decelerating and investors seek safety.

Size. The intuition is that smaller, nimbler companies tend to outperform larger ones. The size factor has worked due to rewarded risk because smaller companies are less liquid and more sensitive to market movements. Similar to the value factor, the size factor may perform best during a recovery.

Minimum volatility. Unlike the previous four style factors, which are primarily used by investors seeking to enhance portfolio returns, minimum volatility seeks to reduce portfolio risk. The intuition is that securities with prices that move around less can deliver returns similar to the market with less risk. The factor has worked due to structural impediment, because some pensions and endowments have restrictions against leverage, driving them toward high-risk stocks to meet high return targets. There is also investor bias when low-risk stocks are overlooked by investors flocking to the next big idea. Minimum volatility, much like quality, may perform best during slowdown and contraction phases when growth is decelerating.

How factors are used

How do investors use factors in portfolios? Three ways:

-

To seek higher returns. Value, momentum, quality and size factors can be used individually or together to seek returns above the broad market.

-

To add diversification. Portfolios allocated across traditional asset classes may develop unintended factor concentrations. Allocating to style and macro factors could diversify across return sources to restore balance.

-

To pursue reduced risk. The minimum volatility factor can be used to help reduce risk in a portfolio.

That just leaves where and who

So, where can style factors fit in a portfolio? Multiple places:

- As an upgrade to style-box holdings, swapping in momentum for large growth and quality for large blend, for example.

- In allocations to fixed income and alternatives. For the latter, enhanced versions of factor strategies invest using both long and short positions, and harvest value, momentum and other factors in several asset classes.

- To express short-term views. I wrote earlier about factor tilting as an example.

And finally, who should consider factors?

Everyone! Factors are a time-tested investment principle that’s been democratized by newly available data and technology. What’s changed is that these economically intuitive broad and persistent sources of returns used to be available only to the most sophisticated investors, and now they are accessible to everyone.

One of my least favorite tasks as a professor was assigning grades. And now you can grade me! I did cover what factors are, why they have worked, how they’re used, when they might be rewarded, where to use them in a portfolio and who can benefit from factors. Maybe I get bonus marks for mixing up the original order!

© BlackRock

© BlackRock

Read more commentaries by BlackRock