From time to time we illustrate our analysis of highly innovative companies in a Knowledge Leader spotlight. Today we look at Microchip Technology Inc. (MCHP), a highly innovative semiconductor manufacturer that produces programmable microcontroller products used in autos, computing and lighting, among many other applications. It also produces application development tools for microcontrollers, analog devices, timing products, memory products, and it licenses technology under trademarked brands. The firm is following a deliberate innovation strategy that can be observed and measured from a forensic accounting perspective. Key traits of most innovation strategies include a shift from tangible to intangible forms of investment, falling overall capital intensity, stable to rising profitability, the production of excess cash, and the return of that cash to shareholders in some form. We observe those highly-sought-after traits when decomposing MCHP’s financials, which make it an interesting stock from a fundamental perspective. Furthermore, even though the company may be in an operationally superior position now compared to the tech boom period of the late 1990s and early 2000s, it is selling for a fraction of the valuation.

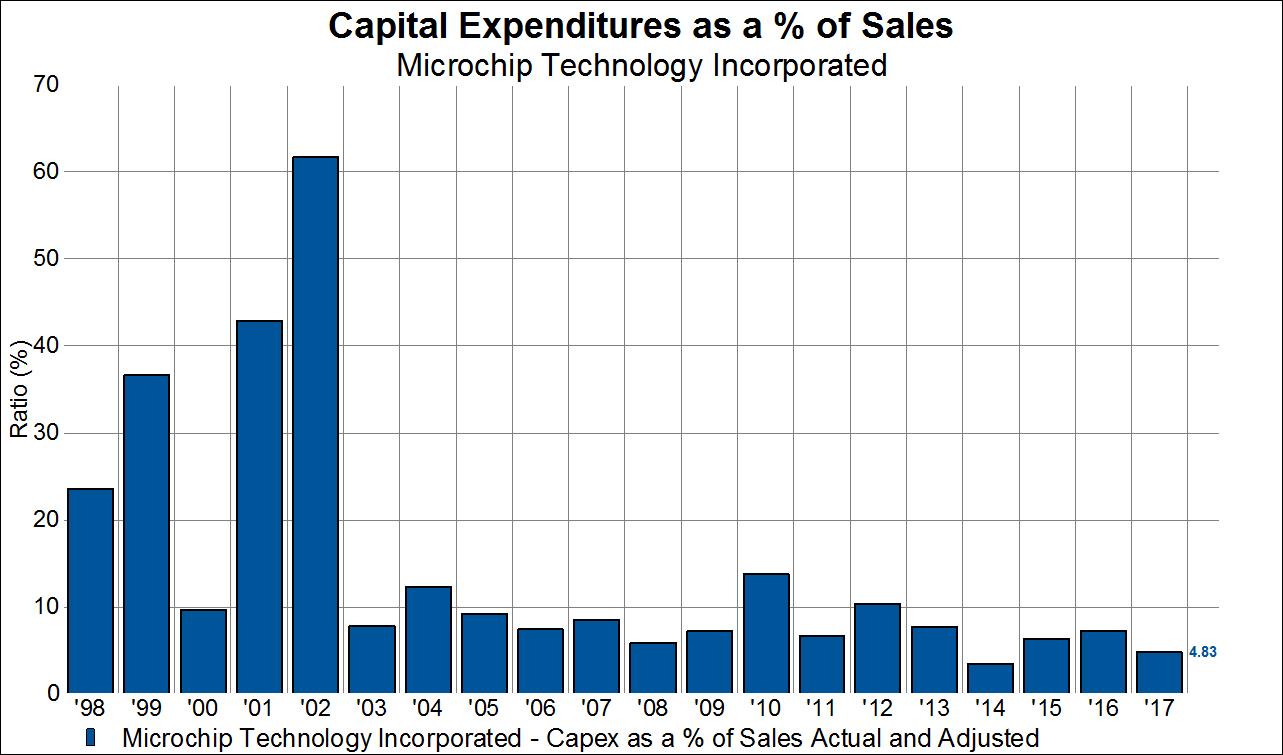

A classic, if not required, signal that a company is following an innovation strategy is a shift in investment from tangible to intangible forms of capital. Since 2002 MCHP has cut investment as a percent of sales on physical capital by 94%.

