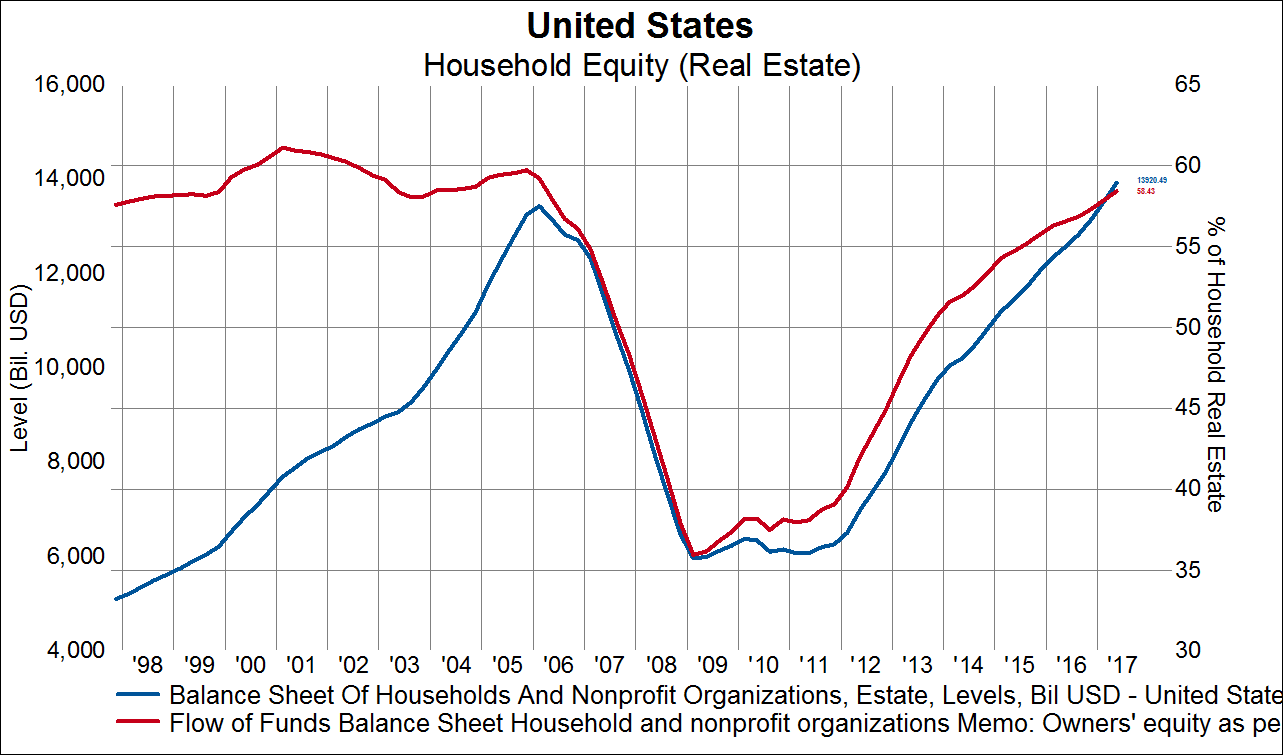

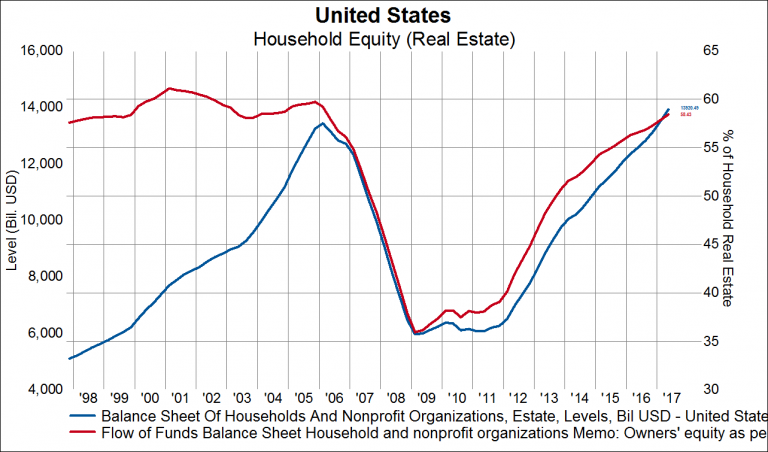

The rise in home prices from the trough in 2009 has added $8tn to home values, pushing the value of homes to a level surpassing the 2006 peak (chart 1).

