Economists view the growth in labor productivity, or output per worker, as the single most important variable in an economy. It’s what lifts the standard of living, helps keep prices low, reduces government budget strains, and drives corporate profits. Over the next few decades, achieving faster productivity growth will be key as labor force growth slows. The outlook is encouraging, but uncertain.

Productivity growth has slowed significantly over the last decade. Some may be quick to blame polices out of Washington. However, the slowdown in productivity growth has been observed worldwide (that is, it can’t be due to U.S. policies alone). Most economists believe that the slowdown reflects weaker capital spending following the Great Recession. In the U.S. capital spending had begun to pick up in the middle of 2016 and has been further fueled by improvement in business optimism in 2017. A stronger global economy has helped. Most long-term economic models include stronger productivity growth assumptions over the next ten years.

One of the long-standing strengths of the U.S. economy has been its ability to re-invent itself. New industries arrive over time while others fade away. Through this process, low-productivity jobs are shed, replaced by higher-productivity jobs. However, as the population ages, we can expect to see less turnover in the economy. There is less job-hopping and less migration to other areas of the country. In turn, productivity growth will be less than it would be otherwise.

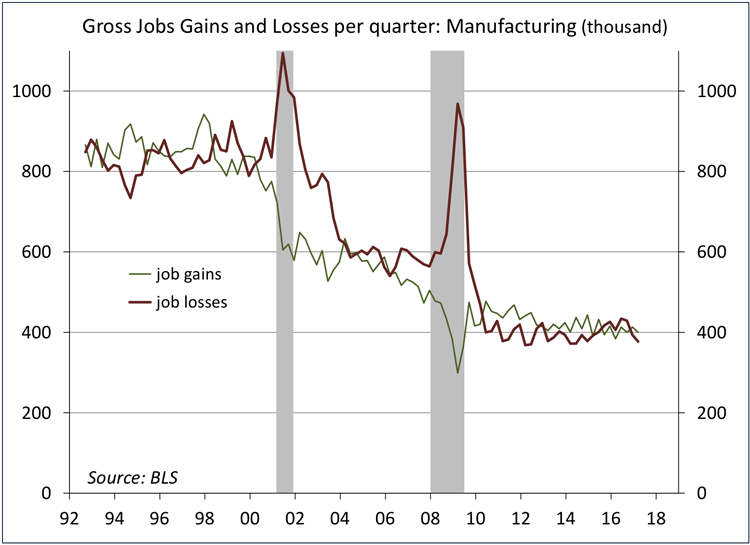

This has been especially true in manufacturing, where growth in output per worker has long outpaced overall productivity growth by a wide margin, reflecting advances in technology and the impact of increased global trade. The share of employment in manufacturing had been trending lower for decades, well before the rise of trade with China.