“Collectively, the Fed, European Central Bank and Bank of Japan own one-third of the global bond market. “

– Mary Ellen Stanek, CFA

Managing Director and Director of Asset Management, Robert W. Baird & Co.,

Chief Investment Officer, Baird Advisors

“Don’t Fight the Tape or the Fed!” It is one of investing’s “golden” rules and is perhaps never more true than it is today. The Fed, ECB and BoJ own one-third of the global bond market. One-third! Pause, put finger to chin and wrap your mind around that one. Print and use that money to buy bonds — tens of trillions of dollars, yen and Euros worth of bonds. Liquidity created out of thin air. If I buy bonds from you, where are you going to reinvest your proceeds?

The massive amount of global quantitative easing and central bank buying has driven yields to 5,000-year lows. Well, technically we are off those lows but still low, unattractive and negative in many places. Central banks have inflated the global fixed income markets and equity markets. Don’t fight the big guy has gained new meaning. Good news for us but now what?

Game plan: Keep our eyes on the central bankers, keep our eyes on the market’s trend evidence and keep our eyes on the recession indicator signals. Every Fed tightening period has ultimately landed us in recession. Bad stuff happens to equity markets and high yield corporate bonds in recession. This week, let’s take a look at several of my favorite recession watch indicators. Objective: avoid pain.

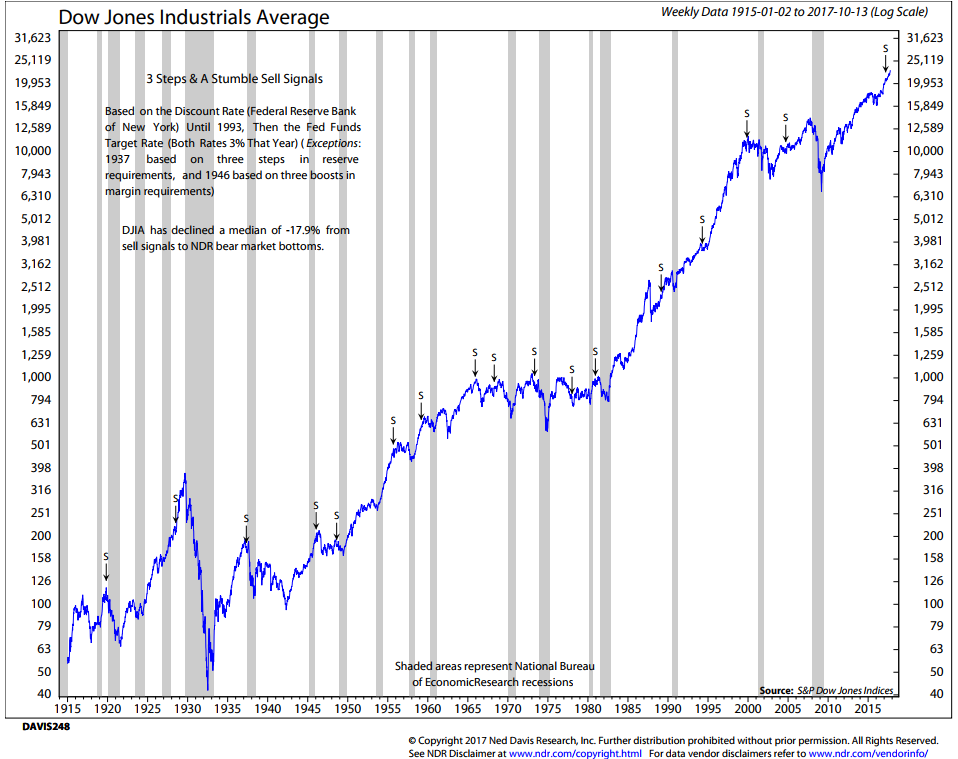

Three Steps and a Stumble – Don’t Fight the Tape or the Fed

You may have heard the phrase, “three steps and a stumble.” It means that when the Fed raises rates three times in a row, a market stumble is likely to follow.