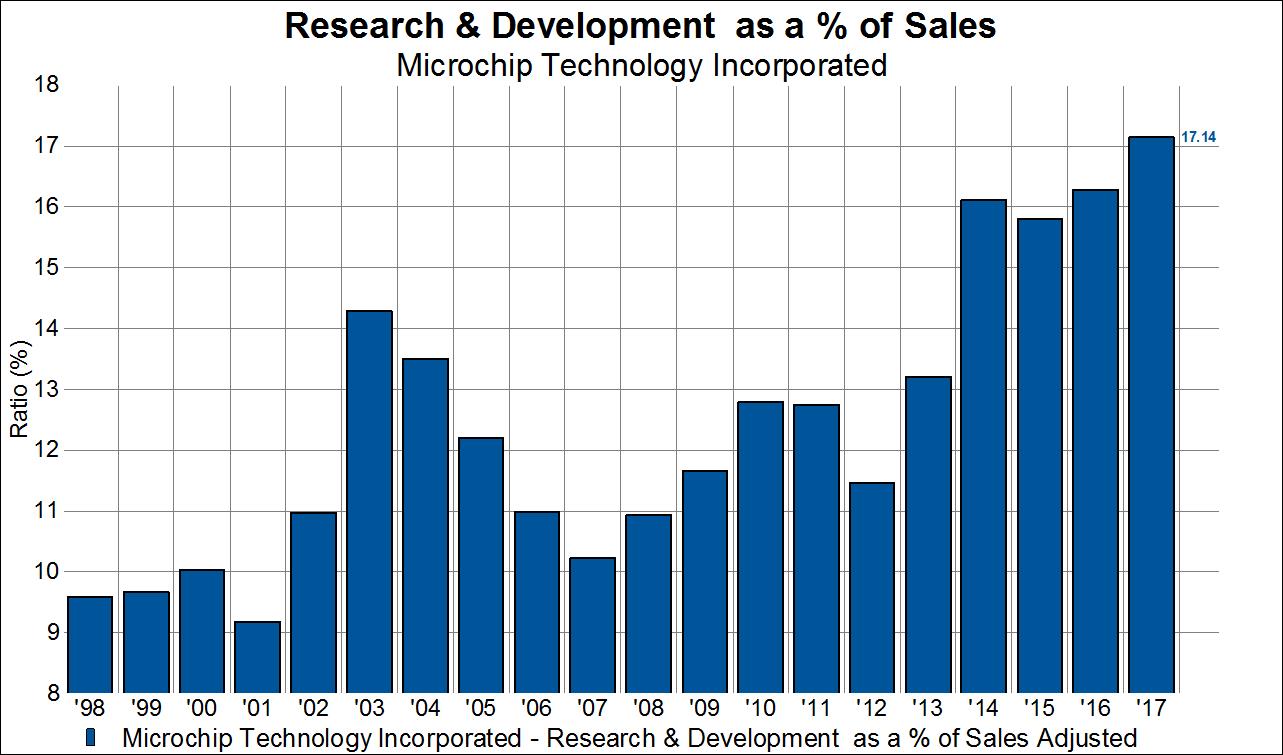

MCHP has raised investment in R&D by 54%.

In this next chart we can see the metamorphosis in the company’s asset base. In 2007 property, plant & equipment (red line, right axis) accounted for 24% of assets versus just 9% of assets today. Intellectual property assets (blue line, left axis) have risen from 13% of the total to 17% of the total since 2007.

