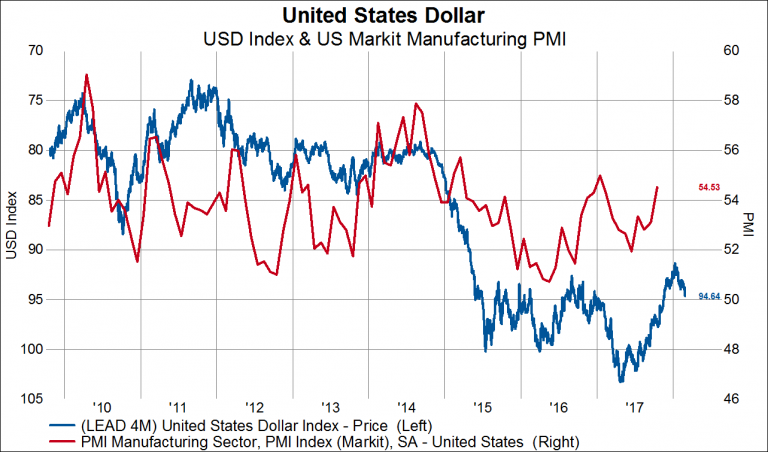

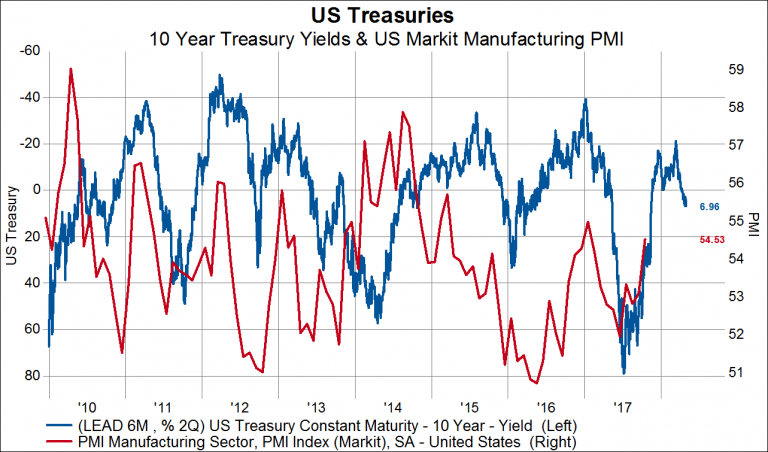

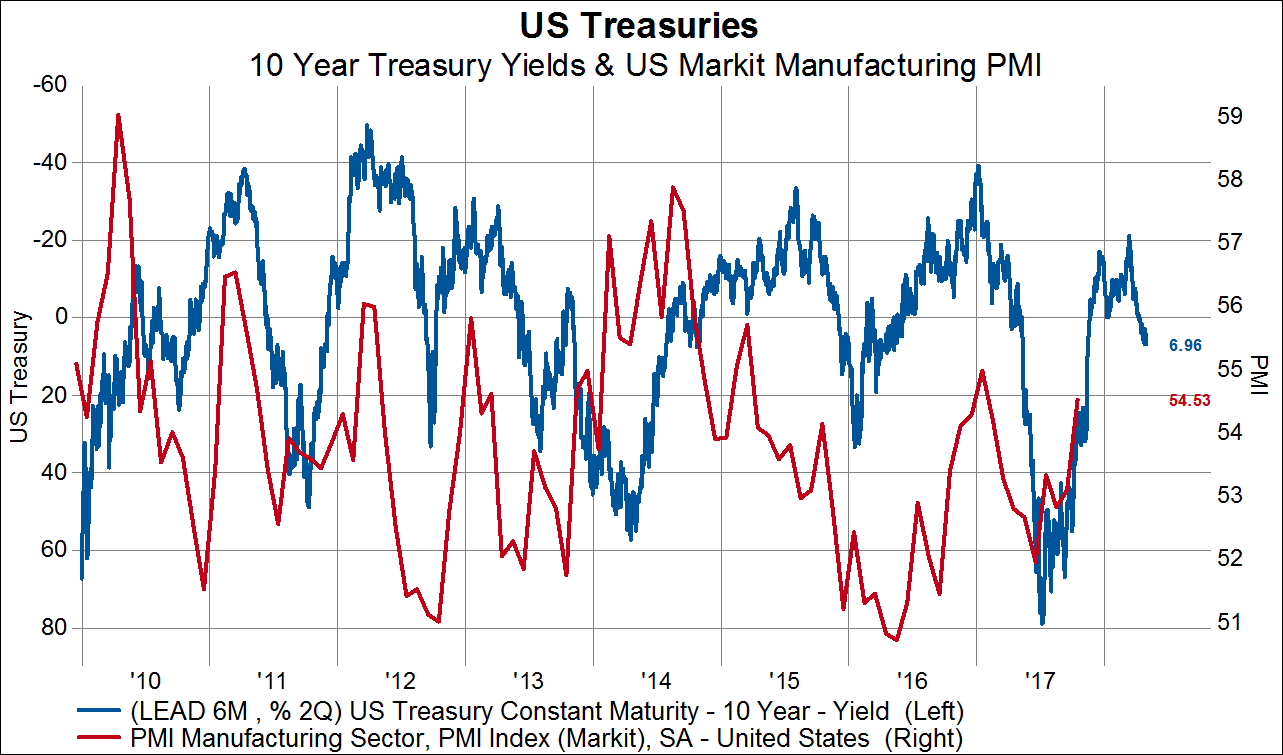

Several months ago we wrote that looser financial conditions should support economic data and stocks through year end. So far so good. Since then economic indicators such as the Markit manufacturing PMI have continued to chug higher and US stocks are up about 6%. With the economy seemingly on strong footing and and stocks hitting on all cylinders, its easy to extrapolate recent history well into the future, but we caution against doing so. Much of the improvement we’ve seen in business sentiment has been due to the lagged effects of the weaker USD and the large move lower in 10-year treasury rates we experienced from the beginning of the year through the summer. Whether semi-permanent or not, both of those metrics of financial conditions have turned the corner, suggesting that we may not be able to eek much more out of this late cycle growth spurt, all else equal. Indeed, the same models we used to suggest the econ data (as narrowly measured by the Markit manufacturing PMI) would improve through year end now point to a peaking of the PMI in December. Of course, the recent strength of the USD and the backup in rates could be transitory, and tax reform could prove to be a boon to economic growth, but the realities of 2% growth may re-exert themselves in the new year.