Chinks in the Armor and Its Implications for Asset Allocation

Indicators of market breadth are often useful in confirming or telegraphing important trend changes in equity markets. In simple terms, indicators of market breadth measure the level of participation of individual stocks in the general trend of the market. At bear market lows, almost all stocks have been going down and readings like the percent of stocks in up-trends and the percent of stocks making new lows hit extremes. At these junctures, an improvement in market breadth (read fewer stocks participating in the bear market) is often an early sign that the worst of the decline has passed. Conversely, market breadth indicators often start to deteriorate ahead of important intermediate and long-term highs even as the general trend in the market still appears to be strong. Large divergences between market breadth and stock prices is an early warning sign to market participants that all may not be well underneath the surface.

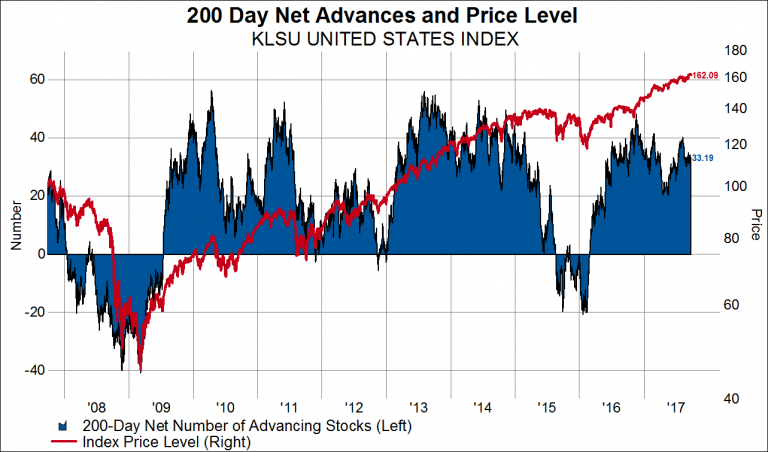

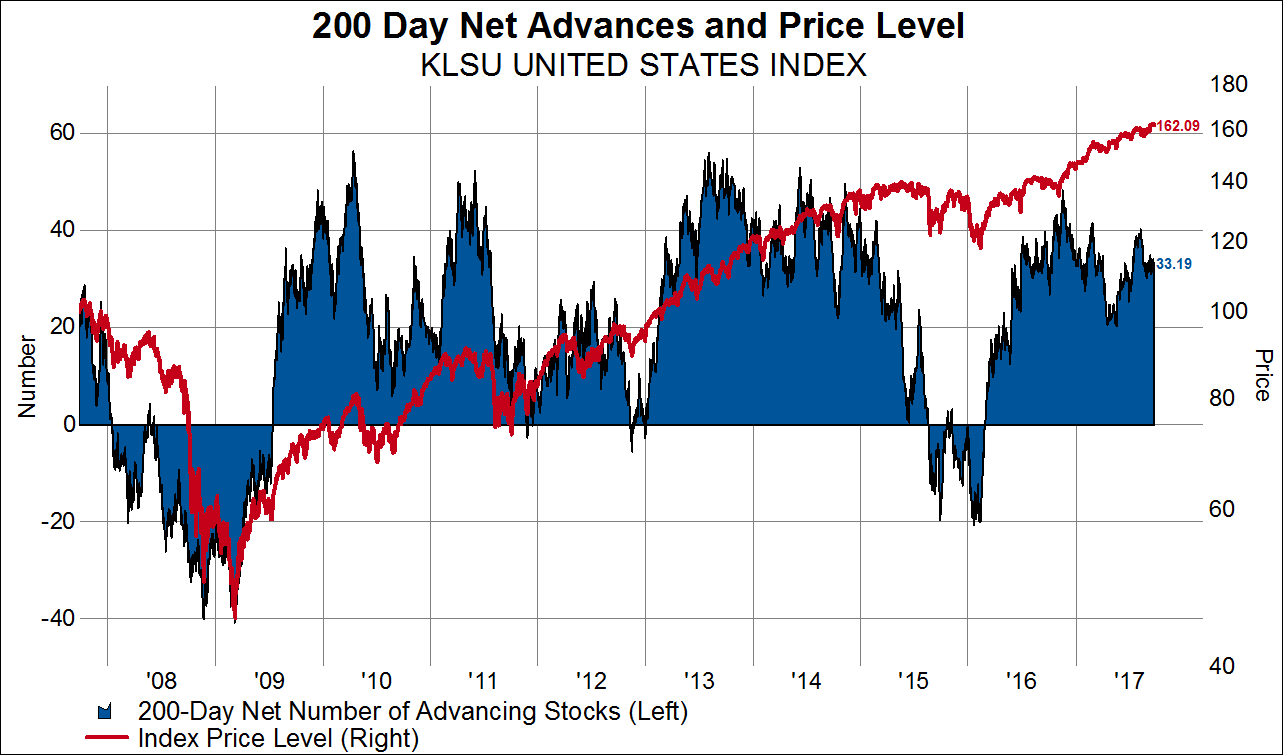

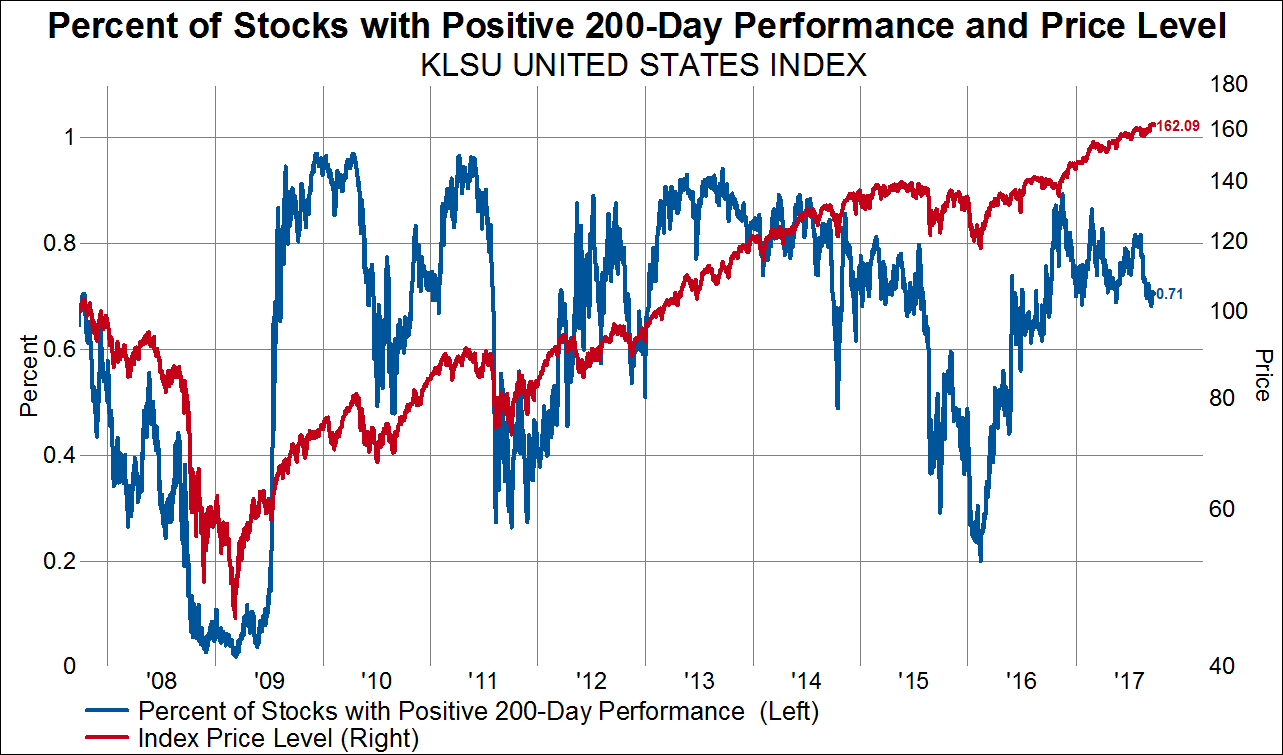

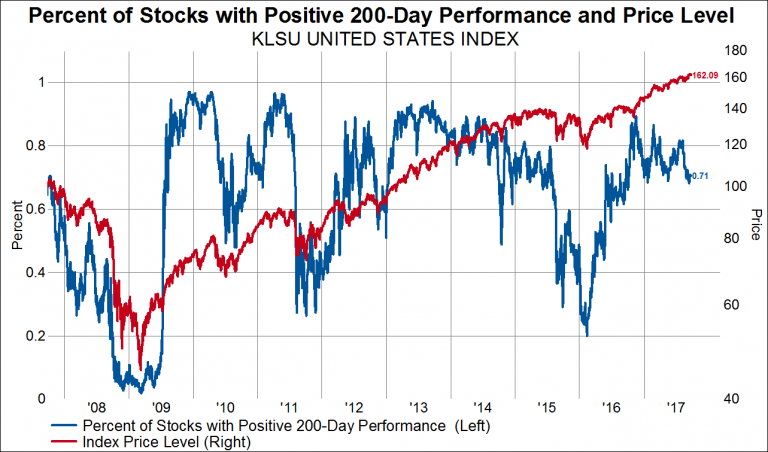

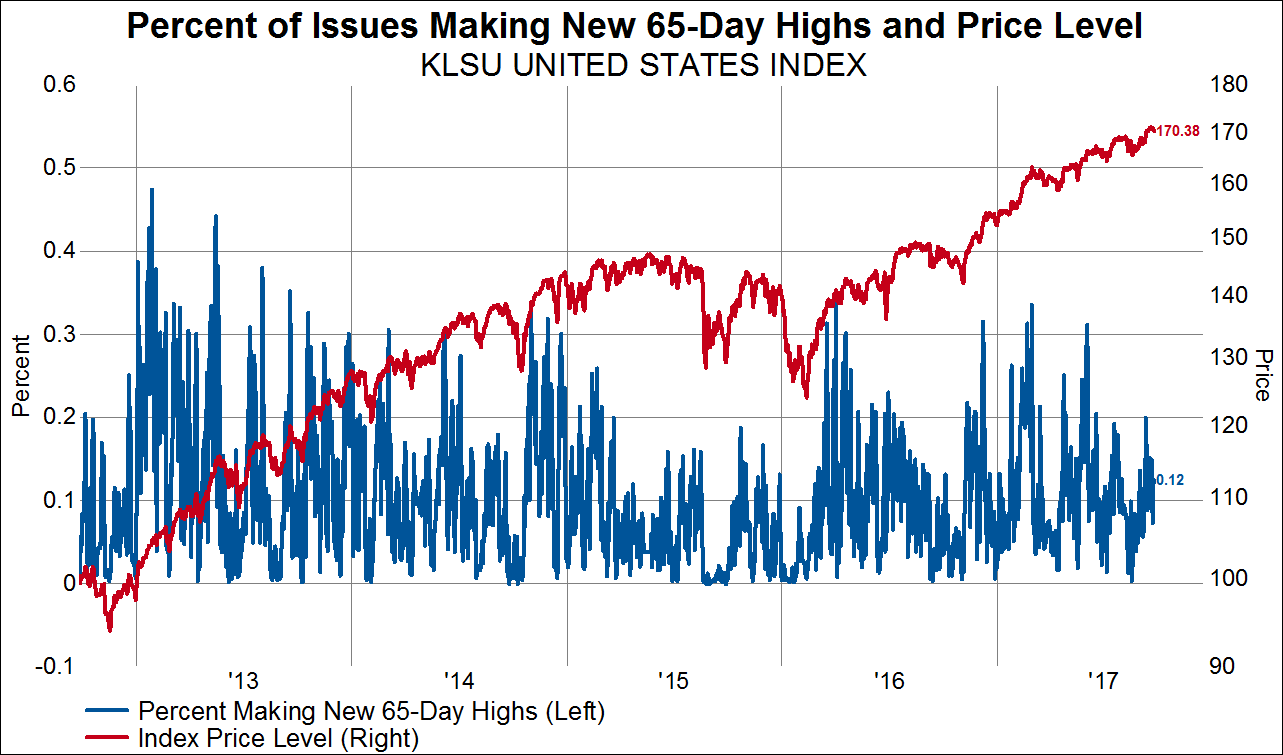

This brings us to the topic du jour, which is that we are taking note of an early deterioration in some of our most useful market breadth indicators even as the stock market continues to make new highs. That is to say, the stock indexes are making new highs, but the number of stocks participating in that trend is waning. In each of the charts below the market breadth indicator is marked by the blue line plotted on the left axis and the price level index is marked by the red line plotted on the right axis. For this post we’ll focus just on stocks in our United States index, which covers the largest 85% of companies and is a near replica of the MSCI USA index.