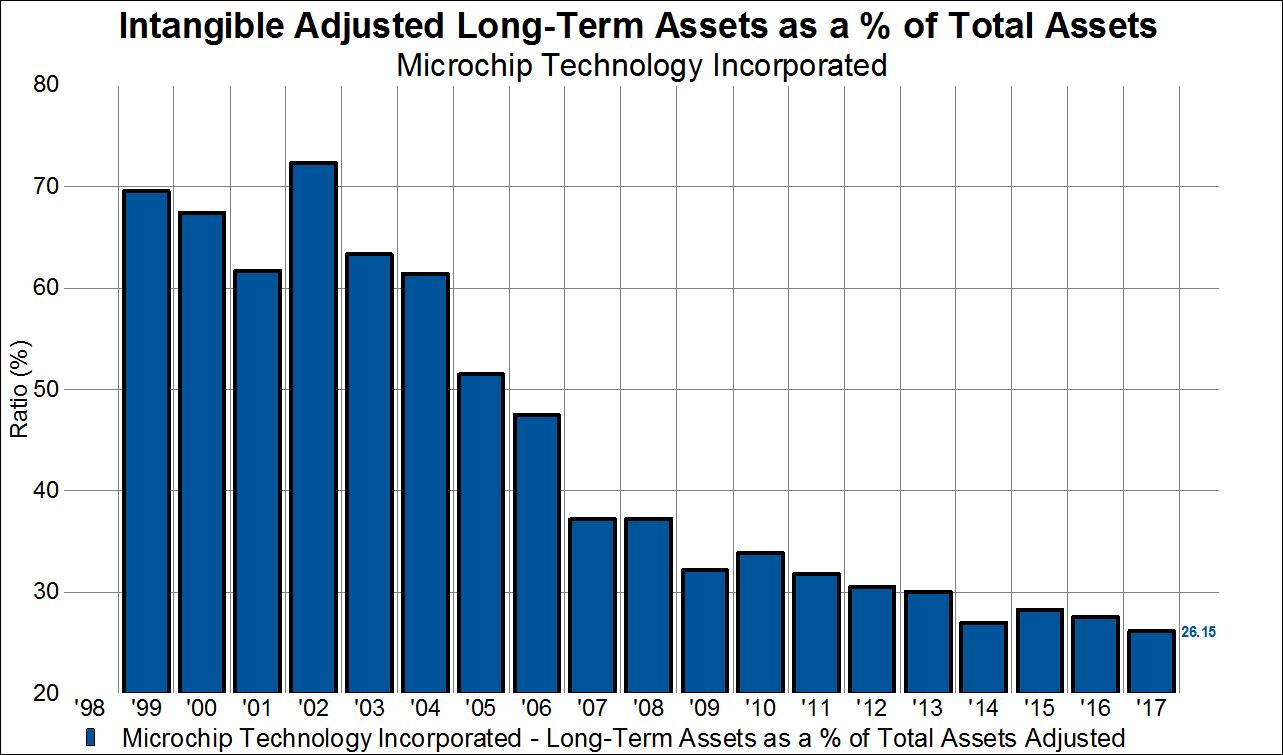

In total, investment in physical capital has fallen more than investment in intangible capital has risen. This has meant total long-term assets (physical plus intangible capital) as a percent of total assets has fallen by about 2/3 since 2002. Generally, a shrinking productive asset base would be seen as counterproductive to growth, since firms need assets to make products. But with MCHP this isn’t the case.

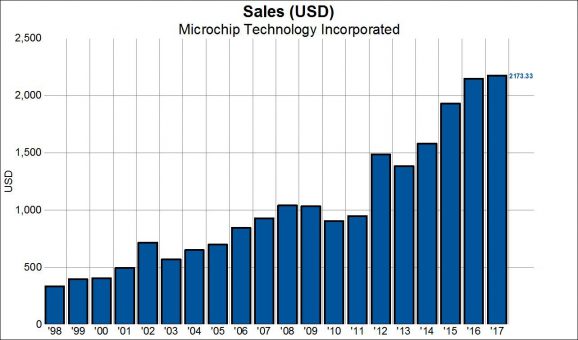

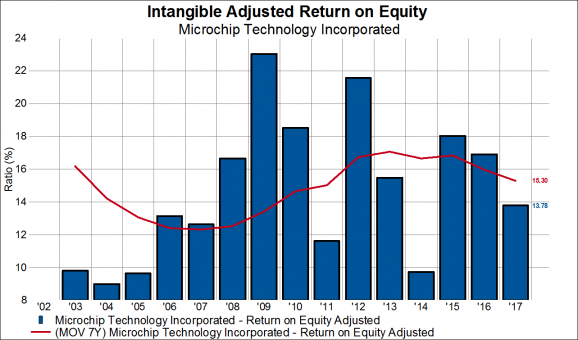

For example, sales have more than tripled since 2001. It looks like all those investments in R&D are paying off.

