On My Radar: Global Macro Outlook & Probable 7-, 10- and 12-Year Equity Market Returns

Learn more about this firm“We are going to have to address the debt. And we are going to get more debt.”

– Joe Kalish, Chief Global Macro Strategist, Ned Davis Research

This week’s On My Radar is an investment outlook piece. While current trend evidence remains bullish, you’ll see valuation data below that tells us the coming 7-, 10- and 12-year equity market returns are not so good. Your and my clients are expecting 10% forward returns; however, due to extremely high valuations they are likely get 0% to 2%. Trouble spots? There are many. It is the bubble in the bond market that has me most concerned. Let’s be grateful for the run and be prepared to shift from offense to defense.

Trend evidence continues to point positive for equities. My favorite weight of evidence indicator is The Ned Davis Research CMG U.S. Large Cap Long/Flat Index. It looks at the momentum and overall market breadth measuring 22 sub-industries. When the majority of industries are in positive up trends, equity markets do best. When just a few stocks carry the market indices higher and the majority are breaking down, equity markets fair worse. The NDR CMG Long/Flat signal is bullish.

GMO has put out a 7-year Real Asset Return Forecast for many years. It 1999, they forecasted -1.5% returns. Today, you’ll see in a chart below, GMO is forecasting -4.1% annualized over the coming 7-years. Yes… minus. Image your $1,000,000 in Large Cap stocks worth $750,000 in the year 2024. That’s the forecast. Many thought they were nuts in 1999. They were right. You and I may think they are nuts today. What if we are wrong? GMO’s valuation process is sound.

You’ll also see in the charts I share with you below that the 10-year and 12-year numbers are not as dire but they are not so good. It’s what happens when valuations reach near all-time highs.

As posted each week in Trade Signals, the equity market trend has been bullish all year and that remains the case today. Also, Don’t Fight the Tape or the Fed remains bullish and there continues to be more buyers than sellers, as measured by Volume Demand vs. Volume Supply. So for now the trend remains ‘risk on’ but let’s keep a close eye on the signals as we move into 2018.

Looking at the macroeconomic landscape from 30,000 feet, the global economy is on solid footing and corporate earnings are generally good. Our favorite recession watch indicators tell us the probability of recession in the next six to nine months is low. There are, of course, serious geopolitical issues, sovereign debt default concerns, demographic challenges, a nearing pension crisis, record high valuations, ultra-low bond yields and inflation is picking up its head. And lest we forget that central bankers are tapping the brakes, pressing the clutch and starting to shift their engine into reverse gear.

We are eight years into a bull market and I personally believe there is more run left in the run. Yet front of mind that recessions have occurred one or two times each decade since 1850 (last was the great recession in 2008-09) and the debt load and today’s initial starting conditions make it a more challenging for the Fed when it comes time to fight the next fight. I have my doubts the current decade escapes recession.

Currently, there is no sign of recession and there are other positives such as the potential repatriation of $3 trillion in offshore corporate cash and tax reform. My two cents: stay alert and risk-minded and go with the weight of stock and bond market evidence.

Yesterday, I spent two hours with the Ned Davis Research global macro team. It was a lunch meeting at the famed Union League in downtown Philadelphia. You’ll find my summary notes in the first section below, followed by the most recent valuations and forward return data. I conclude with my thoughts on fixed income exposure. With 10-year Treasury yields at 2.40% but less than 1.00% after you factor in inflation, bonds are the least productive asset in your portfolio.

The biggest bubble of them all is in the bond market. Global debt is out of hand. Rates are negative in much of the world. I believe that inflation will be higher a year or so from now, the central bankers will raise rates and that move will kill the economy and drive us into recession. We go higher then lower and may ultimately take out the 1.37% yield low made in July 2016. We’ll see.

I put this week’s post together with the intention of not only sharing it with you, but also using it as a template for my team’s December investment research committee debate. I hope it helps you as well and please reach out to me if you have any questions.

Grab a coffee and find your favorite chair, click through and read on. A number of charts but a relatively quick read.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- Global Market Outlook

- Stock Market – Valuations and 10-year Forward Returns

- Bond Market – Higher Rates, Flattening Yield Curve, Then Lower Rates

- High Yield Junk Bonds

- Personal Note — NYC, Chicago, Michigan, St. Louis and Vacation

Global Market Outlook

Ned Davis Research (NDR) has a holistic way of looking at markets. They consider how the market “should be” acting and how the market “is” acting. A global macro fundamental, technical and investor behavioral total view.

I’ll cut through the two hours and give you my high-level summary notes:

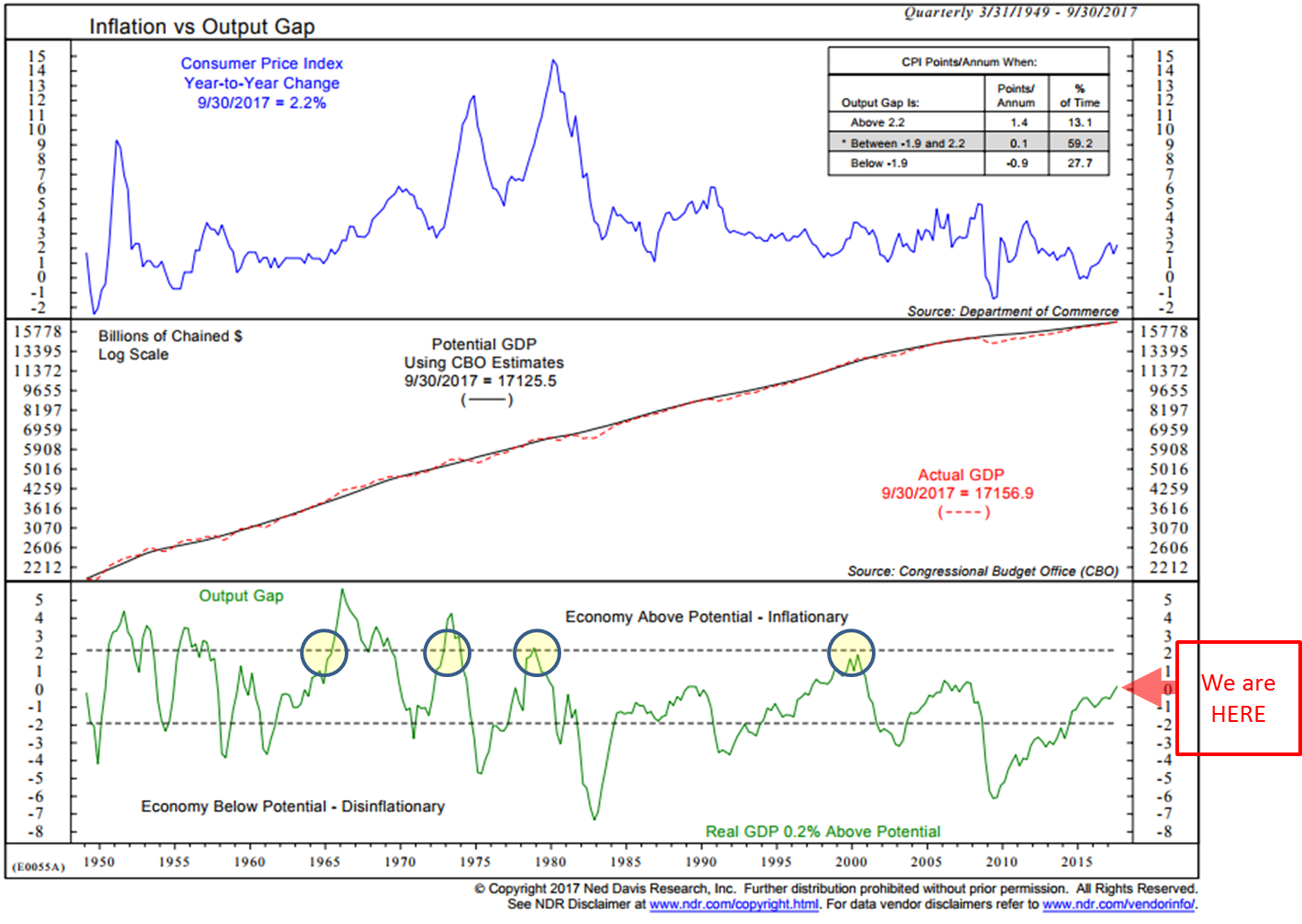

On Inflation and Central Banks

- Low core inflation currently persists in the U.S. and around the world.

