“If you are adding to your long-term holdings of stocks and other risk assets at current market valuations,

you are likely to be betting — knowingly or not — on a combination of three drivers of future returns;

or you are planning to sell your holdings to someone who is or will be making that bet.

Understanding the importance of these three scenarios, both in relative and absolute terms,

indicates not only the probability of being right over time,

but also the tilts you should be applying to your current “risk-on” portfolio positioning.”

- Mohamed A. El-Erian

“The Three Scenarios that Should Guide Investors,” Bloomberg View

My daughter, Brianna, and I were recently listening to a Charlie Rose interview on Bloomberg Radio. I love the way he asks direct questions. The interview featured Jeremiah Tower, a little-known chef who pioneered a restaurant revolution in the 1970s that gave rise to the culinary style known as “California Cuisine.” I have an appreciation for good food, but Brianna is always interested in the best new restaurants so we listened in.

Rose asked Tower a question about his short-lived job at Tavern on the Green. Tower explained why he took the job at the restaurant. His answer grabbed me, “I have a fatal attraction for the slim chance. It was an adventure, a dangerous adventure, and I’m very often stupid enough to step up and take a swing at it.” “Brie,” I said, “write that quote down.” A fatal attraction for the slim chance… And there I was back thinking about the Fed, tax reform and the markets.

In a recent Bloomberg View column, Mohamed A. El-Erian advised,

If you are adding to your long-term holdings of stocks and other risk assets at current market valuations, you are likely to be betting — knowingly or not — on a combination of three drivers of future returns; or you are planning to sell your holdings to someone who is or will be making that bet.

Understanding the importance of these three scenarios, both in relative and absolute terms, indicates not only the probability of being right over time, but also the tilts you should be applying to your current ‘risk-on’ portfolio positioning.

As you may know from following Trade Signals, I’ve been on the risk-on side for some time and that remains the case for now.

The three drivers of future returns? They are:

- Economic and financial healing;

- Long-awaited policy breakthroughs; and

- Bigger liquidly waves from central bankers.

El-Erian says, “The U.S. is gaining momentum in driver number one and so is much of the world and this process would be turbocharged were Congress able to work with the administration to pass pro-growth measures, including tax reform and infrastructure.”

Congress working with the Administration? That game is ongoing and you and I are painfully watching it play out. I’m going to touch on what that looks like right now and, frankly, I find myself disappointed and upset. More on that below.

El-Erian continues saying we need, “[F]urther improvements in the actual and future functioning of the labor market – that in the context of educational reforms and greater skill acquisition. And all accompanied by better international policy coordination, including in order to reduce currency and trade tensions.” (Emphasis mine.)

Economic and financial healing? Done. Policy breakthroughs? I’m not so sure. Bigger liquidity waves from central bankers? Central bankers are attempting to reverse course.

In summary, we need policy breakthroughs, such as tax reform, infrastructure and de-regulation, better international policy coordination, including, in order, to reduce currency and trade tensions, and a dependence on global central bank liquidity — as we currently sit at record high valuations and record low volatility. Well, that’s the bet. “A fatal attraction for the slim chance?”

If Mohamed A. El-Erian’s name is new to you, which I doubt, he is the chief economic adviser at Allianz, the parent company of Pacific Investment Management Company or “Pimco,” where he served as CEO and co-CIO. He was chairman of President Obama’s Global Development Council, CEO and president of Harvard Management Company, managing director at Salomon Smith Barney and deputy director of the IMF. His books include New York Times best-seller, The Only Game in Town: Central Banks, Instability and Avoiding the Next Collapse.

Avoiding the next collapse requires domestic and global political and central bank coordination. It’s certainly a delicate dance. I just can’t see the folks in Washington as anything but dysfunctional. But here we sit “risk-on.”

The three drivers of future returns? If El-Erian is right, we have to wonder are we investors “stupid enough to step up and take a swing?” My two cents is to embrace a risk management mindset. “Next Collapse?” I believe it will be epic both in terms of magnitude and opportunity. Borrowing from the great Art Cashin, “Stay alert, stay wary and very, very nimble.”

Tax reform looks to me to be anything but reform. Frankly, I find myself a little bit more than just upset. A “Come on… this is all you guys got?”

