“No man is so foolish but he may sometimes give another good counsel, and no man so wise that he may not easily err if he takes no other counsel than his own. He that is taught only by himself has a fool for a master.”

-Hunter S. Thompson, 1937-2005 Journalist and Author

Though the seething pits of humanity at the New York Stock Exchange and Chicago Mercantile Exchange, with their traders all shouting at each other, are largely things of the past, that is still what markets basically are: a bunch of people shouting different things. A market price is the price at which the same amount of people are buying as are selling. Even if that price is falling, each tick represents the price where an equal number of buyers and sellers came together. Buyers think the price will go up, sellers think the price will go down, and hence market prices also reflect the balancing of disagreement.

As such, one cannot successfully navigate the investment landscape by listening to everybody, as one will end up perplexed after receiving perfectly conflicting advice. But does this also mean one should not listen to anybody? We think that is overkill. Instead, we seek to tune out almost everyone and carefully listen to only those voices we believe are “smart”. Others are ignored, even if they sound “smart”. We especially pay attention when those to whom we listen challenge our current beliefs, which has happened recently.

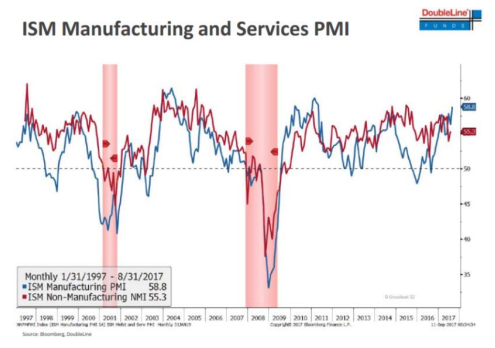

In the past we’ve talked about how little effect politics has on economic growth, and specifically that economic growth wouldn’t be accelerating in the near term due to recent political changes. And this indeed had been the case until recent multi-year-high readings from the ISM’s Manufacturing PMI and Non-Manufacturing PMI Indexes1 . These high readings indicating increased economic activity would have caught our attention on their own, but we especially took note when we heard famed deal-maker Sam Zell talking about how, despite whatever misgivings one might have concerning the Trump Administration, it is certainly pro-business and the roll back of regulations is starting to unleash economic activity. People railing against regulations are a dime a dozen. However, it matters more coming from Zell, who puts his money behind his opinions and who has a history of correctly calling large shifts in economic behavior2 . Could this be happening?

It might be. While we stand by our prediction that little will be accomplished legislatively3 , we have also said that action is much easier on the deregulation side. We see it anecdotally in many areas; here are just a few examples:

- New payday lending regulations were stalled and ultimately watered down when issued. The Consumer Finance Protection Bureau’s lead enforcer just stepped down and we shall see if these new regulations are even enforced at all.

- Recent appointments enabled a regulatory panel to vote in favor of removing AIG from the list of Systemically Important Financial Institutions (SIFIs), allowing the insurer to operate with more flexibility.

- The Environmental Protection Agency recently repealed Obama era rules which sought to limit emissions from coal plants (the Clean Power Plan).

Because Trump assumed office lacking the usual political establishment followers typically used to fill administration posts, he has often turned to former industry veterans and lobbyists to run the agencies that are supposed to regulate their industries. How could this not affect the regulatory landscape? We had not thought deregulation would make a very large difference in business activity and GDP, but between Zell’s comments and recent macro strength readings, i.e. the ISM data previously mentioned, perhaps it will. In fact, we have become open to the possibility that we could be in for a longer, stronger economic expansion, potentially historic in length.

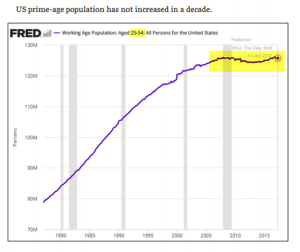

However, any increase in growth will still have to contend with one of the big reasons behind subpar GDP growth this past decade: the absence of growth in the prime working age population. This cohort is not set to resume growing again until the year 2022. We find it kind of amazing that people don’t talk about this growth input more. We guess politics is a little more fun to discuss than demographics.

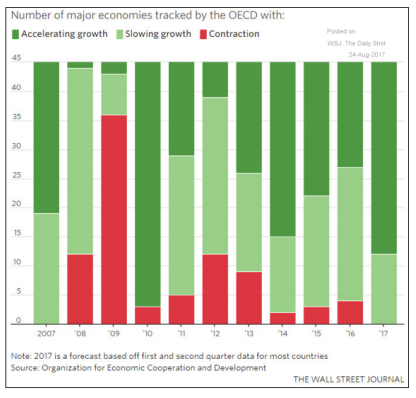

Certainly part of the economic strength seen recently does not have to do with U.S. politics, as it is global in nature. For the first time in a decade, all 35 OECD economies are growing at the same time. So it’s not just American vibrancy, we are seeing synchronized global growth.