- Interestingly or frustratingly (for those bearing the brunt), shelter (housing) is running at 3.25% but overall inflation is low (below 2%). NDR noted that if individuals are spending more on shelter, they have less left over to spend on other things. Thus overall low inflation.

- In the U.S., the labor markets have tightened. Recruiting difficulty is high. Labor compensation is rising! That may lead to rising inflation pressures.

Why is inflation so low?

- The Fed is underappreciating aging demographics.

- Debt is high and a drag on growth.

- Technology and globalization are both keeping prices down.

When will inflation pick up?

- It may be two years before we see inflation pressures pick up.

- Note in the following chart the bottom section showing the “Economy Above Potential – Inflationary.”

- We should see inflation pick up when we get above the dotted line in the bottom section of the chart.

- Bottom line: short-term cyclical pickup in inflation but no serious long-term secular inflationary risk at this time. I’ll post this chart for you from time to time:

Economic Outlook:

Economic Outlook:

- Global growth remains steady.

- Seeing broad breadth in Manufacturing Purchasing Managers Index – a strong reading leaves NDR to not worry about the economy for at least three to six months or perhaps through the balance of 2018.

Recession:

- Overall economic outlook is good.

- There is little chance of recession in the next six to nine months.

Equity Markets:

- Stocks are richly priced.

- Haven’t had a 5% correction in over a year.

- Global breadth and momentum are positive.

- Stocks still look like a better value vs. bonds.

Bond Markets:

- Seeing cyclically higher inflation, but a long-term secular inflation call is far away.

- Not enough evidence to declare the bond bear market is here.

Why volatility is low:

I found the discussion around volatility interesting (especially the thinking around target date funds – I hadn’t thought of that). More of my notes:

- Technology and better information systems.

- Asset allocation rebalancing – As time steps forward, target date funds must sell equities and rebalance to bonds…aging population and the popularity of target date funds. (SB here – interesting…forcing clients into more and more bond exposure at near zero interest rate returns… seems pretty risky to me).

- Central Banks – QE and better communication. Noted was that central banks are buying securities you and I would never consider buying, such as negative yielding bonds.

- Index Funds – All the money into passive index funds causes buying of every stock in the index. Reducing overall market volatility.

- Bank regulations requiring higher capital and liquidity.

NDR expects an extended period of low vol and noted that outside of 2007 we’ve never really been at these (low vol) levels before.

Bottom line: while there are some short-term signs of a pickup in inflation, enough to give the Fed cover to continue to raise rates… they want to normalize rates (get them to 3% before the next recession)… those rate increases may likely send us into recession… in recession, we’ll likely see rates move lower.

I’ll repeat what I shared in the introduction today, “The biggest bubble of them all is in the bond market. Global debt is out of hand. Rates are negative in much of the world. I believe that inflation will be higher a year or so from now, the central bankers will raise rates and that move will kill the economy and drive us into recession. We go lower and may ultimately take out the 1.37% yield low made in July 2016.”

Stock Market — Valuations and Forward 10-Year Returns

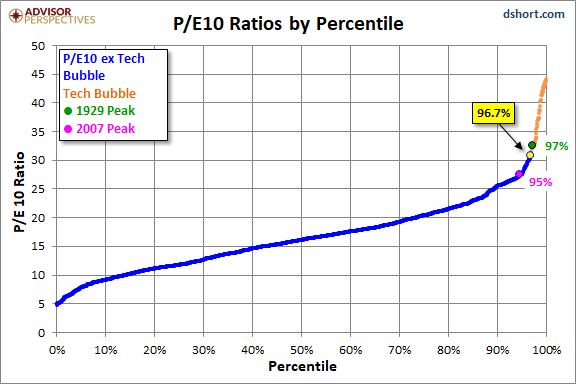

I shared this next chart with you last week. Let’s use it as a starting point. Simply note that valuations are high.

Chart 1:

- Note the yellow dot vs. the 1929 and 2007 market peaks.

- The orange line marks the Tech bubble period.

- We are 3/10ths of a percent from the 1929 valuation high.

Source: dshort.com

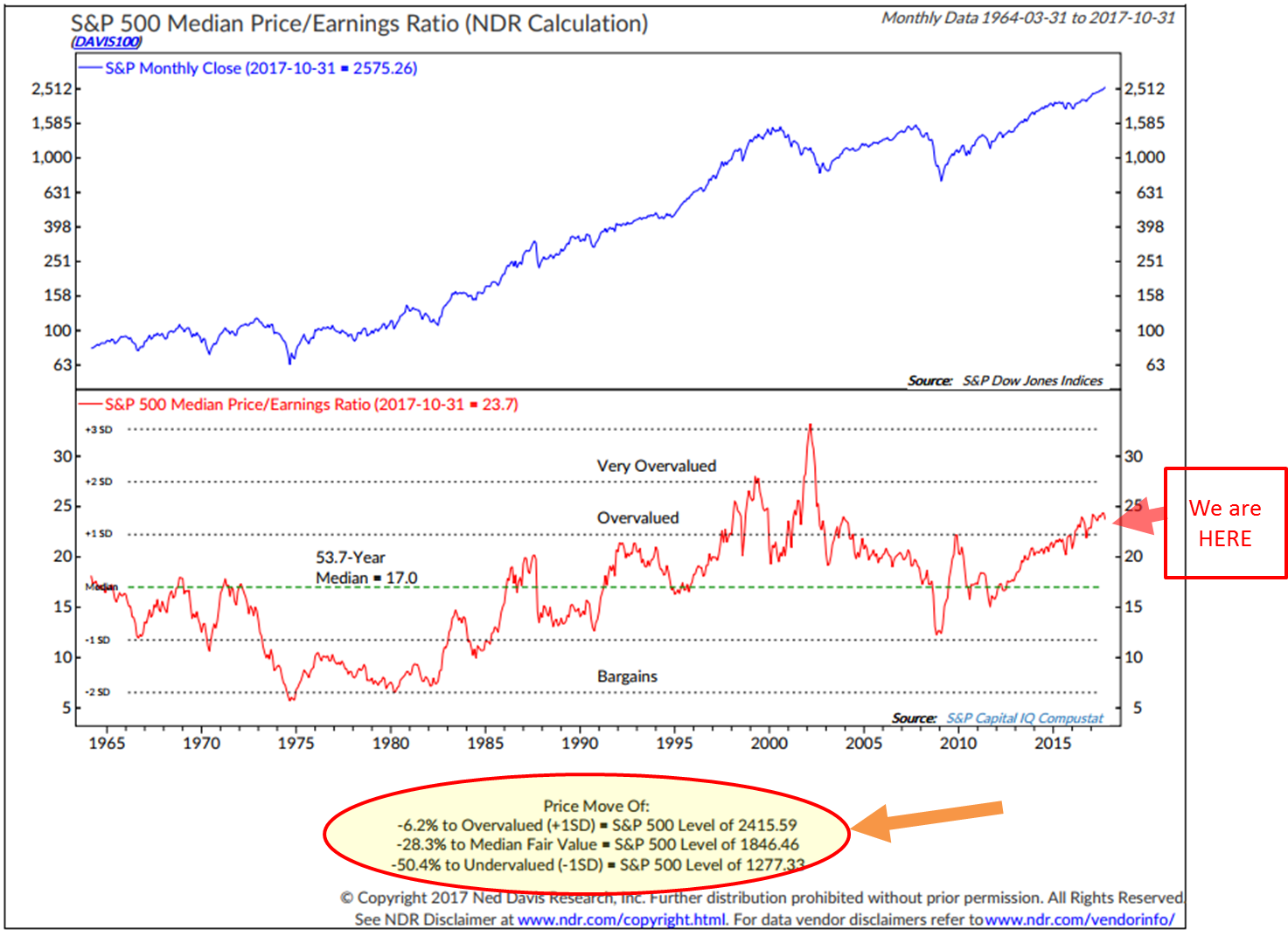

My favorite valuation chart is median P/E. I like it because by looking at the median P/E (the P/E is the middle out of all the stocks in the S&P 500 Index), it tends to eliminate one-time accounting items, etc. I also like it because we can then compare where we are valuation-wise vs. where we have been historically and get a good sense of what the forward 10-year returns might be.

