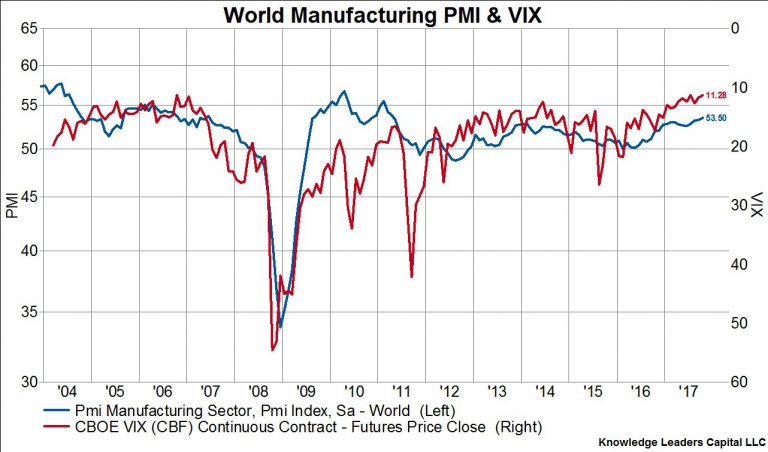

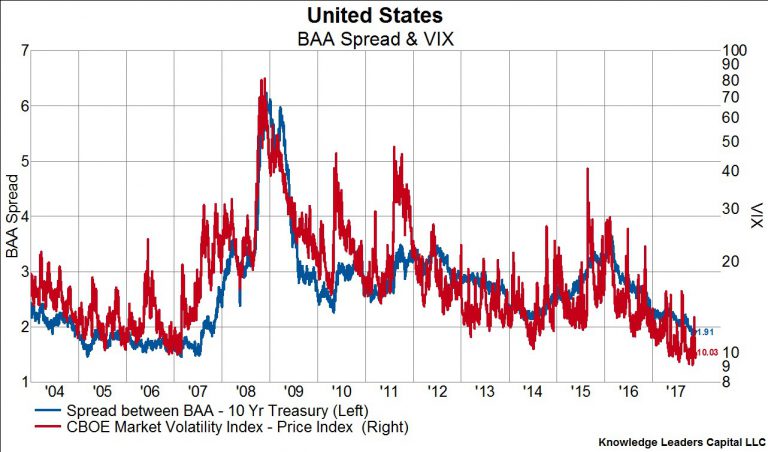

The drop in the VIX to ultra-low levels in 2017 has been a point of consternation for market participants and largely misunderstood. Some market participants view the low level of the VIX as an indication of excessively positive sentiment among investors and thus a contrary indicator for the general direction of stock prices. But, the level of the VIX has to be framed in the context of other variables that affect it, including the prospects for global growth and liquidity conditions. For example, since the beginning of 2016 the Markit World Manufacturing PMI has moved up from 50 to a reading of 53.5, which is the highest level of this indicator going back to the early acceleration phase of the recovery. As the first chart below shows, the VIX has a strong negative correlation with this metric for global growth. Additionally, the VIX has a strong negative correlation with measures of liquidity, such as the spread between BAA corporate bonds and that of the 10-year US Treasury bond, as shown in the second chart below. Corporate spreads have been falling since early 2016 and are now at a level consistent with that of the 2005-2007 period. Global growth hitting on all cylinders for the first time in seven years and liquidity conditions improving – thanks in no small part to central banks maintaining easy monetary policy – go a long way in explaining the historically low level of the VIX. Unless or until those dynamics change, we should expect more of the same from the VIX in 2018.