Following is a visual look at that rule:

- The S’s in the chart mark the third consecutive rate hike

- Note how the hikes almost always precede a new recession

- Note the current signal is a sell or “S” and

- Note the DJIA has declined a median of 17.9% from sell signals to bear market bottoms

Source: Ned Davis Research

Minus 17.9% is not too tough to deal with. We would need a return of approximately 20% to get back to even. That may not take too long a period of time. It’s the -40% and -50% that kills the compounding. While I like the three steps and stumble rule, it’s not my go to.

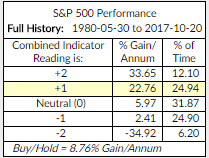

I favor the Tape (which means trend) and the Fed combined in one indicator. Ned Davis Research has a process I track and post weekly for you in Trade Signalstitled, Don’t Fight the Tape or the Fed. Frankly, it’s in the weekly post so I remind myself to look at it often.

The indicators used are a combination of NDR’s Big Mo Multi-Cap Tape Composite indicator to determine the general technical health on the broad equity market (trend) and the 10-week Treasury Yield percentage. Big Mo measures the percentage of the component indicators that are currently giving bullish signals for the S&P 500 Index. Bullish readings score +1, neutral readings 0 and bearish readings -1.

In short, it provides a single summary reading of the U.S. stock market’s technical health based on historical analysis of many trend and momentum indicators. As for the Fed, instead of looking directly at the Fed rate hike moves, they look at the impact of Fed activity on the 10-week Treasury Yield and specifically they measure current yields versus a 70-week linear regression moving average trend line. Historically, the S&P 500 has produced larger gains when yields are below the line (falling) versus above it (rising).

As an economic control tool, the Fed uses the interest rate (via raising and lowering the Fed Funds rate) to drive expansion (lowering rates) and to cool the economy if it gets too hot (raising rates).

The NDR Don’t Fight the Tape or the Fed model produces a score that ranges from -2 (both indicators bearish) to 2 (both indicators bullish). When these two indicators (Tape and Fed) are used in conjunction, they produce a historically strong market indicator.

Here’s where we are today (yellow highlight in chart) and how you look at the data:

- Currently Big Mo is neutral (0) and the 10-week Treasury Yield is lower than its 70-week moving average (+1).

- So the combined score is +1. The score is highlighted in yellow.

- Note the percentage gain per annum of 22.76% and note the % of time since 1980 the indicator has signaled +1.

- Note the percentage gain of -34.92% when the model scores -2.

Source: Ned Davis Research

You can see that the best returns come when the trend is positive and the Fed accommodative. The bad stuff happens when trend/momentum is negative and interest rates are rising.

Smooth sailing? While we sit at nosebleed valuation levels, grab some cotton to slow the bleed, trend evidence by this measure (as well as our NDR CMG U.S. Large Cap Long/Flat Index) remains moderately bullish. We may continue higher. Our other trend indicators (link through to Trade Signals below), along with Don’t Fight the Tape or the Fed, remain supportive of further advance.

On My Radar is about being aware of different macro and potentially systemic market and economic risks. And those risks are elevated because our current starting conditions (ultra-low interest rates and record high valuations) are not like they were in the spring of 2009. They are more like they were in late 1999 and 2007.

If we take a step back and look at the world from 30,000 feet, I believe what we should be thinking about is what the markets look like on the other side of QE (or quantitative tightening). A central bank that buys bonds and stocks does not care about the current price or valuation. Their motives are different than yours and mine.

Unwind? We must ask ourselves what happens when they stop and reverse course.

Recession watch is on my mind. From time to time, I like to share with you my favorite recession signal charts. Let’s do that again today. Additionally, you’ll also find a link to a short video by my friend, Grant Williams, and his partner, Raoul Pal, founders of Real Vision. It’s really good. Finally, I share a personal happy moment seated in seat 34B on the flight home from Dallas yesterday. The motivation for this week’s title, “Start Small, Grow Strong.” True for many things in life.