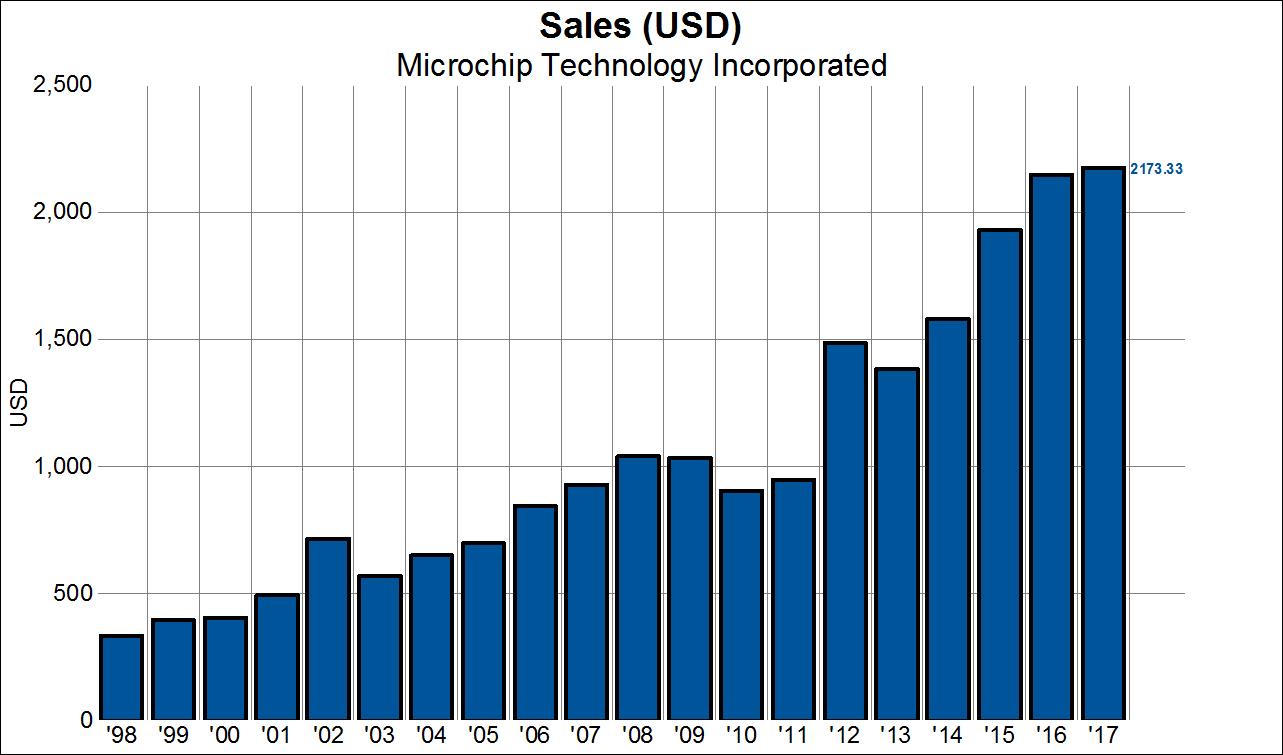

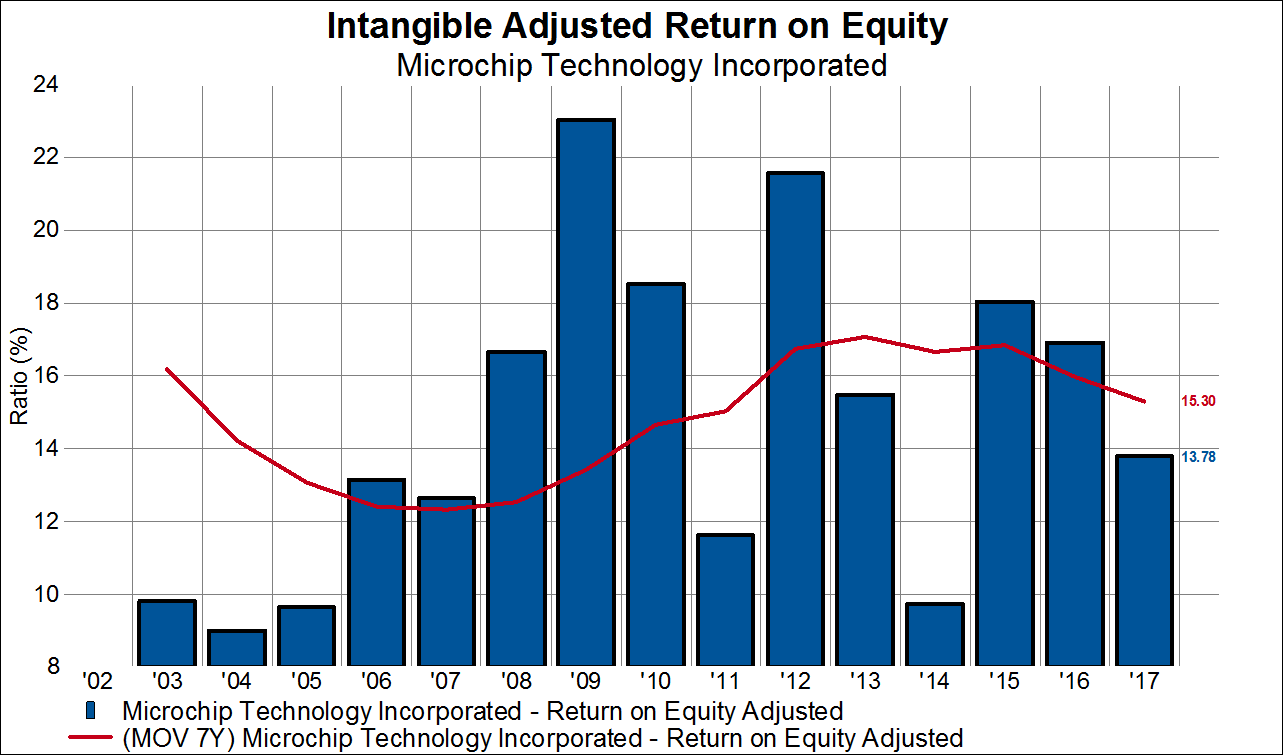

Meanwhile, profitability has remained steady, if not on a generally rising trend as measured a long-term average (red line). How can profitability be steady to rising while total productive assets are falling as a percent of the asset base? The answer is that the return from investing in intangible capital is much higher than the return from investing in traditional property, plant & equipment.

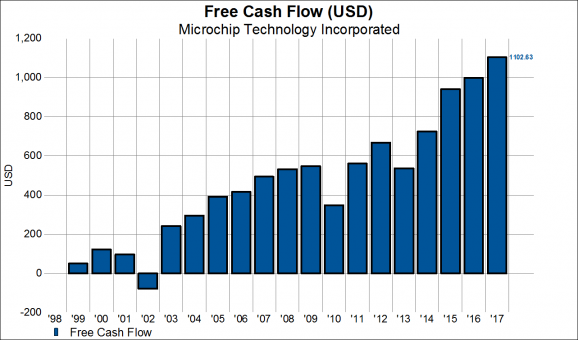

The consequence of strong profitability and a diminished need to reinvest in the business – because the investments undertaken today are more productive than those undertaken yesteryear – is the generation of lots of free cash flow. Free cash flow is what is left over after paying all the expenses and making new investments in the business.

