“Long-term Investors need to be invested in long-term assets, but pay special attention to limiting downside losses.

The best way to make money in the long term is not losing it in the short term.”

– Dr. David Kelly, Chief Global Strategist

J.P. Morgan Asset Management

Long-time readers know I’m an avid Ned Davis Research fan. I’ve been a loyal client since the 1990s. Ned Davis built a fact-based, technology-driven research organization. Some years ago, Ned wrote a book titled, Being Right or Making Money and I believe that title sums up NDR’s investment research culture. Much of what you and I hear every day is nonsense. NDR seeks to identify key data relationships that matter most and presents their research in a mathematically sound way.

One of Ned’s great beliefs is that we investors need to avoid the really big mistakes. Right… but how and by what process? Is the process viable? The probabilities favorable? Do you believe in it? Can you stick to it? No process is perfect, but there are processes you can put into place that may help you minimize mistakes.

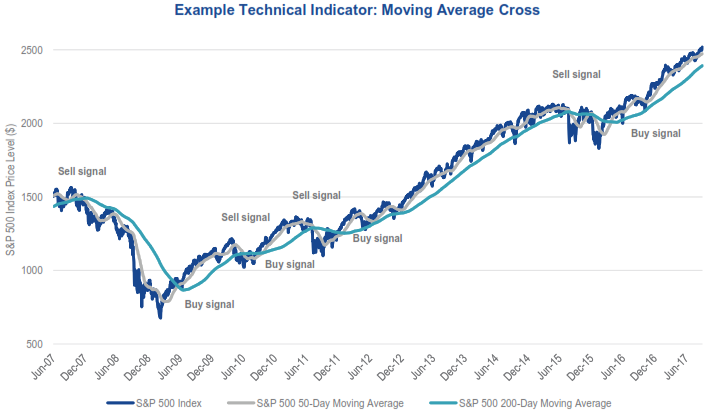

The great trader, Paul Tudor Jones, teaches his MBA students that if you do nothing else, put a 200-day moving average stop-loss on everything you own. Tested, you’ll find it is a pretty good trading strategy rule. Here is a look at a simple “Moving Average Cross” trend following system. The blue line is the S&P 500 Index. The gray line is its 50-day moving price average and the green is its 200-day moving average. Signals occur when the shorter-term trend line crosses above or below the longer-term trend line.

As you can see, a pretty good risk management process. The sell signal in late 2007 would have gotten you out of the market near 1450 on the S&P 500 and the subsequent buy back in near 850 in mid-2009. Since then, there have been a few whipsaw trades but generally you would have participated in most of the upside. Not perfect, but overall pretty good.

“It’s about not losing it in the short term.” Roger that.

Buying-and-holding is an investment process and it works over many years. If you believe in it and have the years to let it work, and strong belief in it, go for it. The problem is that many individuals can’t stick to the process; that is, buying and selling at the wrong times. And if you sold, when do you decide it’s safe to get back in. Emotion plays a big role in the decision process… mostly a negative role.

The great Sir John Templeton said, “To buy when others are despondently selling and to sell when others are avidly buying requires the greatest of fortitude and pays the greatest ultimate rewards.” That’s an investment process. My mother-in-law is a great investor and her process is much like Sir John’s. I’ve come across just a few people that can follow that process. It requires conviction and patience and an ego that is ok with being wrong at times. Sir John was one of the greats and so is Paul Tudor Jones. And, of course, my mother-in-law is fantastic.

A number of years ago, I approached NDR to do some custom work for CMG. One of the most popular indicators on NDR’s site is Ned’s “Big Mo.” It’s an excellent momentum indicator that’s done a fine job at signaling risk-on or risk-off, but we wanted a proprietary risk management process for our clients.

One of the things that tends to happen when cyclical bull markets peak is that fewer and fewer of the stocks that make up the S&P 500 Index continue to rally. Just a few companies carry the index on to higher highs; yet more of the underlying company stocks are breaking down. Stocks tend to be a leading economic indicator and, at the individual company level, if more and more companies are breaking their trend lines, it is a signal that perhaps there is something bigger going on economically. At bull market cycle tops, investors are euphoric and margin leverage is high. Tops generally roll over while bottoms tend to “V” bottom. It has nothing to do with fundamentals and a lot to do with the unwinding of leverage (forced margin call selling). That’s when fear kicks in and margin debt pressures lead to forced selling. Weaker hands can’t take the heat and unload their equities as well. At market peaks, investors are typically overweight equities and any would-be buyers simply step away. Market behavior at a bull market top is different than at a bear market bottom.

