“It isn’t what’s in my head that’s most valuable, although I did learn a lot along the way;

it’s knowing how to deal with not knowing that’s been the source of my success.”

– Ray Dalio

I’d like to take you to two places today. One is life and the pursuit of dreams. “I was born with a silver spoon in my mouth,” legendary Coach Lou Holtz begins. (Below I provide you a link to a short video clip.) “You have to have something to hope for and something to dream about.” It is a six-minute happy pill. I watched it with my kids and they loved it. You’ll love it too, I promise.

For several weeks, I’ve been promising you the link to Barry Ritholtz’s interview of Professor Richard Thaler. My friend Barry interviewed Professor Thaler at the 2017 Morningstar ETF Conference earlier this month.

Thaler is called the father of behavioral economics and is the author of over 50 books. He also runs an investment management firm. So the second place I take you today is the replay of that keynote interview. It is entertaining and full of investment insight.

I’m not sure about you, but I find myself listening to more and more podcasts. I load them into my phone and play them as I drive to work or while I’m taking a long walk/run with loyal dog, Shiloh. Wireless data (e.g., LTE) and Wi-Fi coverage just keep getting better. Pretty cool.

Get your headphones ready and lace up those sneakers. Listen to Coach Holtz first. You’ll want to go out and conquer the world. And don’t miss the 41-minute Ritholtz-Thaler interview. Thaler has such a dry and witty fun way.

Put on your sneakers… click and go:

Click on image to view the video.

Click here for the audio only of Barry Ritholtz’s “A Conversation with Richard Thaler” or click below for the video.

Click on the image to view the video.

It’s early Friday morning as I write today’s piece and thankfully Susan just handed me a coffee. “Good Will Hunting” was on HBO last night and I got caught up in the story. It might have been the fourth time I’ve watched it. Robin Williams was brilliant. And boy is he missed. The coffee this morning is needed.

I am rushing to finish as I’m heading (with a few podcasts loaded) to Penn State. My son, Kyle, is touring the theater school this afternoon. I’m a crazed Penn Stater, as you probably know by now, who frankly needs to keep all that on the down low. The college tour season begins anew and trips to Pittsburgh, Boston, Chicago and New York are on the calendar. I’m really looking forward to the time together with Kyle.

Theater is a challenging path with few Matt Damon and Ben Affleck success stories. But passion matters and dad says go for it… Coach Holtz says find something to dream about. Coach Holtz says go for it too.

If you’re not lacing up your sneakers, then grab that coffee and find your favorite chair. Ray Dalio is out with a new book entitled, Principles: Life and Work. He has been in the press frequently and for good reason.

Dalio says the closest historical period to today is 1937. High debt, strong support from the Fed and protectionism. World War II followed in 1939. It’s the rise in global protectionism (putting up trade barriers, etc.) I fear most. That will throw a monkey wrench into the system. But history doesn’t have to repeat itself and, fortunately, Dalio’s on a mission to help policy makers understand how the economic machine works.

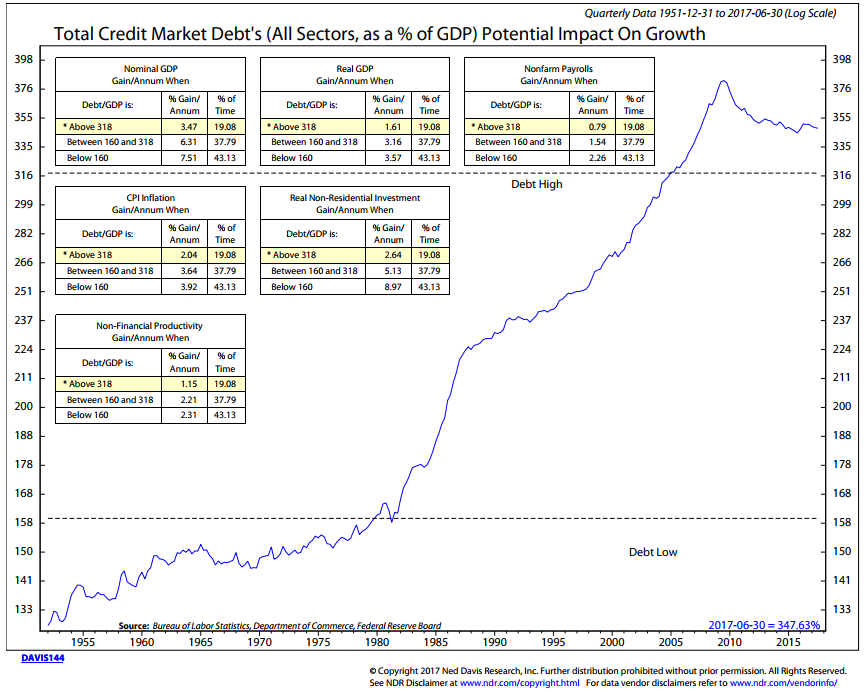

You’ll find “More on Ray Dalio” in the body of today’s On My Radar. Also, there is a great chart on debt and what it means for growth. High debt = low growth. Debt’s clearly a drag on growth. How we restructure is yet to be known.

I hope you find the audio and videos as interesting as I did. Have a great weekend!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- More on Ray Dalio and Link to Bloomberg Interview

- Debt and Demographics – Two Powerful Ds

- Just When They Said Active Management is Dead

- Trade Signals – A Look at Margin Debt and its Trend – 09-27-2017

- Personal Note

Ray Dalio – From a Think Advisor Interview

To give you a feel for some of Ray’s current thinking, I’ve clipped a few questions and answers from a recent interview. You’ll find the Bloomberg – Ray Dalio podcast link after the Q&A.

Do you see a disconnect between the U.S. stock markets being at an all-time high, while at the same time the economy continues to grow slowly?

No, I don’t. Markets, in general, are driven by the interest rate. As interest rates go down, as they have, that’s helped. Second, the purchases of financial assets by central banks have pushed asset prices up. Third, the expected returns of bonds and equities going forward are at relatively normal premiums to the existing short-term interest rate.

What are the implications of all that?

People buy profits, not the economy. So if the corporate tax rate is cut, a company is worth more even though the economy might or might not pick up on that. If regulation is reduced, that stimulates business. It might have other consequences, but it causes profits to rise.

Any other critical reason for what’s happening in the economy and market?

Technology, which is improving profitability, is also worsening [employment]. That worsens the economy because technology is replacing people [in jobs]. Improving profitability [through technology] is good for companies but not good for the economy as a whole because the people losing jobs are also the people who are more inclined to spend income. I call that group the lower 60%. So technology helps profits but hurts employment and helps to cause a slower economy at the same time it has caused companies to be worth more.

Has the U.S. ever been in a situation like that before?

We had a similar one between 1935 and 1940. I would say that 1937 [during the Great Depression, two years before the start of World War II] is most like the year today. We had the same sort of debt crisis; interest rates went to zero and the central banks printed a lot of money and bought financial assets, which went up in price. We had the same sort of wealth gap and the same sort of populism around the world.

So is there a lesson from 1937?

It’s very important that the Federal Reserve be very cautious and slow to tighten monetary and fiscal policy because we have asymmetrical risks: many more risks on the downside than on the upside. And be cautious about how political and social conflict is handled. Can we work together, or are we going to be split? Even though the stock market is at its peak and the unemployment rate is at a low, for the bottom 60% it’s a bad economy. We must not have an economic downturn.

On Decision Making…

You write that collective decision-making is the “secret sauce” behind your success. How so?

In order to be successful in the market, as I said, you have to be an independent thinker who bets against the consensus and is right. It’s so easy to be wrong. If you have quality collective decision-making with people who are willing to disagree well and work themselves through it well, you raise the probability of being right.

You stress in your book that one of the greatest tragedies is people persisting to hold opinions in their head that are wrong. Why is that a tragedy?

They don’t put them out to stress-test, and that causes them to make worse decisions. If people could be more open-minded and assertive at the same time, they can learn a lot. You can’t be attached to what you know. That’s the most important thing in my book. And also, to learn from painful mistakes.