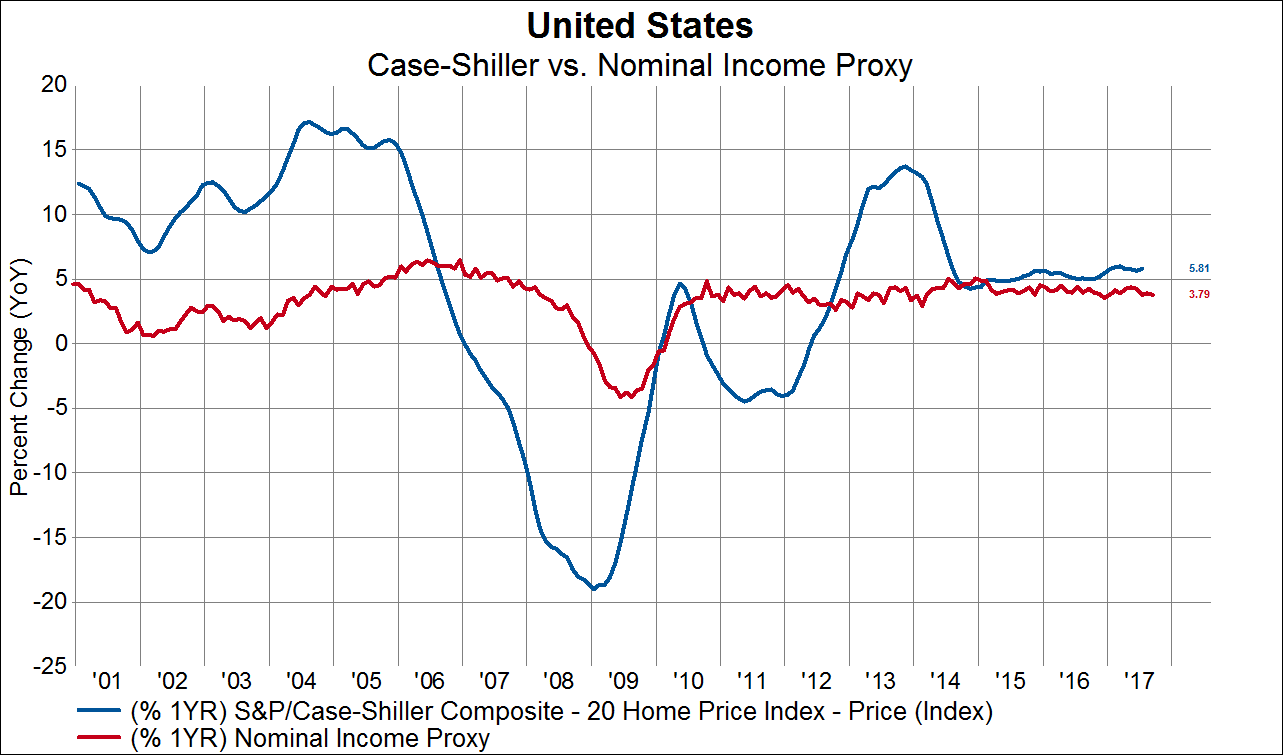

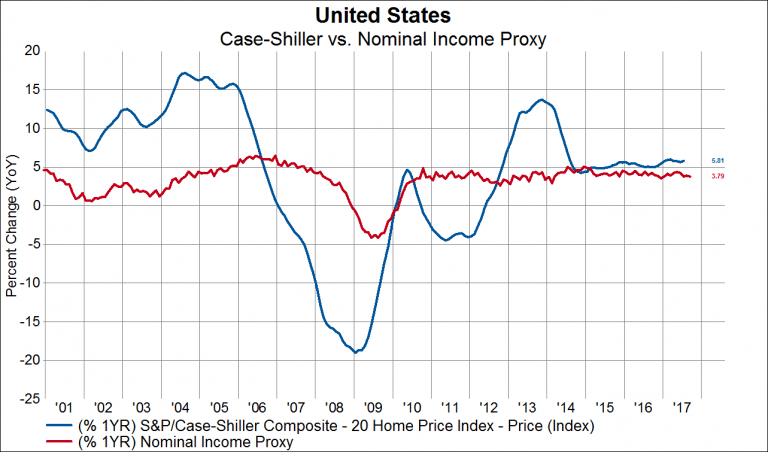

In order to accomplish such dramatic growth, home price growth outpaced nominal household income growth in each of the last six years. In chart 2 below we plot the year-over-year change Case-Shiller home price index (blue line) on top of the year-over-year change in our nominal income proxy (hours worked * employment * average hourly earnings). As we saw from in the period leading up to the financial crises, home price growth can exceed nominal income growth for a long period of time, especially when interest rates are falling, but eventually the excess must be reversed.

