As expected, nonfarm payrolls rebounded from hurricane-related effects. The unemployment rate edged lower, but that may have been noise. Leisure and hospitality was the sector most affected by Hurricane Irma, which might explain the choppiness in average hourly earnings (up 0.5% in September, flat in October). Looking through the noise, the job market data are consistent with a further increase in short-term interest rates, most likely at the December policy meeting.

Click here to enlarge

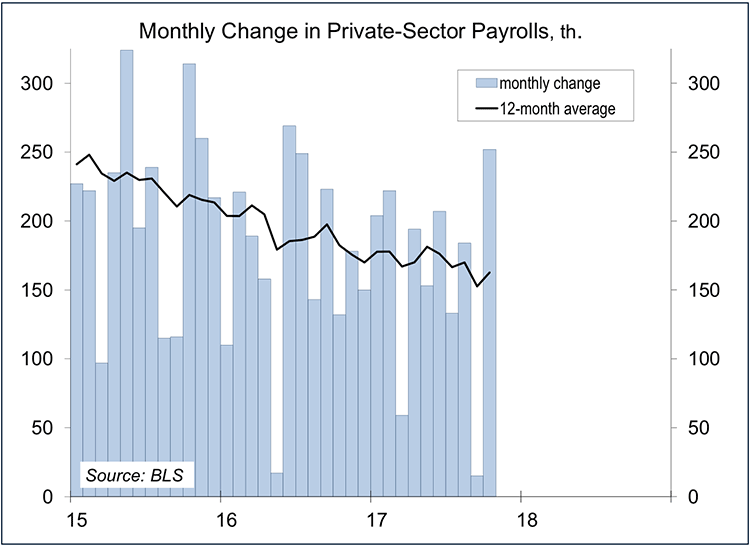

Prior to seasonal adjustment, nonfarm payrolls rose by 1.042 million in October, vs. 885,000 a year ago. Leisure and hospitality fell by 126,000 (vs. 219,000 in October 2016). This supports the view that Hurricane Irma pulled forward some of the seasonal job losses (mostly in restaurants) into September. Seasonally adjusted, private-sector payrolls averaged a 150,000 gain over the last three months (vs. 171,000 in the first seven months of 2017 and a +170,000 average for all of 2016). Payroll growth ought to slow as the job market tightens.

Click here to enlarge

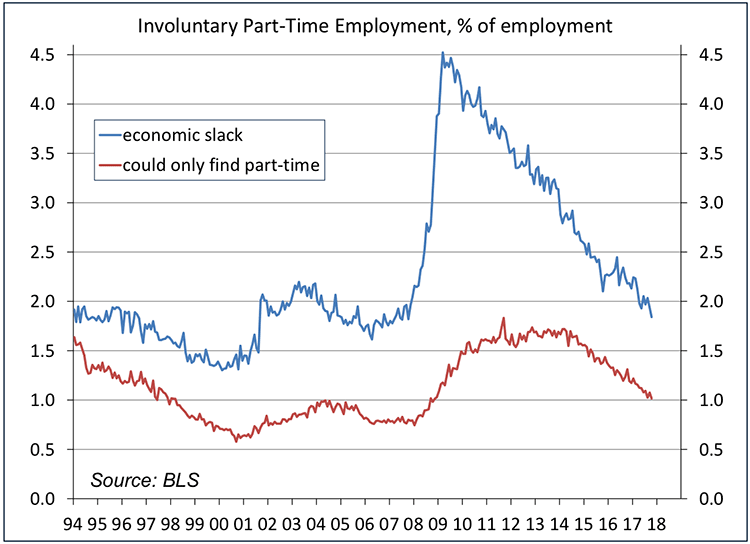

The Affordable Care Act was supposed to push workers from full-time to part-time. In the household survey, the Bureau of Labor Statistics asks part-time workers why they are working part-time. Most work part-time because they choose to (this could be an older worker supplementing retirement income, or someone who has to care for a sick loved one, etc.). Involuntary part-time is divided into those who are part-time due to economic conditions (not enough work) and those that took part-time because that was the only thing the firm offered. The share of non-economic part-time was rising before the ACA was passed and has been declining since it went into effect.

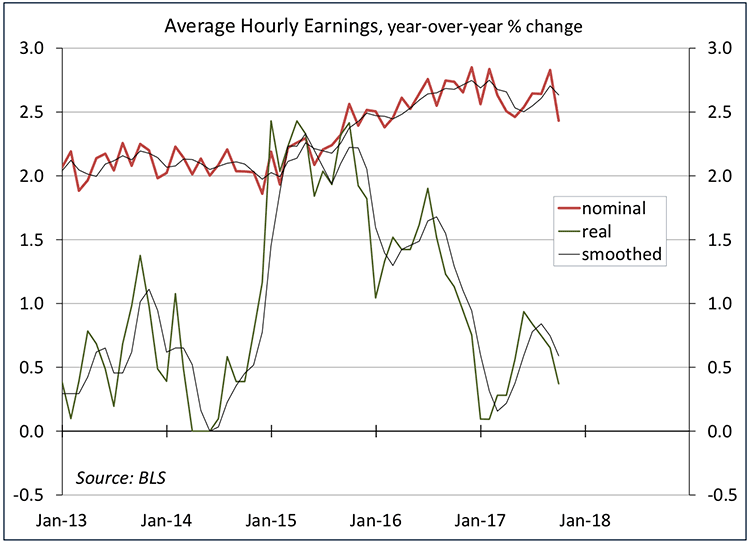

Tighter job market conditions should lead to faster wage growth. Average hourly earnings is a quirky measure. Faster job growth in lower-paying industries reduced the overall average. Job losses in September were concentrated in leisure and hospitality (AHE = $15.55, vs. an overall average of $26.54). The decline in restaurant jobs likely pushed overall wages up in September, with the effect unwinding in October. The underlying wage trend remains moderate.

Click here to enlarge

The Fed will get one more employment report before the December 12-13 policy meeting (although policymakers are not going to react to any one particular piece of data). The wording of the November 1 policy statement suggests that another 25 basis point hike is more likely than not. If approved by the Senate (and there’s no reason to expect he wouldn’t be), Jerome Powell, President Trump’s selection to replace Janet Yellen, will take over on February 4. Not much is expected to change. However, Powell, who is not an economist, is expected to rely much more on advice given to him. The Fed is a strong institution, so this shouldn’t be a problem. However, President Trump will likely fill other vacancies on the Fed’s Board of Governors. While some Republicans have criticized the Yellen Fed for keeping interest rates low, they are more likely to welcome low rates as long as they are in power.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James