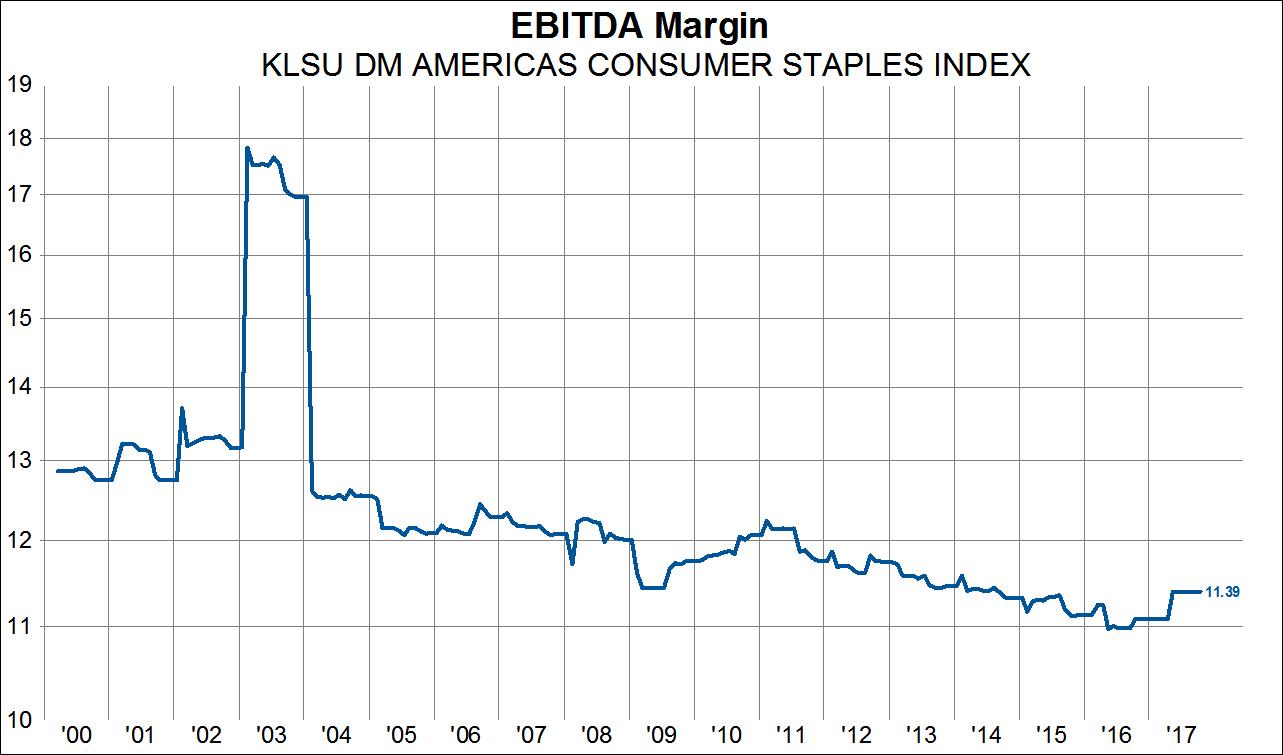

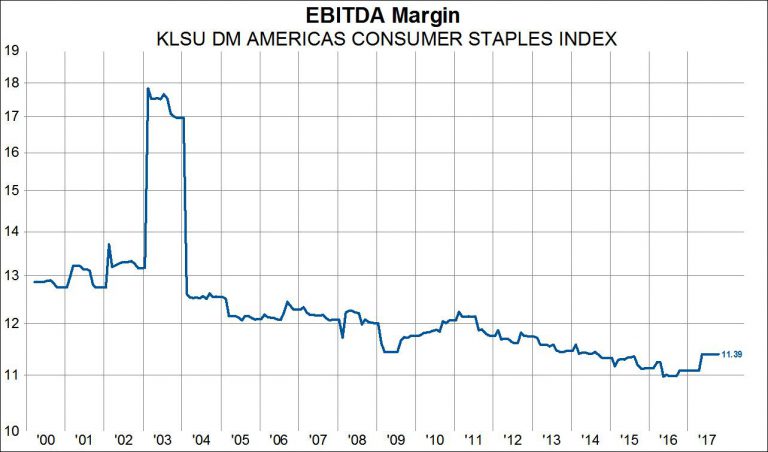

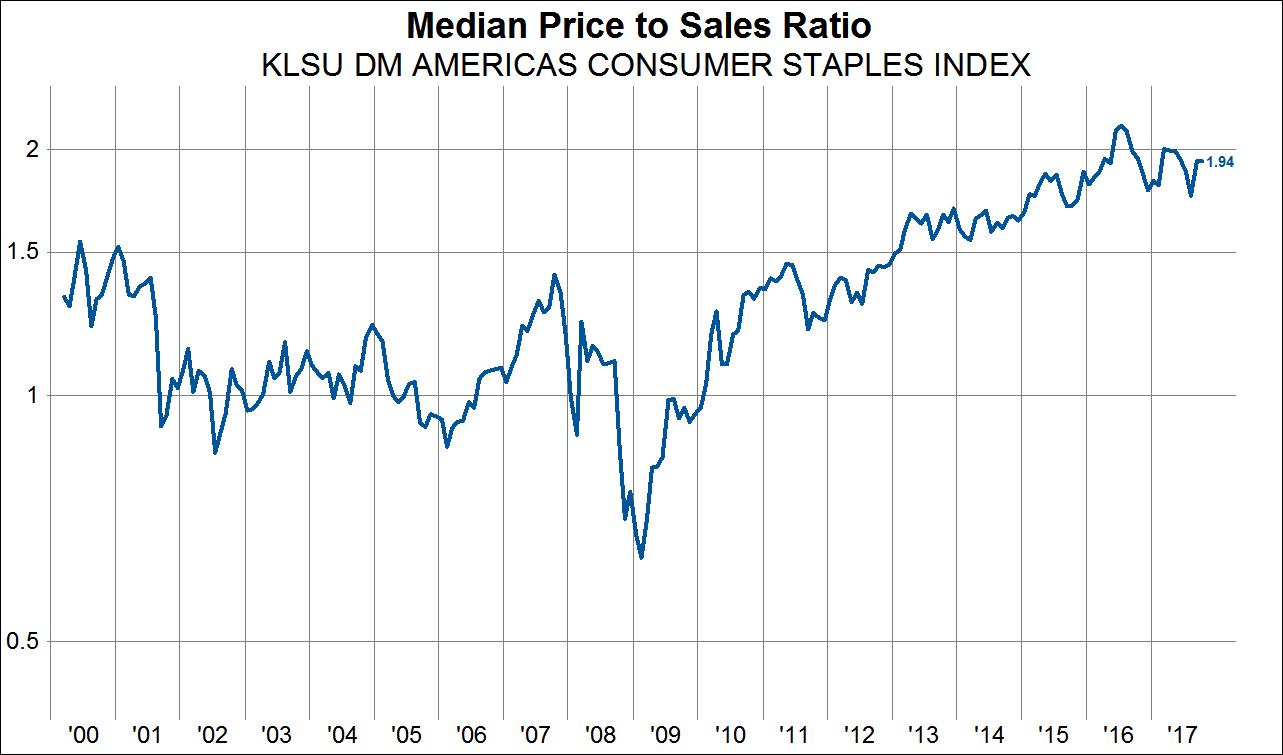

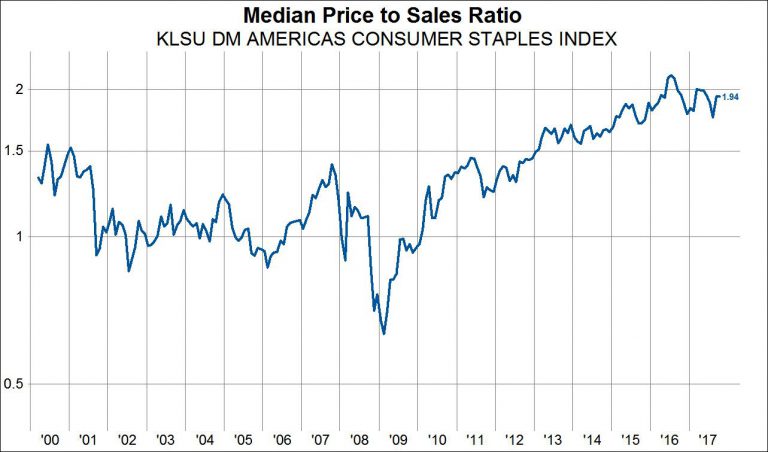

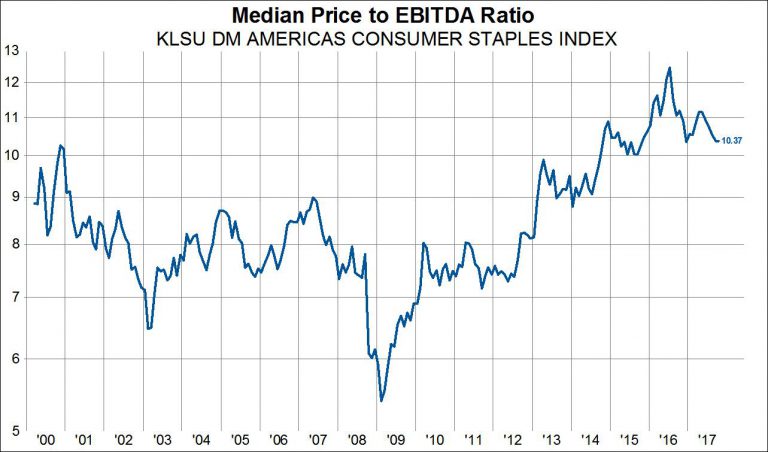

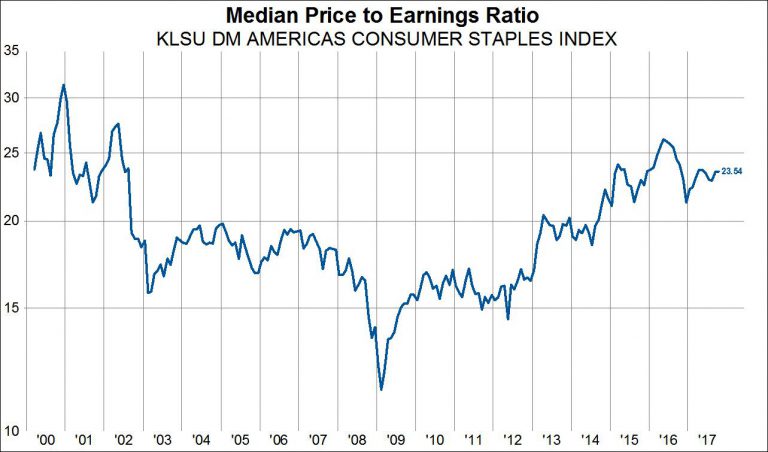

The Consumer Staples sector is often viewed as a safe haven; a sector that, because of its inherent cash flow stability, market participants can turn to as a place of refuge when things get shaky. Yet, persistent fundamental decline among North American Staples companies may well be throwing a wrench in these companies’ abilities to weather a broad market downturn. In this post we’ll briefly touch on financial statement and valuation indicators that suggest Staples may not be as risk averse as they used to be.