On Active vs. Passive Investment Management…

[Active management is when a manager picks stocks or asset classes in an attempt to outperform the stock market, or the bond market or a combination of the two like 60/40. Passive management is a simple buy-and-hold approach. It is what the market gives you. Like buying-and-holding the S&P 500 Index, for example.]

What’s your take on the long-running debate about active vs. passive management and the move toward ETFs and other passive investments?

The question is: How much alpha can I buy by going to [a manager]? That alpha game is a zero-sum game. So don’t expect, on average, to get alpha because when somebody buys, somebody else has to sell. It’s like at a poker table: somebody will take money from somebody else — and there will be better players. There will always be smart people who will be able to make better decisions and pursue alpha. The challenge is to find them because those who are good at it are largely closed to new investors.

Debt and Demographics – Two Powerful Ds

The global economy continues to improve. Recession probability for the U.S. remains minimal in the next six to nine months. Europe’s economy is on better footing. Risks persist, including North Korea, a sharp slowdown in China, fiscal dysfunction in the U.S. (e.g., tax cuts, fiscal spend), and growing protectionist risks to global trade. Debt remains a significant headwind to growth as can be seen in this next chart.

Total Credit Market Debt-to-GDP

Here’s how to read the chart:

- The chart looks at a number of growth factors.

- For example, nominal GDP (before inflation is factored in) is lowest when Total Credit Market is above 318% Total Debt-to-GDP.

- The blue line tracks the Total Debt-to-GDP ratio over time.

- Note the upper dotted “high debt” line at 318%.

- The yellow highlights show the growth when in the high debt zone.

- Note how much better growth is when in the low debt zone. Also note that Total Debt-to-GDP peaked in late 2009 but remains high.

Source: Ned Davis Research

Also note the very last data box “Non-Financial Productivity.” Overall GDP growth comes from the total number of workers multiplied by their collective productivity. More workers producing more equals greater growth. With aging demographics (typically people moving into their lower spending years… they have a lot of stuff and kids out of the house) and fewer workers… you can see the pressure it can put on growth. And then with debt to be repaid, how much extra money is there to spend on things. Growth suffers.

Two Ds: Debt and Demographics are headwinds to growth. It is going to be hard for corporations to grow earnings much faster than GDP. Some will, of course, but in the aggregate, it’s a headwind and we are seeing it consistently in the low growth GDP stats. What we really need is Dedication, Determination, and Discipline. Let’s tell that to our representatives in Washington.

Hat tip to Ned Davis Research for the above chart. Amazing data. Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at 617-279-4876. John’s email address is [email protected]. I am not compensated in any way by NDR. I’m just a big fan of their work.

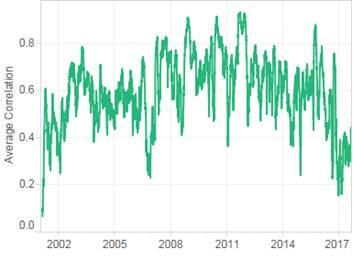

Just When They Said Active Management is Dead

Sector correlation is still low, alpha rising, by Phil Mackintosh & Rachel Liang

A lot of factors point to 2017 being a better year for stock pickers: Hedge fund returns are improved (as we’ve recently highlighted).

Active returns are also staging a comeback as even the SPIVA indexes have demonstrated.

It probably shouldn’t be surprising – 2017 has had markedly lower stock and sector (today’s chart) correlations. In fact the shift is really quite dramatic…and persistent. Read Macro+ETF Dashboard for more details.

Average Sector Correlations

It’s been a bit of a rough stretch for us active managers. This is some good news. Active is not dead.