Grab that coffee and jump in. You’ll find it to be a quick read.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- Recessions by Decade

- The Point of Maximum Financial Opportunity

- Real Vision – The Edge of the Cliff

- Trade Signals – Don’t Fight the Tape or the Fed Still Bullish

- Personal Note – Start Small, Grow Tall

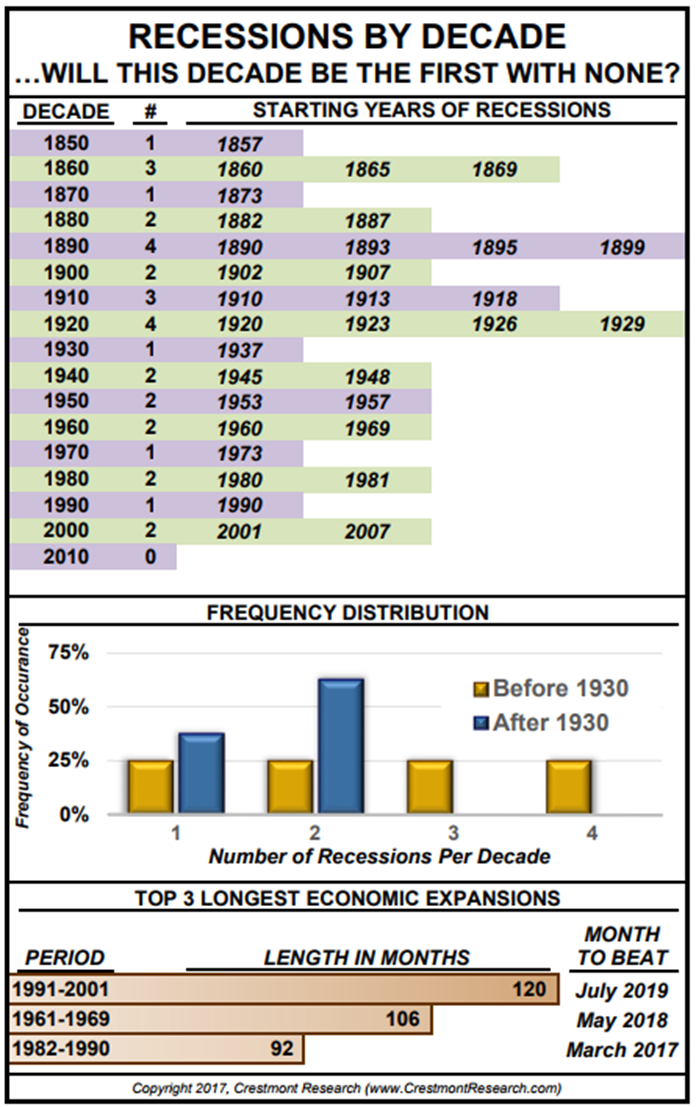

Recessions by Decade

Why my recession obsession? Because the average equity market decline is approximately 38%. The last two recessions both declined more than 50%. It takes a 100% subsequent return to recover from a -50%. The definition of recession is a decline in GDP in two successive quarters. That is only known in hindsight. So we must do our best to avoid them in advance.

You’ll see in Charts 1, 2 and 3 below that, barring an unforeseen shock, the economy will avoid recession this year.

Let’s first look at data that details the number of recessions by decade. There has never been a decade without recession. I personally believe we’ll see one in 2018. But no signal just yet… data dependent as they say.

Source: Crestmont Research

The problem with recessions is that it is when all the bad stuff in terms of your equity portfolio happen. I suspect the next recession could be worse. Why? In a word – debt.