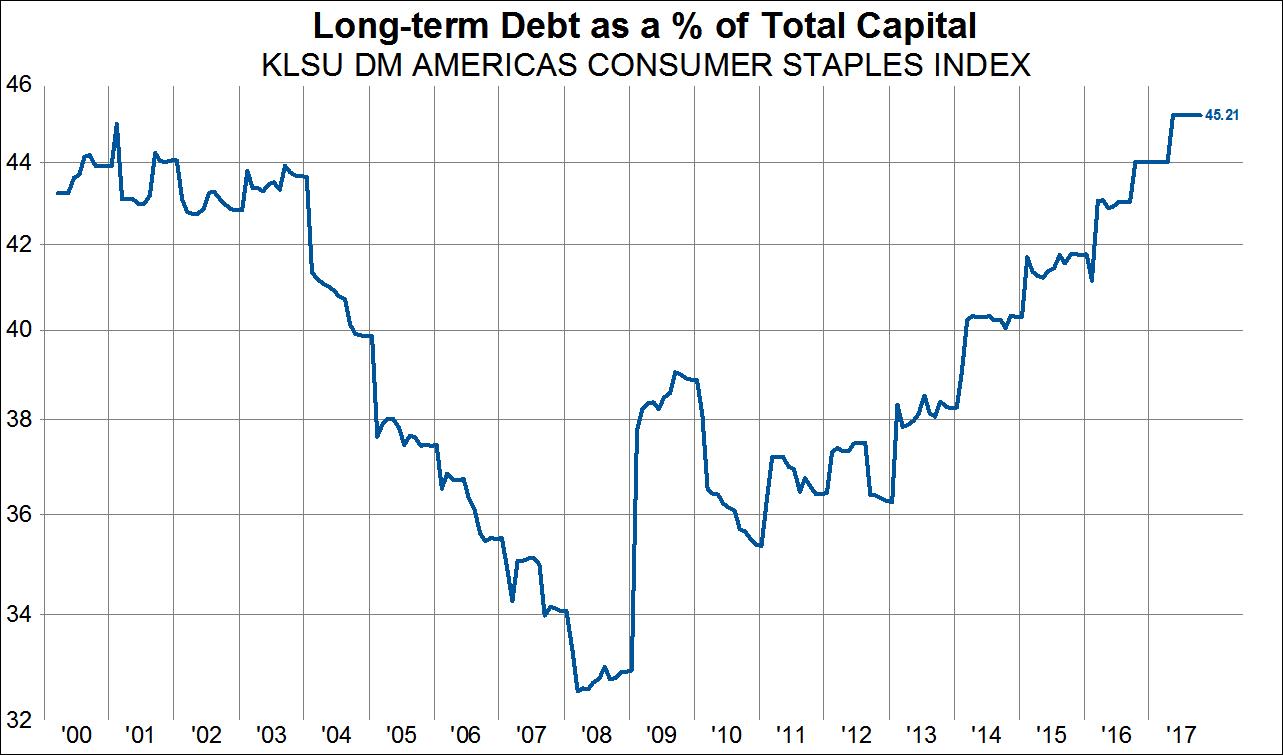

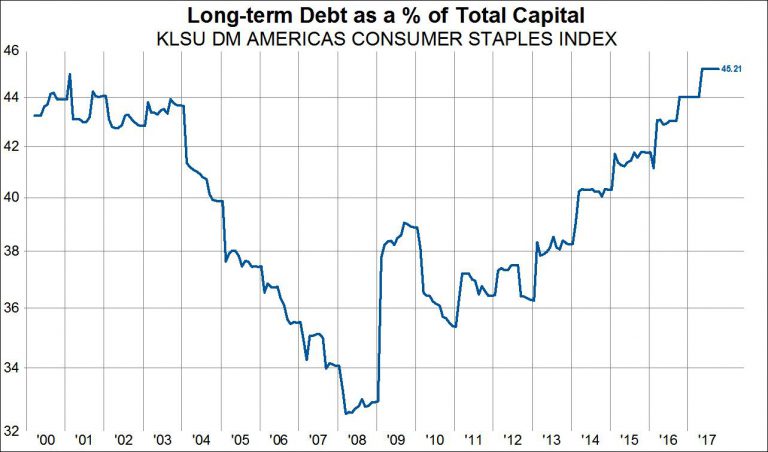

One highly important quality factor is long-term debt as a percent of capital. As the first chart below demonstrates, North American Staples companies have been loading up on debt year after year for the entirety of this recovery. Long-term debt as a percent of capital is now at levels not seen in at least 18 years.

