An Unremarkable GDP Report and Why Trend Growth is Still 2%

Today’s preliminary Q3 GDP number of 3% growth at a QoQ annualized rate has been met with a mix of relief and hope. Relief that one of the most destructive hurricane seasons ever didn’t completely sap growth and hope that two consecutive quarters of 3%+ growth is evidence that trend growth has, finally in the 9th year of this recovery, accelerated above 2%. While we are careful to not completely write off the decent number, evidence from two components in particular point to the underlying trend of domestic product growth still being closer to 2% than 3%.

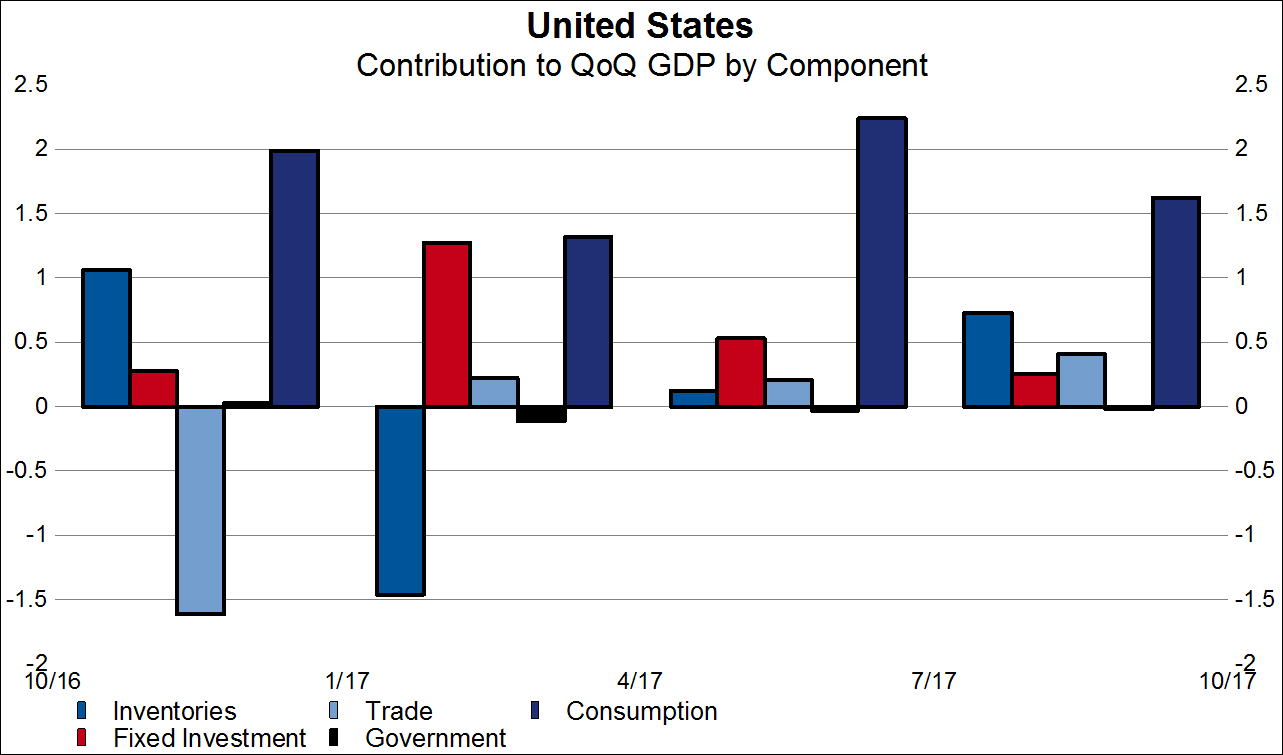

The first and most obvious such component is inventories. An analysis of today’s report shows that inventories contributed .7% of the 3% growth for the quarter. Said differently, inventories accounted for 23% of the growth in Q3. The last two times inventories contributed such a large share of growth (4Q16 and 3Q15), they subsequently detracted 1.5% and .6%, respectively, the following quarter. The first chart below shows the QoQ contrition to growth by the major components of GDP.