Chart 2: S&P 500 Index Median P/E

- Note the “We are Here” – Overvalued area.

- Note few times since 1964 where the market was this much overvalued.

- Take a look at the orange arrow and the yellow highlighted oval.

- It shows just how far the market is priced above “median fair value” and the amount of decline it would take to get to that level.

- I also like how it considers levels of both “Overvalued” and “Undervalued.”

- Think of them as risk and return targets.

Source: Ned Davis Research

If we get a 28.3% correction, buy the market. If we get a 50.4% correction, go all in. Until then, follow trend evidence to help you risk-manage your exposures.

I want to note that valuations are a poor market indicator. What is overvalued today can grow to be even more overvalued. That is what the bullish trend evidence is suggesting today. More run left in the run? Maybe.

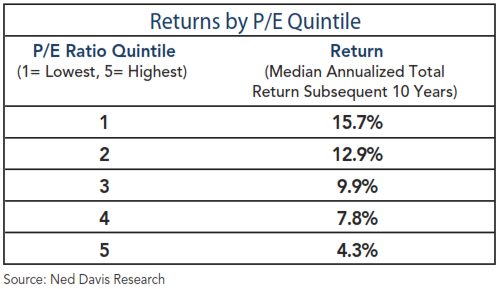

Chart 3: What Median P/E Tells Us About Coming 10-year Returns

When valuations are high, forward returns are low. We have no idea as to the next one to two years but we have a really good idea about the coming 10 years.

Here is a look at the data (1926 to December 31, 2014) and how to read it:

- Returns are ranked by quintile. 1 is lowest incidences of median P/E, 5 are the highest incidences. Reported is the nominal (before factoring inflation) subsequent 10-year realized median returns by quintile.

- They took each month-end median P/E and looked at the annualized return that occurred in the S&P 500 Index 10 years later.

- Then they sorted the results into five quintiles and posted the median annualized return by quintile.

- We currently sit in Quintile 5 today.

You can read more in a white paper I wrote called, “The Total Portfolio Solution.”

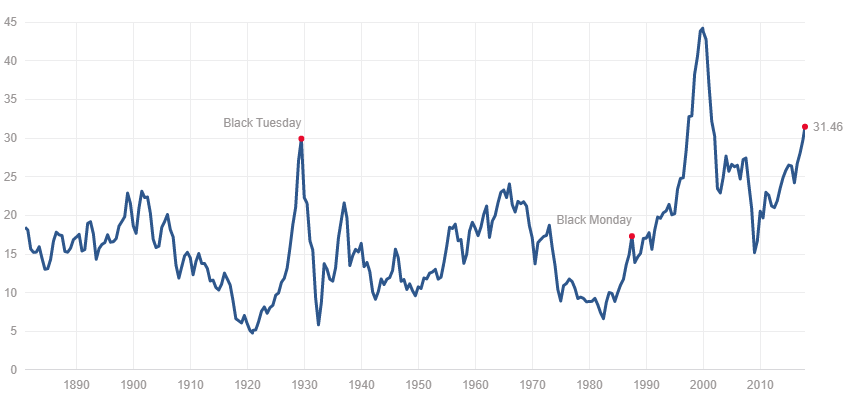

Chart 4: Shiller P/E Currently 31.46 (11-10-2017)

- Data is from 1880 to present (source).

- Note higher than 1929’s “Black Tuesday” and 1987’s “Black Monday.”

- Note higher than any other time with the exception of the 2000 Tech bubble.

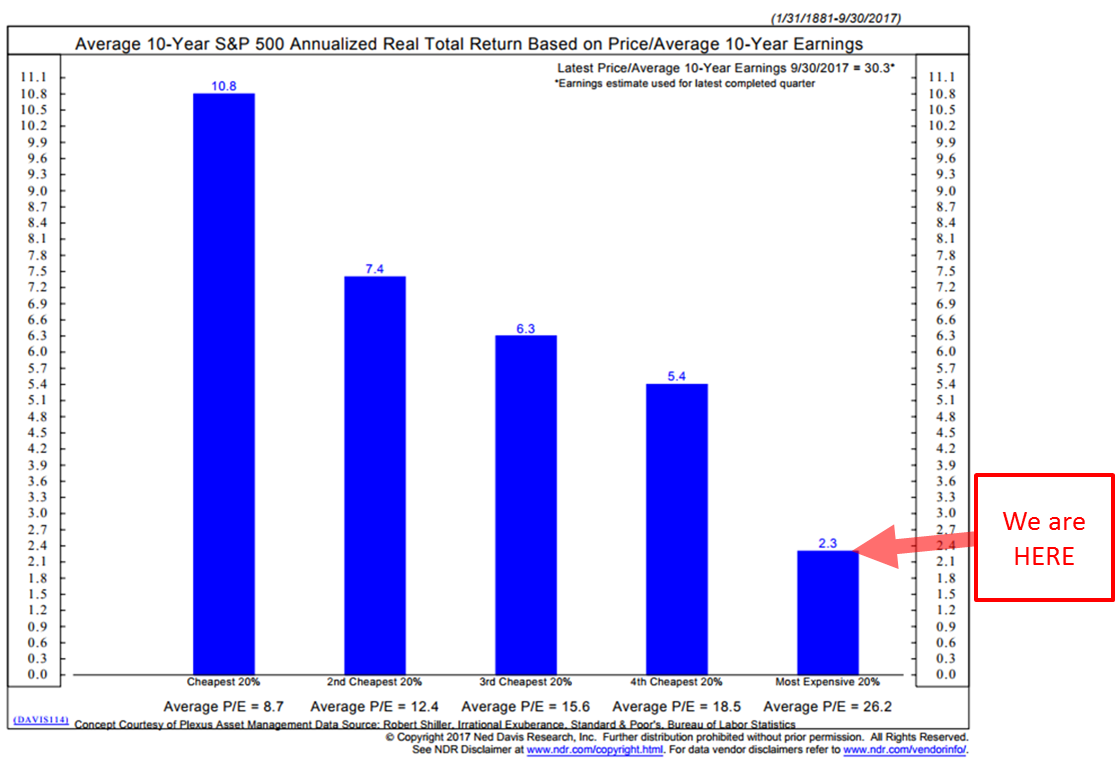

Chart 5: What Shiller P/E can tell us about coming 10-year REAL returns

Here’s how to read the chart:

- We sit high in the highest 20% of all monthly valuation numbers since 1880.

- The chart details the returns that occurred 10 years after each month-end Shiller P/E reading. It then groups the numbers into five quintiles ranging from lowest P/Es to highest P/Es and shows the average annualized return after inflation based on each quintile.