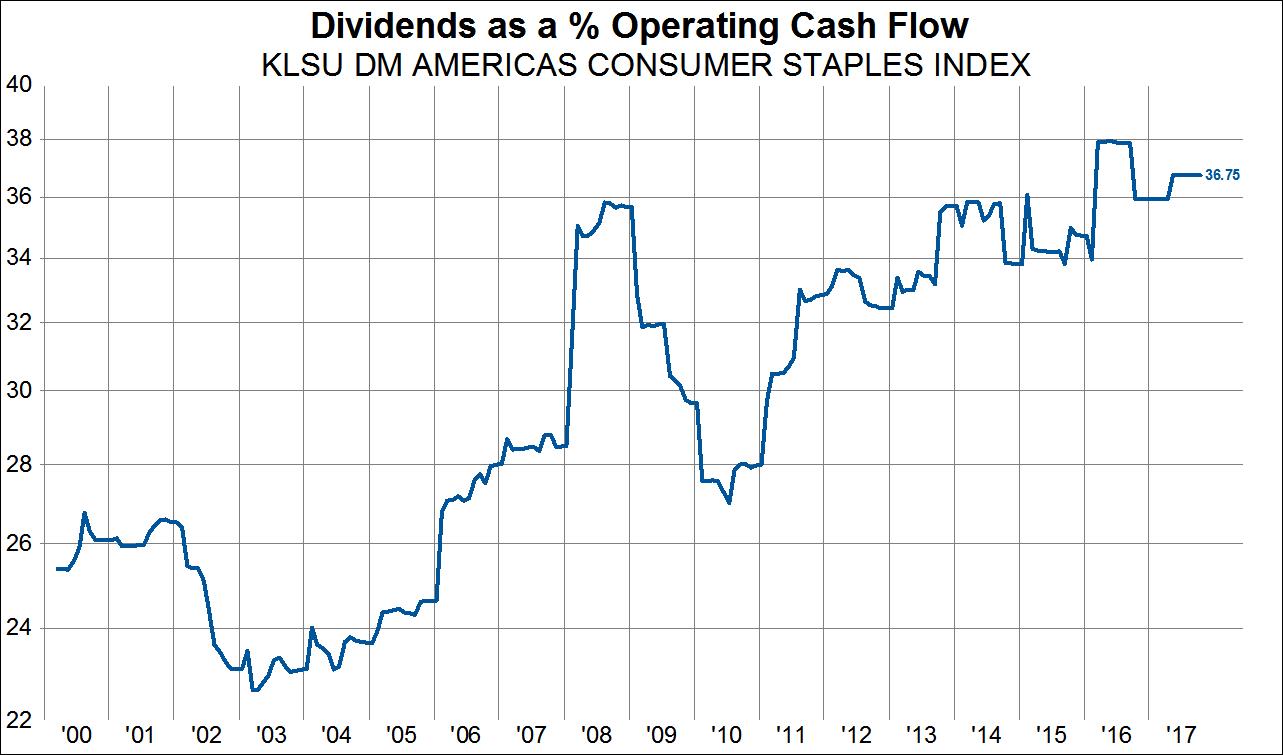

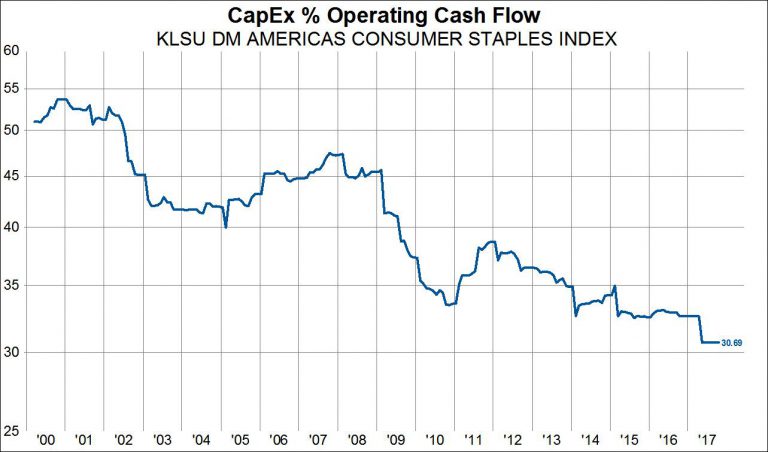

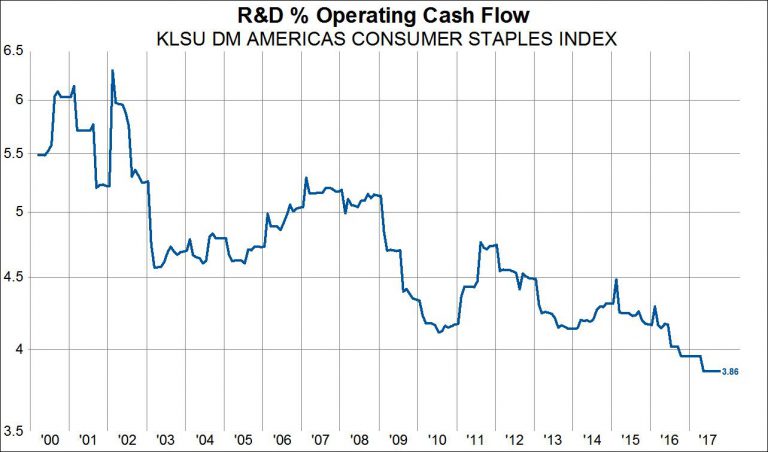

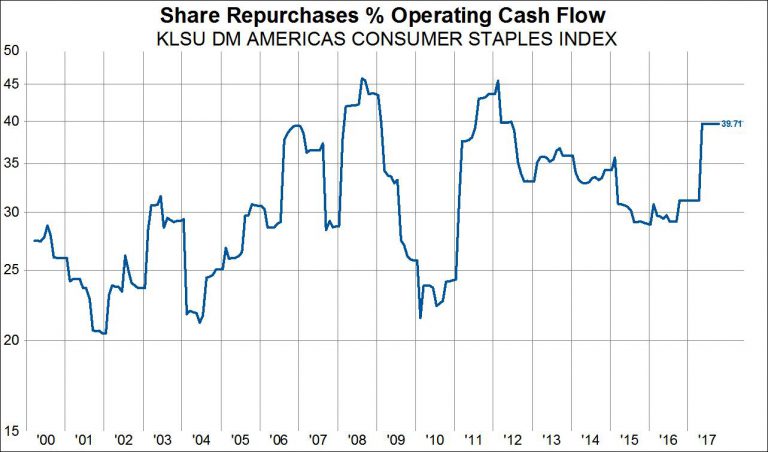

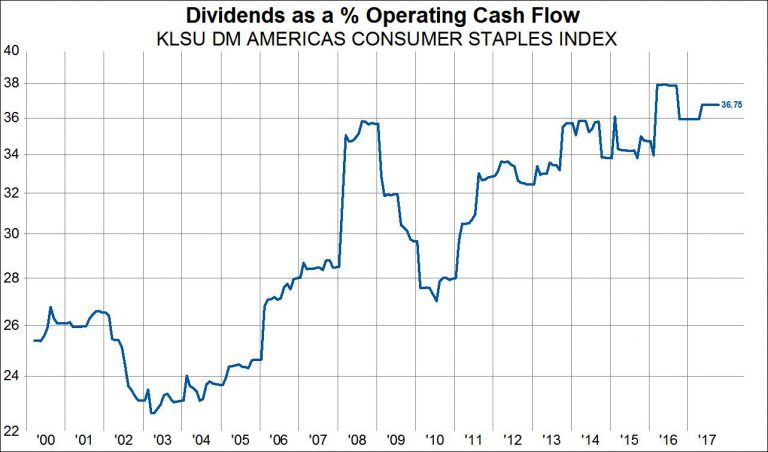

This begs the question of what are these companies doing with all that debt? The next four charts show capex, R&D, share repurchases, and dividends as a percent of operating cash flow, respectively. The trends are unmistakable. Capex and R&D investments have nearly halved since 2000 and have been cut especially hard since 2008 while share repurchases are basically range bound at a high level and dividends have been on an unabated uptrend. Together, capex + R&D + share buybacks + dividends = 111% of operating cash flow. Debt must be issued to finance that which operating cash flow cannot fund, and this after slashing reinvestment in the capital stock. This is to say, North American Staples companies are issuing debt and eating themselves from the inside out to finance dividends and maintain stock buy backs.