Nothing causes more anger, confusion, and bewilderment than the trade deficit – that is, except for the federal budget deficit. In past decades, these were often called “the twin deficits.” They are not identical, but they are related.

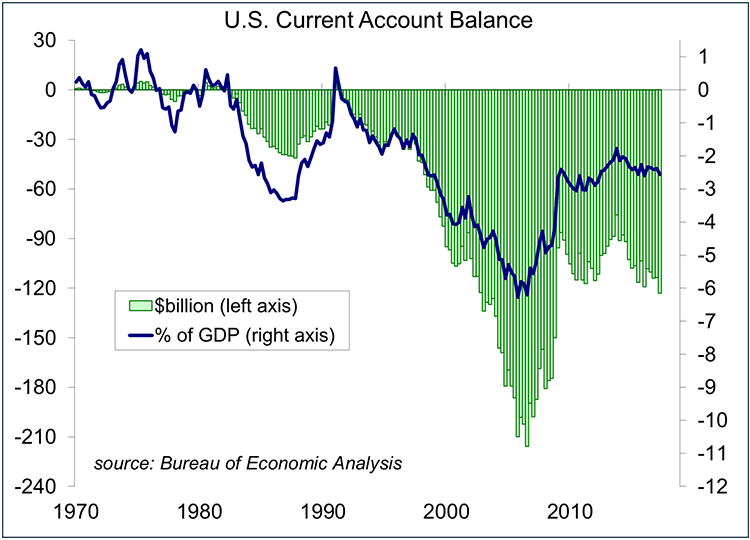

The current account balance is the trade balance (we currently run a surplus in trade services, which is more than offset by a deficit in trade goods), plus balances on primary income and secondary income – but it’s mostly the balance in goods and services. Primary income includes investment income and compensation of employees. Secondary income includes transfers (government and private), “such as U.S. government grants and pensions, fines and penalties, withholding taxes, personal transfers (remittances), insurance-related transfers, and other current transfers.” The numbers are large (the current account deficit totaled $123 billion in 2Q17), so you need to scale that relative to GDP to compare it over long periods of time. The current account deficit reached 6.3% of GDP in 4Q05, a worrisome level, but has moderated in recent years, down to 2.6% of GDP in 2Q17.

President Trump has said that the trade deficit reflects poor negotiations in international trade agreements. Other countries “have been taking advantage of us.” Economists do believe that. The trade deficit reflects the strength of the U.S. economy (if we consume more domestic goods and services, we can expect to consume more imported goods and services) and, importantly, the ability to borrow cheaply from the rest of the world. If the U.S. runs a trade deficit, it must import capital to finance that. Alternatively, if the U.S. does not save enough relative to its consumption, it has to borrow from the rest of the world – and that means that it has to run a trade deficit.

There is a simple way to reduce the trade deficit: have a recession. The trade deficit fell sharply in the 90-91 recession and in the 08-09 recession, but not by much in the 2011 recession (which was relatively mild by historical standards).

Over the years, there has been much hand-wringing about trade deficits with individual countries (Japan in the 1980s, China more recently). However, this concern is misplaced. As Nobel Laureate Robert Solow once noted, “I’ve had a long-standing trade deficit with my barber.” It’s the total trade picture that matters, not the deficit with any one country. In this way, economists favor multi-lateral trade agreements (such as the TPP and NAFTA), rather than bilateral agreements.

The current account deficit is the mirror image of the capital account surplus. As noted, if the U.S. does not save enough, it has to borrow from the rest of the world. The federal budget deficit is part of national savings. All else equal, a larger budget deficit would imply a larger trade deficit.

In the late 1990s to the mid-2000s, the pace of economic growth was unsustainable. How do we know? The trade deficit was rising and the unemployment rate was falling – two trends that clearly could not go on forever. And as Herbert Stein noted, if a trend cannot go on forever, it won’t.

The Great Recession was widely characterized as the collapse of a housing bubble, but it was also a massive deleveraging (in the financial sector as well as housing). The increase in government debt reflected the magnitude of the recession (lower revenues and higher recession-related spending) and the increase in borrowing roughly offset the deleveraging going on in the private sector (leaving national borrowing about flat). In FY09, the budget deficit totaled $1.4 trillion or 10% of GDP. As the economy recovered, the budget deficit fell to 2.4% of GDP in FY15. However, in FY17 (which ended in September), the deficit rose to 3.4% of GDP. It is set to increase in the years ahead as the baby-boom generation retires, and Social Security and Medicare expenditures rise. That’s before any tax cuts.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James