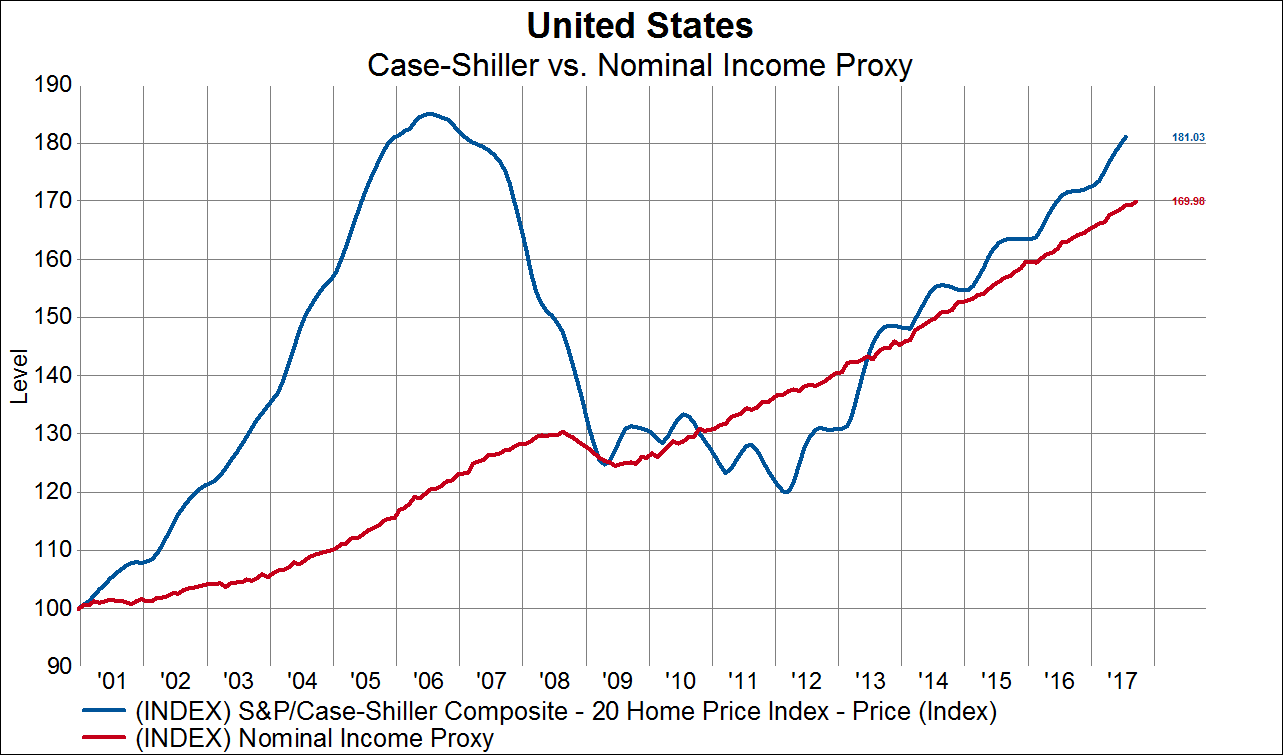

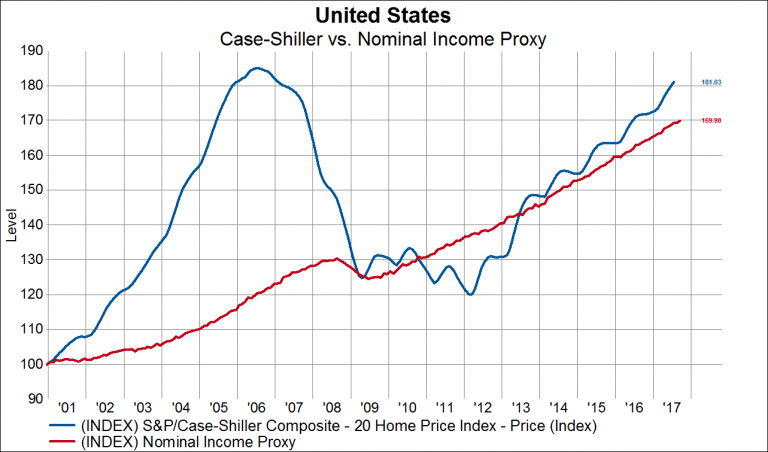

Chart 3 depicts the level of the Case-Shiller home price index (blue line) overlaid on the level of nominal incomes (red line). In this chart we can more clearly observe the recent divergence in home prices and nominal incomes.