Grab a coffee and find your favorite chair. In the peak of my anger yesterday I called my friend, John Mauldin, to talk about tax reform. I can say he did calm me down. You’ll find my notes from that call and you’ll also find a link to an outstanding interview where former Goldman Sachs co-chairman and former Secretary of the Treasury, Robert Rubin, interviews Yale Endowment’s David Swenson.

Really, you do want to watch the interview. Add Swenson to the list of famed investors predicting low single-digit forward returns. He shares some sage advice on portfolio management and diversification.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- Mauldin and More on Tax Reform

- A Conversation with David Swenson

- Trade Signals – High Yield Warning Signal?

- Personal Note — He Ain’t Heavy, He’s My Brother

Mauldin and More on Tax Reform

I called John and told him these guys in DC really have me pissed off. He began with what at this point in time remains true, “We don’t yet know the finality of what comes out.”

John continued (my notes in bullet point format):

- The problem is they have this idea that they will help businesses, but they are only going to help a few manufacturing businesses but; if you are a services business, this bill doesn’t do anything for you. Doesn’t move the needle anywhere at all.

- Basically, our taxes may go up.

- That’s not what I think of as tax reform.

John said he hasn’t yet looked deeply at the Senate’s bill. He said, “I don’t get any of the lower pass-through rates. It does give higher deductions, it gives people at the lower end of the income spectrum lower taxes and noted:

- The bottom 50% of people only pay 3% of the taxes. They’ll get benefits.

- But they don’t create businesses, hire new employees, give raises, and those are the people who are not getting a break and may actually pay more…

- Overall, I don’t see how this moves the economic needle, how it creates jobs.

“C” corporations benefit with a tax rate reduction from 35% to 20%. So the bill gives big corporations a lower tax bill and will bring money in from offshore, but what do those corporations do with that money?

- Buy their own stock

- Increase dividends

- Good for investors, but for the overall economy… not much impact

I asked John his thoughts around small business. In his view, this bill does not benefit small business, especially non-manufacturing businesses. His answer is something he’s shared in his recent letters:

- Small businesses are not creating new jobs…

- We are in a place where we are producing fewer new businesses

- More businesses are failing vs. new businesses being created… that’s not healthy.

John added, “I came back from the inauguration all pumped up. All the things they were going to get done. And now it’s like, they… ugh… the problem is they have a rift right down the middle… the ones that want to cut taxes and the ones who want to balance the budget… they are not going to play nice in the sandbox.

- McConnell, Ryan and Brady are all trying to come up with something that will satisfy a very diverse and divided group of Republicans.

Following are some sources for your further research and indigestion. Click at your own emotional risk. I recommend Tums.

From The New Yorker:

Mark Zandi, the chief economist of Moody’s Analytics, was even more scathing about the Republican plan. According to his economic model, he said, the tax cuts that the G.O.P is proposing would have virtually no impact on G.D.P. growth over the next ten years, but would widen the budget deficit substantially and increase the debt-to-G.D.P. ratio by about six percentage points. Raising the question of why anybody would want to adopt such a plan, he said, “I don’t get it.”

Dambisa Moyo, is an author and a public speaker who sits on the boards of three big companies—Chevron, Barclays, and Barrick Gold—all of which stand to benefit from the Republican proposal to cut the corporate tax rate from thirty-five per cent to twenty per cent. But, far from praising the G.O.P. plan, Moyo pointed out that the last time the corporate rate was reduced, in the nineteen-eighties, corporations used their tax savings to increase dividend payouts to shareholders rather than to invest in plant and capital equipment, or to raise wages.

Mark Cuban was the other person on the panel. Was he any more positive on the tax plan? No. He described the effort to cut corporate taxes as a distraction from the real challenge facing businesses: the ongoing digital revolution. “Competition drives what I do in my businesses a whole lot more than tax rates,” Cuban said. “Amazon is going to affect a whole lot more companies and futures, as will Microsoft and Facebook and Google and other big companies, a lot more than a marginal tax rate.” Cuban also pointed out that if the goal of tax policy is to put more money into the pockets of ordinary Americans—which is what the Republicans and the White House claim—it would be more effective to cut payroll taxes, which everybody pays.

The article concludes, “A year after the election, how can it be staking its future on a tax plan that represents the antithesis of populism?” I think they are kind of right. The party appears to be staking its future on a tax overhaul that represents the antithesis of the populist movement that helped elect Donald Trump.

Here is the Tax Policy Center (TPC) analysis.

Here is the Tax Foundation Analysis – Who Gets a Tax Cut Under the Senate Tax Cuts and Jobs Act?

I got this note from CMG’s PJ Grzywacz, “As an aside, the pass-through reduction, which is targeted towards manufacturing sectors as I understand it, would have a limited impact on jobs per my Vistage group members who are active in the manufacturing associations in Pennsylvania. They cannot find people to do the work and in other cases can’t get them trained properly or fast enough.”

The House plan does absolutely nothing to incent a small business to invest, like mine, unless there is something under capital expenditures for technology. Would we be able to write off software for marketing automation or something like it? Doubt it.

Ultimately, it appears that the House bill is going to benefit the wealthiest and the poorest. It appears to do very little for the middle class. Thus, my great frustration.

Mauldin concluded where he began. “We don’t yet know the finality of what comes out.” He’s hopeful and optimistic, as we should all be. A fatal attraction for the slim chance? Let’s see what we ultimately get.

A Conversation with David Swenson

Click photo for the full interview.

Selected highlights from the interview:

RUBIN: And what we’re going to do is I’m going to ask David a few questions, which he can respond to as a long-term investor, with all faces of an extremely complicated environment. And I’ll do that for about half an hour. And then the second half-hour, we’ll take questions from all the members who are here.

OK, David, let’s start with this: The markets have been up for about eight years, or thereabouts. There are all sorts of risks out there. Richard Haass was quoted in Nick Kristof’s column the other day as saying he thought there was a 50 percent chance we would have some sort of military engagement with North Korea. And we have a whole host of other risks that we can think about.

When you, as a long-term investor at Yale, think about your portfolio, do you take into consideration these—the possibility, at least, and whatever the probabilities you may think are—the possibility of a major downturn, given the circumstance I just cited? Or do you take the view that you’re a long-term investor and if things go down, they’ll come back up, and you don’t take that into consideration?

SWENSEN: You have to think about what’s going on in the tails of the distribution. I think that’s incredibly important. We spend too much time in finance class, in business schools or in colleges, thinking about normal distributions. And we know—we know the distribution isn’t normal. If securities returns were normally distributed, the crash in 1987 wouldn’t have happened. It was a 25-standard-deviation event. That’s an impossibility.

And when you look at defining moments for portfolio management, they came in 1987, they came in 1998 and they came in 2008-2009. If you ignore that, you’re not going to be able to manage your portfolio effectively. But when you started out, you were talking about fundamental risks in this world. And when you compare the fundamental risks that we see all around the globe with the lack of volatility in our securities markets, it’s profoundly troubling, and makes me wonder if we’re not setting ourselves up for an ’87 or a ’98, or a 2008-2009.

RUBIN: But then I think the question, David, is this—and this is what I think myself; I’m very focused on it. I agree with what you just said. But then do you have—does that enter—since you’re not a market timer, but a long-term investor, does that enter into your asset allocation at Yale? Should it enter into my asset allocation? I’m a long-term investor. Or should you just take the view these things are going to happen, they’re pretty much unpredictable in terms of timing and duration and magnitude, and so we accept them and figure that if it goes down, it’ll go back up? Which do you do?

SWENSEN: So we’re absolutely not market timers, but I would talk about market timing as kind of a short-term swing in the portfolio to take advantage of some knowledge that you have or some belief that you have about where markets are headed in the short term. But I think we have to take strategic positions in the portfolio. One of the most important metrics that we look at is the percentage of the portfolio that’s in what we call uncorrelated assets. And that’s a combination of absolute return, cash, and short-term bonds. And those are the assets that would protect the endowment in the—in the event of a market crisis.

Prior to the downturn in 2008, we were probably about 30 percent in uncorrelated assets. By the time 2009-2010 rolled around, we were probably around 15 percent. And the reason for the dramatic decline is these are the sources of liquidity in times of stress. And so today we’ve rebuilt that. It actually works out quite nicely from a cyclical perspective, if you’ve got a rebound afterwards. Instead of being 70 percent in risk assets, you’re 85 percent in risk assets. But over the years subsequent to the crisis, we’ve rebuilt our uncorrelated assets position to an excess of 30 percent. And we’re currently targeting about 32½ percent, which is somewhat above the long-term goal.

RUBIN: And is the uncorrelated, David, something that you think has a beta of close to zero?

SWENSEN: Yes.

RUBIN: OK.

SWENSEN: We worked very hard to engineer absolute return to have as little correlation to market as possible.

Swenson talks about manager selection and portfolio diversification and discusses the coming pension crisis and much more. I hope the above gives you a feel and I encourage you to put on your headphones, grab your sneakers, grab the dog and leash and walk as you listen. Or stay seated and grab a second coffee. You’ll really like David Swenson. As Rubin told Swenson, he’s a true American icon. Indeed.

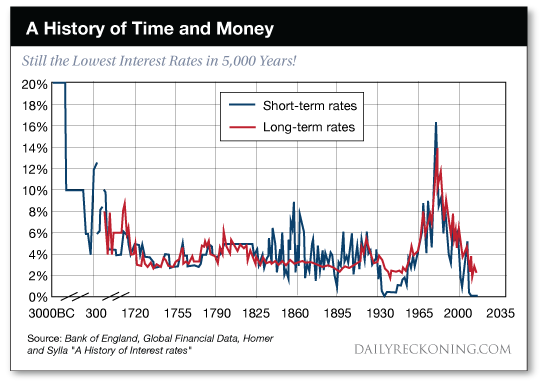

Keep this chart in the back of your mind as you watch the interview. Normal? Short-term rates are the lowest in 5,000 years, while debt is the most in the last 100 years. Negative rates in Europe. European junk bonds yielding the same as U.S. Treasury bonds. The Bank of Japan owning 45% of Japanese government bonds and 71% of their ETFs, according to Bloomberg. The ECB is buying up every bond they can find. Higher tax pressures, massively underfunded pensions, central banks exiting QE… I’m betting on beautiful and our models have us “risk-on” but I feel that I, too, may have a “fatal attraction for the slim chance.” OK, just saying… it’s a tricky time.

Trade Signals — High Yield Warning Signal?

S&P 500 Index — 2,570 (11-15-2017)

Notable this week:

Risk is becoming more evident in the markets. Notable since last week’s post are the following:

- High Yield moved to a sell signal (merits watching as HY tends to lead the equity markets). A warning signal? Too early to tell. There have been several false sell signals over the last twelve months; however, it bears watching.

- The Ned Davis Research CMG U.S. Large Cap Long/Flat Index remains moderately bullish but the trend, as measured across 22 sub-industry sectors, has turned down again – the fourth time this year. I expect the index will signal a reduction in large cap stock market exposure from 100% to 80% in the near future. When fewer and fewer stocks are carrying the markets higher, that’s when we should get most concerned. Below you’ll see we are beginning to see such signs.

- Gold remains in a buy signal per our intermediate trend indicators (below). The short-term gold signal also moved to a buy over the past week. We like gold for its diversification benefits and it serves as a hedge against central bank activity.

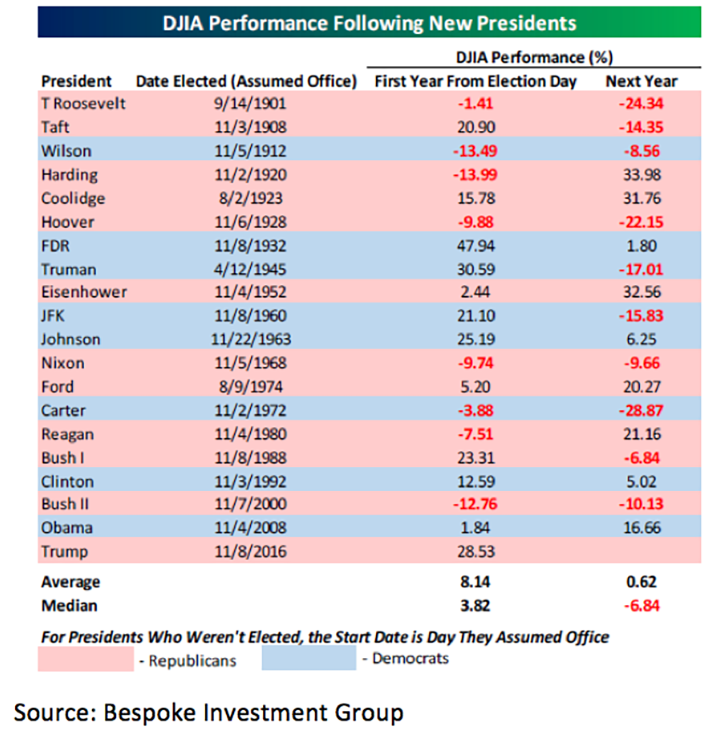

Tax reform? We’ll see. The following from Bespoke Investment Group courtesy of Jeffrey Saut of Raymond James. Source

