Our long-time readers are familiar with the work of Professor Baruch Lev of the NYU Stern School of Business, whose research forms the basis for the Knowledge Leaders investment strategy. In his decades-long study of financial records, Lev first discovered a link between a firm’s knowledge capital and its subsequent stock performance, ultimately identifying a market inefficiency that leads highly innovative companies to deliver excess returns. We call this market anomaly the Knowledge Effect.

In a new article in Financial Analysts Journal, Lev and co-author Feng Gu continue to advance the findings on intangibles. The article, “Time to Change Your Investment Model,” identifies that earnings prediction has lost “much of its relevance in recent years.” As a form of predicting corporate results, “earnings no longer reliably reflect changes in corporate value and are thus an inadequate driver of investment analysis.”

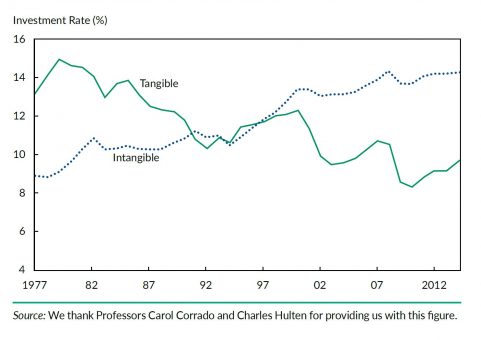

The basis for this shift, the authors explain, occurred after the emergence of the semiconductor. “Starting in the early 1980s, investment in traditional, tangible assets (structures, factories, machinery, inventory) – considered assets by accountants and reported accordingly on the balance sheet – dropped precipitously from 15% of gross added value in 1977 to 9% in 2014, a 40% drop. In contrast, the investment rate in intangible capital (R&D, patents, information systems, brands, media content, business processes) – mostly expensed in corporate income statements – increased continuously from 9% to 14% of added value, a 56% increase. This radical business model transformation came to be known as the knowledge – or information revolution, an irreversible trend in developed economies.”