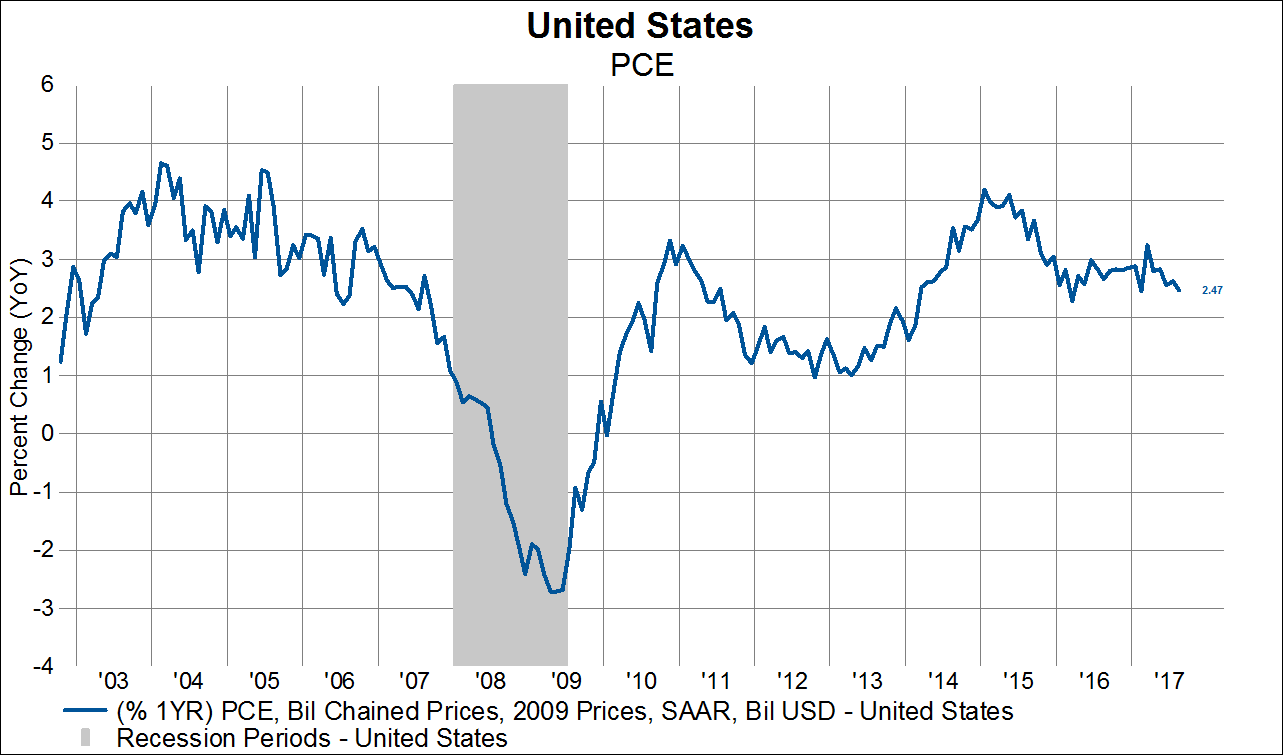

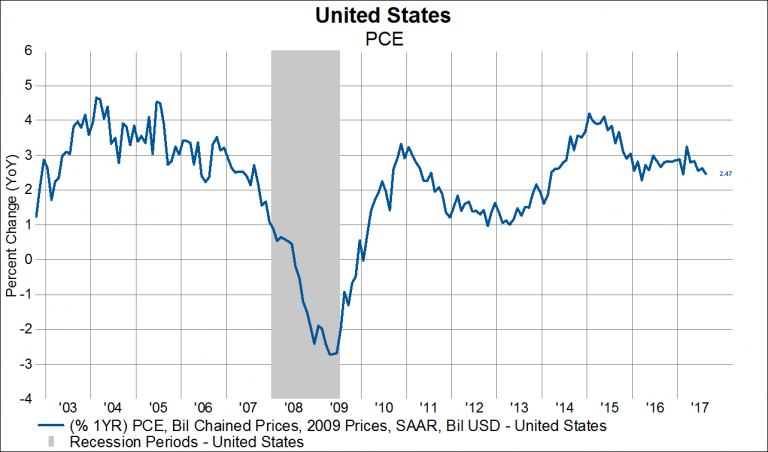

The second, and more structurally worrying component of GDP growth, is personal consumption expenditure (PCE). PCE is the largest and most stable component of GDP growth in the United States. In Q3 PCE contributed 1.6% of the 3% growth, or a little over half of overall growth. This is the smallest contribution from PCE since 3Q14, suggesting that PCE may possibly be a source of growth in the quarters ahead. PCE’s contribution to growth is represented by the dark blue bar in the chart above.