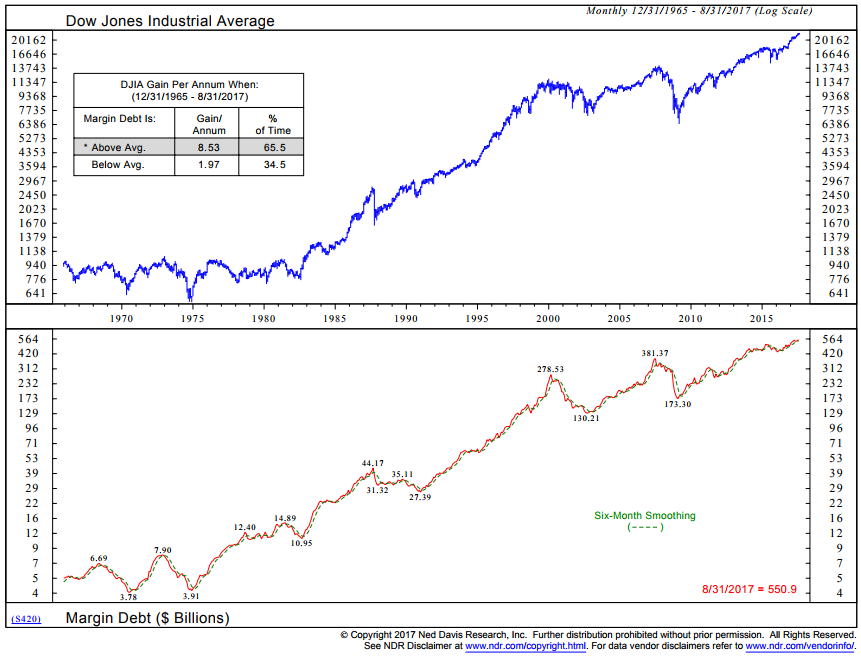

Trade Signals — A Look at Margin Debt and its Trend

S&P 500 Index — 2,497 (9-27-2017)

Notable this week:

The short-term gold signal moved to a sell this week. The intermediate term remains in a cyclical bull trend. I remain overall constructive on gold and the longer-term cyclical trend model remains bullish. No changes in the equity and fixed income trend indicators: bullish.

I like to take a look at the amount of margin debt in the system. Higher levels of leverage will elevate risk when selling pressure mounts. The following chart shows we are currently at record highs in margin debt. However, at this time, there’s more buying demand than selling pressure. Concerns increase when the current amount drops below its six-month moving average line (green dotted line below.) Note the signals given prior to the 2000 and 2008 corrections. Recall the margin calls and forced selling. When margin calls kick in, forced selling occurs and would-be buyers back away. Well, unless of course the central bankers step in. Interesting times. Anyway, worth keeping an eye on. Bottom line: this indicator remains bullish (see shaded box in upper left hand corner of chart.)

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note

Coach Lou Holtz said, “You need four things in your life, everybody needs something to do, everybody needs someone to love, everybody needs something to believe in… and everybody needs something to hope for.”

There are certain people with the gift to lead. What a great man. “And don’t tell people about your problems. 90% of people don’t care and the other 10% are glad you’ve got them.” Loved that line.

I have four rules for my kids and I try so hard to follow them myself. They come from a book called The Four Agreements by Don Miguel Ruiz.

- Rule #1: “Be absolutely impeccable with your word.”

- Rule #2: “Don’t make assumptions.”

- Rule #3: “Don’t take things personally.”

- Rule #4: “Give it your best.”

Some days your best is better than others. It is hard to give it your all when you’re not feeling well. But do give it the best you can on any given day. I loved how Coach Holtz put it. I’m not sure my kids have taken it all in over the years, but they’re grown now and I sure hope so. It took a long time for me to embrace rules two and three. Who doesn’t take things personally from time to time? So, I’m still working on those rules. My old man drilled rule number one into me and, most importantly, I watched him live his life that way.

Speaking of giving it one’s best, it’s been an emotional few years for the Penn State family. There are no excuses for the sins of recent past nor the lapse in leadership. But there is opportunity to step forward and do right and heal. And I think that is happening. Sport has a way of bringing people together and football, in many places, has become part of the glue that binds.

My pledge class brothers and I are getting together and tomorrow will find me wearing blue and white, holding a cold IPA, tailgating with great food and celebrating with my old college friends. A fun weekend ahead. The 4-0 Nittany Lions face Indiana and we’ve got a great kid named Saquon Barkley. He’s a great student and a truly wonderful human being. If you don’t have a team to root for this year, root with me.

Wishing you and your family a wonderful weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group