Let’s look at my favorite indicators:

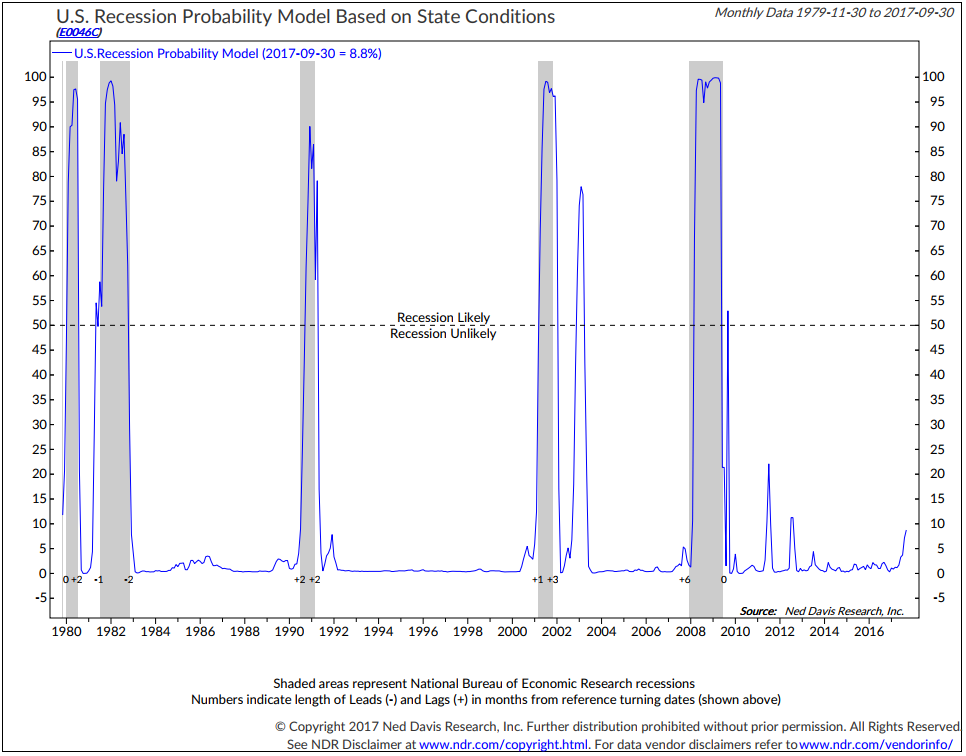

Chart 1: U.S. Recession Probability Model Showing Low 8.8% Risk of Recession

Here is how to read the chart:

- The individual state indexes combine nonfarm employment, average manufacturing hours worked, the unemployment rate, and real wages and salaries. As economic conditions deteriorate across a growing number of states, the estimated recession probability for the U.S. increases.

- When the blue line in the chart crosses above the dotted line at 50, recession is likely. Below 50 recession is unlikely (current signal is “recession is unlikely”).

- The +1 or +2 or +6 indicates the number of months the indicator lagged behind the actual recession state date.

- Note the advance warning the model has historically provided (not perfect but pretty good).

Source: Ned Davis Research

Generally, the stock market tops out about a year before a recession. So the market becomes a great recession signal indicator.