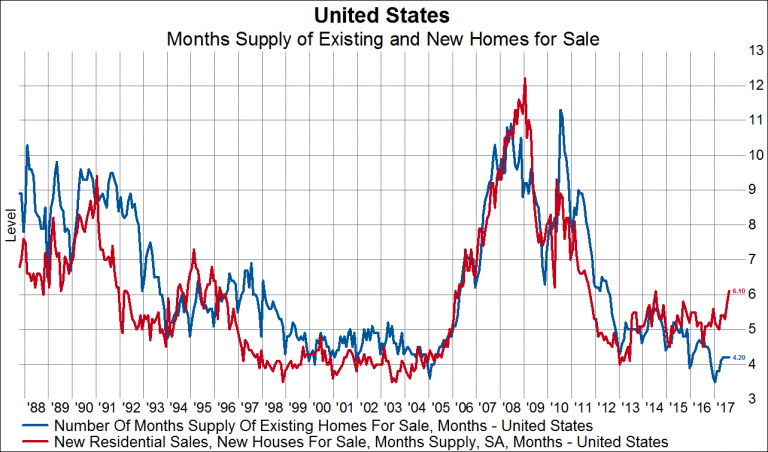

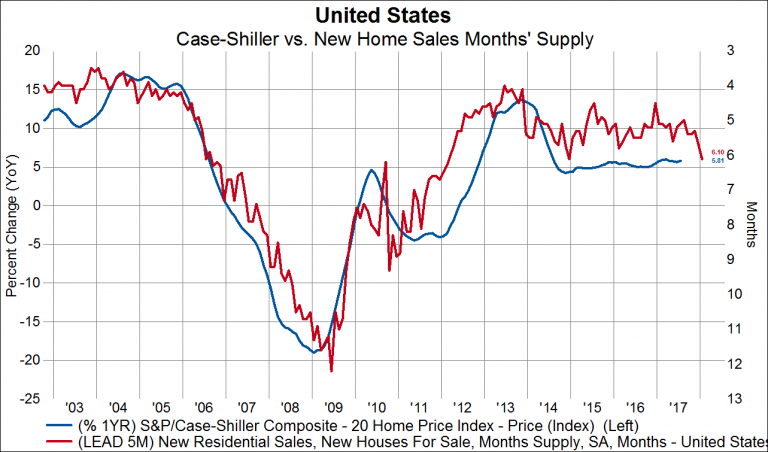

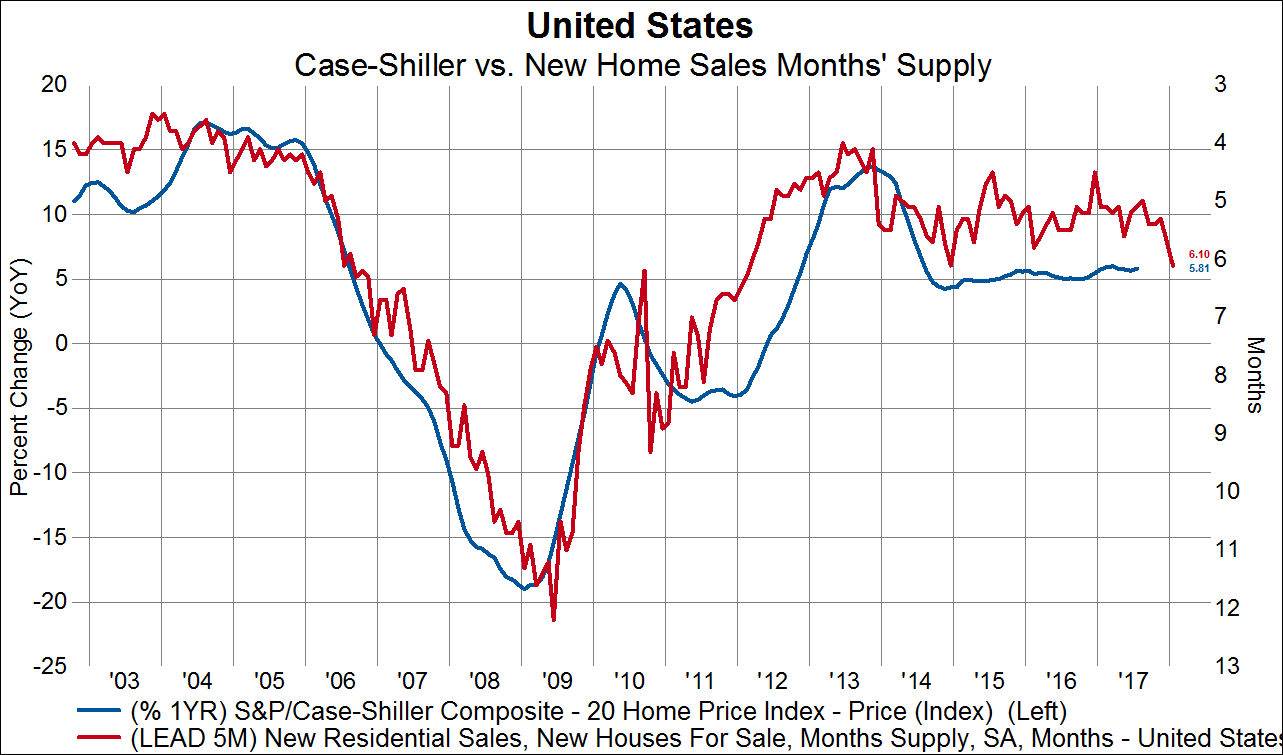

So the question is now, will home price growth continue to outpace income growth or are we somewhere near the end of this home price recovery cycle? For that we turn to inventory data. The next chart below shows the months supply of new (red line) and existing (blue line) homes. One nuance of this chart is that new home supply tends to lead existing home supply at important turning points. For example, in the late-90s cycle the supply of new homes peaked in 1994 and troughed in 1998 where as existing home supply peaked in 1997 and troughed in 2000. Before the housing boom got going in earnest, new supply troughed in 2003, but existing home supply didn’t trough until 2005. During the downturn new home supply peaked in 2009 whereas existing home supply peaked in 2010. Currently, new home supply has made an upside breakout, which suggests existing home supply will follow suit.

The implication of more supply is of course lower price growth. In the final chart below we plot the year-over-year growth in the Cash-Shiller home price index (blue line, left axis) overlaid on the months supply of new homes (red line, right axis, inverted, leading by 5 months). If new home supply continues to grow as the trend suggests it should drag down home price growth with it, a positive development in our opinion that would allow nominal incomes to catch up to home prices.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital