Investors don’t pay much attention to the monthly report in personal income and spending. We already have a good handle on income from the employment report. Unit auto sales and the retail sales data tell us a lot about consumer spending. However, while monthly spending figures are subject to revision, they are a direct input into the GDP calculations (and consumer spending accounts for about 69% of GDP). The personal income and spending report also include the PCE Price Index, which is the Fed’s inflationary benchmark for monetary policy. The August report confirmed a softer trend in consumer spending growth in 3Q17. The trend in core inflation moved further away from the Fed’s 2% goal.

Click here to enlarge

Excluding food and energy, the PCE Price Index rose 0.1% in the initial estimate for August. That’s not a big miss relative to the median forecast (+0.2%), but it resulted in a further decline in the year-over-year change (+1.3%). One alternative measure of core inflation excludes the largest monthly moves in prices each month. Fed Chair Yellen recently noted that this trimmed-mean PCE Price Index (prepared by the Dallas Fed) “shows less of a slowdown” in inflation this year. The August figures also showed a further downtrend in the year-over-year calculation (to 1.6% from 1.9% at the start of the year).

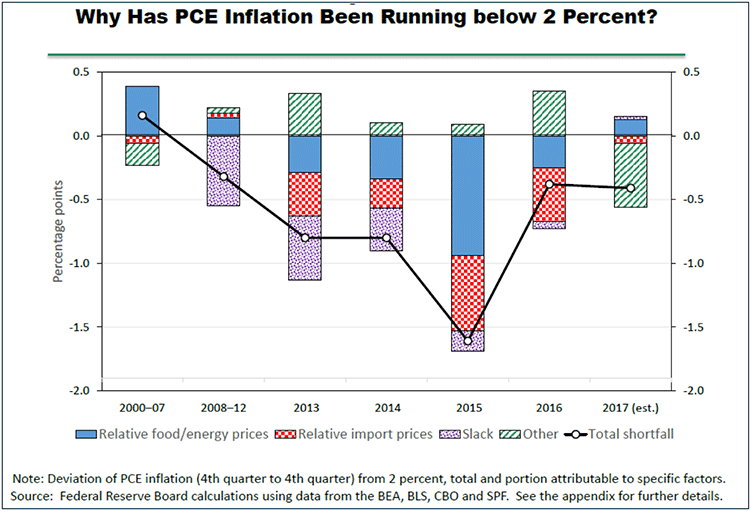

In her September 26 speech to the National Association for Business Economics, Yellen presented a graph of the decomposition of inflation relative to the Fed’s 2% goal. In the last two years, energy prices, import prices, and labor market slack put downward pressure on headline inflation. Those factors have all but disappeared. Energy prices have firmed. The dollar’s decline has lifted prices of imported supplies and raw materials. Wage pressures have remained moderate, but clearly the job market has grown tighter. The Atlanta Fed’s Wage Growth Tracker has picked up over the last year.

Click here to enlarge

The Fed’s decomposition of inflation also shows a shortfall this year that can’t be explained by energy prices, import prices, or economic slack. Some of this, according to Yellen, “reflects idiosyncratic shifts in the prices of some items, such as the large decline in telecommunication service prices seen earlier in the year, that are unlikely to be repeated.” Excluding these idiosyncratic factors, the Fed would be a lot closer to achieving its 2% inflation goal. Of course, the Fed could be wrong.

Meanwhile, while the personal income and spending figures for August were in line with expectations, the details imply a weaker trend in inflation-adjusted spending in the third quarter. Consumer spending accounts for about 69% of Gross Domestic Product, so we should see slower GDP growth. Inventory data through August suggest a possible unintentional buildup (the likely result of disappointing sales), which will add to GDP growth, but may take some time to work off. It’s not unusual for consumer spending growth to be uneven from quarter to quarter (as we saw clearly in the first half of the year) and the monthly figures are subject to revision. So, the 3Q17 slowdown is nothing to panic about, but it does bear watching closely.

The White House has unveiled its tax reform proposal, eight pages, vs. the previous one. Although, it’s more of a guideline than a plan and it’s more tax “cuts” than reform. Getting rid of deductions (which totaled $1.5 trillion in FY16) is extremely difficult. Lobbyists were reported to have been out in full force almost immediately after the announcement, with one of the loudest pushbacks coming against the proposal to eliminate the deduction for state and local taxes. Whatever the merits of the proposal, the mechanics of getting much done remain daunting.

In the meantime, the hurricanes are expected to cloud up much of the economic data in the near term. One should take any one piece of economic data with a grain of salt, but that will be especially so as we try to gauge the underlying strength of the economy over the next several weeks.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James