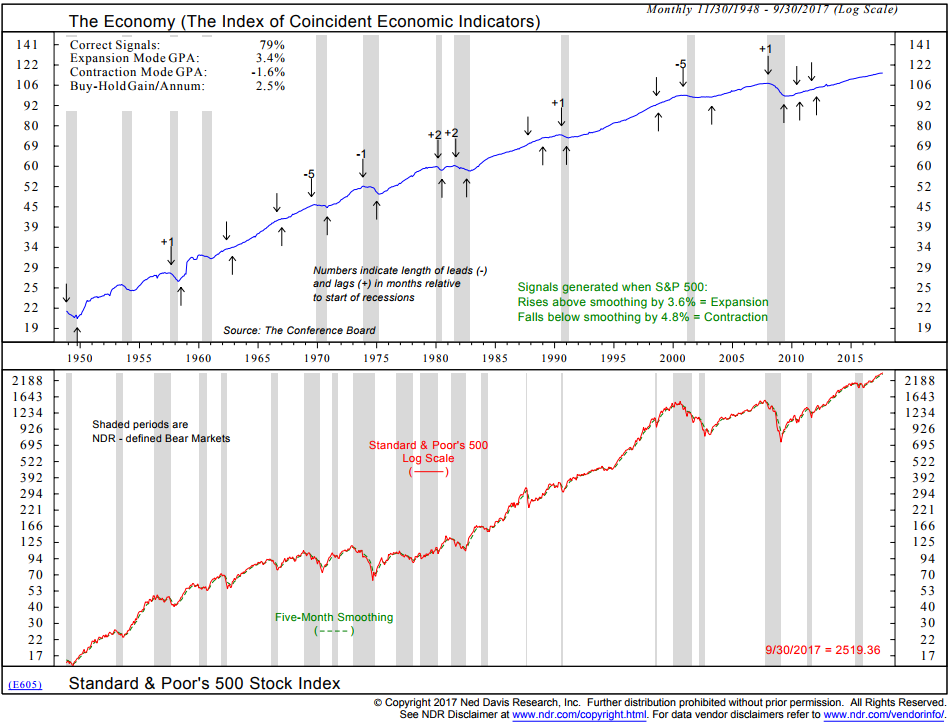

Chart 2: The S&P 500 Index vs. Its Five-Month Smoothed Moving Average

Here’s how to read the chart:

- The bottom section plots the S&P 500 Index (red line) against its Five-Month Smoothing (green line).

- Signals are generated when the S&P 500 Index rises above the smoothing by 3.6%. That signals expansion.

- When the S&P 500 Index falls below the smoothing by 4.8%, that signals contraction.

- The top section shows the up (expansion) and down (contraction) arrows.

- Think of stocks as a leading economic indicator (which they are).

- There are some false signals, but 79% of them have been correct.

- Note how close many of the signals happened near the start of recession (the minus sign shows how many months signals occurred before recession start and a plus shows how many months after a recession the signals occurred post actual recession start.

- Bottom line: No current sign of recession.