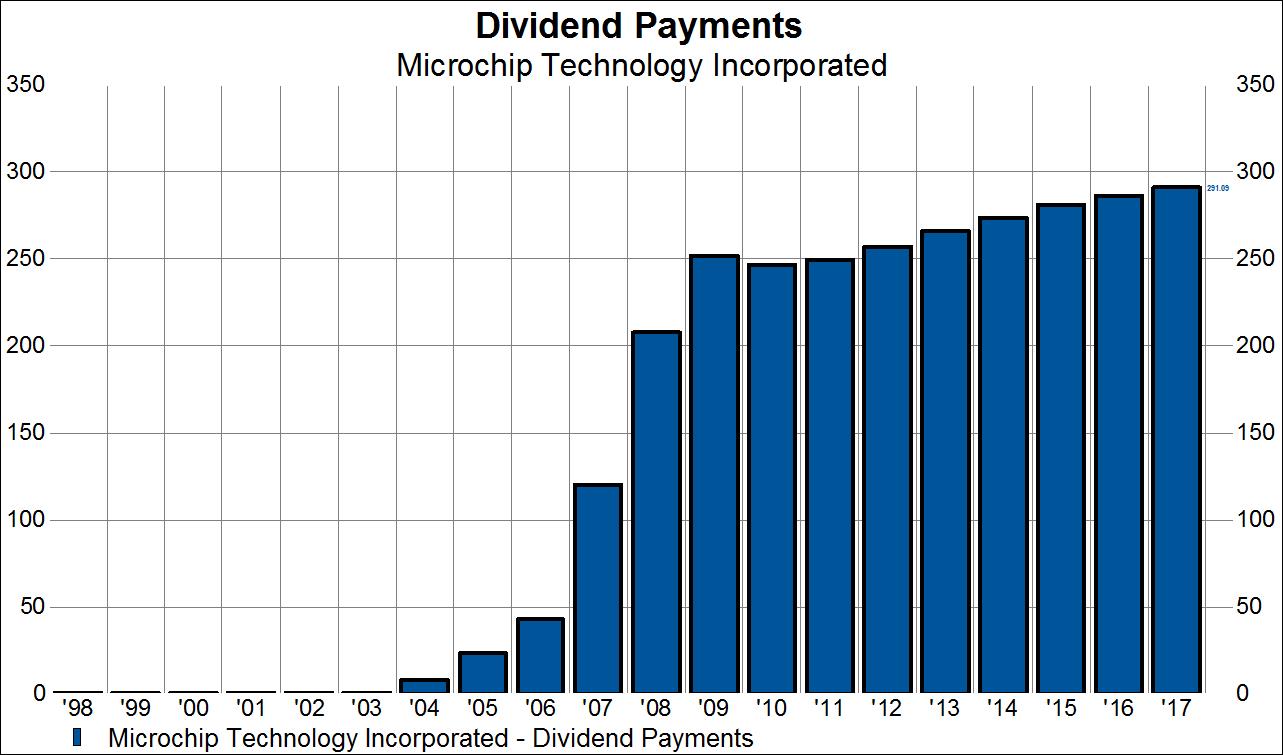

When free cash flow is abundant then firms can begin to do shareholder friendly things like pay dividends.

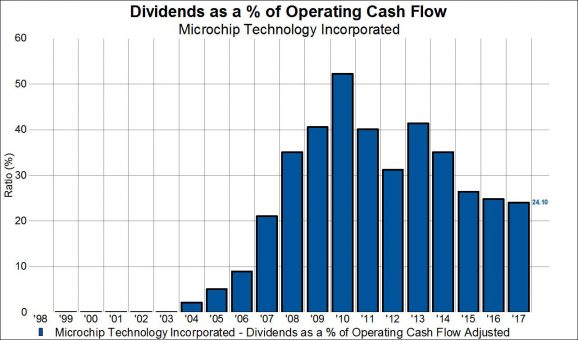

Even though dividend payments are the highest they’ve ever been, they only account for 24% operating cash flow, implying lots of room to grow the dividend in the future. Investors love to see that companies have room to raise the dividend.