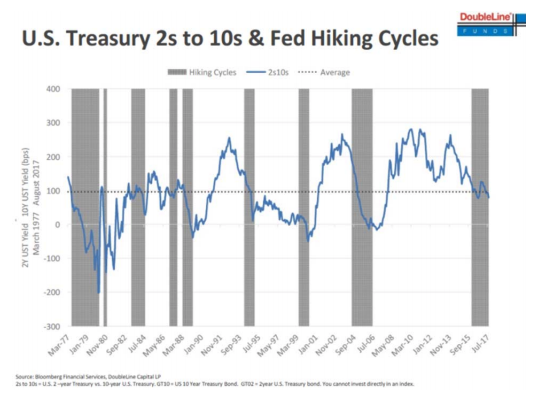

We have been somewhat concerned with the risk of recession, but a number of market signals pointed out by Jeffrey Gundlach of DoubleLine, dubbed the new “bond king”, have lead us to think perhaps our recent caution may have been premature. For example, the yield curve, meaning the difference between the 10-Year Treasury yield and the 2-Year Treasury yield, inverted (i.e. became negative) before each of the past five recessions began.

The current yield curve is not near inversion; in fact, despite flattening recently, the 10-year minus 2-year steepness is near its longer term average (the dotted horizontal line on the above chart).

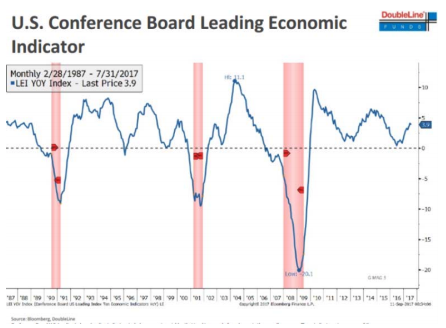

The chart above tracks the U.S. Conference Board Leading Economic Indicator, which is a composite of especially economically sensitive indicators, and below that we again show the ISM Manufacturing and Services PMI. Recessionary periods are represented by the red bars on both charts. Recent readings have generally been trending upward and away from levels typically seen before a recession.

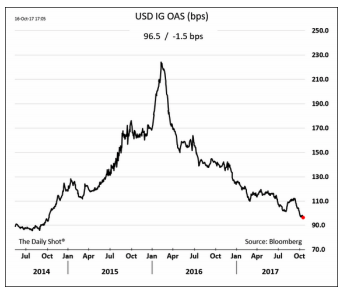

Finally, investment grade corporate bond spreads4 (the extra yield over Treasuries) have been tightening whereas they typically are widening when heading into an economic slowdown. All of these indicators confirm that the U.S. is not at all close to tipping into recession in the near term.

Does our more positive economic outlook mean we shouldn’t be cautious? No. The time to be greedy is when others are fearful and we are still attempting to somewhat stifle our greed.

For one thing, large developments with interest rates might rock the boat. More specifically, this month the Fed is reversing its “quantitative easing” program, i.e. it is no longer printing money to buy bonds but is instead selling bonds5 and sticking the cash in a giant sock drawer (sadly only metaphorically). While this got a decent amount of financial press... we feel like it hasn’t resulted in sufficient financial discussion. Certainly, it hasn’t punctuated the general psyche like when the Fed started buying bonds. Does everyone remember people screaming about the Fed’s “non-stop printing of money”? Where is the jubilation at the outset of the opposite? We once called quantitative easing “lending money into existence”... well starting this month it is now being “repaid into oblivion”. This is a big change worth noting, not only for its direct effect on the market reality but also the potential effect on market psychology. At the very least, the constant selling of bonds is a new, persistent, and increasing force for higher long-term rates (though of course, this force may be overwhelmed by the other myriad forces of the economy and global capital markets). As a refresher, the Fed had been buying Treasury and mortgage-backed bonds from late 2008 through late 2014, reducing supply and driving prices up and yields down. Now it will effectively be selling $10 billion of those bonds per month ($6 billion of Treasuries and $4 billion of mortgages), and increasing the monthly sales by $10 billion each quarter until it is finally selling $50 billion worth of bonds per month a year from now. $50 billion here and $50 billion there and pretty soon you’re talking real money.

On interest rates, we will take another cue from Mr. Gundlach, who we will sum up as saying rates are done declining (though he’s been saying this for a while and was arguably early). Thus we are retiring our “rates are never going up” mantra and replacing it with, “rates might be going up in the future, but probably not immediately, and not very far”. It’s less catchy we realize. Despite the change of direction in money printing/money destruction at the U.S. central bank, U.S. interest rates will be effectively capped by low foreign interest rates, until foreign central banks too change tack, which is not imminent.

Nevertheless, it’s the end of an era... which was part of our motivation in increasing our weightings in certain financial stocks, as they are beneficiaries of higher rates (and more importantly, they were trading at uncommanding valuations).

We will offer a word on rising rates: don’t be too scared. Rising real rates (not high nominal rates that lag inflation) are actually beneficial to the investor, because they mean his or her money will be growing faster in the future, even if values take a hit in the short term. Simply put, high rates are good for savers, and bad for borrowers. We expect most of our readers are in the former category.

We will close with our answer to a frequent question: is the U.S. stock market overvalued? No, despite the market’s advance, we wouldn’t go so far as to say it is overvalued; the high prices and multiples appear to be justified by a strong economy and low rates. However, the market is expensive, which does leave it vulnerable if and when these conditions change. We anticipate this to occur more “eventually” than “imminently”. The stock market has returned 15% so far this year, an excellent return with potentially more on the way. We should enjoy it; it will not always be so.

We thank you for the trust you place in us.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

© Knightsbridge Asset Management, LLC