As expected, hurricanes Harvey and Irma had a significant impact on the nonfarm payroll data. However, it’s impossible to say exactly how much. The distorted September payroll figures were never going to be a factor in the Fed policy outlook. There will be two more employment reports before the mid-December policy meeting and we can expect a recovery from hurricane effects. However, an unexpected drop in the unemployment rate and a pickup in wage growth seemed to further cement the market’s view that the Fed will hike in December.

Click here to enlarge

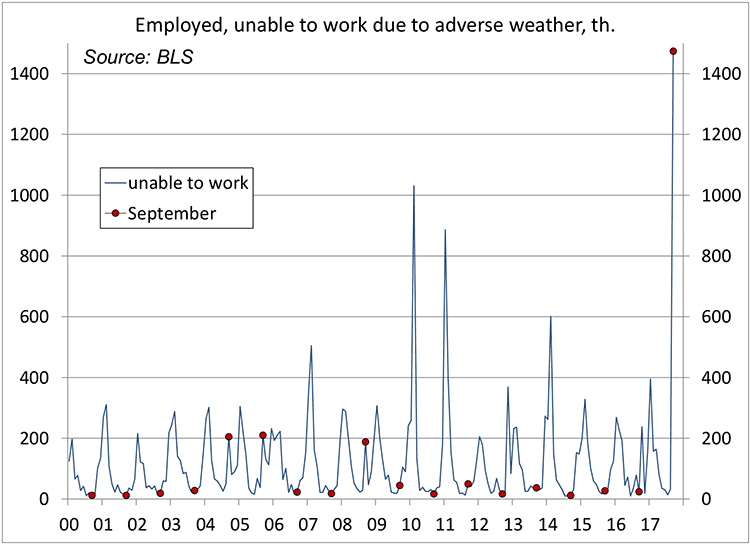

For the monthly employment data, timing is everything. The establishment survey is for the pay period that includes the 12th of the month. This can vary from firm to firm depending on whether the pay cycle is weekly or semi-monthly. A person working anytime during that pay period is counted in the nonfarm payrolls. In hindsight, it looks like the hurricanes had a disproportionate effect on smaller firms. The number of people who couldn’t work due to adverse weather jumped sharply, but these figures aren’t directly comparable to the payroll data.

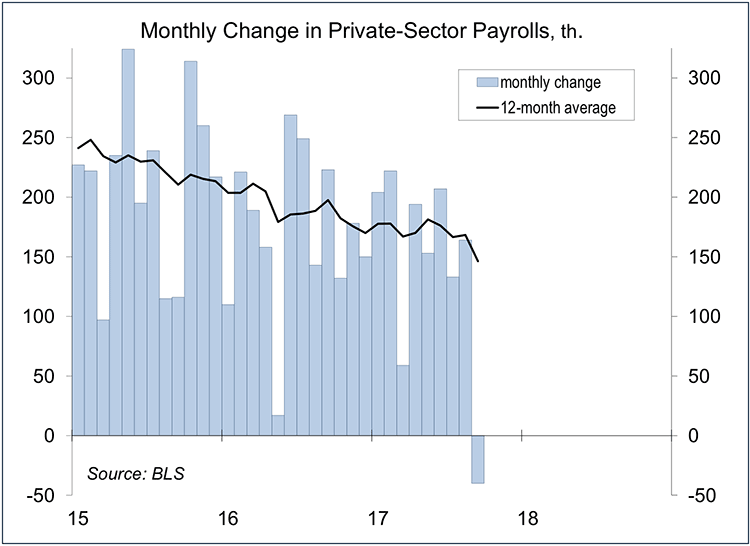

Nonfarm payrolls fell by 33,000 in September (+340,000 before seasonal adjustment), with a net downward revision of 38,000 to July and August. Prior to seasonal adjustment, education (public and private) rose by 1.537 million (vs. 1.536 million a year ago), while non-education jobs fell by 1.197 million (vs. -893,000 a year ago). We normally lose jobs at the end of the summer travel season. Hurricane Irma apparently made that worse than usual. Payrolls for eating and drinking establishments fell by 105,000 (-255,000 before seasonal adjustment, vs. -125,000 a year ago).

Click here to enlarge

The household survey covers the week of the 12

th and a person with a job is counted as employed even if they didn’t work that week, “regardless of whether or not they are paid.” Hence, the September survey failed to register an impact for Irma. The unemployment rate fell to 4.2% (from 4.4%), but household survey results are often quirky around the start of the school year (and the end of the summer travel season).

Click here to enlarge

Average hourly earnings rose 0.5% in September, more than was expected, lifting the year-over-year pace to 2.9%. Note that the wage data are often revised the next month – so, take that with a grain of salt. Hurricane Irma likely had some impact on the wage data, as job losses were concentrated in lower-paying industries (lifting the average). The ADP employment report, based on private-sector payroll processing data, showed reduced hiring at smaller firms. However, a pickup in wage growth would coincide with tighter labor market conditions and recent anecdotal evidence of broad-based wage pressures.

Is this enough to force the Fed’s hand in December? Not by itself, but in their recent comments, most Fed officials appear to have remained on the tightening path. We will get two more employment reports between now and the mid-December FOMC meeting. The hurricane effects, however uncertain, are likely to wash out of the economic data by then.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James