Source: Ned Davis Research

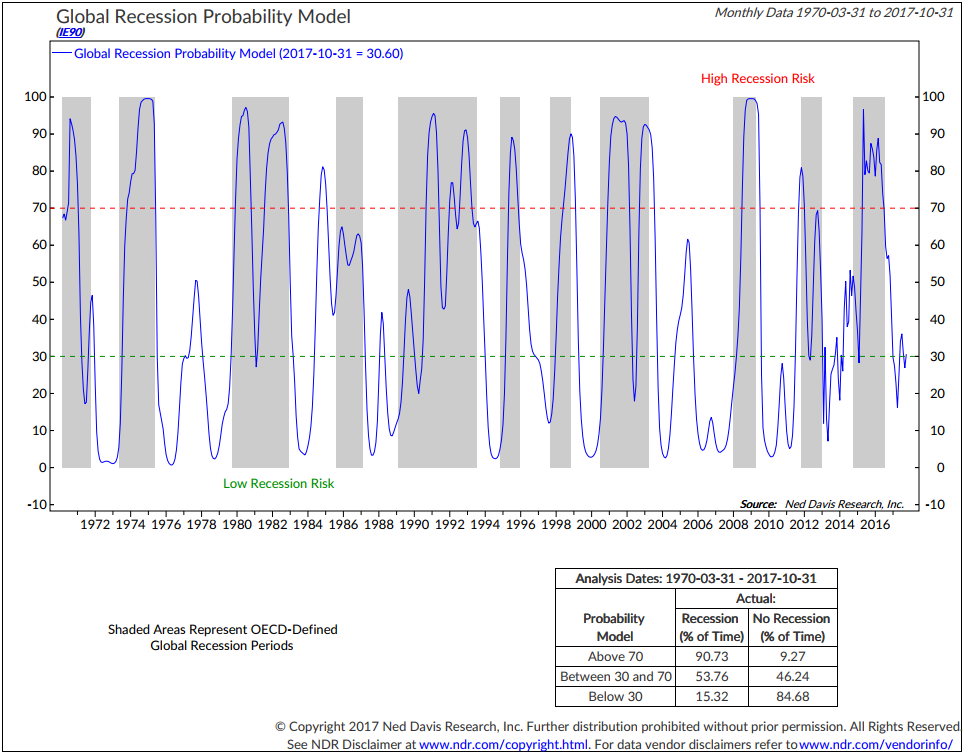

Chart 3: Global Recession Probability Model

Since most investors now invest globally and the global economy will certainly impact the U.S. domestic economy, I like to watch this next chart.

Here’s how to read it:

- Based on the Amplitude-Adjusted Composite Leading Indicators (CLIs) created by OECD for 35 countries, each CLI contains a wide range of economic indicators such as money supply, yield curve, building permits, consumer and business sentiment, share prices, and manufacturing production. There are usually five to ten indicators, which vary by type and weight, depending on the country, and are selected based on economic significance, cyclical behavior, and quality.

- The model uses a logistic regression method incorporating both the CLI level and trend data of all 35 countries to predict the likelihood of a global recession.

- A score above 70 indicates high recession risks while a score below 30 means low risks.

- The model is a forward-looking model using a two-month lead in the CLI data.

- The blue line in the chart tracks the model score.

- When the blue line is above 70 (dotted red line in the chart), there is a “High Recession Risk.”

- When the score is between 30 and 70 (as is the case currently), there is a moderate risk of global recession.

- When the score is below 30 (the dotted green line), there is a low risk of global recession.

- The current Global Recession Probability is 30.60%.

- The data box in the bottom right-hand side shows the levels and it shows the percentage of time since 1970 that recession has occurred based on the score.

- Bottom line: let’s call it a 30.60% chance of recession.

Source: Ned Davis Research

I was in Dallas the last few days at an advisor meeting. I’ve traded high yield since the early 1990s. I’ve seen three epic buying opportunities. I told the group number four is coming and it will be the biggest. Why? The quality of high yield junk bonds is the worst on record. All that cash looking for yield has enabled companies to issue debt on their terms… a kind of take it or leave it. Unsuspecting investors are going to get their clocks cleaned. At the 2008 great financial crisis low, high yield bonds were yielding 22%. That’s because prices of the bonds declined and defaults rose. I believe the next opportunity will be much greater.

I told the group about a piece I wrote in late 2008 entitled, “It’s So Bad It’s Good.” Expect a piece from me within the next few years titled, “It’s So Much Worse than Last Time, It’s Great.” Frankly, I was scared on that late 2008 buy signal. I suspect I’ll be equally scared again. Let’s you and I look forward to that opportunity. I believe we’ll get 30% yields. Note for now, our HY signal remains risk on.

On the way to that great opportunity lies some challenges. Last week I shared a chart with you forecasting 1% annualized returns for the coming ten years. John Hussman is forecasting negative returns. This is what he said this week:

At present, the most reliable measures of U.S. equity market valuation — the measures that are best-correlated with actual subsequent market returns in market cycles across history — are 2.75 times (or 175% above) their historical norms. Given that depressed interest rates are matched by commensurately low U.S. growth rates, little or none of this premium is actually “justified” by interest rates. Rather, the S&P 500 is likely to post negative total returns over the coming 10-12 year horizon, with a likely interim loss in excess of -60%. (Emphasis mine.)

I’m not looking at a market top today. I think we may go higher. But it’s late in the game. I’m forecasting a -50% to -70% decline. Everyone is loaded on the passive index same side of the trade. And 75% of the money is in the hands of pre-retirees and retirees. They can’t afford to take a hit. How will they behave in the next great market correction?

