Rick and Jacob examine why 2017 provides a seemingly unlikely source of evidence for the effectiveness of an active approach to fixed income.

At first blush, late 2017 may seem to be a curious time to be writing about the advantages of active management in fixed income. For much of the past year, markets have felt incredibly quiet and there has been little price volatility. In fact, market participants could almost hear the proverbial pin drop during this period. Looking at realized volatility, there have been few times as quiet as what we’ve seen this year. Of course, this isn’t to say that there haven’t been periods of uncertainty, risk and market movement over the past several months; but stepping back, this has been a very docile period. To highlight how low volatility has been this year, we’ve frequently seen both realized rate and equity volatility resting in the bottom decile relative to a long history (see first graph).

Markets Have Been Quiet

One might be tempted to think that this kind of low volatility environment isn’t favorable for active fixed income strategies of the kind that we outlined in March 2017; if volatility creates opportunity, one could ask whether there has even been enough of an opportunity set available. In short, we think there has been. In our view, a lot has been going on under the hood in markets over the past several months, and we think there have been plentiful prospects for active strategies to function well and generate returns. This point is crucial—if these strategies can find the raw material needed to generate returns above that of the market in environments that are as quiet as this one, we think it’s possible to create durable and consistent active returns across varying market regimes.

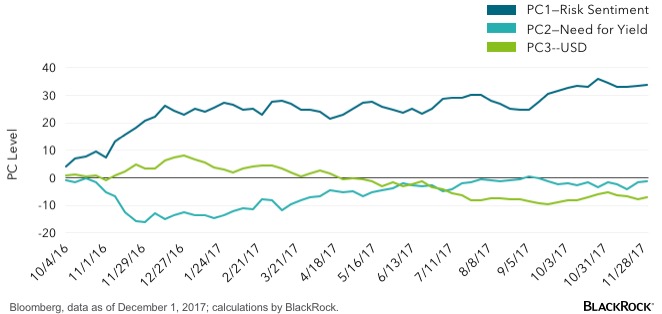

However, we can see clearly that there has been opportunity in this environment when we uncover the thematic drivers of markets utilizing Principle Component Analysis (PCA, see second graph). It’s easy to think that markets have been on a steady grind higher during this period of low volatility, but when we look more closely, we find that there have been distinct, dynamic and evolving trends in place. Indeed, these trends could serve as a fertile opportunity set, particularly for dynamic active strategies, which generate return from evolving macro trends.

Following the November 2016 election in the U.S., we saw a surge in risk sentiment, where assets with perceived credit risk gained and assets thought to be risk-free sold off, as investors rotated their portfolios (PC1). However, since then, this driver of markets has more or less flat-lined, until recently. Yet, risk markets have continued to see strong performance. We find that a different trend (PC2), what we have termed “the need for yield,” where investors’ thirst for income-generating assets drives all asset prices higher, has been driving markets. Risk sentiment’s ascent has slowed and this latter theme has been pushing risk assets higher in price. Meanwhile, we’ve seen numerous gyrations of the U.S.dollar (USD) exchange rate driver of markets (PC3), which can act in complex ways on the economy and on cash flows. PC3 in our graph roughly tracks broad USD moves. In all, despite near-record low realized volatility, there have been plenty of shifts and trends that could serve as opportunities for active macro strategies.

The Evolving Drivers of Markets Over the Past Year

We want to take a closer look into what we call the “need for yield” principal component. This is important not solely because the fluctuations of this component have shown an opportunity available to active investors this year, but because it may highlight how structural themes drive markets and generate investible trends for those using active strategies. We’ve held a longstanding view that changing demographic trends and an aging population in the developed world mean that there will be a demand for income that is structurally higher than what we’ve seen in the past. Due to this massive structural thirst for yield, we imagine possible impacts across a number of income-generating assets within the fixed income universe.

While this demand for yield trend may explain some of why this principal component moved this year and may even highlight some recent alpha opportunities, the broader point here is more profound. There are structural forces at play within the market that generate investable crosscurrents for investors using active strategies, and that is the case for all time horizons an investor might consider. In fact, even in this quiet and seemingly boring environment, there have been ample opportunities to generate alpha looking deep into different corners of the markets. Thus, while it may appear paradoxical, 2017 was actually the acid test for active fixed income management.

Rick Rieder, Managing Director, is BlackRock’s Chief Investment Officer of Global Fixed Income and is a regular contributor to The Blog. Jacob Caplain is a member of the Fixed Income Portfolio Management team focused on portfolio construction, analytics and emerging markets fundamental research, and he contributed to this post.

© BlackRock

© BlackRock

Read more commentaries by BlackRock