We wanted to improve upon the 200-day MA stop-loss rule that many people use. If too many investors use the same signal point, you can imagine the number of hedge fund vultures and flash traders looking to take advantage of the activity that occurs at such knowable price points. Yet, absent other risk management processes you can believe in and follow, it is still a pretty good rule.

“Long-term investors need to be invested in long-term assets, but pay special attention to limiting downside losses.” Sound advice from JP Morgan’s Dr. David Kelly. Trend analysis is a way to help minimize short-term loss.

This week, I’d like to share with you a paper I wrote for VanEck entitled, Risk Management for All Markets. It’s a quick overview on how the NDR CMG US Large Cap Long/Flat Index process works. You’ll also find a few charts you may find helpful in your work with your clients.

- There is an updated chart showing all of the secular bull and bear market periods since 1900 along with the return data (without and with inflation). For example, since 1900, the market has been in a bull market cycle 54% of the time.

- On a price basis, an investor spent 70% of the time in a bear market or recovering from one. That means that just 30% of the time a buy-and-hold investor is creating new wealth. I bet most people don’t know these stats. With dividends factored in, 41% of the time is creating new wealth. Better, but still much lower than your client might guess. My personal guess was 60%. I was surprised.

- There is also a helpful chart showing just how much return is required to overcome various amounts of loss. “The best way to make money in the long term is not losing it in the short term.” Indeed!

You can find it by clicking below:

Risk Management for All Markets

Enter your email address and VanEck will send the paper to your inbox. And please feel free to email me if you have any questions.

Why VanEck? CMG and NDR licensed our index to VanEck and they created an ETF. What started with a coffee with a close and trusted friend, Kol Estreicher, three years ago grew to become a new ETF. Kol had just joined VanEck, knows CMG’s history well and asked me if I had a strategy or two that might work well packaged inside an ETF. Certain strategies may work well inside of an ETF. I told him about the work we did with Ned Davis Research and a light was lit.

While we are really excited about the ETF, please know my goal is to simply message that there are processes that may help you both participate in the market and manage risk. None are perfect. Ours is one idea. I believe it is important to diversify to several trading strategies. To wit, find experienced managers with defined processes.

I believe that by mixing together different strategies you can fine-tune the risk and return metrics in a way that suits your investment profile: risk, needs and goals. If you are more aggressive and willing to take on more risk, then combine several equity-focused processes. If you are more moderate or conservative, broaden the choice of asset classes.

The good news is that technology has advanced so far that you can run analyses to see how different asset classes and strategies may fit together to align with your return and risk goals. The tools available to you and me are far advanced from where we were just a handful of years ago. Talk to your investment advisor.

I’m writing from Washington, DC this week. Dr. Kelly’s presentation was exceptional. His quote couldn’t have been timelier for this week’s missive. Last night we had a behind-the-scenes tour of the National Museum of Natural History, then dinner at the National Museum of American History. It was great fun. I wanted to share Dr. Lacy Hunt’s latest quarterly letter. He sees low inflation and low growth ahead… he makes a compelling case but let’s bump that to next week along with my notes I’ll share from David Kelly’s presentation.

Grab a coffee and let me know what you think about the research paper. When you click through, you’ll find the latest Trade Signals and a few photos from DC.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Trade Signals — The Bull Market is Everything

S&P 500 Index — 2,551 (10-11-2017)

Notable this week:

The equity market and fixed income trade signals remain bullish. U.S. economic growth remains strong. Risk of recession in the next six to nine months remains low. Inflation risk is neutral.

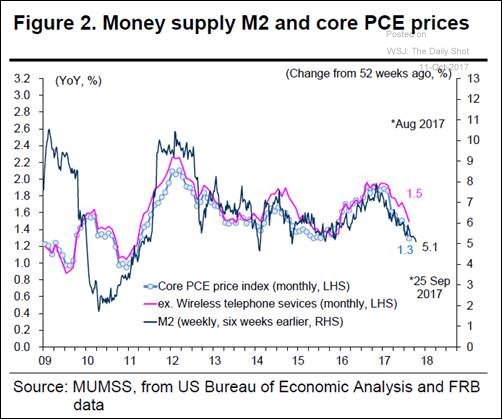

The broad money supply growth in the United States is slowing. Does it suggest weaker inflation ahead? I don’t see signs of inflation yet.