When you are late in a move and have high valuations, you should be taking less risk. This is a time to play more defense than offense and, importantly, to have a plan in place to manage your downside. Participate and protect.

Last thought on recession. One of the best indicators is an inverted yield curve. That’s when short-term rates are higher than long-term rates. Not the case today. So that’s good news.

Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at 617-279-4876. John’s email address is [email protected]. I am not compensated in any way by NDR. I’m just a big fan of their work.

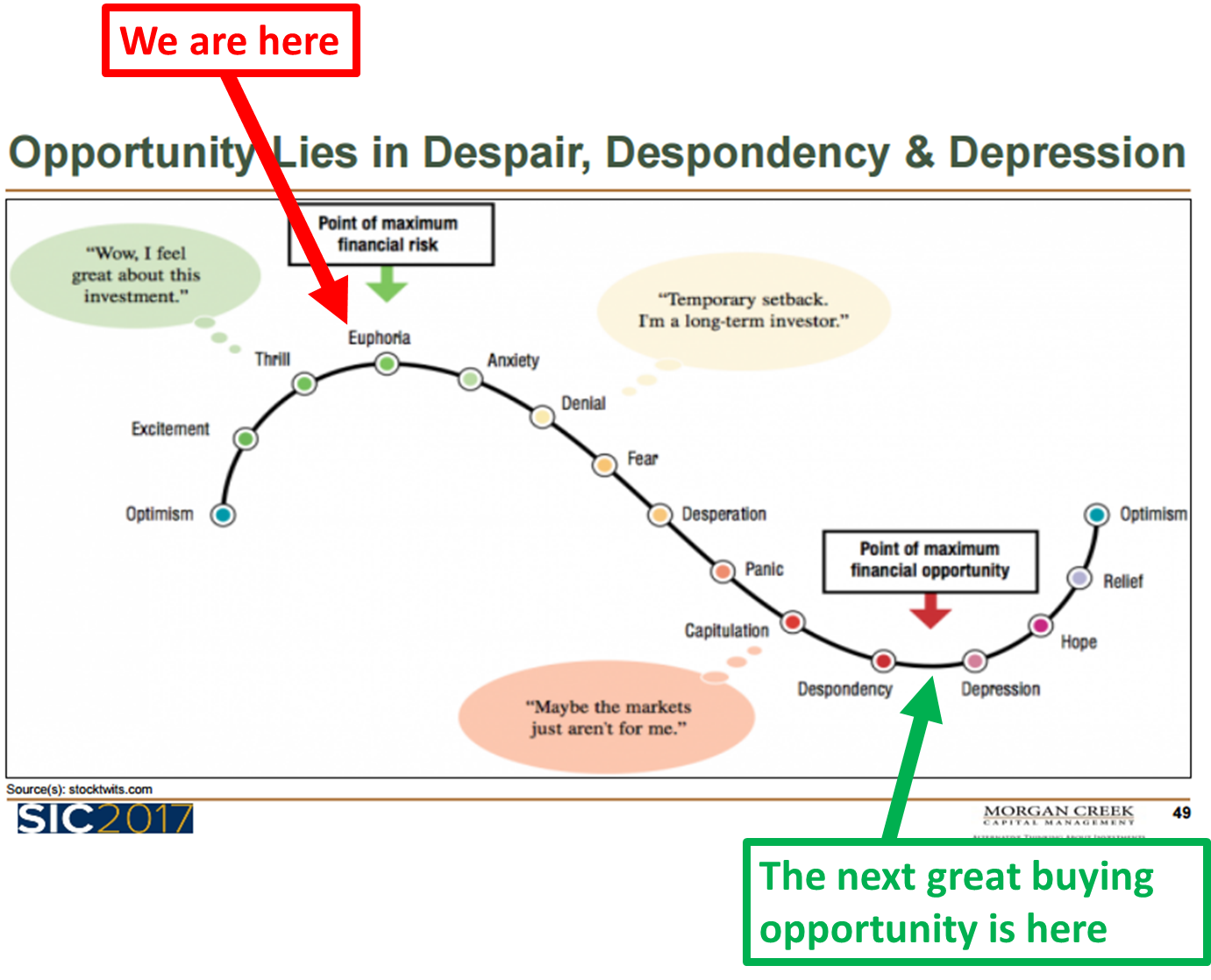

The Point of Maximum Financial Opportunity

Just for fun, let’s take a look at the next behavior chart. We are at a point of maximum financial risk. We will get to a point of maximum financial opportunity. Just remember that it feels safest when risk is greatest and it will feel scariest when risk is least.

Source: Morgan Creek Capital Management

Real Vision – The Edge of the Cliff

Grant Williams and Raoul Pal founded Real Vision on this idea:

After the crisis in 2008, people were left feeling betrayed because no one warned them what was about to happen. …We needed to give our audience access to the very smartest brains in finance.

It’s where we invite the world’s most successful investors to share their thoughts on video or written research about what’s happening in the markets. Some people have described it as the “TED Talks for Finance.”

It’s worth noting the growing drum beat of smart investors signaling caution. Ray Dalio, Howard Marks, Paul Singer, John Mauldin and Jim Rogers are messaging caution. As am I, your humble letter writer and portfolio manager.

Take 30 minutes and watch the following from Real Vision. Maybe load the following link on your phone, jump on the treadmill, stationary bike or take a quick walk. It’s worth the time.

Simply click on the picture.

Sound advice:

- “Eight years into one of the greatest bull markets of all time is not a time to be adding risk.” Kyle Bass, Hedge Fund Manager

- “We are going to have a recession when rates normalize and if you think otherwise, you’re delusional.” Peter Boockvar, The Boock Report

- “We are going to have the greatest bear market of your lifetime and mine.” Jim Rogers, Famed Investor

Opportunity lies in despair, despondency and depression. We are at the RED arrow (chart above). We’d be better off if we were at the GREEN arrow. It will come.