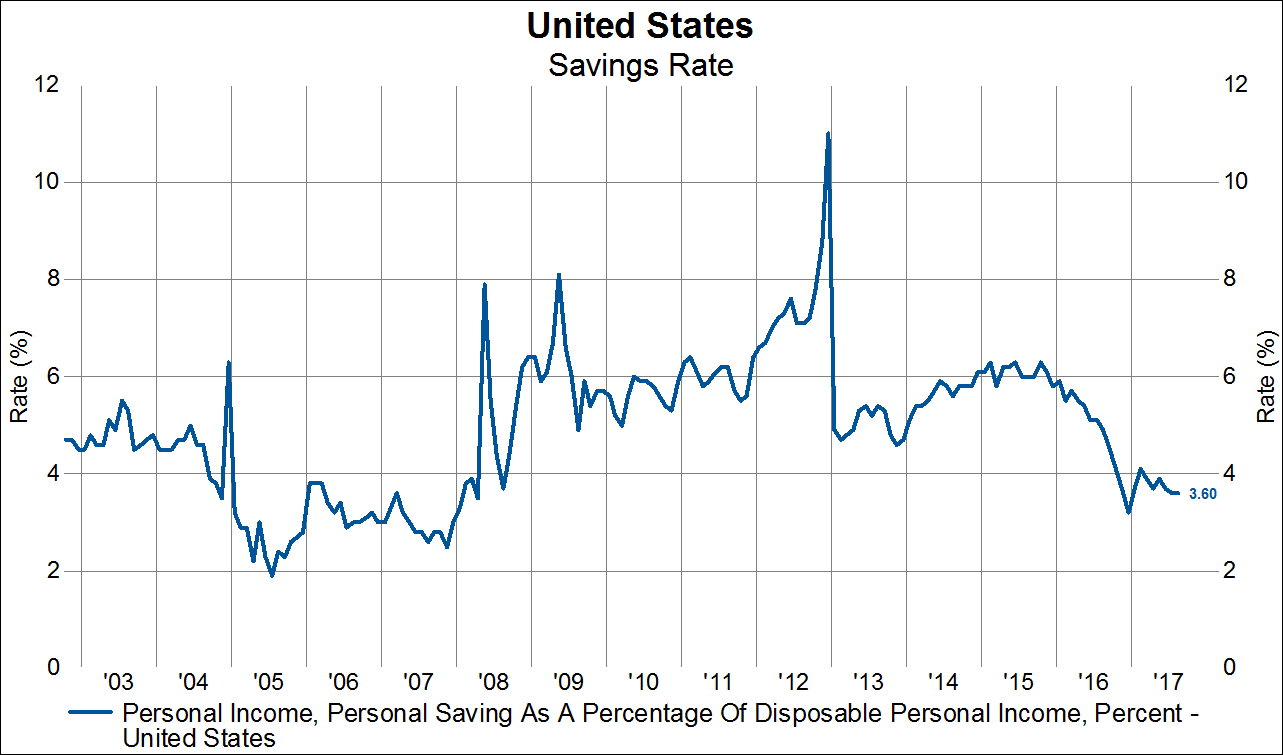

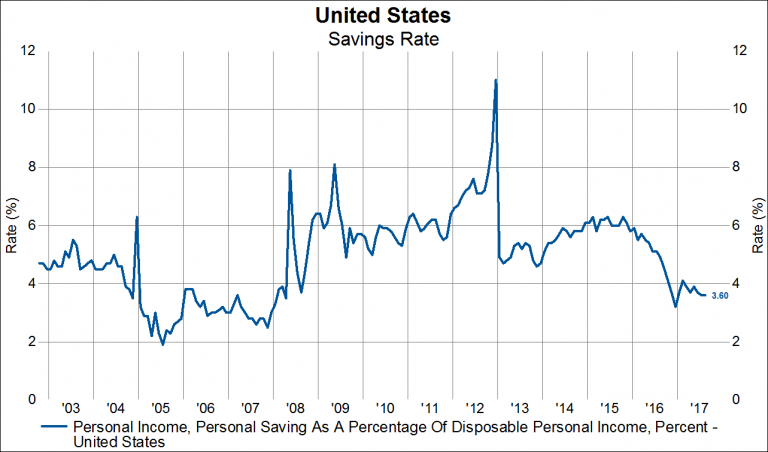

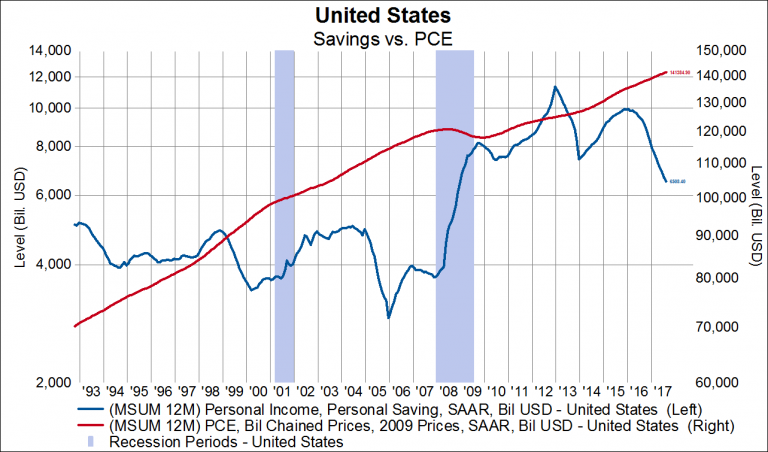

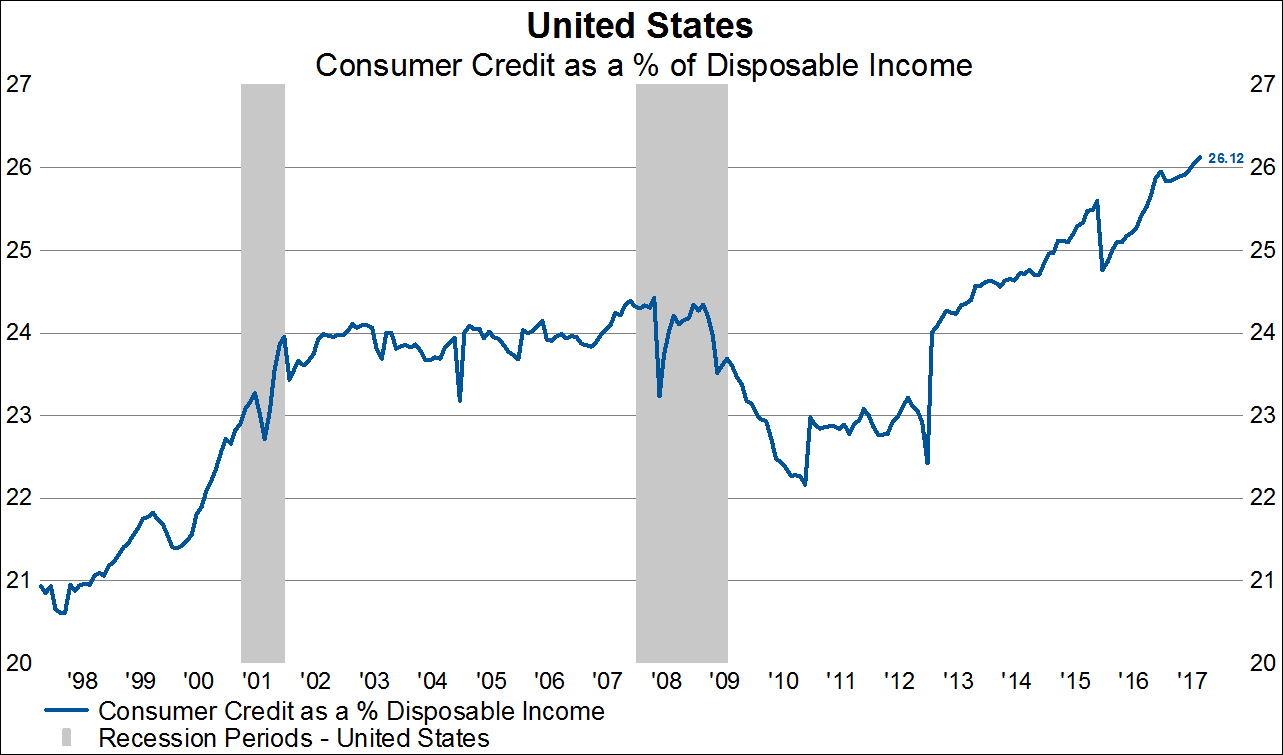

But here is where things start to get more interesting. Year-over-year growth in PCE peaked back in 2014 and has been on a declining trend since, as the next chart below shows. It would be one thing if trend PCE growth had room to accelerate, but indicators of household savings and credit point to exactly the opposite.