- Note the average P/E for each quintile is shown at the bottom of each blue bar.

- Bottom line: you get much more return on your money when you buy low (valuations are most attractive) and least when you buy high (like today). Expect 2.3% real annualized returns over the coming 10 years (and likely a bumpy road on the way to those low returns).

Source: Ned Davis Research

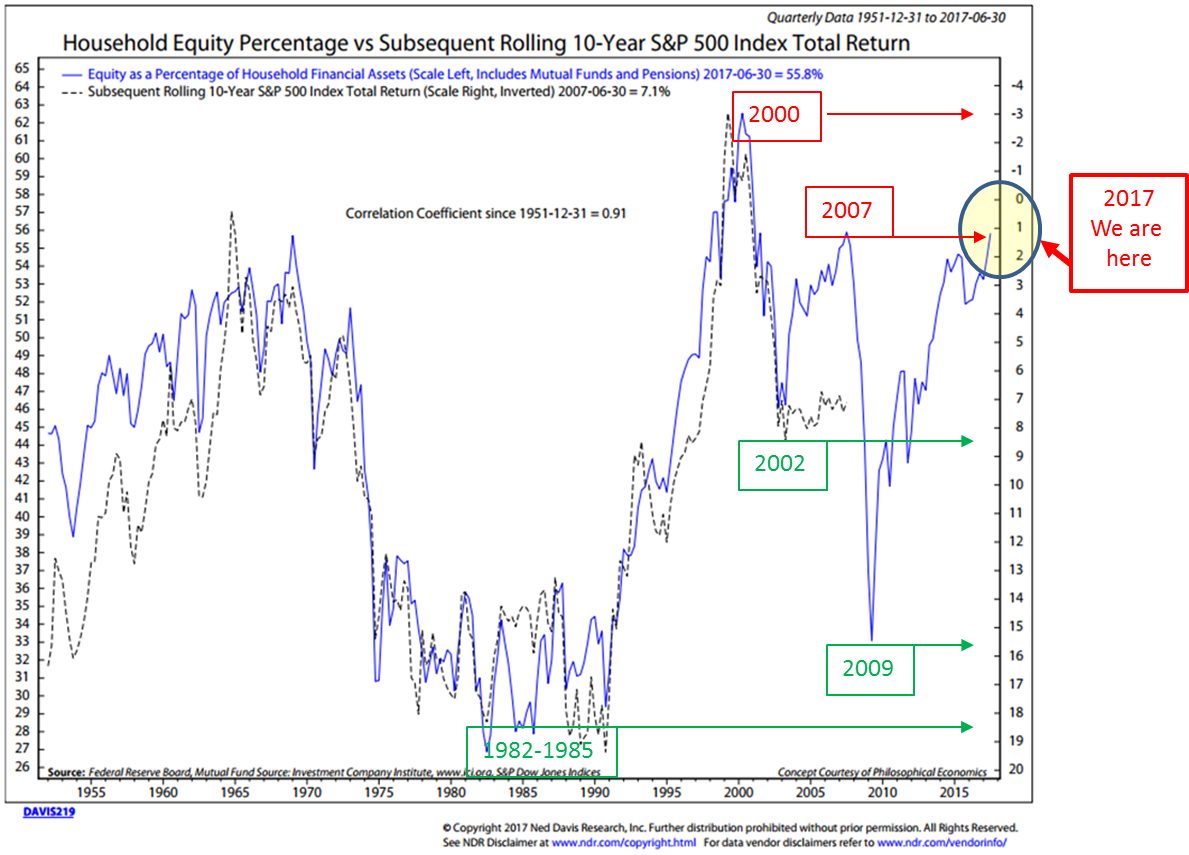

Chart 6: Stocks as a Percentage of Household Equity vs. Subsequent Rolling S&P 500 Index Total Returns

Here’s how to read the chart:

- Blue line tracks the percentage of household financial assets that are allocated to equities.

- When investors are heavily weighted into stocks, much of the buying has been done.

- Such periods of high stock ownership correlate with lower subsequent returns and low stock ownership correlates with higher subsequent returns.

- As Sir John Templeton said, “The secret to my success is I buy when everyone else is selling and I sell when everyone else is buying.” This chart demonstrates that saying.

- Note how the dotted black line (the plotting of the actual return over a rolling 10-year period) closely tracks the blue line… with a 0.91 correlation coefficient since 1951. In geek language, that’s a statistically significant correlation not to be ignored.

- This chart says we should expect 1.25% annualized returns over the coming 10-years… before inflation. Not so good.

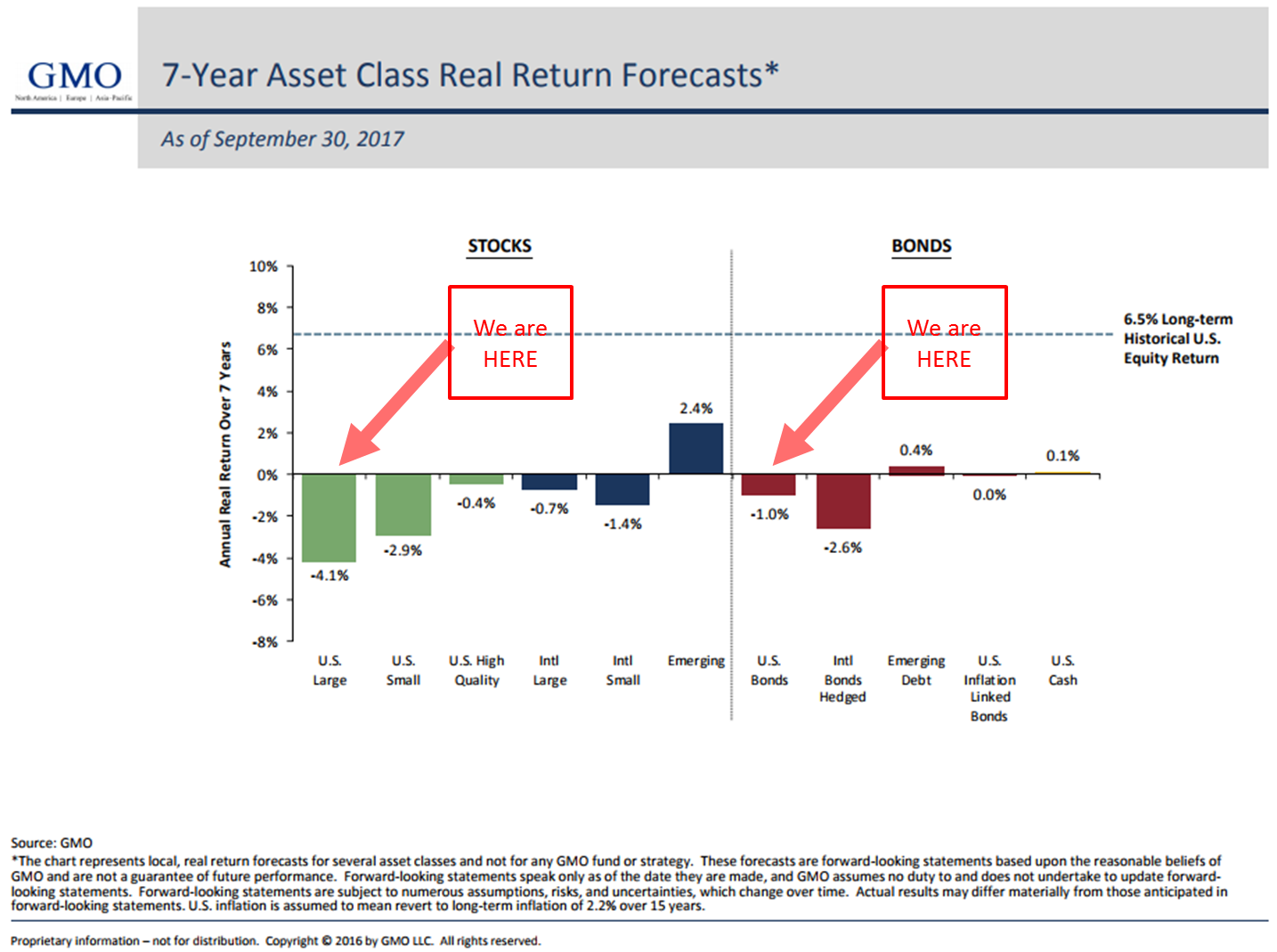

Chart 7: GMO’s 7-Year Real Return Forecast

- I added the red arrows for emphasis.