The scatter chart shows the performances of the DJIA for each President listed on their first and second year from Election Day or assuming office. What’s important to note about this chart is that while market performance following first year gains of less than 20% were pretty much evenly split between gains and losses, after years where the DJIA rallied more than 20%, performance was negative in the second year two-thirds of the time.

And more from Jeff:

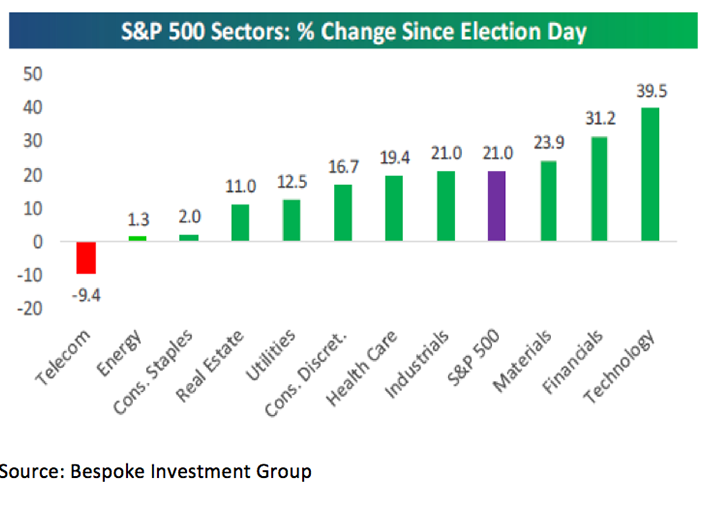

As written in Barron’s, “A Wellington Shields report notes that the records come with a surprisingly few stocks advancing. Last Tuesday’s new high in the Dow came with fewer than half the components participating. The NASDAQ likewise hit an all-time record with fewer than 30% of [its] stocks rising.” Ladies and gentlemen, there is a reason for that.

For the last three years 28% of the S&P 500’s 27.2% return has come from the FAANG stocks.

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note — He Ain’t Heavy, He’s My Brother

He Ain’t Heavy, He’s My Brother

The Hollies

The road is long

With many a winding turn

That leads us to who knows where

Who knows where

But I’m strong

Strong enough to carry him

He ain’t heavy, he’s my brother

So on we go

His welfare is of my concern

No burden is he to bear

We’ll get there

Long, winding, leads us to who knows where. Let’s put all negative frustrations aside. We’ll get there… Glad to be sharing the ride with you. I tell my kids to create great things… because they can. Let’s focus on doing great. Because we can.

Everyone is coming home for Thanksgiving. The “Tuscan table” awaits along with a celebration of family. Crazy about my family. I can’t wait.

I’ll be in NYC on Tuesday to meet with the team from VanEck and may try to schedule some media. I’ll be driving home with Brianna. I see some high 40 degree golf in our near future. Dad likes that.

Normally I take the train in, but this time I plan on driving. Her apartment is so small, I believe the summer clothes are coming home with me to store for the winter, thus the car.

Business follows in St. Louis just after Thanksgiving and then Susan and I are heading to Mexico for a few days in early December. It looks like a quick trip to Boston to visit the team at Shepherd Kaplan, then Utah follows just prior to Christmas for a few advisor meetings and a few days of skiing at Snowbird. Hoping for big snow.

Wishing you a wonderful Thanksgiving holiday. Here’s a toast to you and those most important to you.

Finally, can I ask you a favor, if you know someone you feel may benefit from On My Radar, please send them a copy. I believe we are going to have another major market dislocation within a year or two and I hope to help as many people as I can. We need to not get run over on our way to the next great buying opportunity. There are things we can do. I want to get the “participate and protect” message out to as many people as I can. The subscription link is below… Thank you – and thanks for reading. Please know how appreciative I am of you.

Have a great weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group