“Steve, you are such a bear!” Yet, as bearish as that all sounds, our trend indicators remain bullish and our equity strategies continue to remain long risk. My message is to simply remain mindful of the level of risk in the system and step forward with a solid risk management game plan in place. Doable.

Trade Signals — Don’t Fight the Tape or the Fed Still Bullish

S&P 500 Index — 2,569 (10-25-2017)

Notable this week:

No changes in the indicators or signals since last week. The equity market and fixed income trade signals remain bullish. U.S. economic growth remains strong. Risk of recession in the next six to nine months remains low. Inflation risk is neutral.

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note — Start Small, Grow Tall

Thought I was in my prime

But I was naked dressed in my pride

You saw through the things I hide

Yet still said be yourself, you’ll turn out all right

You made me run like I never run

Try like I never tried

Fight like I never fought

Made me want it…

Start small, grow tall

“Little Giant” by Roo Panes

Squeezed into seat 34B on my return flight home from Dallas, headphones on and mind deep in writing this week’s piece, the song “Little Giant” came on. I closed my eyes, listened and out of nowhere tears came to my eyes. Start small, grow tall. The song is about a son looking back at his parents. The kids are getting older and much of the heavy lifting is done. Sitting largely on the other side of all that hard work, I thought about my mom and dad and I thought about my kids.

Click on the link to the song and see what you think. Personally, I love it. And know that in those many tough moments when your kid is giving you the business, doesn’t want to do the homework, go to practice, stick with a team, do the dishes or take out the trash – stick to the drill and always show up. Hard to do.

It’s been a long week and I’m happy to be heading home. I sent the link to my boys. When your son calls and says “Thanks, dad. I really liked the song.” Well… that’s a good day. Start small, grow tall. True for many things in life.

And even if you’re not a parent, I hope you enjoy the song.

Here’s a toast to slowing down and reflecting on what’s most important in life… You, your family and your friends.

Have a great weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group