Source: WSJ, The Daily Shot, 10/11/2017

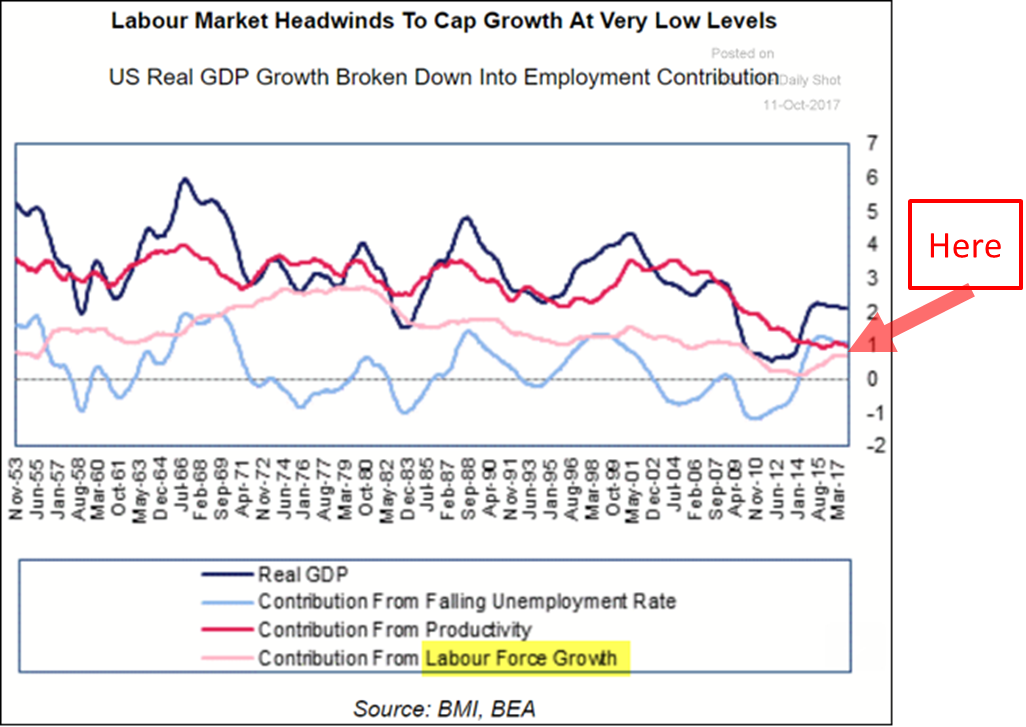

Slow productivity improvements and a stagnant labor force size will hold back GDP growth (second chart below). The policy of tightening legal immigration makes the situation worse.

Source: WSJ, The Daily Shot, 10/11/2017

But we do have – The Bull Market in Everything… This from The Economist this week:

Raging Bull… It sure feels like it.

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note

I’m finishing the piece early Friday morning so I can get back to a few more conference sessions. OK, it’s been years since I’ve been to the Smithsonian. And that’s been a mistake. I couldn’t help but think about Susan’s science-minded son and we’ll have to come back again soon with kids in tow.

On Wednesday, I spent the afternoon with my old college roommate, good friend and fraternity brother, Congressman Charlie Dent. The following picture is from House Speaker Ryan’s balcony overlooking the Mall and the Washington Monument.

Here are a few pictures from the Smithsonian.

My group got the insect, bugs and bones tour:

I’ll spare you the skulls and bones. The work the scientists do is pretty cool.

We’ve come far in a short period of time. I owned that large cell phone (lower left next photo) and I looked ridiculous using it:

And I got a big kick out of these early Band Aid boxes:

How many of those did our moms throw out?

I’m in Dallas on October 24 and 25 for a Mauldin Solutions advisor event, followed by a trip to Charleston on the 30th. Some golf is in the weekend plans. Matthew is coming home from school and we are teamed together in a fun tournament at Stonewall. But he’s really home to celebrate his brother at today’s home soccer game. It’s senior day. I’m heading to the train for home soon. Can’t wait. Wishing you and your family the very best!

Have a great weekend!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group