- Forecasting -4.1% for equities and -1.0% for U.S. Bonds over the coming seven years.

- Stay calm and read along… there are things you can do…

Chart 8: Other Valuation Measures

- Simple conclusion, most metrics are “Extremely Overvalued.”

Warren Buffett has a saying about hamburgers. He thinks investors should think about stocks like they think about hamburgers. When hamburgers are low in price, you get more for your money. When they are high in price, you get less. Same with the stock market.

I was going to add Hussman’s 12-year forecast (google it) and it too is telling us to expect flat to slightly negative returns over the coming period. But that’s enough for today and, importantly, don’t get depressed.

I often get an email saying, “Steve, you are so bearish.” I’m really not. If I was stuck in a buy-and-hold mindset, yes, I’d read the tea leaves as bearish and be depressed. However, I see like Sir John Templeton a way forward and my advice remains, simply follow the weight of evidence to risk-manage what you’ve got. So I’m happy.

Bond Market — Flattening Yield Curve

In case you missed the post, following is a reprint of a previously-shared OMR topic. I believe it is something that may help us assess overall market risk.

Let’s move on and take a quick look at what’s going on in the bond market. Take these charts with you when you meet with your clients or investment team. I’ll be printing copies for me to review with my team.

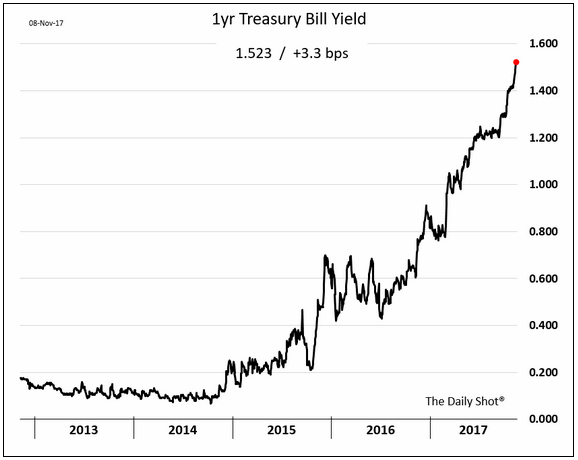

Short-term interest rates have risen sharply due to expectations for the Fed to continue to raise rates. Inflation rumblings are supporting the odds.

Here is a look at the one-year T-Bill yield.

At the same time, the long-end of the yield curve is not responding. Rates are little changed.

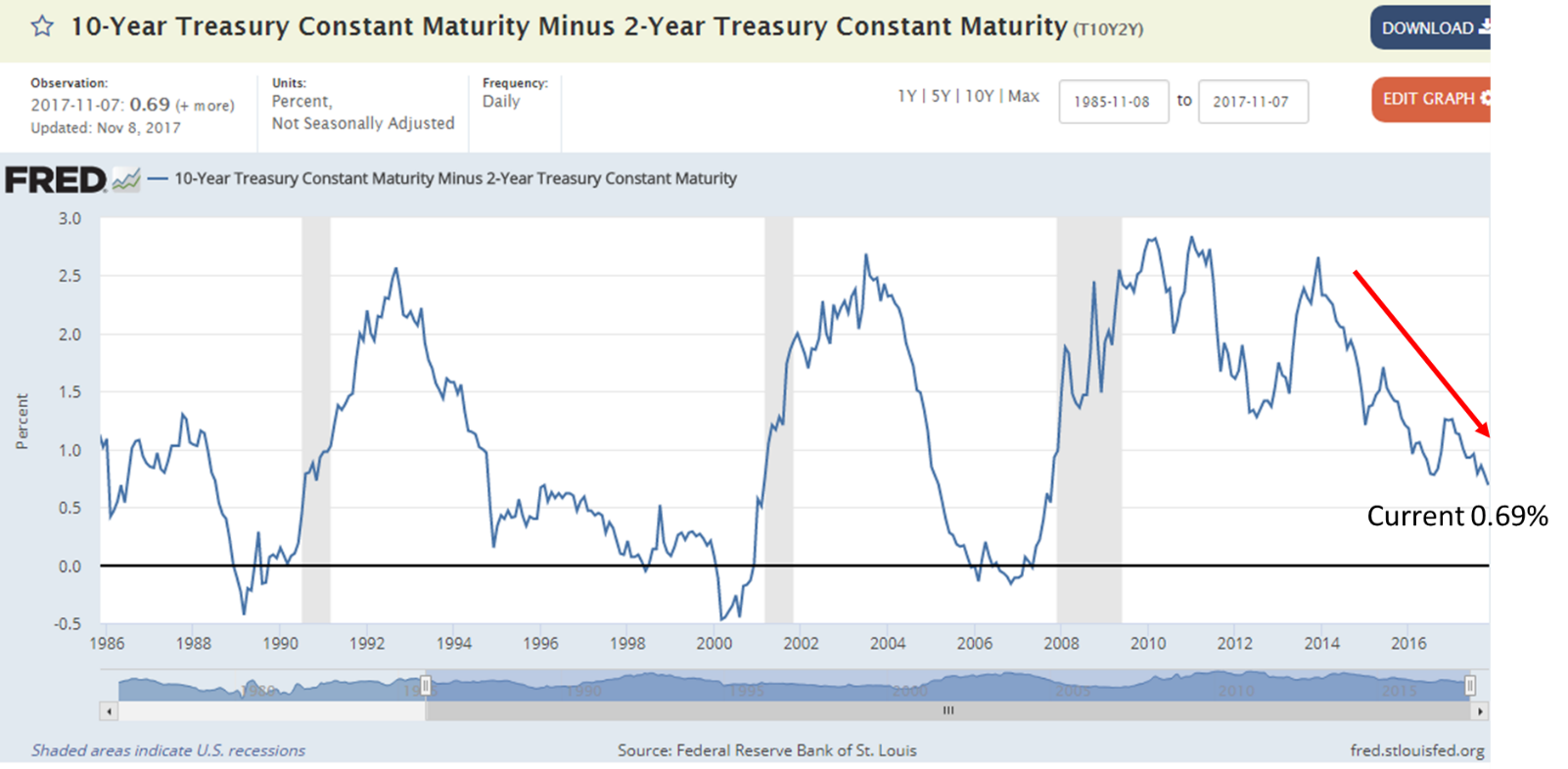

With short-term rates rising and longer-term rates stable, the yield curve (difference between short-term yields and long-term yields is flattening).

The current spread is about 69 bps or 0.69%, meaning the 10-year is getting only that much more over a two-year Treasury note. It is the lowest level since 2007.

Recession on the horizon? The most predictable indicator is an inverted yield curve (where short-term rates are higher than long-term yields) but not a mandatory condition.

Note that the yield curve can stay flat for a long time prior to a recession. For example, the spread was 35 bps in 1995 and it was 20 bps in 1999. The immediate good news is that all of our recession watch indicators show no sign of recession in the next six to nine months.

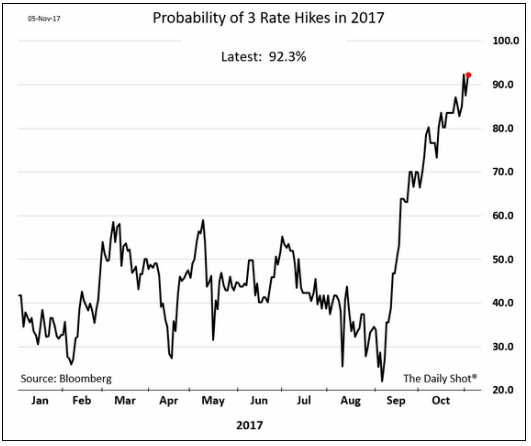

But the flattening squeeze is on. Odds of a December Fed rate hike currently sits at 92.3%. That’s another 25 bps off the spread.

Here is a look at the difference between the 10-year and two-year Treasury yields (red arrow is current trend). The data is through yesterday. 0.69% is the current difference. Note past inversions prior to recessions (shaded grey areas). Raise rates three more times at 25 bps each time and we likely invert

Source: Federal Reserve Bank of St. Louis

Let’s look at High Yield

High yield is rolling over. Our high yield signal moved to a sell yesterday. Too early to draw much conclusion, but it’s on my radar.

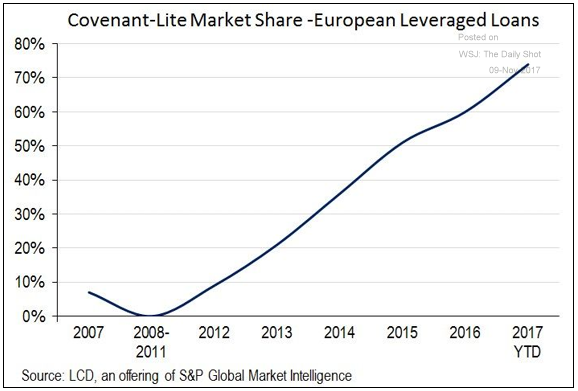

Historically, high yield turns early so we keep watch. The problem is the next correction will result in a high number of defaults as the quality of bonds and very low investor covenant protection (default and company restrictions outlined in the bond contract).

It is also bad in Europe (my bet as the epicenter of next crisis). Here is a look:

Oh, and you get about as much for a European HY bond as you do for a AAA-rated U.S. government-backed Treasury bond. Really? Really… #Madness I tweeted last week. Follow me @SBlumenthalCMG.

Default rates have been low globally because liquidity has been so high. The result of investors searching for yield in an ultra-low yield world. And too, the ECB has been buying up bonds in Europe. Few understand the high level of risk they have taken on.

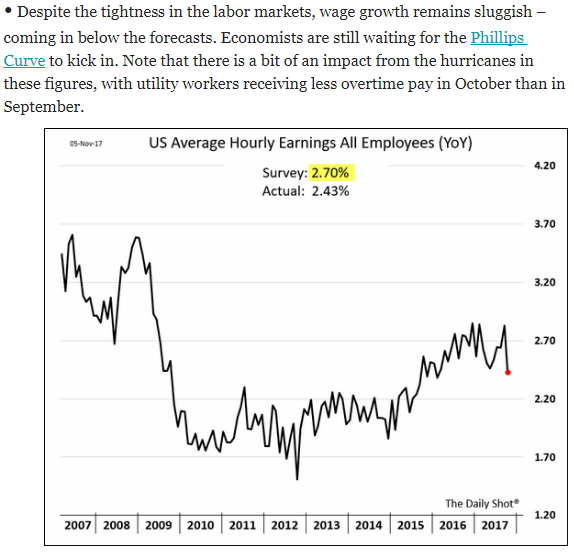

I’ve written about the Fed’s unyielding conviction in the Phillips Curve. They believe that low unemployment will lead to higher wages and higher inflation. This next chart shows that correlation is not working.

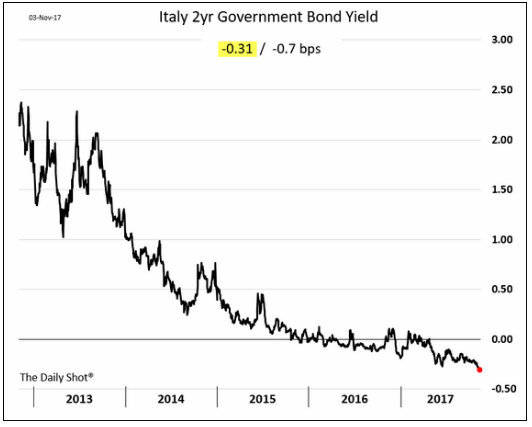

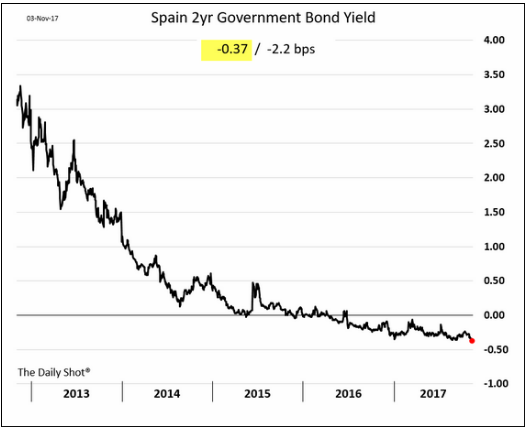

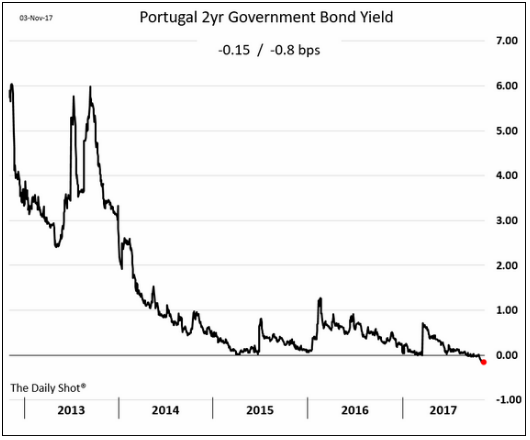

Other yield comparisons…

-0.31% in Italy, -0.37% in Spain and -0.15% in Portugal. All negative yields.

Again, thanks to the ECB bond buying program. Come on folks, this is crazy. The biggest bubble of all bubbles is in the bond market. If inflation kicks in and/or if default rates spike, the bubble will pop. A sovereign debt crisis lies ahead.

In the “what you can do” category. Think about your bond allocations differently. We’ve seen managers put tactical risk-managed ETF strategies in place of fixed income. There are also tactical risk-managed fixed income strategies. I like both ideas. Also, the Zweig Bond Model I post each week in Trade Signals has a good history and worth review/consideration.

Let’s next take a quick look at the High Yield Junk Bond Market. It’s important.

Are High-Yield Bonds the Canary in the Coal Mine?

My friend, Chris Dieterich, from the WSJ wrote this yesterday morning:

Keep your eye on junk bonds.

An improving global economy and ever-present demand for income has supported high-yield bonds all year. Valuations became stretched, but investors held their noses and bought them anyway, accepting some of the smallest rewards for owning risky debts in a decade because, well, what’s the alternative?

But junk-bond indexes have hit a rough patch, even as the major U.S. stock market benchmarks have continued to grind higher. Take the $19 billion iShares iBoxx $ High Yield Corporate Bond ETF, which is down 1.4% over the past two weeks. Wednesday’s drop, 0.4%, was its worst in over a month and cut the price of the ETF, which trades under the ticker HYG, to the lowest since August.

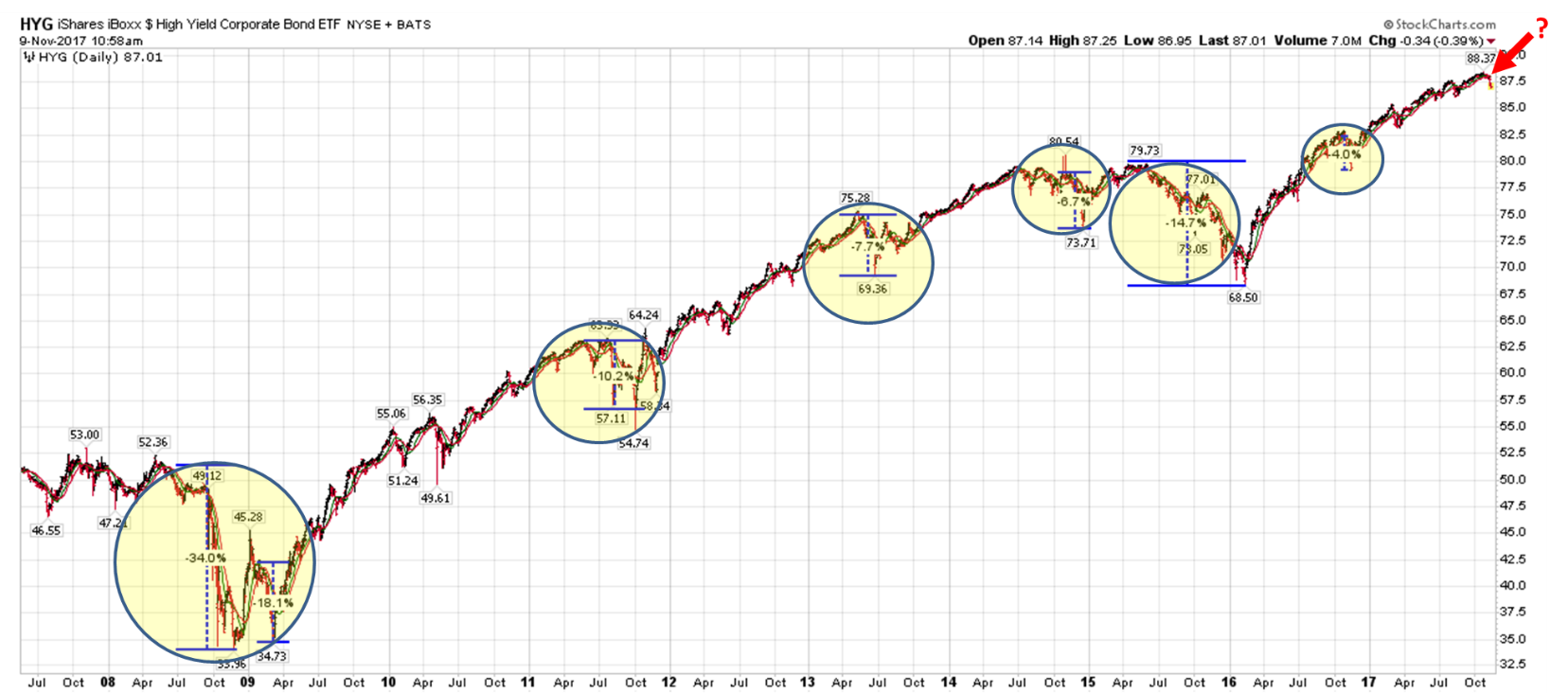

HY Chart 1:

- There have been several whipsaws in the last year (yellow circles).

- Current down trend marked by red arrow.

HY Chart 2:

- This is a longer-term look at HY.

- Best to avoid the big declines – this is where trend following can help.

- Note the large decline in 2008 of -34% and the early 2009 decline of -18%.

- A few bumps since in 2013 and 2015, but new highs since.

HY Chart 3:

Concluding thoughts:

- Yields in 2008 pre-correction touched 7.5%. Last recession is highlighted in grey.

- In late 2008, prices crashed and yields shot up to 23%.

- The current yield is 5.7%.

- Today, credit quality and investor protection (bond covenants) has never been worse.

- We will see record defaults in the next recession.

- I’m looking for yields north of 25%.

Continue to follow the trend. There may be a few whipsaws along the way, but getting to that opportunity in sound shape is the goal.

I’ve been trend trading HY since the early 1990s. I’ve seen three outstanding buying opportunities. The best opportunities came in crisis. I believe that the opportunity that will present in the next recession will be epic.

Keep the trend in the HY space on your radar. It almost always leads equities.

One last chart and we’ll call it a day:

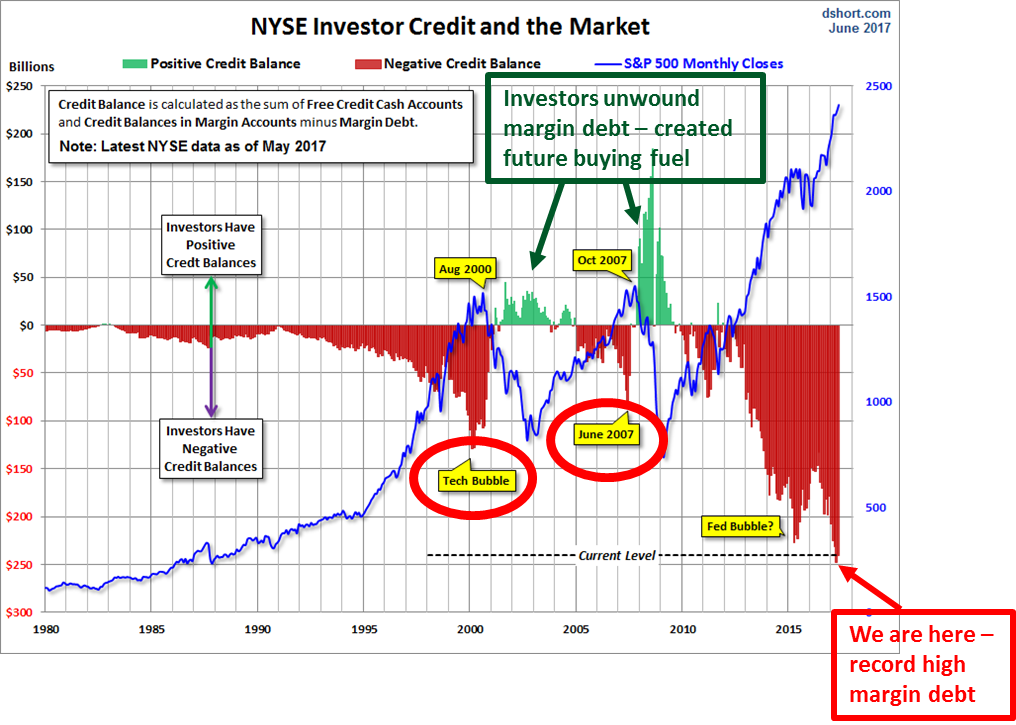

Margin Debt:

- The system has never been more leveraged.

- Just saying… be careful.

Source: dshort.com

Risk is present. The system is loaded with risk, yet we could continue higher. The NDR CMG U.S. Large Cap Long/Flat Index is up over 15% year-to-date. It has helped us keep our equity exposure invested despite my fundamental risk concerns. Find something you can get comfortable with in a way that gives you complete conviction to follow. Consider letting the weight of market evidence help guide your positioning — when to de-risk and when to re-risk back up.

Trade Signals — Inflation Signal

S&P 500 Index — 2,594 (11-8-2017)

Notable this week:

The biggest bubble of all-time bubbles, I believe, is in the bond market. What trips the switch will be rising inflation and, in turn, rising interest rates. So inflation is on “On My Radar” and I’m sure it’s “On Your Radar” as well.

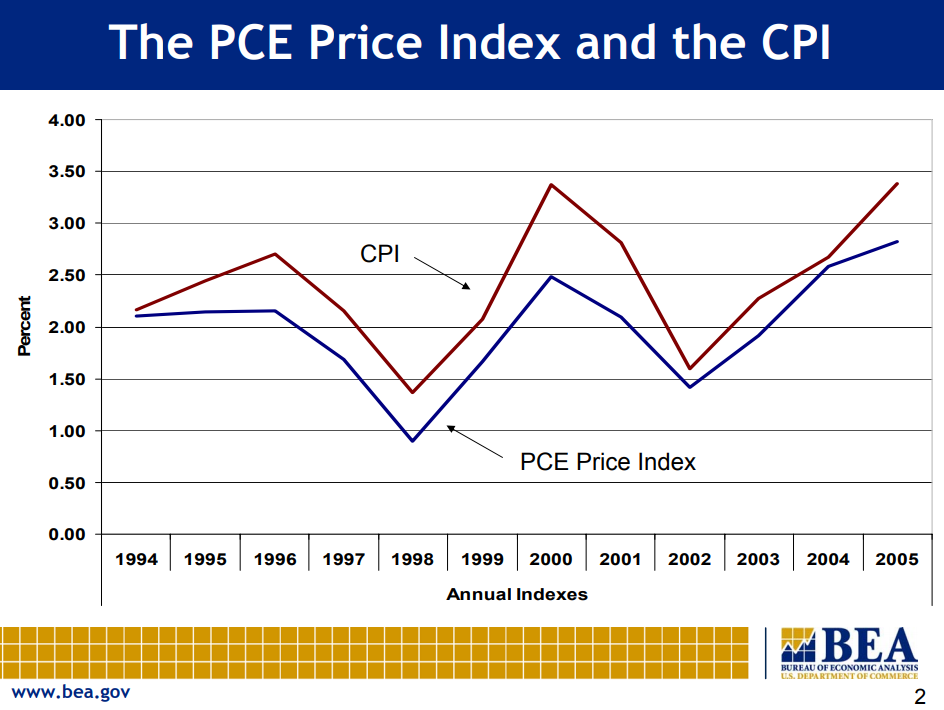

In last week’s On My Radar, I wrote about the PCE Price Index. That is the Fed’s go-to “preferred” inflation measure. The official switch from CPI to PCE occurred in 2000 when the FOMC stopped publishing CPI forecasts and began to frame its inflation projections in terms of the PCE Price Index. The findings were that the PCE has several advantages over the CPI, including (1) the changing composition of spending that is more consistent with actual consumer behavior; (2) the weights, which are based on a more comprehensive measure of expenditure; and (3) the fact that PCE data can be revised to account for newly-available information and improved measurement techniques.

Bottom line is that PCE and CPI track each other closely with PCE tending to come in lower than CPI. Here is a look at the trend from 1994-2005.

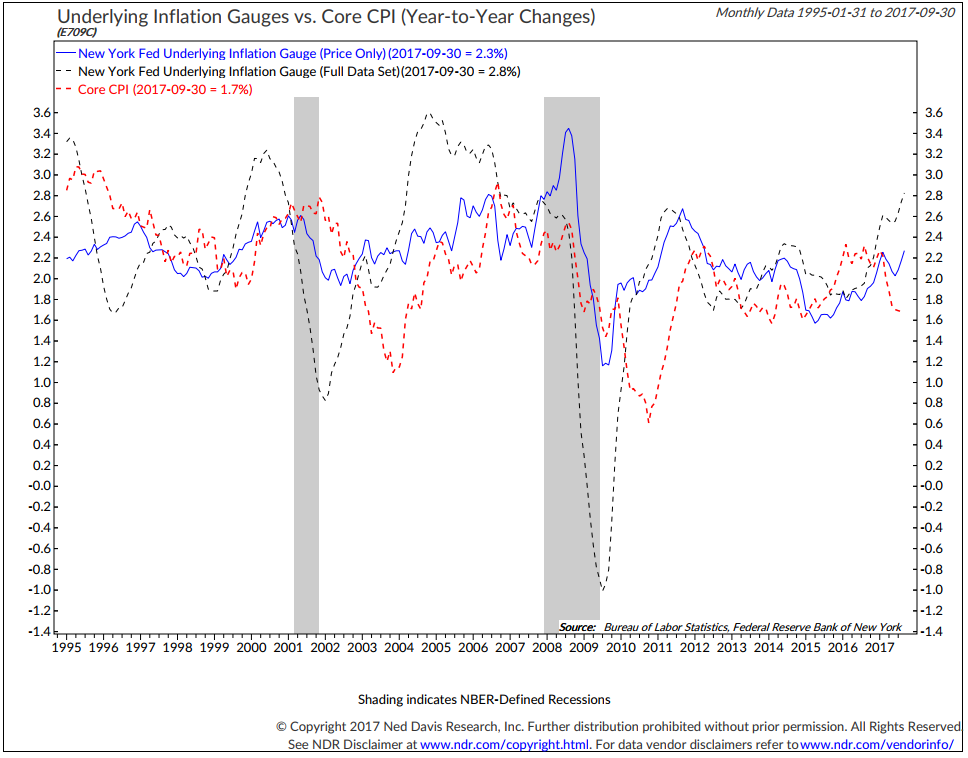

Next is a chart I’m watching on inflation. Note how the dotted red line (Core CPI) follows the dotted black line (NY Fed Underlying Inflation Gauge). You can see that the black line tends to lead and the red line follows. Point is, the Underlying Inflation Gauge is rising (as is the blue line) and the Core CPI will likely follow higher.

Total U.S. nonfinancial debt is at $47.9 trillion. That’s 249% of GDP (6-30-17 GDP was $19.2 trillion). If rates rise 1%, that raises the annual debt service costs by $479 billion. No small number. This is just in the U.S. Debt is the issue – globally. It will be rising interest rates that trips the switch.

Inflation? Keep watch. Fundamentally, I believe one more recession is around the corner and rising inflation provides cover for a Fed looking to get the Federal Funds rate to 3%. I’m expecting a rate increase in December and perhaps one or two more next year. I believe their tightening drives will drive us into recession. If so, rates will likely turn lower; thus, we may have one more decline to test the lows before rates ultimately move higher. Deflation remains the predominant force.

While I have that said fundamental view, I trade based on trend evidence and have far more faith in what the trend evidence is telling us. Right now, the Zweig Bond Model (trend model) signal remains bullish trend for bonds. Inflation is inching higher. Let’s keep watch on inflation.

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note

It’s a cold few days here in the northeast. It’s time to put the outdoor furniture away. I’m sure the boys can’t wait to help. Right. We’ll put the fire pit out and load some logs inside. I see a warm indoor fire with a cold IPA in hand with Susan tonight.

Tomorrow morning I’m heading out early to drive to NYC. Kyle is touring NYU today and I’m meeting up with him and daughter Brianna to tour Julliard tomorrow. Talk about two stretch schools… I’m really looking forward to seeing what the Julliard campus is like. Two more schools to tour early next week. We fly to Chicago on Monday.

Business follows in St. Louis just after Thanksgiving and then Susan and I are heading to Mexico for a few days in early December. Utah follows just prior to Christmas with a few meetings and some time at Snowbird. Family time and some fun in my near future. Somehow I’m convincing myself I’m due. Frankly, I really need to clear my head. It has been a busy year and while overall I feel pleased, there is so much more to accomplish.

My wish for you is to find a great book and some downtime with those you love most. And if you have a book recommendation, send me a note.

Finally, can I ask you a favor, if you know someone you feel may benefit from On My Radar, please send them a copy. I believe we are going to have another major market dislocation within a year or two and I hope to help as many people as I can. We need to not get run over on our way to the next buying opportunity. There are things we can do. I want to get the “participate and protect” message out to as many people as I can. The subscription link is below… Thank you – it’s appreciated!

Have a great weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group