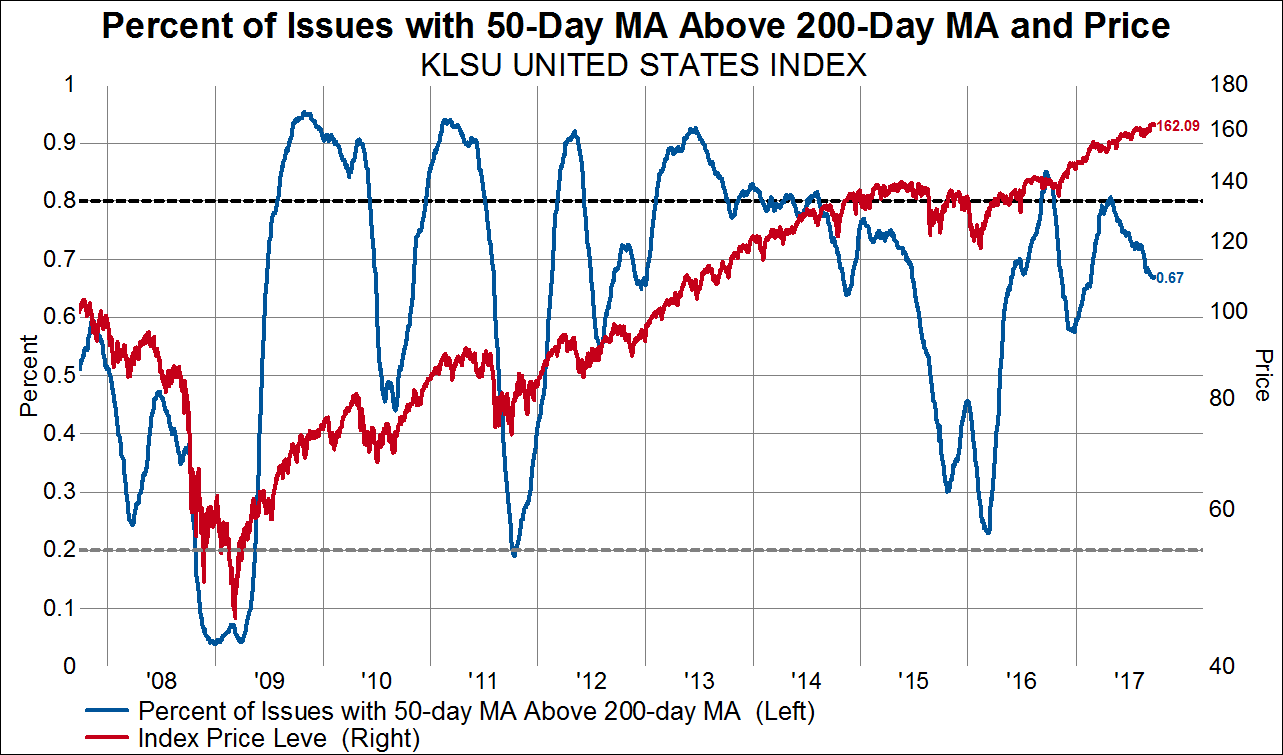

In this first chart we show the percent of stocks with their 50-day moving average price above their 200-day moving average price overlaid on the price level of our United States index. This is a blunt tool to measure the percent of stocks that are in an up-trend. As readers can see, our breadth indicator has been deteriorating for some time even as the overall market has been grinding higher. Similar patterns were seen before market declines in 2010, 2011, 2012 and 2015.

This next chart shows the net number advancing stocks over the last 200 days overlaid on the price level index. The number of net advancing stocks is simply the number of stocks trading higher now compared to 200 days ago minus the number of stocks trading lower now compared to 200 days ago. It peaked at the end of 2016 even as the market has marched higher so far through 2017. This indicator peaked before declines in 2010, 2011 and 2015.