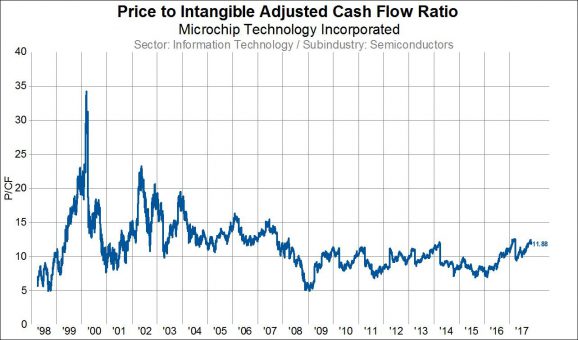

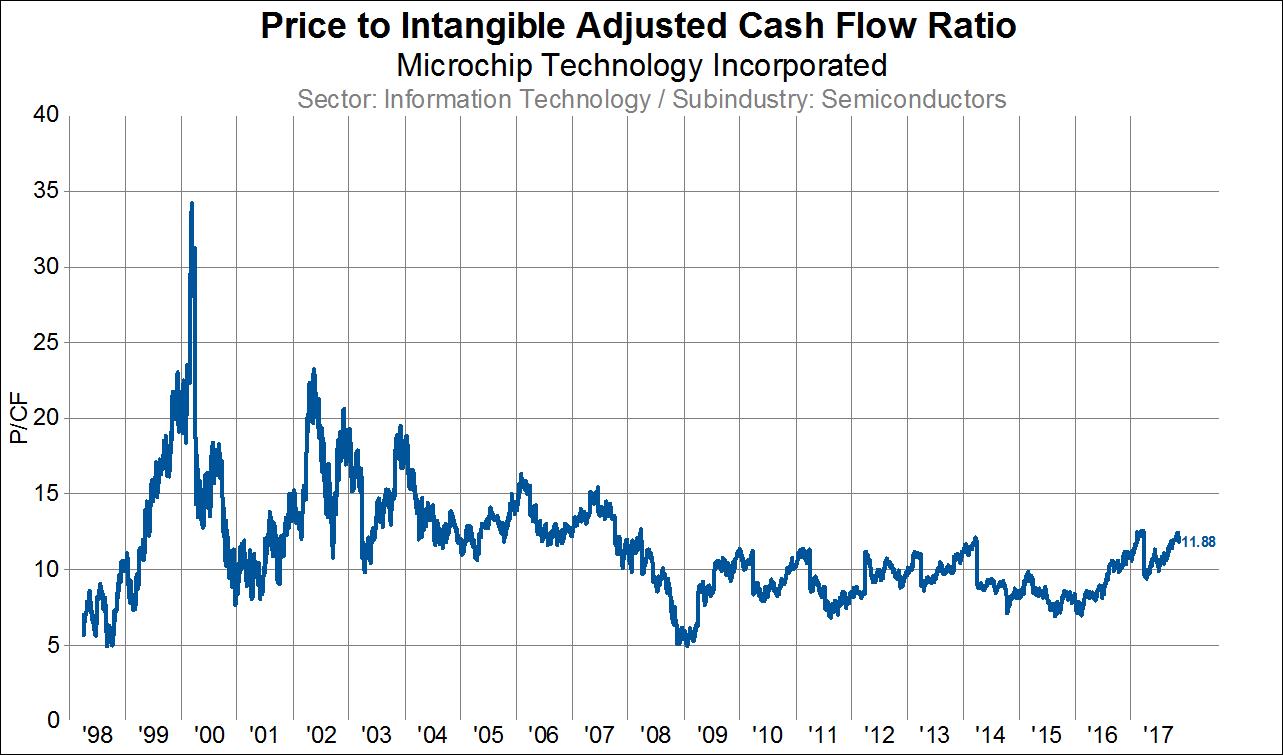

So far, we’ve witnessed MCHP transform how it invests and the beneficial consequences of its deliberate intention to innovate. The company today is operating more productively than it did during the tech boom and has demonstrated a continued ability to grow and make money. Yet, it trades for about 1/3 of peak valuation seen back in 2000 as measured by the price to cash flow multiple. Even though the valuation has risen recently, the stock still trades for a lower multiple to cash flow than it did during most of the period from 1999-2007.

Disclosure: as of 10/31/2017, Microchip Technology Inc. was held in the Knowledge Leaders Strategy.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital